Deck 2: Asset and Liability Valuation and Income Measurement

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Balance Sheet Equation

Refer to Balance Sheet Equation. JCP Company purchased marketable securities for $5,000 during the year, at the end of the year the company revalues the securities to $5,700. This revaluation would result in an increase to non-cash assets and ____________________________________________________________.

Refer to Balance Sheet Equation. JCP Company purchased marketable securities for $5,000 during the year, at the end of the year the company revalues the securities to $5,700. This revaluation would result in an increase to non-cash assets and ____________________________________________________________.

Refer to Balance Sheet Equation. JCP Company purchased marketable securities for $5,000 during the year, at the end of the year the company revalues the securities to $5,700. This revaluation would result in an increase to non-cash assets and ____________________________________________________________. Question

Question

Question

Question

Question

Question

Question

Question

Balance Sheet Equation

Refer to Balance Sheet Equation. The payment of dividends by a firm reduces cash and ______________________________.

Refer to Balance Sheet Equation. The payment of dividends by a firm reduces cash and ______________________________.

Refer to Balance Sheet Equation. The payment of dividends by a firm reduces cash and ______________________________. Question

Balance Sheet Equation

Refer to Balance Sheet Equation. If ORP Corporation sells $25,000 of its product on account, it will see an increase in non-cash assets and ___________________________________.

Refer to Balance Sheet Equation. If ORP Corporation sells $25,000 of its product on account, it will see an increase in non-cash assets and ___________________________________.

Refer to Balance Sheet Equation. If ORP Corporation sells $25,000 of its product on account, it will see an increase in non-cash assets and ___________________________________. Question

Question

Question

Balance Sheet Equation

Refer to Balance Sheet Equation. ORP Corporation sells land with a book value of $12,000 for $9,000. This transaction results in ORP recording an increase in cash of $9,000, a decrease in non-cash assets of $12,000 and a decrease in ______________________________ of $3,000.

Refer to Balance Sheet Equation. ORP Corporation sells land with a book value of $12,000 for $9,000. This transaction results in ORP recording an increase in cash of $9,000, a decrease in non-cash assets of $12,000 and a decrease in ______________________________ of $3,000.

Refer to Balance Sheet Equation. ORP Corporation sells land with a book value of $12,000 for $9,000. This transaction results in ORP recording an increase in cash of $9,000, a decrease in non-cash assets of $12,000 and a decrease in ______________________________ of $3,000. Question

Question

Question

Balance Sheet Equation

Refer to Balance Sheet Equation. To recognize the cost of goods sold ORP Corporation will reduce retained earnings and reduce ______________________________.

Refer to Balance Sheet Equation. To recognize the cost of goods sold ORP Corporation will reduce retained earnings and reduce ______________________________.

or

Refer to Balance Sheet Equation. To recognize the cost of goods sold ORP Corporation will reduce retained earnings and reduce ______________________________.or

Question

Question

Question

Question

Question

The analytical framework used to evaluate transactions is reproduced below:

Using this analytical framework indicate the effect of each of the following transactions for TX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for TX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for TX Corporation: Question

Question

Question

Question

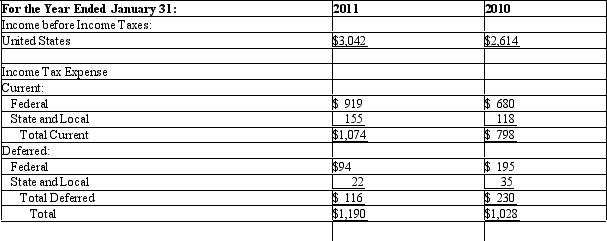

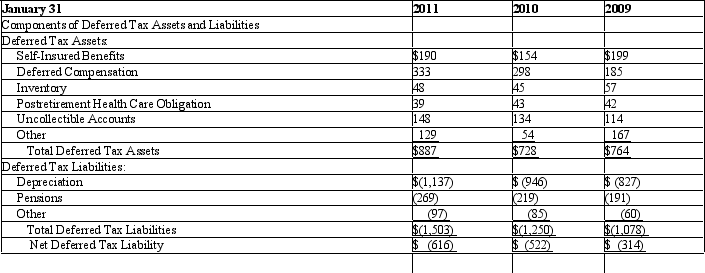

The financial statement disclosures for Able Company, a retail chain, revealed the following information regarding the firm's income taxes:

Required:

Required:

a. Assuming that Able had no significant permanent differences between book income

and taxable income, did income before taxes for financial reporting exceed or fall

short of taxable income for 2010? Explain.

b. Did income before taxes for financial reporting exceed or fall short of taxable

income for 2011? Explain.

c. Will the adjustment to net income for deferred taxes to compute cash flow from

operations in the statement of cash flows result in an addition or a subtraction for

2010? For 2011?

d. Able does not contract with an insurance agency for property and liability insurance;

instead, it self-insures. Able recognizes an expense and a liability each year for

financial reporting to reflect its average expected long-term property and liability

losses. When it experiences an actual loss, it charges that loss against the liability. The

income tax law permits self-insured firms to deduct such losses only in the year sustained.

Why are deferred taxes related to self-insurance disclosed as a deferred tax

asset instead of a deferred tax liability? Suggest reasons for the direction of the

change in amounts for this deferred tax asset between 2009 and 2011.

e. Able treats certain storage and other inventory costs as expenses in the year incurred

for financial reporting but must include these in inventory for tax reporting. Why

are deferred taxes related to inventory disclosed as a deferred tax asset? Suggest reasons

for the direction of the change in amounts for this deferred tax asset between

2009 and 2011.

f. Firms must recognize expenses related to postretirement health care and pension

obligations as employees provide services, but claim an income tax deduction only

when they make cash payments under the benefit plan. Why are deferred taxes

related to health care obligation disclosed as a deferred tax asset? Why are deferred

taxes related to pensions disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for these deferred tax items between 2009 and

2011.

g. Firms must recognize expenses related to uncollectible accounts when they recognize

sales revenues, but claim an income tax deduction when they deem a particular

customer's accounts uncollectible. Why are deferred taxes related to this item disclosed

as a deferred tax asset? Suggest reasons for the direction of the change in

amounts for this deferred tax asset between 2009 and 2011.

h. Able uses the straight-line depreciation method for financial reporting and accelerated

depreciation methods for income tax purposes. Why are deferred taxes

related to depreciation disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for this deferred tax liability between 2009

and 2011.

Required:a. Assuming that Able had no significant permanent differences between book income

and taxable income, did income before taxes for financial reporting exceed or fall

short of taxable income for 2010? Explain.

b. Did income before taxes for financial reporting exceed or fall short of taxable

income for 2011? Explain.

c. Will the adjustment to net income for deferred taxes to compute cash flow from

operations in the statement of cash flows result in an addition or a subtraction for

2010? For 2011?

d. Able does not contract with an insurance agency for property and liability insurance;

instead, it self-insures. Able recognizes an expense and a liability each year for

financial reporting to reflect its average expected long-term property and liability

losses. When it experiences an actual loss, it charges that loss against the liability. The

income tax law permits self-insured firms to deduct such losses only in the year sustained.

Why are deferred taxes related to self-insurance disclosed as a deferred tax

asset instead of a deferred tax liability? Suggest reasons for the direction of the

change in amounts for this deferred tax asset between 2009 and 2011.

e. Able treats certain storage and other inventory costs as expenses in the year incurred

for financial reporting but must include these in inventory for tax reporting. Why

are deferred taxes related to inventory disclosed as a deferred tax asset? Suggest reasons

for the direction of the change in amounts for this deferred tax asset between

2009 and 2011.

f. Firms must recognize expenses related to postretirement health care and pension

obligations as employees provide services, but claim an income tax deduction only

when they make cash payments under the benefit plan. Why are deferred taxes

related to health care obligation disclosed as a deferred tax asset? Why are deferred

taxes related to pensions disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for these deferred tax items between 2009 and

2011.

g. Firms must recognize expenses related to uncollectible accounts when they recognize

sales revenues, but claim an income tax deduction when they deem a particular

customer's accounts uncollectible. Why are deferred taxes related to this item disclosed

as a deferred tax asset? Suggest reasons for the direction of the change in

amounts for this deferred tax asset between 2009 and 2011.

h. Able uses the straight-line depreciation method for financial reporting and accelerated

depreciation methods for income tax purposes. Why are deferred taxes

related to depreciation disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for this deferred tax liability between 2009

and 2011.

Question

Question

The following problem requires present value information:

Biotech sold a patent on a new blood analyzer to Pharma. The sales agreement which was signed on January 1, 2009 requires Pharma to pay Biotech $1 million immediately. In addition, Pharma is required to pay $600,000 each December 31 for 20 years starting with December 31, 2009. Pharma and Biotech judge that a 10 percent is an appropriate interest rate for this arrangement.

Biotech sold a patent on a new blood analyzer to Pharma. The sales agreement which was signed on January 1, 2009 requires Pharma to pay Biotech $1 million immediately. In addition, Pharma is required to pay $600,000 each December 31 for 20 years starting with December 31, 2009. Pharma and Biotech judge that a 10 percent is an appropriate interest rate for this arrangement.

Question

Question

Question

Question

Question

The analytical framework used to evaluate transactions is reproduced below:

Using this analytical framework indicate the effect of each of the following transactions for CX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for CX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for CX Corporation: Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/77

Play

Full screen (f)

Deck 2: Asset and Liability Valuation and Income Measurement

1

At origination which of the following temporary differences would create a deferred tax asset?

A) Tax basis of an asset exceeds its financial reporting basis.

B) Tax basis of a liability exceeds its financial reporting basis.

C) Financial reporting basis of an asset is equal to its tax basis.

D) Financial reporting basis of an asset exceeds its tax basis.

A) Tax basis of an asset exceeds its financial reporting basis.

B) Tax basis of a liability exceeds its financial reporting basis.

C) Financial reporting basis of an asset is equal to its tax basis.

D) Financial reporting basis of an asset exceeds its tax basis.

A

2

The traditional accounting model delays the recognition of value changes of assets and liabilities until what event occurs?

A) A change in value.

B) A market transaction.

C) A balance sheet date.

D) Cash is received or cash is paid.

A) A change in value.

B) A market transaction.

C) A balance sheet date.

D) Cash is received or cash is paid.

B

3

The use of acquisition cost as a valuation method is justified on the basis that acquisition cost is:

A) timely

B) relevant

C) subjective

D) objective

A) timely

B) relevant

C) subjective

D) objective

D

4

When income tax expense for a period is greater than income tax payable the difference will be reported how and on which financial statement?

A) Deferred tax asset and Statement of Cash Flows

B) Deferred tax asset and Balance Sheet

C) Deferred tax liability and Statement of Cash Flows

D) Deferred tax liability and Balance Sheet

A) Deferred tax asset and Statement of Cash Flows

B) Deferred tax asset and Balance Sheet

C) Deferred tax liability and Statement of Cash Flows

D) Deferred tax liability and Balance Sheet

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

5

The net amount a firm would receive if it sold an asset or the net amount it would pay to settle a liability is referred to as

A) current replacement cost

B) net realizable value

C) current cost

D) acquisition cost

A) current replacement cost

B) net realizable value

C) current cost

D) acquisition cost

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

6

The income statement approach to measuring income tax expense

A) is required by FASB Statement No. 109.

B) compares revenues and expenses recognized for book and tax purposes, eliminates permanent differences, and computes income tax expense based on book income before taxes excluding permanent differences.

C) computes income tax expense as a difference between the tax basis of an asset or a liability and its reported amount in the [balance sheet] that will result in taxable or deductible amounts in some future year(s) when the reported amounts of assets are recovered and the reported amounts of liabilities are settled.

D) is required by IAS 12.

A) is required by FASB Statement No. 109.

B) compares revenues and expenses recognized for book and tax purposes, eliminates permanent differences, and computes income tax expense based on book income before taxes excluding permanent differences.

C) computes income tax expense as a difference between the tax basis of an asset or a liability and its reported amount in the [balance sheet] that will result in taxable or deductible amounts in some future year(s) when the reported amounts of assets are recovered and the reported amounts of liabilities are settled.

D) is required by IAS 12.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

7

Shareholders' equity consists of what three components:

A) Assets, liabilities, and contributed capital.

B) Contributed capital, accumulated other comprehensive income, and retained earnings.

C) Liabilities, contributed capital, and retained earnings.

D) Liabilities, contributed capital, and accumulated other comprehensive income.

A) Assets, liabilities, and contributed capital.

B) Contributed capital, accumulated other comprehensive income, and retained earnings.

C) Liabilities, contributed capital, and retained earnings.

D) Liabilities, contributed capital, and accumulated other comprehensive income.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following assets appears on the balance sheet at fair value?

A) Equipment

B) Land

C) Investments in Marketable Securities

D) Intangible Assets

A) Equipment

B) Land

C) Investments in Marketable Securities

D) Intangible Assets

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

9

Future tax deductions

A) result in deferred tax assets.

B) result in deferred tax liabilities.

C) occur where the tax basis of liabilities is more than the financial reporting basis.

D) occur where the tax basis of assets is less than financial reporting basis.

A) result in deferred tax assets.

B) result in deferred tax liabilities.

C) occur where the tax basis of liabilities is more than the financial reporting basis.

D) occur where the tax basis of assets is less than financial reporting basis.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

10

Disregarding cash flows with owners, over sufficiently long periods of time, net income equals:

A) revenues minus dividends and expenses

B) assets minus liabilities

C) stockholders' equity

D) cash inflows minus cash outflows

A) revenues minus dividends and expenses

B) assets minus liabilities

C) stockholders' equity

D) cash inflows minus cash outflows

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

11

Plaxo Corporation has a tax rate of 35% and uses the straight-line method of depreciation for its equipment, which has a useful life of four years. Tax legislation requires the company to depreciate its equipment using the following schedule: year 1- 50%, year 2 - 30%, year 3 - 15% and year 4 - 5%. In 2010 Plaxo purchases a piece of equipment with a four year life and an original cost of $100,000. What amount will Plaxo record as a deferred tax asset or liability in 2010?

A) Deferred tax asset of $25,000.

B) Deferred tax liability of $25,000.

C) Deferred tax asset of $8,750.

D) Deferred tax liability of $8,750.

A) Deferred tax asset of $25,000.

B) Deferred tax liability of $25,000.

C) Deferred tax asset of $8,750.

D) Deferred tax liability of $8,750.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

12

Fish Farm Corporation purchases a new tract of land on which it is going to build new growing and holding tanks in order to expand its business. Which of the following costs would not be part of the cost of the land?

A) costs to run a title search

B) costs of grading to level the land

C) costs of tearing down an existing structure

D) cost of the new holding tanks

A) costs to run a title search

B) costs of grading to level the land

C) costs of tearing down an existing structure

D) cost of the new holding tanks

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is not one of methods used by GAAP for treating value changes?

A) Recognize value changes on the balance sheet and income statement when they are realized in a market transaction

B) Recognize value changes in the income statement when the value changes occur over time, but recognize them on the balance sheet when they are realized in a market transaction

C) Recognize value changes on the balance sheet when the value changes occur over time, but recognize them in the income statement when they are realized in a market transaction

D) Recognize value changes on the balance sheet and income statement when they occur over time, even though they are not realized in a market transaction

A) Recognize value changes on the balance sheet and income statement when they are realized in a market transaction

B) Recognize value changes in the income statement when the value changes occur over time, but recognize them on the balance sheet when they are realized in a market transaction

C) Recognize value changes on the balance sheet when the value changes occur over time, but recognize them in the income statement when they are realized in a market transaction

D) Recognize value changes on the balance sheet and income statement when they occur over time, even though they are not realized in a market transaction

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following valuation methods reflects current values?

A) acquisition cost

B) present value of cash flows using historical interest rates

C) net realizable value

D) adjusted acquisition cost

A) acquisition cost

B) present value of cash flows using historical interest rates

C) net realizable value

D) adjusted acquisition cost

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following transactions is consistent with recognizing value changes on the balance sheet and income statement when they are realized in a market transaction?

A) Selling land at a cost greater than its original purchase price.

B) Recording an increase in the fair value of investments at year end.

C) Translating foreign operations accounted for in Yen back to U.S. dollars in order to prepare consolidated financial statements.

D) Writing down the value of an asset due to obsolescent.

A) Selling land at a cost greater than its original purchase price.

B) Recording an increase in the fair value of investments at year end.

C) Translating foreign operations accounted for in Yen back to U.S. dollars in order to prepare consolidated financial statements.

D) Writing down the value of an asset due to obsolescent.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

16

Why might income tax expense on the income statement differ from actual income taxes paid to the government?

A) There are timing differences to when income is recognized and there are items that may or may not be subject to taxation.

B) The IRS uses the accrual method of calculating income.

C) Financial statement preparers can use an estimated tax rate.

D) The IRS requires deferral of most expenses.

A) There are timing differences to when income is recognized and there are items that may or may not be subject to taxation.

B) The IRS uses the accrual method of calculating income.

C) Financial statement preparers can use an estimated tax rate.

D) The IRS requires deferral of most expenses.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

17

Future taxable income is characteristic of all of the following situations except:

A) where deferred tax assets result.

B) where deferred tax liabilities result.

C) where the tax basis of liabilities exceed the financial reporting basis.

D) where the tax basis of assets is less than financial reporting basis.

A) where deferred tax assets result.

B) where deferred tax liabilities result.

C) where the tax basis of liabilities exceed the financial reporting basis.

D) where the tax basis of assets is less than financial reporting basis.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

18

Firms use acquisition cost valuations and adjusted acquisition cost valuations for which of the following types of assets?

A) Assets that do not have fixed amounts of future cash flows.

B) Assets that have fixed amounts of future cash flows.

C) Assets with certain future economic benefits.

D) monetary

A) Assets that do not have fixed amounts of future cash flows.

B) Assets that have fixed amounts of future cash flows.

C) Assets with certain future economic benefits.

D) monetary

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

19

Permanent tax differences are revenues and expenses

A) that firms include in income tax returns, but do not appear in the income statement.

B) that are included in both the tax return and income statement, but in different accounting periods.

C) that firms include in the income statement, but do not appear in income tax returns.

D) that are not included in either the tax return or the income statement.

A) that firms include in income tax returns, but do not appear in the income statement.

B) that are included in both the tax return and income statement, but in different accounting periods.

C) that firms include in the income statement, but do not appear in income tax returns.

D) that are not included in either the tax return or the income statement.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

20

Current replacement cost represents

A) the amount a firm would have to pay currently to acquire an asset it now holds

B) the amount a firm would have to pay currently to acquire an asset it does not now hold

C) the amount a firm would have to pay in the future to acquire an asset it now holds

D) the amount a firm would have to pay to purchase a comparably depreciated version of the asset it now holds

A) the amount a firm would have to pay currently to acquire an asset it now holds

B) the amount a firm would have to pay currently to acquire an asset it does not now hold

C) the amount a firm would have to pay in the future to acquire an asset it now holds

D) the amount a firm would have to pay to purchase a comparably depreciated version of the asset it now holds

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

21

When recognizing deferred tax assets and liabilities, the income statement approach and the balance sheet approach yield identical results

A) when enacted tax rates applicable to future periods do not change.

B) when the firm recognizes no valuation allowance on deferred tax assets.

C) Both (a) and (b) are correct.

D) None of these answers is correct.

A) when enacted tax rates applicable to future periods do not change.

B) when the firm recognizes no valuation allowance on deferred tax assets.

C) Both (a) and (b) are correct.

D) None of these answers is correct.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

22

All of the following can be used to describe reliability of accounting information except:

A) biased.

B) credible.

C) verifiable.

D) supported by source documents.

A) biased.

B) credible.

C) verifiable.

D) supported by source documents.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

23

Historical costs include all of the following except:

A) acquisition costs for assets

B) net realizable values for assets.

C) adjusted acquisition costs for assets.

D) initial present value for assets and liabilities

A) acquisition costs for assets

B) net realizable values for assets.

C) adjusted acquisition costs for assets.

D) initial present value for assets and liabilities

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

24

If a portfolio manager had to estimate the fair value of publicly traded bonds, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

25

Reporting financial assets and liabilities at fair values also is referred to as:

A) historical cost.

B) acquisition cost.

C) mark-to-market.

D) mortgage-backed cost

A) historical cost.

B) acquisition cost.

C) mark-to-market.

D) mortgage-backed cost

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

26

If a portfolio manager had to estimate the fair value of real estate, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

27

What level are inputs for estimating fair values based on a firm's own assumptions about the fair value of an asset or a liability, such as using various data to estimate present values?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

28

If a portfolio manager had to estimate the fair value of privately placed bond issues, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

29

What level are inputs for estimating fair values are based on inputs that are readily available via prices for identical assets or liabilities in actively traded markets such as securities exchanges?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

30

What level are inputs for estimating fair values are those inputs include quoted prices for similar assets or liabilities in active or inactive markets, other observable information such as yield curves and price indexes, and other observable data such as market-based correlation estimates?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

31

U.S. GAAP, IFRS, and other major accounting standards are best characterized as

A) historical accounting models.

B) current value accounting models.

C) acquisition cost accounting models.

D) mixed attribute accounting models.

A) historical accounting models.

B) current value accounting models.

C) acquisition cost accounting models.

D) mixed attribute accounting models.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

32

If a portfolio manager had to estimate the fair value of illiquid mortgage-backed securities, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

33

If a portfolio manager had to estimate the fair value of investments in timber, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Levels 1 and 2.

C) Levels 2 or 3.

D) All levels would be applicable.

A) Level 1.

B) Levels 1 and 2.

C) Levels 2 or 3.

D) All levels would be applicable.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

34

Valuation methods that reflect current valuesor a combination of historical and current values include all of the following except:

A) fair value for assets and liabilities.

B) current replacement cost for assets.

C) net realizable value for assets.

D) adjusted acquisition costs for assets.

A) fair value for assets and liabilities.

B) current replacement cost for assets.

C) net realizable value for assets.

D) adjusted acquisition costs for assets.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

35

The existence of subjectivity in an asset valuation does not necessarily mean the valuation will not be reliable. All of the following are examples of this except:

A) where historical cost is used for accounts receivable, fixed assets, and other assets with values that remain relatively stable.

B) where market value is used for marketable equity securities, commodities, and financial assets are traded in liquid markets

C) where historical cost is used for LIFO inventory layers where inventory has seen an inflationary increase in costs.

D) where historical cost is used for internally generated intangible asset valuations.

A) where historical cost is used for accounts receivable, fixed assets, and other assets with values that remain relatively stable.

B) where market value is used for marketable equity securities, commodities, and financial assets are traded in liquid markets

C) where historical cost is used for LIFO inventory layers where inventory has seen an inflationary increase in costs.

D) where historical cost is used for internally generated intangible asset valuations.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

36

Relevant asset valuations refer to all of the following except:

A) they are timely.

B) they have the capacity to affect a user's decisions, based on the information.

C) they incorporate all available information.

D) they are always subjective.

A) they are timely.

B) they have the capacity to affect a user's decisions, based on the information.

C) they incorporate all available information.

D) they are always subjective.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

37

If a portfolio manager had to estimate the fair value of private equity funds invested in a young, privately-held start-up company, which of the following would he/she most likely identify as the level of inputs to determine this?

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

A) Level 1.

B) Level 2.

C) Level 3.

D) None of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

38

Approximately what percentage of assets reported under fair value by S&P 500 companies currently incorporate Level 3 inputs for fair value estimation?

A) 1%

B) 10%

C) 50%

D) 90%

A) 1%

B) 10%

C) 50%

D) 90%

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

39

Use of acquisition costs generally results in more reliable asset and liability valuations than do

A) appraised values.

B) unrealized cost values.

C) current values.

D) all of these.

A) appraised values.

B) unrealized cost values.

C) current values.

D) all of these.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

40

Firms may not include all income taxes for a period on the line for income tax expense in the income statement. Other places that income tax expenses may occur include all of the following except:

A) Discontinued Operations

B) Extraordinary Items

C) Other Comprehensive Income

D) Common Stock

A) Discontinued Operations

B) Extraordinary Items

C) Other Comprehensive Income

D) Common Stock

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

41

The amount that a company would have to pay today to acquire an asset it now holds is called ________________________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

42

Net income equals revenues plus ____________________ minus expenses and ____________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

43

Balance Sheet Equation

Refer to Balance Sheet Equation. JCP Company purchased marketable securities for $5,000 during the year, at the end of the year the company revalues the securities to $5,700. This revaluation would result in an increase to non-cash assets and ____________________________________________________________.

Refer to Balance Sheet Equation. JCP Company purchased marketable securities for $5,000 during the year, at the end of the year the company revalues the securities to $5,700. This revaluation would result in an increase to non-cash assets and ____________________________________________________________. Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

44

Stockholders' equity can be expanded into the following three accounts: contributed capital, retained earnings and _________________________________________________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

45

The difference between income tax payable and income tax expense is reported on the balance sheet as either ___________________________________ or a ___________________________________.

or

or

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

46

What valuation methods reflect historical cost? Discuss the advantages and disadvantages of valuing assets and liabilities using historical valuations.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

47

Acquisition costs includes all costs necessary to get an asset ready for its _________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

48

The application of GAAP requires firms to write down assets whose fair values decrease below their book values, but does not allow firms to revalue upward the values of assets whose fair values have increased. This asymmetric treatment rests on the ________________________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

49

____________________ assets and liabilities represent amounts of cash a firm can expect to receive or pay in the future.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

50

Revenues and expenses that firms include in both net income to shareholders and in taxable income, but in different periods are referred to as _____________________________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

51

Balance Sheet Equation

Refer to Balance Sheet Equation. The payment of dividends by a firm reduces cash and ______________________________.

Refer to Balance Sheet Equation. The payment of dividends by a firm reduces cash and ______________________________. Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

52

Balance Sheet Equation

Refer to Balance Sheet Equation. If ORP Corporation sells $25,000 of its product on account, it will see an increase in non-cash assets and ___________________________________.

Refer to Balance Sheet Equation. If ORP Corporation sells $25,000 of its product on account, it will see an increase in non-cash assets and ___________________________________. Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

53

Items, such as interest revenue on municipal bond holdings, that do not affect taxable income or income taxes paid in any year are referred to as _____________________________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

54

Firms recognize the reduction in service potential of assets such as building and equipment using the process of ____________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

55

Balance Sheet Equation

Refer to Balance Sheet Equation. ORP Corporation sells land with a book value of $12,000 for $9,000. This transaction results in ORP recording an increase in cash of $9,000, a decrease in non-cash assets of $12,000 and a decrease in ______________________________ of $3,000.

Refer to Balance Sheet Equation. ORP Corporation sells land with a book value of $12,000 for $9,000. This transaction results in ORP recording an increase in cash of $9,000, a decrease in non-cash assets of $12,000 and a decrease in ______________________________ of $3,000. Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

56

________________________________________ is the net amount that a firm would receive if it sold an asset or the net amount it would have to pay to settle a liability.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

57

What valuation methods reflect current values? Discuss the advantage(s) and disadvantage(s) of valuing assets and liabilities using current values.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

58

Balance Sheet Equation

Refer to Balance Sheet Equation. To recognize the cost of goods sold ORP Corporation will reduce retained earnings and reduce ______________________________.

or

Refer to Balance Sheet Equation. To recognize the cost of goods sold ORP Corporation will reduce retained earnings and reduce ______________________________.or

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

59

The amount initially paid to acquire an asset is called ______________________________.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

60

A change in the _________________________ or _________________________ will not change a preset series of cash flows, however it will change the present value of those cash flows.

or

or

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

61

On January 1, 2010, Starlight Company's balance sheet reported a deferred tax liability of $185,000 and a deferred tax asset of $99,900. The future taxable amounts that existed as of January 1, 2010 will reverse equally over the next four years beginning in 2010, while the future deductible amounts that existed as of January 1, 2010 will reverse equally over the next three years beginning in 2010. The enacted income tax rate for all tax years as of January 1, 2010 was 37%. On February 1, 2010, the tax laws were amended resulting in income tax rates of 38% for 2010 and 2011; the income tax rate will be 40% for tax years 2012 and later.

Required:

Prepare the journal entry on February 1, 2010 to record the impact of the amended income tax rates.

Required:

Prepare the journal entry on February 1, 2010 to record the impact of the amended income tax rates.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

62

Fellsmere Company's income tax return shows income taxes for 2010 of $35,000. The firm reports deferred tax assets before any valuation allowance of $32,600 at the beginning of 2010 and $35,200 at the end of 2010. It reports deferred tax liabilities of $26,900 at the beginning of 2010 and $24,300 at the end of 2010.

Required:

a. Assume for this part that the valuation allowance on the deferred tax assets totaled

$14,400 at the beginning of 2010 and $15,100 at the end of 2010. Compute the amount

of income tax expense for 2010.

b. Assume for this part that the valuation allowance on the deferred tax assets totaled

$14,400 at the beginning of 2010 and $12,700 at the end of 2010. Compute the amount

of income tax expense for 2010.

Required:

a. Assume for this part that the valuation allowance on the deferred tax assets totaled

$14,400 at the beginning of 2010 and $15,100 at the end of 2010. Compute the amount

of income tax expense for 2010.

b. Assume for this part that the valuation allowance on the deferred tax assets totaled

$14,400 at the beginning of 2010 and $12,700 at the end of 2010. Compute the amount

of income tax expense for 2010.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

63

The analytical framework used to evaluate transactions is reproduced below:

Using this analytical framework indicate the effect of each of the following transactions for TX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for TX Corporation: Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

64

Discuss the two principal reasons income before taxes for financial reporting differs from taxable income.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

65

Accord Inc. income tax return shows taxes currently payable for 2011 of $85,000. The company reported deferred tax assets of $35,000 at the end of 2010 and $24,000 at the end of 2011. Accord reported deferred tax liabilities of $48,000 at the end of 2011 and $54,000 at the end of 2011.

Determine the amount of income tax expense reported by Accord for 2011.

Determine the amount of income tax expense reported by Accord for 2011.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

66

For some transactions GAAP requires that value changes are recognized on the balance sheet and the income statement when they occur, even if not realized. Discuss what types of transactions get this type of treatment and the logic behind this accounting.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

67

The financial statement disclosures for Able Company, a retail chain, revealed the following information regarding the firm's income taxes:

Required:

a. Assuming that Able had no significant permanent differences between book income

and taxable income, did income before taxes for financial reporting exceed or fall

short of taxable income for 2010? Explain.

b. Did income before taxes for financial reporting exceed or fall short of taxable

income for 2011? Explain.

c. Will the adjustment to net income for deferred taxes to compute cash flow from

operations in the statement of cash flows result in an addition or a subtraction for

2010? For 2011?

d. Able does not contract with an insurance agency for property and liability insurance;

instead, it self-insures. Able recognizes an expense and a liability each year for

financial reporting to reflect its average expected long-term property and liability

losses. When it experiences an actual loss, it charges that loss against the liability. The

income tax law permits self-insured firms to deduct such losses only in the year sustained.

Why are deferred taxes related to self-insurance disclosed as a deferred tax

asset instead of a deferred tax liability? Suggest reasons for the direction of the

change in amounts for this deferred tax asset between 2009 and 2011.

e. Able treats certain storage and other inventory costs as expenses in the year incurred

for financial reporting but must include these in inventory for tax reporting. Why

are deferred taxes related to inventory disclosed as a deferred tax asset? Suggest reasons

for the direction of the change in amounts for this deferred tax asset between

2009 and 2011.

f. Firms must recognize expenses related to postretirement health care and pension

obligations as employees provide services, but claim an income tax deduction only

when they make cash payments under the benefit plan. Why are deferred taxes

related to health care obligation disclosed as a deferred tax asset? Why are deferred

taxes related to pensions disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for these deferred tax items between 2009 and

2011.

g. Firms must recognize expenses related to uncollectible accounts when they recognize

sales revenues, but claim an income tax deduction when they deem a particular

customer's accounts uncollectible. Why are deferred taxes related to this item disclosed

as a deferred tax asset? Suggest reasons for the direction of the change in

amounts for this deferred tax asset between 2009 and 2011.

h. Able uses the straight-line depreciation method for financial reporting and accelerated

depreciation methods for income tax purposes. Why are deferred taxes

related to depreciation disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for this deferred tax liability between 2009

and 2011.

Required:a. Assuming that Able had no significant permanent differences between book income

and taxable income, did income before taxes for financial reporting exceed or fall

short of taxable income for 2010? Explain.

b. Did income before taxes for financial reporting exceed or fall short of taxable

income for 2011? Explain.

c. Will the adjustment to net income for deferred taxes to compute cash flow from

operations in the statement of cash flows result in an addition or a subtraction for

2010? For 2011?

d. Able does not contract with an insurance agency for property and liability insurance;

instead, it self-insures. Able recognizes an expense and a liability each year for

financial reporting to reflect its average expected long-term property and liability

losses. When it experiences an actual loss, it charges that loss against the liability. The

income tax law permits self-insured firms to deduct such losses only in the year sustained.

Why are deferred taxes related to self-insurance disclosed as a deferred tax

asset instead of a deferred tax liability? Suggest reasons for the direction of the

change in amounts for this deferred tax asset between 2009 and 2011.

e. Able treats certain storage and other inventory costs as expenses in the year incurred

for financial reporting but must include these in inventory for tax reporting. Why

are deferred taxes related to inventory disclosed as a deferred tax asset? Suggest reasons

for the direction of the change in amounts for this deferred tax asset between

2009 and 2011.

f. Firms must recognize expenses related to postretirement health care and pension

obligations as employees provide services, but claim an income tax deduction only

when they make cash payments under the benefit plan. Why are deferred taxes

related to health care obligation disclosed as a deferred tax asset? Why are deferred

taxes related to pensions disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for these deferred tax items between 2009 and

2011.

g. Firms must recognize expenses related to uncollectible accounts when they recognize

sales revenues, but claim an income tax deduction when they deem a particular

customer's accounts uncollectible. Why are deferred taxes related to this item disclosed

as a deferred tax asset? Suggest reasons for the direction of the change in

amounts for this deferred tax asset between 2009 and 2011.

h. Able uses the straight-line depreciation method for financial reporting and accelerated

depreciation methods for income tax purposes. Why are deferred taxes

related to depreciation disclosed as a deferred tax liability? Suggest reasons for the

direction of the change in amounts for this deferred tax liability between 2009

and 2011.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

68

When income tax expense differs from income taxes currently payable on taxable income companies recognize deferred tax assets and deferred tax liabilities. What type of event would create a deferred tax asset and deferred tax liability?

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

69

The following problem requires present value information:

Biotech sold a patent on a new blood analyzer to Pharma. The sales agreement which was signed on January 1, 2009 requires Pharma to pay Biotech $1 million immediately. In addition, Pharma is required to pay $600,000 each December 31 for 20 years starting with December 31, 2009. Pharma and Biotech judge that a 10 percent is an appropriate interest rate for this arrangement.

Biotech sold a patent on a new blood analyzer to Pharma. The sales agreement which was signed on January 1, 2009 requires Pharma to pay Biotech $1 million immediately. In addition, Pharma is required to pay $600,000 each December 31 for 20 years starting with December 31, 2009. Pharma and Biotech judge that a 10 percent is an appropriate interest rate for this arrangement.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

70

Deferred tax assets and liabilities are created due to temporary differences between the tax and financial reporting basis of certain assets and liabilities. Discuss which scenarios result in a deferred tax asset and which result in deferred tax liabilities.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

71

On December 31, 2009, Loran Corporation reported a deferred tax liability totaling $12,000, resulting from depreciation timing differences pertaining to a depreciable asset purchased during 2009. Loran uses straight-line depreciation over four years for GAAP (book) purposes; for tax purposes, the depreciation deduction is 40% of cost during 2009, 30% of cost during 2010, 20% of cost during 2011, and 10% of cost during 2012. During 2010, Loran expensed $75,000 of warranty costs that will be deducted for tax purposes in future years. Loran also accrued revenue totaling $150,000 which is taxable in 2011. Loran's GAAP (book) income before taxes during 2010 totaled $397,700. The marginal income tax rate is 40% for all years.

Required:

(1) What is the taxable income?

(2) Prepare the journal entry to record income tax expense for the year ended December 31, 2010.

Required:

(1) What is the taxable income?

(2) Prepare the journal entry to record income tax expense for the year ended December 31, 2010.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

72

Plaxo Corporation has a tax rate of 35% and uses the straight-line method of depreciation for its equipment, which has a useful life of four years. Tax legislation requires the company to depreciate this type of equipment using the following schedule: year 1- 50%, year 2 - 30%, year 3 - 15% and year 4 - 5%. In 2011 Plaxo purchases a piece of equipment with a four year life and an original cost of $100,000. Discuss how this transaction will effect Plaxo's income taxes in 2011.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

73

There are three valuation methods that reflect historical values: acquisition cost, adjusted acquisition cost, and present value of cash flows using historical interest rates. For each of three methods discuss what the valuation represents and provide an example of a balance sheet item that is valued using the method. In addition, for each of the three methods valuation methods explain its advantages and disadvantages.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

74

The analytical framework used to evaluate transactions is reproduced below:

Using this analytical framework indicate the effect of each of the following transactions for CX Corporation:

Using this analytical framework indicate the effect of each of the following transactions for CX Corporation: Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

75

H. Solo Company purchased a new piece of equipment with a list price of $175,000 and subject to a 5 percent discount if paid within 45 days. H. Solo paid within the discount period. The company also paid $1,500 to obtain title to the equipment and $600 as the license fee for the first year of operation. It paid $2,500 to level the area in which the equipment would be located and $12,500 to relocate other equipment that would have interfered with the proper operation of the new equipment. H. Solo paid $400 for property and liability insurance for the first year of operation. What is the acquisition cost of this equipment that H. Solo should record in its accounting records? Indicate the treatment of any amount not included in acquisition cost.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

76

Jurgen Company's income tax return shows income taxes for 2010 of $75,000 (that is, $75,000 is owed for 2010). For financial reporting, the firm reports deferred tax assets of $67,900 at the beginning of 2010 and $63,600 at the end of 2010. It reports deferred tax liabilities of $53,600 at the beginning of 2010 and $59,400 at the end of 2010.

Required:

a. Compute the amount of income tax expense for 2010.

b. Assume for this part that the firm's deferred tax assets are as stated above for 2010 but that its deferred tax liabilities were $83,500 at the beginning of 2010 and $72,100

at the end of 2010. Compute the amount of income tax expense for 2010.

c. Explain contextually why income tax expense is higher than taxes owed in Part a and lower than taxes owed in Part b.

Required:

a. Compute the amount of income tax expense for 2010.

b. Assume for this part that the firm's deferred tax assets are as stated above for 2010 but that its deferred tax liabilities were $83,500 at the beginning of 2010 and $72,100

at the end of 2010. Compute the amount of income tax expense for 2010.

c. Explain contextually why income tax expense is higher than taxes owed in Part a and lower than taxes owed in Part b.

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

78

Match between columns

Unlock Deck

Unlock for access to all 77 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 77 flashcards in this deck.