Deck 5: Analyzing Investing Activities: Intercorporate Investments

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

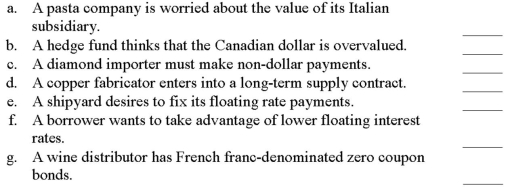

I. Speculative

II. Fair value hedge

III. Cash flow hedge

IV. Foreign currency fair value hedge

V. Foreign currency cash flow hedge

VI. Foreign currency hedge of net investment in foreign operation

VII. Not a derivative

II. Fair value hedge

III. Cash flow hedge

IV. Foreign currency fair value hedge

V. Foreign currency cash flow hedge

VI. Foreign currency hedge of net investment in foreign operation

VII. Not a derivative

Question

Question

Question

Question

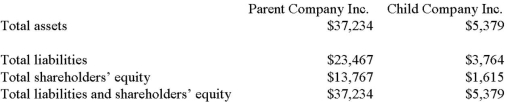

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

Undie Inc. has many foreign operations and uses the U.S. dollar as its functional currency worldwide. Which of the following statements is true with respect to foreign operations?

A)All assets and liabilities are translated at current exchange rates.

B)Monetary assets and liabilities are translated at current exchange rates.

C)Translation gains and losses are reported in equity section of balance sheet.

D)Non-monetary assets and liabilities are translated at average exchange rates for the year.

Undie Inc. has many foreign operations and uses the U.S. dollar as its functional currency worldwide. Which of the following statements is true with respect to foreign operations?

A)All assets and liabilities are translated at current exchange rates.

B)Monetary assets and liabilities are translated at current exchange rates.

C)Translation gains and losses are reported in equity section of balance sheet.

D)Non-monetary assets and liabilities are translated at average exchange rates for the year.

Question

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

Pauly Co. reports a foreign currency translation gain of $5 million in its statement of shareholders' equity. From this, you can infer that:

A)they have foreign operations where the U.S. dollar is the functional currency.

B)they have foreign operations where local currency is the functional currency.

C)they entered into a foreign currency transaction that year.

D)None of the above

Pauly Co. reports a foreign currency translation gain of $5 million in its statement of shareholders' equity. From this, you can infer that:

A)they have foreign operations where the U.S. dollar is the functional currency.

B)they have foreign operations where local currency is the functional currency.

C)they entered into a foreign currency transaction that year.

D)None of the above

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Match between columns

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/69

Play

Full screen (f)

Deck 5: Analyzing Investing Activities: Intercorporate Investments

1

a. Gruber PLC operates in England and is a subsidiary of Szudy International. The functional currency of Gruber is the British pound. Gruber reported net income in 2006 of £350 million and paid a £75 million dividend on July 1, 2006 when the exchange rate was $1.55 per pound. The current rate is $1.65 per pound and the average rate for 2006 was 1.60. Compute the change in retained earnings for the period in US dollars.

b. Windsor PLC operates in England and is a subsidiary of Buckingham International. The U.S. dollar is the reporting currency for Buckingham international. The functional currency of Windsor is the British pound, and it prepares financial information in British pounds for internal use.

Windsor's 2005 and 2006 net assets were 10,000 and 11,500, respectively. The 12/31/06 exchange rate was 1.56, the 12/31/05 exchange rate was 1.50 and the average rate for the year was 1.53.

What was the translation gain or loss for the year for Buckingham when it converted Windsor's financial statements into the reporting currency?

b. Windsor PLC operates in England and is a subsidiary of Buckingham International. The U.S. dollar is the reporting currency for Buckingham international. The functional currency of Windsor is the British pound, and it prepares financial information in British pounds for internal use.

Windsor's 2005 and 2006 net assets were 10,000 and 11,500, respectively. The 12/31/06 exchange rate was 1.56, the 12/31/05 exchange rate was 1.50 and the average rate for the year was 1.53.

What was the translation gain or loss for the year for Buckingham when it converted Windsor's financial statements into the reporting currency?

a. The current rate method should be used, as the British pound is the functional currency.

Retained earnings will increase by the net income and decrease by the dividends paid.

Net income is simply translated using the average rate for the year.

£350 × 1.60 = $560

Dividends are translated using the rate at the time they are paid.

£75 × 1.55 = $116.25

Therefore, retained earnings will change by $443.75 (560 - 116.25).

b. The translation gain or loss can be calculated as:

Beginning of year net assets in the local currency × (change in exchange rate over the year),

Plus

Increase in net assets over year × (end of year rate - average exchange rate for year)

Therefore, the translation gain (loss) is:

This translation gain is the change in the cumulative translation adjustment (CTA) in the stockholders' equity. Therefore, in this case there was a translation gain of $645 for the year, due to the appreciation of the British pound during the year and an increase in the net assets in local currency.

Retained earnings will increase by the net income and decrease by the dividends paid.

Net income is simply translated using the average rate for the year.

£350 × 1.60 = $560

Dividends are translated using the rate at the time they are paid.

£75 × 1.55 = $116.25

Therefore, retained earnings will change by $443.75 (560 - 116.25).

b. The translation gain or loss can be calculated as:

Beginning of year net assets in the local currency × (change in exchange rate over the year),

Plus

Increase in net assets over year × (end of year rate - average exchange rate for year)

Therefore, the translation gain (loss) is:

This translation gain is the change in the cumulative translation adjustment (CTA) in the stockholders' equity. Therefore, in this case there was a translation gain of $645 for the year, due to the appreciation of the British pound during the year and an increase in the net assets in local currency.

2

Agwen Corporation owns 25% of the shares of Bronwo Corporation, which is traded on the New York Stock Exchange. Which method is Agwen most likely to use to account for this investment?

A)Cost method

B)Market method

C)Equity method

D)Consolidation method

A)Cost method

B)Market method

C)Equity method

D)Consolidation method

C

3

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be the net income in the consolidated income statement for year X2?

A)$1,461

B)$1,560

C)$1,450

D)$1,611

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be the net income in the consolidated income statement for year X2?

A)$1,461

B)$1,560

C)$1,450

D)$1,611

$1,461

4

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total assets in the consolidated financial statements for the date on which the merger became effective, assuming any excess purchase price relates to goodwill?

A)$50,008

B)$49,498

C)$41,508

D)$44,113

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total assets in the consolidated financial statements for the date on which the merger became effective, assuming any excess purchase price relates to goodwill?

A)$50,008

B)$49,498

C)$41,508

D)$44,113

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

5

Company ABC, an American company, has a 100% owned foreign subsidiary. The foreign subsidiary's local currency, functional currency and reporting currency are all different. The subsidiary accounts for inventories using the first-in, first-out (FIFO) method.

A. Assume the functional currency is appreciating relative to the reporting currency. Compare each of the following ratios for the foreign subsidiary in the reporting currency after translation to the same ratios in the functional currency before translation. Explain why the ratios do or do not differ.i. Gross profit margin percentage

ii. Current ratio

B. Assume the local currency is appreciating relative to the functional currency. Compare each of the following ratios for the foreign subsidiary in the functional currency after remeasurement to the same ratios in the local currency before remeasurement. Explain why the ratios do or do not differ.i. Gross profit margin percentage

ii. Operating profit margin

iii. Net profit margin

A. Assume the functional currency is appreciating relative to the reporting currency. Compare each of the following ratios for the foreign subsidiary in the reporting currency after translation to the same ratios in the functional currency before translation. Explain why the ratios do or do not differ.i. Gross profit margin percentage

ii. Current ratio

B. Assume the local currency is appreciating relative to the functional currency. Compare each of the following ratios for the foreign subsidiary in the functional currency after remeasurement to the same ratios in the local currency before remeasurement. Explain why the ratios do or do not differ.i. Gross profit margin percentage

ii. Operating profit margin

iii. Net profit margin

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

6

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total assets in the consolidated financial statements for the date on which the merger became effective?

A)$50,008

B)$49,498

C)$41,508

D)$44,113

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total assets in the consolidated financial statements for the date on which the merger became effective?

A)$50,008

B)$49,498

C)$41,508

D)$44,113

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

7

Flowers Inc. an American company has two overseas subsidiaries located in Great Britain (Roses PLC) and in Holland (Tulips Inc.). Flowers prepares consolidated financial statements. The reporting currency is the U.S. dollar.Most of Roses's operations and sales take place in Britain, and the transactions are denominated in the British pound. Additionally, Roses makes its own financing and operating decisions, independently of Flowers Inc.Tulip Inc. is a sales outlet for Roses PLC and operating decisions are made by the British subsidiary, Roses.a. Identify the method(s) Flowers Inc. should use to convert the financial results of Roses PLC into the U.S. dollar for purposes of consolidation.b. Identify the method(s) Flowers Inc. should use to convert the financial results of Tulip Inc. into the U.S. dollar for purposes of consolidation.c. Explain how a decline in the value of the British pound relative to the U.S. dollar will affect Flowers' earnings in the reporting currency.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

8

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be the net income in the consolidated income statement for year X2 assuming any excess purchase price relates to goodwill, and goodwill was found to be impaired by $830?

A)$1,461

B)$1,560

C)$1,012.2

D)$730

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be the net income in the consolidated income statement for year X2 assuming any excess purchase price relates to goodwill, and goodwill was found to be impaired by $830?

A)$1,461

B)$1,560

C)$1,012.2

D)$730

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

9

Compared to the equity method, the cost method of accounting for an investment in a profitable company results in:

A)lower earnings and lower cash flows.

B)higher earnings and higher cash flows.

C)lower earnings and no effect on cash flows.

D)higher earnings and no effect on cash flows.

A)lower earnings and lower cash flows.

B)higher earnings and higher cash flows.

C)lower earnings and no effect on cash flows.

D)higher earnings and no effect on cash flows.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

10

The equity method of accounting for investments requires:

A)investment should be marked to market each accounting period.

B)proportionate share of investee's earnings should be recorded as investment income.

C)company should not have significant influence over investee.

D)goodwill related to purchase of investee stock to be recorded separately on balance sheet.

A)investment should be marked to market each accounting period.

B)proportionate share of investee's earnings should be recorded as investment income.

C)company should not have significant influence over investee.

D)goodwill related to purchase of investee stock to be recorded separately on balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

11

Trading marketable securities:

A)are considered noncurrent assets.

B)are recorded at amortized cost.

C)are marked to the lower of cost or market each accounting period.

D)are marked to market each accounting period.

A)are considered noncurrent assets.

B)are recorded at amortized cost.

C)are marked to the lower of cost or market each accounting period.

D)are marked to market each accounting period.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

12

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total liabilities in the consolidated financial statements for the date on which the merger became effective?

A)$28,221

B)$27,231

C)$27,741

D)$25,462

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total liabilities in the consolidated financial statements for the date on which the merger became effective?

A)$28,221

B)$27,231

C)$27,741

D)$25,462

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

13

Single Station Inc. is acquired by Mega Communications on January 1, 2006 for $9,500. Prior to the acquisition, Single was projecting sales of $10,000 and total expenses of $8,000 in 2006 and forecasted that earnings will accumulate as cash. There are no operating synergies and no taxes.

The acquisition appraisal of Single's assets and liabilities indicates that fair market value (FMV) exceeds book value for the following assets only:

• machinery and equipment-$4,000 with a life 4 year life

• operating lease-$1,000 with 10 years remaining

• broadcast licenses-$500 with a 5 year life

a. Single is required to use push-down accounting. Prepare a pro forma balance sheet at January 1, 2006 for Single.

b. Prepare a pro forma income statement for the year ending December 31, 2006 using Single's projection.

c. Prepare a pro forma balance sheet at December 31, 2006.

d. Assume the pro forma results in b) and c) are achieved. A second appraisal of Single's assets at December 31, 2006 indicates that the FMV for Single as a whole is $7,500 and that the broadcast licenses are now worth $400. The FMV of Single's other assets and liabilities are the same as book. Determine whether goodwill has been impaired and thus, determine the amount of the loss, if any.

The acquisition appraisal of Single's assets and liabilities indicates that fair market value (FMV) exceeds book value for the following assets only:

• machinery and equipment-$4,000 with a life 4 year life

• operating lease-$1,000 with 10 years remaining

• broadcast licenses-$500 with a 5 year life

a. Single is required to use push-down accounting. Prepare a pro forma balance sheet at January 1, 2006 for Single.

b. Prepare a pro forma income statement for the year ending December 31, 2006 using Single's projection.

c. Prepare a pro forma balance sheet at December 31, 2006.

d. Assume the pro forma results in b) and c) are achieved. A second appraisal of Single's assets at December 31, 2006 indicates that the FMV for Single as a whole is $7,500 and that the broadcast licenses are now worth $400. The FMV of Single's other assets and liabilities are the same as book. Determine whether goodwill has been impaired and thus, determine the amount of the loss, if any.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is an effect of the reclassification of trading securities as available-for-sale?

A)The balance sheet would need to be adjusted to report the securities at fair market value and there would be no effect on the income statement.

B)There would be no effect on either the balance sheet or the income statement.

C)The balance sheet would need to be adjusted to report the securities at fair market value and unrealized gains or losses on the date of the transfer would be included in net income.

D)There would be no effect on the balance sheet and unrealized gains or losses on the date of the transfer would be included in net income.

A)The balance sheet would need to be adjusted to report the securities at fair market value and there would be no effect on the income statement.

B)There would be no effect on either the balance sheet or the income statement.

C)The balance sheet would need to be adjusted to report the securities at fair market value and unrealized gains or losses on the date of the transfer would be included in net income.

D)There would be no effect on the balance sheet and unrealized gains or losses on the date of the transfer would be included in net income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

15

Wilde Corporation owns 30% of the outstanding stock of Bernie Inc. Bernie recorded net income of $10 million and paid dividends of $3 million in 2006. For each of the following ratios, state the effect (higher, lower, or no effect) that the use of the equity method would have on Wilde's financial ratios compared to the use of the cost method in 2006. Explain your answers.i. Gross margin

ii. Total asset turnover

iii. Cash flow from operations to current liabilities

iv. Debt-to-equity

ii. Total asset turnover

iii. Cash flow from operations to current liabilities

iv. Debt-to-equity

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

16

I. Speculative

II. Fair value hedge

III. Cash flow hedge

IV. Foreign currency fair value hedge

V. Foreign currency cash flow hedge

VI. Foreign currency hedge of net investment in foreign operation

VII. Not a derivative

II. Fair value hedge

III. Cash flow hedge

IV. Foreign currency fair value hedge

V. Foreign currency cash flow hedge

VI. Foreign currency hedge of net investment in foreign operation

VII. Not a derivative

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is incorrect? An analyst should be aware of the following when analyzing a company that has significant investments recorded using the equity method.

A)Cash flow received from investee may be substantially different from investment income recorded.

B)As investee's liabilities are not recorded on the company's balance sheet, there may be significant off-balance-sheet financing.

C)They must mark investment in investee to market even though there may be no ready market in which they can sell their investment.

D)Company must record pro rata share of investee's earnings, which may not be well correlated with changes in market value of investee.

A)Cash flow received from investee may be substantially different from investment income recorded.

B)As investee's liabilities are not recorded on the company's balance sheet, there may be significant off-balance-sheet financing.

C)They must mark investment in investee to market even though there may be no ready market in which they can sell their investment.

D)Company must record pro rata share of investee's earnings, which may not be well correlated with changes in market value of investee.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

18

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total liabilities in the consolidated financial statements for the date on which the merger became effective, assuming any excess purchase price relates to goodwill?

A)$28,221

B)$27,231

C)$27,741

D)$25,462

Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

-What would be total liabilities in the consolidated financial statements for the date on which the merger became effective, assuming any excess purchase price relates to goodwill?

A)$28,221

B)$27,231

C)$27,741

D)$25,462

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

19

The classification of marketable equity securities as trading or available-for-sale is determined:

A)by management's intent regarding the disposition of the securities.

B)when the securities mature.

C)whether the current assets are greater or less than the current liabilities.

D)whether management wants to mark them to market or not.

A)by management's intent regarding the disposition of the securities.

B)when the securities mature.

C)whether the current assets are greater or less than the current liabilities.

D)whether management wants to mark them to market or not.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

20

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

Undie Inc. has many foreign operations and uses the U.S. dollar as its functional currency worldwide. Which of the following statements is true with respect to foreign operations?

A)All assets and liabilities are translated at current exchange rates.

B)Monetary assets and liabilities are translated at current exchange rates.

C)Translation gains and losses are reported in equity section of balance sheet.

D)Non-monetary assets and liabilities are translated at average exchange rates for the year.

Undie Inc. has many foreign operations and uses the U.S. dollar as its functional currency worldwide. Which of the following statements is true with respect to foreign operations?

A)All assets and liabilities are translated at current exchange rates.

B)Monetary assets and liabilities are translated at current exchange rates.

C)Translation gains and losses are reported in equity section of balance sheet.

D)Non-monetary assets and liabilities are translated at average exchange rates for the year.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

21

Parent Company Inc. successfully bids for Child Company Inc. in year X1. Parent Company Inc. has purchased all of Child's shares outstanding for $8,500. Following are excerpts from both companies' financial statements for year X1, prior to the acquisition.Also assume the following information: the acquisition was accounted for using the purchase method. $1,500 of the excess price relates to depreciable assets, and those assets have an additional useful life of 10 years at the time of the acquisition. Parent Company Inc. uses the straight line depreciation method and has a 34% tax rate. The combined net income for both companies for year X2 (excluding any expenses that need to be recorded as a result of the purchase method accounting for the merger) was $1,560.

Pauly Co. reports a foreign currency translation gain of $5 million in its statement of shareholders' equity. From this, you can infer that:

A)they have foreign operations where the U.S. dollar is the functional currency.

B)they have foreign operations where local currency is the functional currency.

C)they entered into a foreign currency transaction that year.

D)None of the above

Pauly Co. reports a foreign currency translation gain of $5 million in its statement of shareholders' equity. From this, you can infer that:

A)they have foreign operations where the U.S. dollar is the functional currency.

B)they have foreign operations where local currency is the functional currency.

C)they entered into a foreign currency transaction that year.

D)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

22

Which exchange rates are used for foreign subsidiaries with different functional currencies? Using the following abbreviations identify which of the below are correct methods for converting accounts receivable.

Year-end rates: YE

Average rates: AR

Historical rates: HR

A)Option A

B)Option B

C)Option C

D)Option D

Year-end rates: YE

Average rates: AR

Historical rates: HR

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

23

When an acquisition is made and accounted for using the purchase method, the post-acquisition common stock account:

A)is the sum of the pre-acquisition common stock accounts of the two combining companies.

B)is the pre-acquisition common stock account of the acquired company only.

C)is the pre-acquisition common stock account of the acquiring company plus the par value of new stock issued to affect the acquisition.

D)is the pre-acquisition common stock account of the acquiring company plus the fair value of new stock issued to affect the acquisition.

A)is the sum of the pre-acquisition common stock accounts of the two combining companies.

B)is the pre-acquisition common stock account of the acquired company only.

C)is the pre-acquisition common stock account of the acquiring company plus the par value of new stock issued to affect the acquisition.

D)is the pre-acquisition common stock account of the acquiring company plus the fair value of new stock issued to affect the acquisition.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

24

Both consolidation and equity method accounting assume a dollar earned by a subsidiary is equivalent to a dollar earned for a parent, even if not received in cash. The limitations of this assumption of dollar-for-dollar equivalence include which of the following? I. Dividends restricted by law and loan covenants

II) Risks due to political and economic factors

III) Tax liabilities from remittance of earnings

IV) Minority interests that limit parent's discretion

A)II and III

B)II

C)I and III

D)I, II, III, and IV

II) Risks due to political and economic factors

III) Tax liabilities from remittance of earnings

IV) Minority interests that limit parent's discretion

A)II and III

B)II

C)I and III

D)I, II, III, and IV

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

25

Xena Corporation has a foreign subsidiary, Zeta Corporation, located in Japan. At the end of fiscal 2006, Zeta has:

-Assume Xena uses the current rate method for translating Zeta's financial statements from the yen into U.S. dollars. If the yen appreciates relative to the dollar, which of the following is true?

A)Xena will record a foreign currency translation gain on the income statement.

B)Xena will record a foreign currency translation loss on the income statement.

C)Xena will record a foreign currency translation gain in the equity section of the balance sheet.

D)Xena will record a foreign currency translation loss in the equity section of the balance sheet.

-Assume Xena uses the current rate method for translating Zeta's financial statements from the yen into U.S. dollars. If the yen appreciates relative to the dollar, which of the following is true?

A)Xena will record a foreign currency translation gain on the income statement.

B)Xena will record a foreign currency translation loss on the income statement.

C)Xena will record a foreign currency translation gain in the equity section of the balance sheet.

D)Xena will record a foreign currency translation loss in the equity section of the balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

26

Under U.S. GAAP, the method used to convert financial statements of foreign subsidiaries in countries experiencing hyperinflation is:

A)the current rate method.

B)the inflation method.

C)the temporal method.

D)the transition method.

A)the current rate method.

B)the inflation method.

C)the temporal method.

D)the transition method.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

27

When an acquisition is made and accounted for using the purchase method, the post-acquisition retained earnings account:

A)is the sum of the pre-acquisition retained earnings accounts of the two combining companies.

B)is the pre-acquisition retained earnings account of the acquiring company only.

C)is the pre-acquisition retained earnings accounts of the acquiring company plus net income of acquired company in year of acquisition.

D)is the pre-acquisition retained earnings accounts of the acquiring company less treasury stock of the acquired company.

A)is the sum of the pre-acquisition retained earnings accounts of the two combining companies.

B)is the pre-acquisition retained earnings account of the acquiring company only.

C)is the pre-acquisition retained earnings accounts of the acquiring company plus net income of acquired company in year of acquisition.

D)is the pre-acquisition retained earnings accounts of the acquiring company less treasury stock of the acquired company.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

28

Under U.S. GAAP, the method used to convert financial statements of foreign subsidiaries into the reporting currency depends upon:

A)the size of the subsidiary.

B)the functional currency of the subsidiary.

C)the temporal location of the subsidiary.

D)the current method used by the subsidiary.

A)the size of the subsidiary.

B)the functional currency of the subsidiary.

C)the temporal location of the subsidiary.

D)the current method used by the subsidiary.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

29

A U.S. company has a subsidiary located in Great Britain. Information for the subsidiary for the year ended December 31, 2006, is as follows:

-If the British pound was determined to be the functional currency, what would inventory be in US dollars?

A)$3,500

B)$3,200

C)$3,000

D)$2,800

-If the British pound was determined to be the functional currency, what would inventory be in US dollars?

A)$3,500

B)$3,200

C)$3,000

D)$2,800

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

30

Which exchange rates are used for foreign subsidiaries with different functional currencies? Using the following abbreviations, identify which of the below are correct methods for converting inventory.

Year-end rates: YE

Average rates: AR

Historical rates: HR

A)Option A

B)Option B

C)Option C

D)Option D

Year-end rates: YE

Average rates: AR

Historical rates: HR

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

31

A U.S. company has a subsidiary located in Great Britain. If the British pound is the functional currency and is appreciating relative to the dollar, what will happen to the following ratios after translation?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

32

Old Co. was acquired by Raptor for cash, at a significant premium to book value, on January 1, 2004. Since that time, the now wholly owned subsidiary has had modest growth and all of its earnings have been distributed to its parent. Some of Old's bonds remain publicly traded. Which of the following is most likely be true considering the above scenario?

A)An increase in Old's total assets from 2003 to 2005

B)An increase in Old's pretax income from 2003 to 2005

C)An increase in Old's stockholders' equity from 2003 to 2005

D)A Raptor guarantee of the bonds

A)An increase in Old's total assets from 2003 to 2005

B)An increase in Old's pretax income from 2003 to 2005

C)An increase in Old's stockholders' equity from 2003 to 2005

D)A Raptor guarantee of the bonds

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

33

Depreciation expense would be:

A)lower using conversion method than temporal method.

B)lower using temporal method than current rate method.

C)lower using current rate method than conversion method.

D)lower using all-current rate method than temporal method.

A)lower using conversion method than temporal method.

B)lower using temporal method than current rate method.

C)lower using current rate method than conversion method.

D)lower using all-current rate method than temporal method.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

34

A U.S. company has a subsidiary located in Great Britain. If the U.S. dollar is the functional currency and the British pound is appreciating relative to the dollar, what will happen to the following ratios after remeasurement?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

35

A U.S. company has a subsidiary located in Great Britain. Information for the subsidiary for the year ended December 31, 2006, is as follows:

-After converting to U.S. dollars using the appropriate method, gross profit margin is 40%. What method is being used to record British subsidiaries financial statements?

A)The current rate method

B)The temporal method

C)The conversion method

D)Not determinable from information given

-After converting to U.S. dollars using the appropriate method, gross profit margin is 40%. What method is being used to record British subsidiaries financial statements?

A)The current rate method

B)The temporal method

C)The conversion method

D)Not determinable from information given

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

36

Current ratio:

A)would be unchanged after applying the current rate method.

B)would be unchanged after applying the temporal method.

C)would be unchanged after applying the conversion method.

D)would be higher after applying the temporal method.

A)would be unchanged after applying the current rate method.

B)would be unchanged after applying the temporal method.

C)would be unchanged after applying the conversion method.

D)would be higher after applying the temporal method.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

37

Xena Corporation has a foreign subsidiary, Zeta Corporation, located in Japan. At the end of fiscal 2006, Zeta has:

-Assume Xena uses the temporal method for translating Zeta's financial statements from the yen into U.S. dollars. If the yen appreciates relative to the dollar, which of the following is true?

A)Xena will record a foreign currency translation gain on the income statement.

B)Xena will record a foreign currency translation loss on the income statement.

C)Xena will record a foreign currency translation gain in the equity section of the balance sheet.

D)Xena will record a foreign currency translation loss in the equity section of the balance sheet.

-Assume Xena uses the temporal method for translating Zeta's financial statements from the yen into U.S. dollars. If the yen appreciates relative to the dollar, which of the following is true?

A)Xena will record a foreign currency translation gain on the income statement.

B)Xena will record a foreign currency translation loss on the income statement.

C)Xena will record a foreign currency translation gain in the equity section of the balance sheet.

D)Xena will record a foreign currency translation loss in the equity section of the balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

38

In-process R&D:

A)is written-off immediately to retained earnings.

B)is only an issue when purchase accounting is used.

C)is capitalized on the balance sheet and never amortized.

D)is expensed immediately under pooling of interests.

A)is written-off immediately to retained earnings.

B)is only an issue when purchase accounting is used.

C)is capitalized on the balance sheet and never amortized.

D)is expensed immediately under pooling of interests.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

39

When accounting for an investment under the equity method, what situations may reduce the carrying value of the investment? I. Investee experiences significant losses.II. Investee distributes dividends in excess of earnings.III. Investee sells additional shares for less than book value.IV. Investee engages in a stock split.

A)I and II

B)II and IV

C)I, II, and III

D)I, III, and IV

A)I and II

B)II and IV

C)I, II, and III

D)I, III, and IV

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

40

A U.S. company has a subsidiary located in Great Britain. Information for the subsidiary for the year ended December 31, 2006, is as follows:

-If sales were 3,000 in British pounds for the fiscal year and the temporal method was used, what would this be in U.S. dollars?

A)$4,800

B)$4,500

C)$4,200

D)$4,000

-If sales were 3,000 in British pounds for the fiscal year and the temporal method was used, what would this be in U.S. dollars?

A)$4,800

B)$4,500

C)$4,200

D)$4,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

41

The current rate method should be used to translate foreign currency into the parent currency when the functional currency is deemed to be the parent currency.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

42

Held-to-maturity securities are always classified as noncurrent assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

43

The equity method of accounting for investments should be used when a company has a controlling interest in the investee.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

44

Investment securities should always be reported at lower of cost or market.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

45

If the functional currency of a foreign-based subsidiary of an American company is the local currency, the current rate method of translation should be used for consolidation purposes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

46

All derivatives are recorded at market value on the balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

47

When using the current rate method to record foreign subsidiary results, gains and losses arising from the translation process are reported separately as a component of stockholders' equity and excluded from reported net income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is allowed to be reported on fair value basis under SFAS 159?

A)Investment in subsidiaries that need to be consolidated

B)Lease assets and obligations

C)Derivatives

D)Postretirement benefit assets and obligations

A)Investment in subsidiaries that need to be consolidated

B)Lease assets and obligations

C)Derivatives

D)Postretirement benefit assets and obligations

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

49

When purchase accounting is used for acquisitions, prior year financial statements presented for comparative purposes should be restated as if the companies had always been combined.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

50

If a company has a wholly owned foreign subsidiary located at a place where the functional currency is highly inflationary, they should use the temporal method.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

51

When a security is reclassified from available-for-sale to trading, it is transferred at fair market value, and any unrealized gains or losses must be recognized in the income statement.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

52

The equity conformity rule requires that marketable securities must be marked to market for tax purposes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

53

Held-to-maturity securities are equity securities that management intends and has the ability to hold to maturity.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

54

One of the problems with purchase accounting is that there is often very little basis for comparability of financial statements before acquisition and after acquisition.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

55

One of the problems with consolidated financial statements is that all intercompany transactions are not reported.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

56

Translation is the process under which local currency results are translated into the functional currency.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

57

Reported sales in US dollars of revenues from a foreign subsidiary will be the same regardless of the functional currency.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

58

Goodwill recorded as the result of an acquisition is defined as the purchase price less the book value of net assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

59

When using the current rate method to record foreign subsidiary results, all assets and liabilities are translated at a rate, in effect as of the statement date.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

60

When the income statement of a foreign subsidiary is translated into the reporting currency from the functional currency, the gross margin will remain the same in the translation process.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

61

If the temporal method is used for foreign currency translation and the foreign subsidiary has an excess of monetary assets over monetary liabilities, an increase in the strength of the dollar will result in a translation loss.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

62

If the temporal method is used for foreign currency translation and the foreign subsidiary has an excess of monetary liabilities over monetary assets, an increase in the strength of the dollar will result in a translation loss.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

63

Flowers Inc. an American company has two overseas subsidiaries located in Great Britain (Roses PLC) and in Holland (Tulips Inc.). Flowers prepares consolidated financial statements. The reporting currency is the U.S. dollar.Most of Roses's operations and sales take place in Britain, and the transactions are denominated in the British pound. Additionally, Roses makes its own financing and operating decisions, independently of Flowers Inc.Tulip Inc. is a sales outlet for Roses PLC and operating decisions are made by the British subsidiary, Roses.a. Identify the method(s) Flowers Inc. should use to convert the financial results of Roses PLC into the U.S. dollar for purposes of consolidation.b. Identify the method(s) Flowers Inc. should use to convert the financial results of Tulip Inc. into the U.S. dollar for purposes of consolidation.c. Explain how a decline in the value of the British pound relative to the U.S. dollar will affect Flowers' earnings in the reporting currency.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

64

Under SFAS 141, accounting for acquisitions can no longer result in an increase in the consolidated entity's stockholders' equity.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

66

Match between columns

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

67

If a company chooses the fair value option for an asset or liability, all changes in the fair value of the asset (or liability), including unrealized gain and losses, will be included in net income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 69 flashcards in this deck.