Deck 11: Sole Proprietorships and Flow-Through Entities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

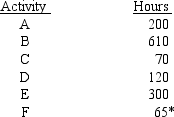

Willy is involved in a number of businesses as a consultant. Below are the businesses and the hours of activity that Willy spent in each. Identify any activities that are passive and explain why the income or loss from the other activities is not passive income or loss.  *F is Willy's sole proprietorship and he has no employees.

*F is Willy's sole proprietorship and he has no employees.

*F is Willy's sole proprietorship and he has no employees. Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/133

Play

Full screen (f)

Deck 11: Sole Proprietorships and Flow-Through Entities

1

The income from a general partnership is passive income to all partners..

False

2

An S corporation shareholder can only deduct losses of the S corporation to the extent he or she has positive stock basis.

False

3

Recourse debts can only be satisfied with the property used as collateral.

False

4

The AAA of the S corporation is a corporate-level account.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

5

A sole proprietorship must use the cash method of accounting.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

6

Limited liability companies are generally taxed as partnerships unless the company elects to be taxed as a corporation.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

7

The entity concept of a partnership views the partnership as separate from the partners and permits certain transactions between the partner and the partnership.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

8

Partners pay taxes on their share of all the partnership net income annually.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

9

Once established at entry, a partner's basis account does not change.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

10

A general partner in a limited partnership is not protected from the partnership's liabilities.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

11

A sole proprietor is considered a self-employed individual.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

12

A loss is never recognized on a nonliquidating distribution from a partnership.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

13

A limited liability company that has only one member must be taxed as a sole proprietorship.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

14

Only 50 percent or more of the shareholders of an S corporation must consent to the S election.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

15

The limited liability partnership form of business offers partners protection from all partnership debts.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

16

A limited partnership must have a general partner.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

17

A flow-through entity aggregates all its income and subtracts all expense items for reporting its net income.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

18

The owners of a limited liability company are called members.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

19

S corporations never pay any income taxes.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

20

The basis limitation rules are applied before the at-risk and passive loss limitation rules.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

21

Active participation requires a higher level of activity than material participation.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

22

A person satisfies material participation requirements only through current activity.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

23

What is the difference between a limited partnership and a general partnership?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

24

How does a partner establish that his current activity meets the material participation requirements?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

25

How are income and loss apportioned to S corporation shareholders for taxation?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

26

How is an S election terminated?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

27

What is required for a taxpayer to actively participate in a rental property activity to qualify for a limited deduction of losses?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

28

Briefly explain the four loss limitation rules applicable to partners.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

29

What is a sole proprietorship and how is this business entity taxed?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

30

When may a partner recognize gain on a nonliquidating distribution from the partnership?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

31

There are special rules for an S corporation that must be followed when the corporation decides to liquidate that differs from the rules for C corporations.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

32

Why are partnerships and S corporations called flow-through entities?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

33

How does a shareholder's basis in his or her S corporation stock change?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

34

What taxes may be assessed an S corporation?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

35

What tax year end must a partnership use?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

36

Briefly explain the difference between the entity and the aggregate concepts as related to partnership taxation.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

37

Wilhelmina operates a daycare center in her home as a sole proprietorship. She has gross revenues of $15,000 and the following expenses:

Cost of food $1,200; allocated costs of using the home $900; allowable depreciation $500; reasonable salary for her 16 year old daughter for after-school help $3,000.

a. Determine Wilhelmina's net income from the sole proprietorship in 2018.

b. Determine Wilhelmina's total of self-employment and income taxes on this activity if her marginal tax rate is 24 percent.

Cost of food $1,200; allocated costs of using the home $900; allowable depreciation $500; reasonable salary for her 16 year old daughter for after-school help $3,000.

a. Determine Wilhelmina's net income from the sole proprietorship in 2018.

b. Determine Wilhelmina's total of self-employment and income taxes on this activity if her marginal tax rate is 24 percent.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

38

What is the difference between recourse and nonrecourse debt for a partnership?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

39

What restrictions are placed on an S corporation to be able to make a valid S election?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

40

What kind of an entity is a limited liability company for the purpose of taxing its income?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

41

Klinger's AGI is $130,000 before the loss of $29,000 from a rental complex he owns and in which he actively participates. What is his AGI after this loss?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

42

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Operating income taxed to entity.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Operating income taxed to entity.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

43

Sue is a 50 percent working partner in a partnership. She is guaranteed an annual salary of $60,000. Jim, the other 50 percent partner, is to receive the first $10,000 of partnership profits before the balance is divided equally between them. During the year, the partnership's accounting results were $40,000 of income before any partner allocations. What amount of income will Sue be taxed on?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

44

Simpco, an S corporation, has gross operating revenue of $450,000, cost of sales of $150,000, salaries and FICA taxes for employees of $40,000, a $25,000 Section 179 expense deduction, $10,000 of other depreciation, interest income of $2,000, a $4,000 capital loss, and a $500 charitable contribution deduction. What are the corporation's net income and its separately stated items?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

45

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Distributions from entity are generally tax-free. (Assume the S corporation shareholder has stock basis and partner has partnership or debt basis.)

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Distributions from entity are generally tax-free. (Assume the S corporation shareholder has stock basis and partner has partnership or debt basis.)

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

46

Candi purchased a 10 percent limited partnership interest in rental property for $30,000. The partnership has a $1,300,000 mortgage that is secured by the building. During the current year, the partnership reports a total loss of $200,000 from the rental building. What is Candi's deductible loss and the amount of her loss carryover if her only other income/loss items are $50,000 in salary, an $8,000 capital loss on some stock, and $5,000 of bond interest income?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

47

The Walden Partnership has two 20 percent general partners and six 10 percent limited partners. During the current year, the partnership paid off $50,000 of notes payable, purchased machinery for $100,000 on a nonrecourse note, borrowed $20,000 for working capital, and had $80,000 income from operations. If the general partners each had a basis of $30,000 in their partnership interests at the beginning of the year, what is each general partner's year-end basis?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

48

A and B are equal shareholders in AB, a calendar-year S corporation. On June 30 (181 days into the year), A sells one-half of her stock to C. The corporation reports $30,000 of income for the year. How much of this income is allocated to A, B, and C?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

49

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owners pay self-employment taxes on income from entity.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owners pay self-employment taxes on income from entity.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

50

The Clio Corporation, an S corporation, makes a nonliquidating distribution of $10,000 cash and property (fair market value = $10,000; basis = $7,000) to James, a 50 percent shareholder. What are the effects of these distributions on Clio and James's incomes, Clio's AAA account, and James's basis in his stock?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

51

The LBJ Partnership has a March 31 year-end. It has three equal partners, L with a June 30 year-end, B with a January 31 year-end, and J with a December 31 year-end. What are the year-end dates for the tax returns of the partners that will include their shares of the partnership's income as of March 31, 2018?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

52

Simpco Partnership has gross operating revenue of $450,000, cost of sales of $150,000, salaries to employees of $40,000, a $25,000 Section 179 expense deduction, $10,000 of other depreciation, interest income of $2,000, a $4,000 capital loss, and a $500 charitable contribution deduction. What are the partnership's bottom line net income and its separately stated items?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

53

Clarence receives a liquidating distribution of receivables (fair market value and basis both equal $20,000) and land (fair market value = $25,000 and basis = $18,000) for his partnership interest with a $70,000 basis in a liquidating distribution. What is Clarence's realized and recognized gain or loss on this distribution and his basis in the property received?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

54

Simpco Partnership has gross operating revenue of $450,000, cost of sales of $150,000, salaries to employees of $40,000, a $25,000 Section 179 expense deduction, $10,000 of other depreciation, interest income of $2,000, a $4,000 capital loss, and a $500 charitable contribution deduction. Simpson is a 20 percent partner in Simpco Partnership. He has a $60,000 basis in his partnership interest at the end of the year after all income/loss items have been passed through to him. What was his beginning-of-the-year basis in his partnership interest?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

55

Willy is involved in a number of businesses as a consultant. Below are the businesses and the hours of activity that Willy spent in each. Identify any activities that are passive and explain why the income or loss from the other activities is not passive income or loss. *F is Willy's sole proprietorship and he has no employees.

*F is Willy's sole proprietorship and he has no employees. Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

56

ABC Partnership has two assets: inventory (fair market value = $20,000; basis = $25,000) and land (fair market value = $100,000; basis = $50,000) when Janine sells her 40 percent interest in ABC with a $30,000 basis for $48,000. What is the amount and type of Janine's gain or loss on the sale of her partnership interest?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

57

For 2018, compare the income and FICA or self-employment tax burdens only for a couple in the 35 percent marginal income tax bracket who jointly own a business with $120,000 of operating income, if the business is a partnership or if it is an S corporation. The husband and wife each take $50,000 out of the business as salary.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

58

For 2018, compare the income and FICA or self-employment tax burdens only of an individual in the 24 percent marginal income tax bracket who owns a business that has operating income of $50,000 if the business is (a) an S corporation or (b) a sole proprietorship. The owner takes $30,000 out of the business as a salary.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

59

The Walden Partnership has two 20 percent general partners and six 10 percent limited partners. During the current year, the partnership paid off $50,000 of notes payable, purchased machinery for $100,000 on a nonrecourse note, borrowed $20,000 for working capital, and had $80,000 income from operations. If one of the limited partners had a $10,000 basis at the beginning of the year, what is his year-end basis?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

60

Quincy received a liquidating distribution of $5,000 cash and inventory valued at $10,000 with a basis of $6,000 for his partnership interest with a basis of $20,000. What is Quincy's basis in the inventory? Does Quincy recognize any gain or loss on this distribution?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

61

Manuel purchased a 30% interest in MAC general partnership for $40,000 cash and materially participated in the partnership for the entire year. The partnership had $50,000 in liabilities when Manuel purchased his interest and the liabilities increased $10,000 during the year. If the partnership incurred a $300,000 loss this year, how much of this loss can Manuel deduct?

A) 0

B) $40,000

C) $58,000

D) $65,000

A) 0

B) $40,000

C) $58,000

D) $65,000

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

62

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Loss recognized on entity liquidation.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Loss recognized on entity liquidation.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following is not a characteristic of a partnership?

A) Must be formed under state law

B) Formation is generally tax free except for services received for a partnership interest

C) Distributions of entity income are tax-free

D) Loss is never recognized on a nonliquidating distribution

A) Must be formed under state law

B) Formation is generally tax free except for services received for a partnership interest

C) Distributions of entity income are tax-free

D) Loss is never recognized on a nonliquidating distribution

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

64

Samantha and Ashley form the MAS General Partnership. Samantha contributed $20,000 cash in exchange for her 50 percent partnership interest. During the first year of partnership operations, the partnership reported net taxable income of $10,000, Samantha withdrew $8,000 cash from the partnership, and the partnership took out an $18,000 loan on the last day of the year. Samantha's adjusted basis for her partnership interest at year end is:

A) $38,000

B) $30,000

C) $26,000

D) $17,000

A) $38,000

B) $30,000

C) $26,000

D) $17,000

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

65

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owner's salary is subject to FICA taxes.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owner's salary is subject to FICA taxes.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

66

A sole proprietorship:

A) must be owned by an individual.

B) provides basic liability protection for the owner.

C) must use the cash method of accounting.

D) can pay the owner a salary.

A) must be owned by an individual.

B) provides basic liability protection for the owner.

C) must use the cash method of accounting.

D) can pay the owner a salary.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

67

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owner may deduct losses if there is basis because of loans to the entity by the owner.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owner may deduct losses if there is basis because of loans to the entity by the owner.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is not a separately stated item on a partnership's Schedule K?

A) A $5,000 long-term capital loss

B) $20,000 of Section 1245 recapture

C) $3,000 charitable contribution

D) $5,000 bond interest income

A) A $5,000 long-term capital loss

B) $20,000 of Section 1245 recapture

C) $3,000 charitable contribution

D) $5,000 bond interest income

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

69

A sole proprietor:

A) deducts his or her retirement plan contributions from business income.

B) may not pay a salary to a related party who works in the business.

C) deducts employee fringe benefit costs from business income.

D) files a separate tax return for business income.

A) deducts his or her retirement plan contributions from business income.

B) may not pay a salary to a related party who works in the business.

C) deducts employee fringe benefit costs from business income.

D) files a separate tax return for business income.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following is not a characteristic of a partnership?

A) Must meet 80 percent control requirement for formation to be tax free

B) Cash distributions to partners may be taxable

C) Loss is only recognized on liquidating distributions

D) General partners' salaries are subject to FICA taxes.

A) Must meet 80 percent control requirement for formation to be tax free

B) Cash distributions to partners may be taxable

C) Loss is only recognized on liquidating distributions

D) General partners' salaries are subject to FICA taxes.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

71

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owners may participate in all tax-free employee fringe benefits.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Owners may participate in all tax-free employee fringe benefits.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

72

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Gain recognized by owners on liquidation of entity.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Gain recognized by owners on liquidation of entity.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

73

Sabrina is single and has taxable income of $195,700 of which $140,000 is attributable to her consulting sole proprietorship. She paid W-2 pages to her employees of $75,000. If the threshold amount for 2018 is $157,500, what is Sabrina's qualified business income deduction?

A) $39,500

B) $28,000

C) $20,360

D) $5,600

A) $39,500

B) $28,000

C) $20,360

D) $5,600

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

74

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Must be formed under state law.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Must be formed under state law.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

75

Sam has $80,000 of net income from his sole proprietorship in 2018. What is his deduction for AGI for self-employment taxes?

A) $9,826

B) $6,120

C) $5,652

D) $4,913

A) $9,826

B) $6,120

C) $5,652

D) $4,913

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following cannot be taxed as a partnership?

A) An accounting PLLC

B) An LLC with only one member

C) An LLC owning only rental property

D) A partnership with no limited partners

A) An accounting PLLC

B) An LLC with only one member

C) An LLC owning only rental property

D) A partnership with no limited partners

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

77

Other Objective Questions

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Formation of the entity is generally a tax-free event.

Indicate by a PRP if the characteristic applies to a sole proprietorship, an SC if it applies to an S corporation, and a PAR if it applies to a partnership, and N if it does not apply to any of the three businesses. A characteristic can apply to more than one entity; write a brief explanation if a characteristic may only apply under certain conditions.

Formation of the entity is generally a tax-free event.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

78

Kylie is single and has taxable income of $320,000 of which $130,000 is attributable to her consulting sole proprietorship. She paid W-2 wages to her employees of $75,000. If the threshold amount for 2018 is $157,500, what is Kylie's qualified business income deduction?

A) $0

B) $11,000

C) $26,000

D) $32,500

A) $0

B) $11,000

C) $26,000

D) $32,500

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

79

Which of the following is not an acceptable partnership tax year?

A) The tax year used by any principal partner

B) The tax year used by the partners who own a majority interest

C) A tax year that results in only a 2-month deferral of income for the partners

D) C's tax year if C owns more than 50 percent of the partnership

A) The tax year used by any principal partner

B) The tax year used by the partners who own a majority interest

C) A tax year that results in only a 2-month deferral of income for the partners

D) C's tax year if C owns more than 50 percent of the partnership

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following is not a characteristic of sole proprietorships?

A) Owners pay self-employment taxes

B) Formation is always tax-free

C) Distributions of entity income are tax-free

D) Loss is recognized on liquidation

A) Owners pay self-employment taxes

B) Formation is always tax-free

C) Distributions of entity income are tax-free

D) Loss is recognized on liquidation

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 133 flashcards in this deck.