Deck 16: Duration and Bond Portfolio Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

You are considering the purchase of two $1,000 bonds,both issued by Tranig Corp.Your expectation is that interest rates will drop,and you want to buy the bond which provides the maximum capital gains potential.The first Tranig bond has a coupon rate of 6% with five years to maturity,while the second has a coupon rate of 9% and comes due six years from now.If market rates of interest are 8% for both bonds,which bond has the best price potential? (Use duration to answer the question. )

Coupon rate 6% Coupon rate 9%

Coupon rate 9%

Coupon rate 6%

Coupon rate 9% Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/55

Play

Full screen (f)

Deck 16: Duration and Bond Portfolio Management

1

The duration of a 20-year zero-coupon bond is equal to the maturity,regardless of the market rate.

True

2

The duration of a ten-year,10%,$1,000 bond at a market rate of 6% is exactly equal to the duration of the same bond at a 14% market rate.

False

3

As the maturity or duration of a bond increases,the impact on price of any changes in interest rates increases at a decreasing rate.

True

4

Terminal wealth analysis is the process of measuring the effects of shifting market rates on bond prices.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

5

High coupon bonds will usually have higher durations than low coupon bonds of the same maturity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

6

A zero-coupon bond has a duration equal to its maturity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

7

Duration times the reinvestment rate will give the approximate change in bond price for a 1% change in interest rates.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

8

Duration analysis is subject to the assumption that all interest income can be reinvested at the market rate of interest.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

9

Duration will not help international bond managers choose bonds for their portfolios because of the foreign exchange risk.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

10

Macaulay duration is a bond's weighted average life based on present value of cash flows.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

11

The actual yield to maturity an investor receives becomes more of a function of the reinvestment rate the shorter the maturity of the bond.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

12

Immunization protects the portfolio value against upward movement in interest rates but not downward movement in interest rates.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

13

Terminal wealth analysis for a zero-coupon bond is irrelevant.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

14

Duration is a useful number because it combines the effects of maturity,coupon,and market rates to indicate how the price of the bond will change with a change in interest rates.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

15

Weighted average life is the most representative value for effective bond life.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

16

Terminal wealth analysis is one way of analyzing the effect of the reinvestment rate risk.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

17

As the yield to maturity on a bond increases,the duration also increases because of the effect of present value on duration.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

18

For two bonds with equal coupons,duration would be higher for the bond with the shortest maturity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

19

Immunization is the process of measuring bond price sensitivity to interest rate changes.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

20

There is an inverse relationship between interest rates and bond values,and between the amount of coupon payments and weighted average life.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

21

Immunization is the process of ________ to ensure an outcome.

A)measuring bond price sensitivity to interest rates

B)tying all investment decisions to a particular market interest rate

C)tying all investment decisions to a duration period

D)none of the above

A)measuring bond price sensitivity to interest rates

B)tying all investment decisions to a particular market interest rate

C)tying all investment decisions to a duration period

D)none of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

22

The value of a bond may be expressed as the sum of:

A)the interest payments and the maturity value.

B)the present value of the par value and the present value of the sum of the interest payments.

C)the present value of the maturity value and the sum of the present values of the interest payments.

D)None of the above

A)the interest payments and the maturity value.

B)the present value of the par value and the present value of the sum of the interest payments.

C)the present value of the maturity value and the sum of the present values of the interest payments.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

23

The highest duration and maximum price sensitivity relative to years to maturity are produced by:

A)a coupon rate equal to the market rate.

B)a low coupon rate.

C)a zero-coupon.

D)None of the above

A)a coupon rate equal to the market rate.

B)a low coupon rate.

C)a zero-coupon.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

24

When duration of a coupon paying bond is plotted against years to maturity on the X axis,the line:

A)is linear.

B)is concave.

C)is convex.

D)is linear at a 45 degree angle.

A)is linear.

B)is concave.

C)is convex.

D)is linear at a 45 degree angle.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

25

In general,duration is the number of years,on a future-value basis,that it takes to recover an initial investment in a bond.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

26

Duration equals maturity if:

A)all cash flows are paid at the end of the year.

B)the coupon rate equals the market rate.

C)the bond is a zero-coupon bond.

D)More than one of the above

A)all cash flows are paid at the end of the year.

B)the coupon rate equals the market rate.

C)the bond is a zero-coupon bond.

D)More than one of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

27

The duration of a 20-year,$1,000 bond at a COUPON rate of 8% is _________ the duration of an identical bond at a coupon rate of 6%.

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

28

Duration is:

A)always longer than maturity.

B)always the same as maturity.

C)normally shorter than maturity.

D)always shorter than maturity.

A)always longer than maturity.

B)always the same as maturity.

C)normally shorter than maturity.

D)always shorter than maturity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

29

One of the problems with duration is that it often assumes a parallel shift in yield curves.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

30

Factors which influence the relationship between duration and maturity include all of the following EXCEPT:

A)the face value of the bond.

B)the coupon rate of the bond.

C)the number of years to maturity.

D)All of the above are factors

A)the face value of the bond.

B)the coupon rate of the bond.

C)the number of years to maturity.

D)All of the above are factors

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

31

Duration is affected primarily by:

A)the maturity of the bond.

B)the market rate of interest.

C)the coupon rate.

D)All of the above

A)the maturity of the bond.

B)the market rate of interest.

C)the coupon rate.

D)All of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

32

Weighted average life refers to the time period over which the coupon payments and maturity payment on a bond are recovered.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

33

One of the major criticisms of duration analysis is:

A)the difficulty of measuring the market rate of interest.

B)the assumption that long-term and short-term interest rates move by equal amounts.

C)the assumption that long-duration bonds are more price-sensitive than short-duration bonds.

D)None of the above

A)the difficulty of measuring the market rate of interest.

B)the assumption that long-term and short-term interest rates move by equal amounts.

C)the assumption that long-duration bonds are more price-sensitive than short-duration bonds.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

34

The only difference between the simple weighted average life of a bond and duration of a bond is:

A)the timing of interest payments.

B)that duration involves the present value of individual cash flows.

C)that duration involves the using of the stated value of individual cash flows.

D)None of the above

A)the timing of interest payments.

B)that duration involves the present value of individual cash flows.

C)that duration involves the using of the stated value of individual cash flows.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

35

It is possible that a bond with a shorter maturity than another bond may actually have a longer duration and be more sensitive to interest rate changes.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

36

The duration of a bond is determined by a combination of the maturity date and value,and:

A)the pattern of coupon payments.

B)the call premium.

C)the put premium.

D)None of the above

A)the pattern of coupon payments.

B)the call premium.

C)the put premium.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

37

Duration is used primarily as a measure of:

A)the relationship between coupon rate and bond rating.

B)bond price-sensitivity to interest rate changes.

C)the present value of investment inflows.

D)None of the above

A)the relationship between coupon rate and bond rating.

B)bond price-sensitivity to interest rate changes.

C)the present value of investment inflows.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

38

One of the benefits of zero-coupon bonds is that they lock in a compound rate of return (or reinvestment rate)for the life of the bond,if held to maturity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

39

The duration on an 8%,25-year bond is ______ the duration on a 9%,30-year bond.

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

40

The duration of a 40-year,$1,000 bond at a market rate of 4% is _________ the duration of an identical bond at a market rate of 6%.

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

A)greater than

B)less than

C)equal to

D)there is not enough information to tell

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

41

What type of bond investor would probably be least concerned about a drop in market interest rates?

A)Individuals who spend their interest income

B)Individuals who are building a retirement portfolio

C)Pension fund managers

D)All of the above would have cause for concern

A)Individuals who spend their interest income

B)Individuals who are building a retirement portfolio

C)Pension fund managers

D)All of the above would have cause for concern

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

42

For all bonds of equal risk,the type of bond that had the greatest duration,and therefore the greatest price sensitivity,is:

A)Treasury bonds.

B)zero-coupon bonds.

C)corporate bonds.

D)long-term government bonds.

A)Treasury bonds.

B)zero-coupon bonds.

C)corporate bonds.

D)long-term government bonds.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

43

Volatile high interest rates have directly caused more emphasis on duration analysis because:

A)investors have responded to the new environment by switching from short-term to longer-term securities.

B)prices of longer-term bonds are more sensitive to shifts in interest rates than shorter-term bonds.

C)duration analysis measures the degree of bond price sensitivity.

D)All of the above

A)investors have responded to the new environment by switching from short-term to longer-term securities.

B)prices of longer-term bonds are more sensitive to shifts in interest rates than shorter-term bonds.

C)duration analysis measures the degree of bond price sensitivity.

D)All of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

44

A terminal wealth table generates the ending value of the investment at the end of the year,assuming that the bond:

A)has a maturity date corresponding to that year.

B)has a maturity date corresponding to the next year.

C)is a zero-coupon bond.

D)None of the above

A)has a maturity date corresponding to that year.

B)has a maturity date corresponding to the next year.

C)is a zero-coupon bond.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

45

Under terminal wealth analysis,the greater the period to maturity,

A)the greater the shift in interest rates.

B)the greater the effect of a decrease in interest rates.

C)the greater the effect of any shift in interest rates.

D)None of the above

A)the greater the shift in interest rates.

B)the greater the effect of a decrease in interest rates.

C)the greater the effect of any shift in interest rates.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

46

Compute the duration for the data in this problem using a discount rate of 12%.

A)3.00 years

B)2.95 years

C)2.85 years

D)2.75 years

E)2.65 years

A)3.00 years

B)2.95 years

C)2.85 years

D)2.75 years

E)2.65 years

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

47

You have invested $1,000 in a 12% coupon bond that matures in three years.You are investing the interest income in a fund earning 8%.At the end of three years,what will be your portfolio sum?

A)$1,120.00

B)$1,249.60

C)$1,360.00

D)$1,389.57

E)$1,540.73

A)$1,120.00

B)$1,249.60

C)$1,360.00

D)$1,389.57

E)$1,540.73

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

48

You are considering the purchase of two $1,000 bonds,both issued by Tranig Corp.Your expectation is that interest rates will drop,and you want to buy the bond which provides the maximum capital gains potential.The first Tranig bond has a coupon rate of 6% with five years to maturity,while the second has a coupon rate of 9% and comes due six years from now.If market rates of interest are 8% for both bonds,which bond has the best price potential? (Use duration to answer the question. )

Coupon rate 6% Coupon rate 9%

Coupon rate 6%

Coupon rate 9% Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

49

Under which of the following circumstances would terminal wealth analysis NOT be relevant?

A)When the bond is sold prior to maturity

B)When market interest rates rise above the coupon rate

C)Terminal wealth analysis is ALWAYS relevant

D)None of the above

A)When the bond is sold prior to maturity

B)When market interest rates rise above the coupon rate

C)Terminal wealth analysis is ALWAYS relevant

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

50

Duration represents the weighted average life of a bond where the weights are based on the:

A)future value of the individual cash flows relative to the present value of the total cash flows.

B)present value of the individual cash flows relative to the future value of the individual cash flows.

C)present value of the individual cash flows relative to the present value of the total individual cash flows.

D)future value of the individual cash flows relative to the future value of the individual cash flows.

A)future value of the individual cash flows relative to the present value of the total cash flows.

B)present value of the individual cash flows relative to the future value of the individual cash flows.

C)present value of the individual cash flows relative to the present value of the total individual cash flows.

D)future value of the individual cash flows relative to the future value of the individual cash flows.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

51

Duration is influenced by everything except:

A)maturity.

B)market rate of interest.

C)coupon rate on the bond.

D)the issuer of the bonD.The three factors that determine the value of duration are the maturity of the bond,the market rate of interest,and the coupon rate.Duration is positively correlated with maturity but moves in the opposite direction of market rates of interest and coupon rates;that is,the higher the market rate of interest or the coupon rate,the lower the duration.

A)maturity.

B)market rate of interest.

C)coupon rate on the bond.

D)the issuer of the bonD.The three factors that determine the value of duration are the maturity of the bond,the market rate of interest,and the coupon rate.Duration is positively correlated with maturity but moves in the opposite direction of market rates of interest and coupon rates;that is,the higher the market rate of interest or the coupon rate,the lower the duration.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

52

Assume you buy a 20-year,$1,000 par value zero-coupon bond that provides a 12% yield to maturity.Almost immediately after you buy the bond,yields decrease to 9%.What will be the percentage gain on the investment?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

53

Duration is:

A)positively correlated with interest rates and coupon rates but moves in the opposite direction of maturity.

B)negatively correlated with maturity but moves in the same direction as market rates of interest and coupon rates.

C)positively correlated with maturity but moves in the opposite direction of market rates of interest and coupon rates.

D)None of the above

A)positively correlated with interest rates and coupon rates but moves in the opposite direction of maturity.

B)negatively correlated with maturity but moves in the same direction as market rates of interest and coupon rates.

C)positively correlated with maturity but moves in the opposite direction of market rates of interest and coupon rates.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

54

The process of measuring the effect of a shift in market interest rates on the value of an investment is called:

A)duration analysis.

B)immunization.

C)terminal wealth analysis.

D)None of the above

A)duration analysis.

B)immunization.

C)terminal wealth analysis.

D)None of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

55

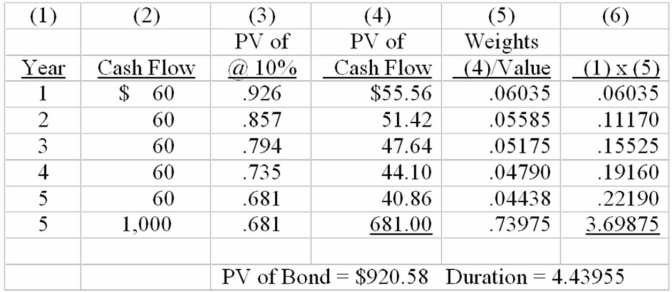

Compute the duration for a bond with an 8% coupon rate,maturing in five years.A discount rate of 10% should be applied.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 55 flashcards in this deck.