Deck 6: Income Statement and Statement of Changes in Equity

Full screen (f)

Question

Question

The following are the transactions for Tara's T-Shirts,a sole trader clothing retailer,for the month of January of the current year.Tara uses the perpetual inventory system.Ignore GST.All transactions are on credit unless otherwise stated.

Additional information:

Additional information:

• The ending stocktake (count)is $42,300.

• Rates are estimated to be $2,100 for the year.

• Commission is for work which is only 25% completed.

• A provision of 5% for doubtful debts is to be made.

• Depreciation on the buildings is to be at 3% per annum straight line (1 month).

• Depreciation on equipment is to be at 25% per annum diminishing value (1 month).

Using the data above,complete an accounting equation worksheet using the format given in Smart,Awan & Baxter,p.163.Show the final calculation of A = L + OE.

Principles of Accounting 5th Edition Chapter 6 Example examination questions

© Pearson 2014 PAGE 13

Additional information:• The ending stocktake (count)is $42,300.

• Rates are estimated to be $2,100 for the year.

• Commission is for work which is only 25% completed.

• A provision of 5% for doubtful debts is to be made.

• Depreciation on the buildings is to be at 3% per annum straight line (1 month).

• Depreciation on equipment is to be at 25% per annum diminishing value (1 month).

Using the data above,complete an accounting equation worksheet using the format given in Smart,Awan & Baxter,p.163.Show the final calculation of A = L + OE.

Principles of Accounting 5th Edition Chapter 6 Example examination questions

© Pearson 2014 PAGE 13

Question

Question

Question

Question

Question

Question

Question

Question

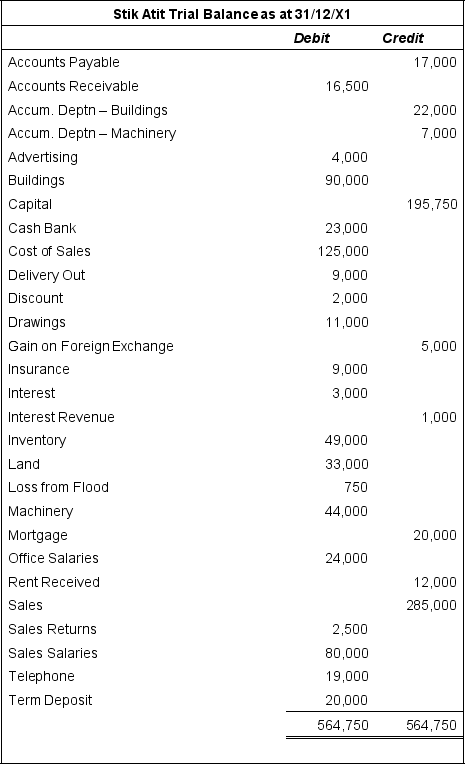

The following information is available at balance date of 31/12/X1;ignore GST:

1.Bad debts to be written off are $4,500.

1.Bad debts to be written off are $4,500.

2.Buildings depreciation rate is 2% straight line for the whole year.

3.Machinery depreciation rate is 20% diminishing value for the whole year.

4.Insurance was commenced and paid on 1 April 20X1 for a whole year.

5.The last rent received was for 3 months in advance on 1/11/X1;rent is $1,000 per month.

6.The term deposit interest rate is 10%;interest was last received on 30/06/X1 to cover up to and including that date.

7.Sales salaries are $8,000 per month;they were last paid on 31/10/X1 to cover up to that date.

State the names of accounts affected by these adjustments,the type of account,whether the account increases or decreases,the adjustment amount,and any necessary calculation.

Below is an example of how to set out your

1.Bad debts to be written off are $4,500.2.Buildings depreciation rate is 2% straight line for the whole year.

3.Machinery depreciation rate is 20% diminishing value for the whole year.

4.Insurance was commenced and paid on 1 April 20X1 for a whole year.

5.The last rent received was for 3 months in advance on 1/11/X1;rent is $1,000 per month.

6.The term deposit interest rate is 10%;interest was last received on 30/06/X1 to cover up to and including that date.

7.Sales salaries are $8,000 per month;they were last paid on 31/10/X1 to cover up to that date.

State the names of accounts affected by these adjustments,the type of account,whether the account increases or decreases,the adjustment amount,and any necessary calculation.

Below is an example of how to set out your

Question

Craig Smith purchased a retail sports clothing business on 1 April.He purchased the business for $160,000.The assets and liabilities taken over were as follows:

The following transactions (events)took place during the month of April:

The following transactions (events)took place during the month of April:

• Craig invested $10,000 cash into the business.

• He purchased stock for $7,500 on credit from I Supply Ltd.

• Paid rent $900 and advertising $1,200.

• Sold inventory for $3,900 on credit (cost price was $1,350).

• Purchased a business motor vehicle for $25,000,paying a $2,500 deposit and agreeing to pay the balance over 24 months under a hire purchase agreement with A Finance Co.

• Paid wages to staff $500 and paid Craig's personal household expenses of $400.

• Sold inventory receiving cash $2,200 (cost price $750).

• A customer returned goods purchased on credit for $360 (cost price was $150).

• Craig took sports clothing for personal use (cost price $250).

• Received $1,000 from a customer paying off her account.She had deducted $50 discount before making this payment.

• Equipment was sold for $250,on credit.This had originally cost $400.

Show the effect of the opening assets and liabilities taken over,and the remaining transactions (events)on the accounting equation.

The following transactions (events)took place during the month of April:• Craig invested $10,000 cash into the business.

• He purchased stock for $7,500 on credit from I Supply Ltd.

• Paid rent $900 and advertising $1,200.

• Sold inventory for $3,900 on credit (cost price was $1,350).

• Purchased a business motor vehicle for $25,000,paying a $2,500 deposit and agreeing to pay the balance over 24 months under a hire purchase agreement with A Finance Co.

• Paid wages to staff $500 and paid Craig's personal household expenses of $400.

• Sold inventory receiving cash $2,200 (cost price $750).

• A customer returned goods purchased on credit for $360 (cost price was $150).

• Craig took sports clothing for personal use (cost price $250).

• Received $1,000 from a customer paying off her account.She had deducted $50 discount before making this payment.

• Equipment was sold for $250,on credit.This had originally cost $400.

Show the effect of the opening assets and liabilities taken over,and the remaining transactions (events)on the accounting equation.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/20

Play

Full screen (f)

Deck 6: Income Statement and Statement of Changes in Equity

1

Other comprehensive income items:

A are realised items that arise from extraordinary transactions of the business

B are required to be shown by large public-type companies

C are required to be shown by small sole trader enterprises

D are unrealised gains,but not unrealised losses

A are realised items that arise from extraordinary transactions of the business

B are required to be shown by large public-type companies

C are required to be shown by small sole trader enterprises

D are unrealised gains,but not unrealised losses

B

2

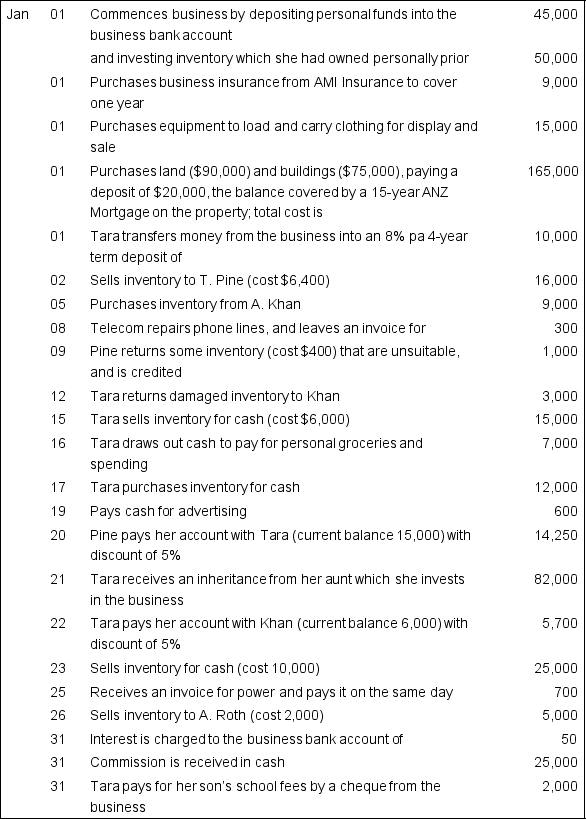

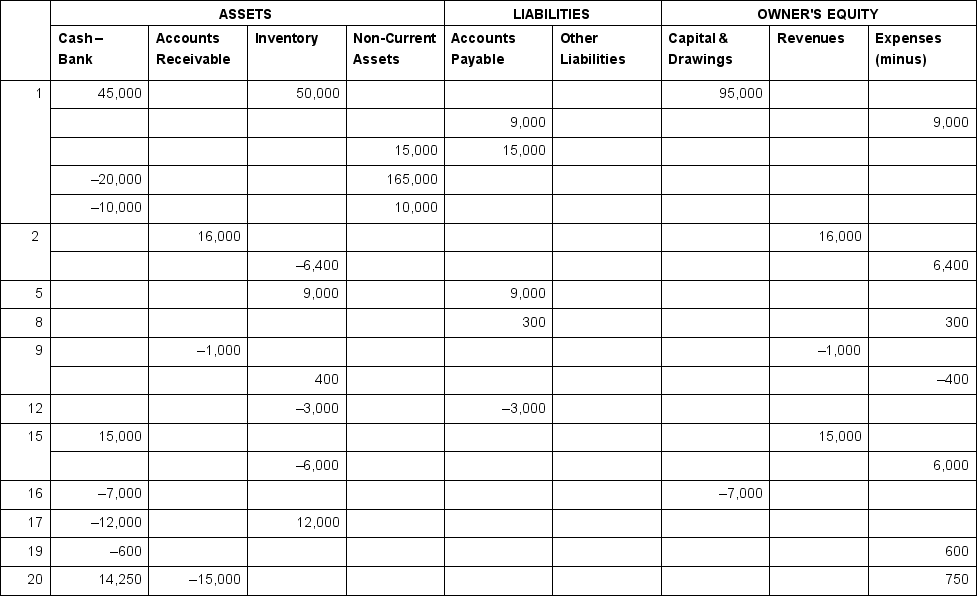

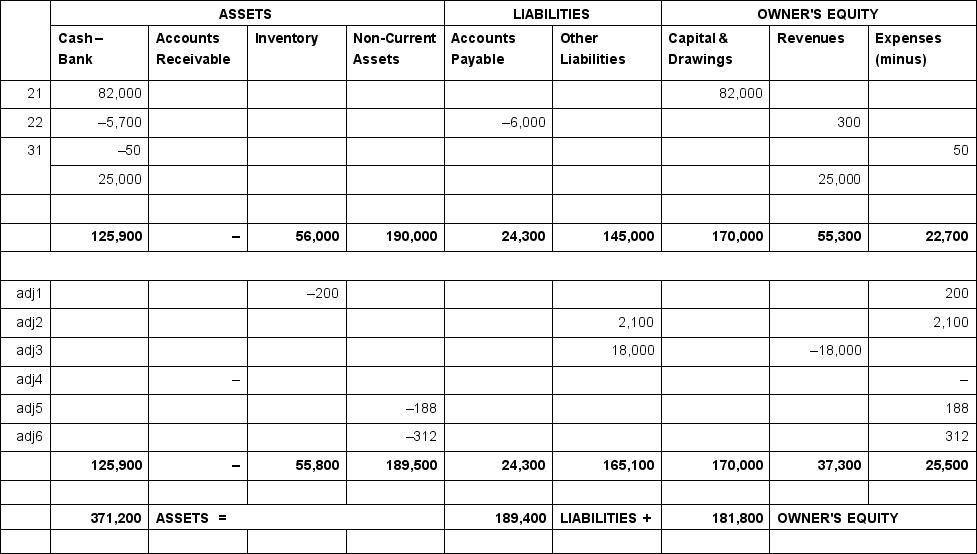

The following are the transactions for Tara's T-Shirts,a sole trader clothing retailer,for the month of January of the current year.Tara uses the perpetual inventory system.Ignore GST.All transactions are on credit unless otherwise stated.

Additional information:

• The ending stocktake (count)is $42,300.

• Rates are estimated to be $2,100 for the year.

• Commission is for work which is only 25% completed.

• A provision of 5% for doubtful debts is to be made.

• Depreciation on the buildings is to be at 3% per annum straight line (1 month).

• Depreciation on equipment is to be at 25% per annum diminishing value (1 month).

Using the data above,complete an accounting equation worksheet using the format given in Smart,Awan & Baxter,p.163.Show the final calculation of A = L + OE.

Principles of Accounting 5th Edition Chapter 6 Example examination questions

© Pearson 2014 PAGE 13

Additional information:• The ending stocktake (count)is $42,300.

• Rates are estimated to be $2,100 for the year.

• Commission is for work which is only 25% completed.

• A provision of 5% for doubtful debts is to be made.

• Depreciation on the buildings is to be at 3% per annum straight line (1 month).

• Depreciation on equipment is to be at 25% per annum diminishing value (1 month).

Using the data above,complete an accounting equation worksheet using the format given in Smart,Awan & Baxter,p.163.Show the final calculation of A = L + OE.

Principles of Accounting 5th Edition Chapter 6 Example examination questions

© Pearson 2014 PAGE 13

Tara's T-Shirts - accounting equation

continues over page

continues over page

Principles of Accounting 5th Edition Chapter 6 Example examination questions

Principles of Accounting 5th Edition Chapter 6 Example examination questions

© Pearson 2014 PAGE 15

continues over page Principles of Accounting 5th Edition Chapter 6 Example examination questions© Pearson 2014 PAGE 15

3

Which of the following defines General and administration expenses?

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

C

4

Select the true statement:

A Revenue expenditure is added to the cost of an asset and depreciated

B Capital expenditure includes costs of repairs after the asset is installed and first used

C Revenue expenditure provides benefits over several accounting periods

D Capital expenditure includes expenses to get the asset into location and ready for use

A Revenue expenditure is added to the cost of an asset and depreciated

B Capital expenditure includes costs of repairs after the asset is installed and first used

C Revenue expenditure provides benefits over several accounting periods

D Capital expenditure includes expenses to get the asset into location and ready for use

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

5

Distinguish between cash basis accounting and accrual basis accounting,by listing the types of transactions that each records and/or does not record.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

6

Explain why accrual accounting is the preferred accounting method,including in your explanation the terms 'accounting period' and 'matching principle'.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

7

Explain the 3 aspects of the NZ Framework definition of income,and relate each aspect to examples of practical recording of business transactions.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following defines Financial expenses?

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

9

Your friend Randolph has been reading about the collapse of Enron in the USA,and has asked about the meaning of the terms 'capital expenditure' and 'revenue expenditure'.

Explain how capital expenditure and revenue expenditure are different,and why it is important to differentiate between them,particularly in regard to their effect on financial statements.

Explain how capital expenditure and revenue expenditure are different,and why it is important to differentiate between them,particularly in regard to their effect on financial statements.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

10

The following information is available at balance date of 31/12/X1;ignore GST:

1.Bad debts to be written off are $4,500.

2.Buildings depreciation rate is 2% straight line for the whole year.

3.Machinery depreciation rate is 20% diminishing value for the whole year.

4.Insurance was commenced and paid on 1 April 20X1 for a whole year.

5.The last rent received was for 3 months in advance on 1/11/X1;rent is $1,000 per month.

6.The term deposit interest rate is 10%;interest was last received on 30/06/X1 to cover up to and including that date.

7.Sales salaries are $8,000 per month;they were last paid on 31/10/X1 to cover up to that date.

State the names of accounts affected by these adjustments,the type of account,whether the account increases or decreases,the adjustment amount,and any necessary calculation.

Below is an example of how to set out your

1.Bad debts to be written off are $4,500.2.Buildings depreciation rate is 2% straight line for the whole year.

3.Machinery depreciation rate is 20% diminishing value for the whole year.

4.Insurance was commenced and paid on 1 April 20X1 for a whole year.

5.The last rent received was for 3 months in advance on 1/11/X1;rent is $1,000 per month.

6.The term deposit interest rate is 10%;interest was last received on 30/06/X1 to cover up to and including that date.

7.Sales salaries are $8,000 per month;they were last paid on 31/10/X1 to cover up to that date.

State the names of accounts affected by these adjustments,the type of account,whether the account increases or decreases,the adjustment amount,and any necessary calculation.

Below is an example of how to set out your

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

11

Craig Smith purchased a retail sports clothing business on 1 April.He purchased the business for $160,000.The assets and liabilities taken over were as follows:

The following transactions (events)took place during the month of April:

• Craig invested $10,000 cash into the business.

• He purchased stock for $7,500 on credit from I Supply Ltd.

• Paid rent $900 and advertising $1,200.

• Sold inventory for $3,900 on credit (cost price was $1,350).

• Purchased a business motor vehicle for $25,000,paying a $2,500 deposit and agreeing to pay the balance over 24 months under a hire purchase agreement with A Finance Co.

• Paid wages to staff $500 and paid Craig's personal household expenses of $400.

• Sold inventory receiving cash $2,200 (cost price $750).

• A customer returned goods purchased on credit for $360 (cost price was $150).

• Craig took sports clothing for personal use (cost price $250).

• Received $1,000 from a customer paying off her account.She had deducted $50 discount before making this payment.

• Equipment was sold for $250,on credit.This had originally cost $400.

Show the effect of the opening assets and liabilities taken over,and the remaining transactions (events)on the accounting equation.

The following transactions (events)took place during the month of April:• Craig invested $10,000 cash into the business.

• He purchased stock for $7,500 on credit from I Supply Ltd.

• Paid rent $900 and advertising $1,200.

• Sold inventory for $3,900 on credit (cost price was $1,350).

• Purchased a business motor vehicle for $25,000,paying a $2,500 deposit and agreeing to pay the balance over 24 months under a hire purchase agreement with A Finance Co.

• Paid wages to staff $500 and paid Craig's personal household expenses of $400.

• Sold inventory receiving cash $2,200 (cost price $750).

• A customer returned goods purchased on credit for $360 (cost price was $150).

• Craig took sports clothing for personal use (cost price $250).

• Received $1,000 from a customer paying off her account.She had deducted $50 discount before making this payment.

• Equipment was sold for $250,on credit.This had originally cost $400.

Show the effect of the opening assets and liabilities taken over,and the remaining transactions (events)on the accounting equation.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

12

a What advantages are there in showing classifications and sub-classifications of items in the Income Statement?

b Why does NZ IAS 1 recommend that an entity use a consistent format in presenting its financial statements?

b Why does NZ IAS 1 recommend that an entity use a consistent format in presenting its financial statements?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

13

What names are acceptable for the statement describing financial performance?

A Income Statement

B Comprehensive Income Statement

C Profit and Loss Statement

D NZ IAS 1 recommends Comprehensive Income Statement but allows for alternative names to be used

A Income Statement

B Comprehensive Income Statement

C Profit and Loss Statement

D NZ IAS 1 recommends Comprehensive Income Statement but allows for alternative names to be used

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

14

Recording an item as capital expenditure instead of revenue expenditure will result in:

A higher recorded net profit and lower recorded net assets

B lower recorded net profit and higher recorded net assets

C lower recorded net profit and lower recorded net assets

D higher recorded net profit and higher recorded net assets

A higher recorded net profit and lower recorded net assets

B lower recorded net profit and higher recorded net assets

C lower recorded net profit and lower recorded net assets

D higher recorded net profit and higher recorded net assets

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following items would be considered as capital expenditure?

A Power used during the current month

B Purchase cost of property,plant or equipment

C Minor repairs to a 2-year-old vehicle

D Regular 6-monthly oil changes on a vehicle

A Power used during the current month

B Purchase cost of property,plant or equipment

C Minor repairs to a 2-year-old vehicle

D Regular 6-monthly oil changes on a vehicle

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

16

Low immaterial-cost items that will benefit several accounting periods:

A are recorded as an asset and depreciated over their useful life

B are recorded as expenses instead of assets,as they are not material amounts

C are matched with income over several accounting periods

D are added to the overall cost of property,plant and equipment

A are recorded as an asset and depreciated over their useful life

B are recorded as expenses instead of assets,as they are not material amounts

C are matched with income over several accounting periods

D are added to the overall cost of property,plant and equipment

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following defines Cost of goods sold expenses?

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following defines Selling and distribution expenses?

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

A Costs incurred in getting goods ready for sale,including purchase cost

B Costs associated with selling the goods or services of the business

C Costs of running the office functions and other costs that do not fit in any other category

D Costs associated with borrowing money to operate the business,as well as costs to provide credit to customers,bad debts and discount

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

19

Why is the Income Statement important?

A Investors may use it to determine if the business is earning a satisfactory return on assets employed

B Suppliers and creditors may use it to assess whether the business is generating enough income in order to pay its suppliers and other creditors

C Net income or net loss may be used as a measure to assess the business's success or failure

D All of the above

A Investors may use it to determine if the business is earning a satisfactory return on assets employed

B Suppliers and creditors may use it to assess whether the business is generating enough income in order to pay its suppliers and other creditors

C Net income or net loss may be used as a measure to assess the business's success or failure

D All of the above

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

20

For an item to be recorded as a provision,there must be:

A a present obligation and a probable outflow of economic resources

B a future obligation and a possible outflow of economic resources

C a present obligation and a possible outflow of economic resources

D a future obligation and a probable outflow of economic resources

A a present obligation and a probable outflow of economic resources

B a future obligation and a possible outflow of economic resources

C a present obligation and a possible outflow of economic resources

D a future obligation and a probable outflow of economic resources

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 20 flashcards in this deck.