Deck 14: Partnerships: Ownership Changes and Liquidations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The partnership of Able, Bower, and Cramer was liquidated. The partners have shared profits and losses in the ratio of 2:4:4. Prior to liquidation, their capital balances were the following*:

* Deficit shown in parentheses

* Deficit shown in parentheses

Cash totaled $20,000, with liabilities amounting to $30,000. A review of the individual partners' personal financial status reveals the following:

Required:

Required:

Prepare a worksheet to liquidate the partnership.

* Deficit shown in parenthesesCash totaled $20,000, with liabilities amounting to $30,000. A review of the individual partners' personal financial status reveals the following:

Required:Prepare a worksheet to liquidate the partnership.

Question

Partners Able, Baker, and Chapman have the following personal assets, personal liabilities, and partnership capital balances:  Assume profits and losses are allocated equally.

Assume profits and losses are allocated equally.

After applying the doctrine of marshaling of assets, the capital balances for Able, Baker, and Chapman, respectively, would be

A) $50,000, $(2,000), and $58,000.

B) $48,000, 0, and $58,000.

C) $49,000, 0, and $57,000.

D) $34,000, 0, and $54,000.

Assume profits and losses are allocated equally.After applying the doctrine of marshaling of assets, the capital balances for Able, Baker, and Chapman, respectively, would be

A) $50,000, $(2,000), and $58,000.

B) $48,000, 0, and $58,000.

C) $49,000, 0, and $57,000.

D) $34,000, 0, and $54,000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Martel, Tusk, and Davis are partners with present capital balances of $40,000, $50,000, and $20,000, respectively. The partners share profits and losses according to the following percentages: 60% for Martel, 30% for Tusk, and 10% for Davis. Frank is to join the partnership upon contributing $40,000 to the partnership in exchange for a 25% interest in capital and a 20% interest in profits and losses. An appraisal of the existing partnerships' assets reveals the following:

Required:

Required:

Calculate the capital balances for each individual in the new partnership assuming use of the bonus and goodwill methods.

Required:Calculate the capital balances for each individual in the new partnership assuming use of the bonus and goodwill methods.

Question

Question

Question

The partnership of Alt, Brown, and Carns has total assets and liabilities of $30,000 and $25,000, respectively. Information relating to the partners is as follows:

Required:

Required:

a.

Assuming that the Uniform Partnership Act is applicable, indicate how the partners' personal assets would be distributed.

b.

Assuming that federal bankruptcy laws are applicable, indicate how the partners' personal assets would be distributed.

c.

Assume that the partnership had a deficit of $10,000, allocated among Alt, Brown, and Carns as follows: $2,000 surplus, $7,000 deficit, and $5,000 deficit, respectively. Indicate how the deficit would be satisfied when bankruptcy laws are applicable.

Required: a.

Assuming that the Uniform Partnership Act is applicable, indicate how the partners' personal assets would be distributed.

b.

Assuming that federal bankruptcy laws are applicable, indicate how the partners' personal assets would be distributed.

c.

Assume that the partnership had a deficit of $10,000, allocated among Alt, Brown, and Carns as follows: $2,000 surplus, $7,000 deficit, and $5,000 deficit, respectively. Indicate how the deficit would be satisfied when bankruptcy laws are applicable.

Question

Merz, Dechter, and Flowers are partners in a partnership and share profits and losses 40%, 40%, and 20%, respectively. The partners have agreed to liquidate the partnership and anticipate that liquidation expenses will total $14,000. Prior to the liquidation, the partnership balance sheet reflects the following book values:

Required:

Required:

Assuming that the actual liquidation expenses are $20,000 and that noncash assets are sold for $160,000, determine how the assets will be distributed. Flowers has net personal assets of $10,000.

Required:Assuming that the actual liquidation expenses are $20,000 and that noncash assets are sold for $160,000, determine how the assets will be distributed. Flowers has net personal assets of $10,000.

Question

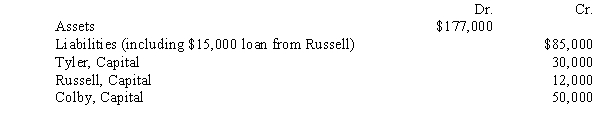

The Tyler, Russell, and Colby partnership is liquidating. The three partners share profits and losses equally. The following is the post-closing trial balance for the partnership:

Required:

Required:

Draft a predistribution plan for the partnership liquidation and provide a schedule of payments.

Required:Draft a predistribution plan for the partnership liquidation and provide a schedule of payments.

Question

Question

Question

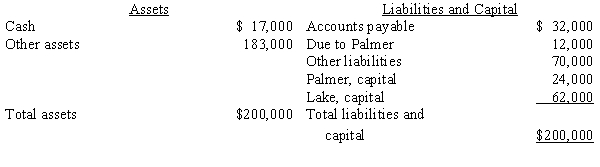

On July 1, 20X9, the Crawford Company has the following balance sheet:

As of July 1, 20X9, the partners have personal net worth as follows:

As of July 1, 20X9, the partners have personal net worth as follows:

The personal net worth of each partner does not include any amounts due to or from the partnership.

Required:

Assume the other assets are sold for $103,000 after incurring liquidation expenses of $4,000. After liquidation of the partnership, determine how much is available to Lake's unsatisfied personal creditors based on the following:

a.

Application of the Uniform Partnership Act

b.

Application of common law

As of July 1, 20X9, the partners have personal net worth as follows:The personal net worth of each partner does not include any amounts due to or from the partnership.

Required:

Assume the other assets are sold for $103,000 after incurring liquidation expenses of $4,000. After liquidation of the partnership, determine how much is available to Lake's unsatisfied personal creditors based on the following:

a.

Application of the Uniform Partnership Act

b.

Application of common law

Question

Question

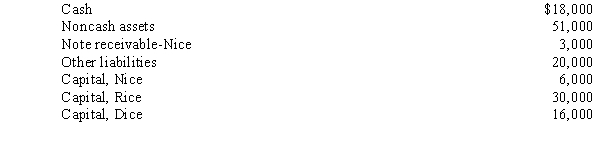

The Nice, Rice, and Dice Partnership has not been successful. The partners have determined they must liquidate their partnership. The partners have agreed to liquidate the partnership and anticipate that liquidation expenses will total $1,000. Prior to the liquidation, the partnership balance sheet reflects the following book values:

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner's personal net worth reveals the following:

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner's personal net worth reveals the following:

The following transactions occur:

The following transactions occur:

a.

Assets having a book value of $40,000 are sold for $22,000 cash

b.

Liabilities are paid, where possible

c.

Partners contribute from their personal net worth, according to UPA requirements and Marshaling of Assets concepts

Required:

Prepare liquidation schedule and determine how the available assets will be distributed using a schedule of safe payments.

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner's personal net worth reveals the following: The following transactions occur: a.

Assets having a book value of $40,000 are sold for $22,000 cash

b.

Liabilities are paid, where possible

c.

Partners contribute from their personal net worth, according to UPA requirements and Marshaling of Assets concepts

Required:

Prepare liquidation schedule and determine how the available assets will be distributed using a schedule of safe payments.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/48

Play

Full screen (f)

Deck 14: Partnerships: Ownership Changes and Liquidations

1

If goodwill is traceable only to the previous partners,

A) the book value of the previous partnership plus the investment of the incoming partner will be greater than the fair market value of the partnership as suggested by the incoming partner's investment.

B) the new partner's initial capital balance is equal to his or her investment in the partnership.

C) existing assets of the previous partnership will never be revalued.

D) none of the above.

A) the book value of the previous partnership plus the investment of the incoming partner will be greater than the fair market value of the partnership as suggested by the incoming partner's investment.

B) the new partner's initial capital balance is equal to his or her investment in the partnership.

C) existing assets of the previous partnership will never be revalued.

D) none of the above.

B

2

When a new partner is admitted to a partnership under the goodwill method, an original partner's capital account may be adjusted for

A) a proportionate share of the incoming partner's investment.

B) his or her share of previously unrecorded intangible assets traceable to the original partners.

C) his or her share of previously unrecorded intangible assets traceable to the incoming partner.

D) none of the above.

A) a proportionate share of the incoming partner's investment.

B) his or her share of previously unrecorded intangible assets traceable to the original partners.

C) his or her share of previously unrecorded intangible assets traceable to the incoming partner.

D) none of the above.

B

3

Palit buys Quincy's partnership interest in the Q-R-S partnership. Quincy thus retires, leaving Reale and Susien as Palit's co-partners. Prior to Palit entering the partnership, Quincy, Reale, and Susien split profits and losses equally. Palit pays $75,000 for Quincy's capital which, at the time, totaled $60,000. No revaluation of partnership assets or liabilities occurs at the time. In recording this event on the partnership books

A) Goodwill is booked based on the book value/fair value difference.

B) $7,500 bonuses are added to Reale and Susien capital.

C) $5,000 bonuses are added to Quincy, Real, and Susien capital.

D) Palit capital is created in the amount of $60,000.

A) Goodwill is booked based on the book value/fair value difference.

B) $7,500 bonuses are added to Reale and Susien capital.

C) $5,000 bonuses are added to Quincy, Real, and Susien capital.

D) Palit capital is created in the amount of $60,000.

D

4

Assume the existing capital of a partnership is $100,000. Two partners currently own the partnership and split profits 40/60. A new partner is to be admitted and will contribute net assets with a fair value of $50,000. An appraisal of existing partnership assets indicates accounts receivable overstated by $10,000, inventory overstated by $12,000 and land understated by $25,000. What is the total capital of the new partnership if the bonus method is being used?

A) $153,000

B) $128,000

C) $175,000

D) $150,000

A) $153,000

B) $128,000

C) $175,000

D) $150,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

5

Scenario 14-1

Callie is admitted to the Adams & Beal Partnership under the bonus method. Callie contributes cash of $20,000 and non-cash assets with a market value of $30,000 and book value of $15,000 in exchange for a 20% ownership interest in the new partnership. Prior to the admission of Callie, the capital of the existing partnership was $130,000 and an appraisal showed the partnership net assets were fairly stated.

Refer to Scenario 14-1. What will be Callie's initial capital balance?

A) $36,000

B) $50,000

C) $35,000

D) $30,000

Callie is admitted to the Adams & Beal Partnership under the bonus method. Callie contributes cash of $20,000 and non-cash assets with a market value of $30,000 and book value of $15,000 in exchange for a 20% ownership interest in the new partnership. Prior to the admission of Callie, the capital of the existing partnership was $130,000 and an appraisal showed the partnership net assets were fairly stated.

Refer to Scenario 14-1. What will be Callie's initial capital balance?

A) $36,000

B) $50,000

C) $35,000

D) $30,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

6

If an existing partner withdraws from a partnership,

A) his or her interest may be sold to the partnership or an individual partner.

B) the consideration received for that partner's interest may suggest the existence of undervalued existing assets and/or goodwill.

C) either the bonus or the goodwill method may be used to record the transaction if the partnership acquires the withdrawing partner's interest.

D) all of the above.

A) his or her interest may be sold to the partnership or an individual partner.

B) the consideration received for that partner's interest may suggest the existence of undervalued existing assets and/or goodwill.

C) either the bonus or the goodwill method may be used to record the transaction if the partnership acquires the withdrawing partner's interest.

D) all of the above.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

7

Changes in partnership ownership are presumed to be arm's length transactions that may require which of the following actions?

A) recognitions of goodwill to existing partners

B) revaluation of existing partnership assets

C) recognition of goodwill or other intangible assets attributable to the incoming partner

D) all of the above are possible

A) recognitions of goodwill to existing partners

B) revaluation of existing partnership assets

C) recognition of goodwill or other intangible assets attributable to the incoming partner

D) all of the above are possible

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

8

If goodwill is suggested by the consideration paid to a withdrawing partner,

A) only the goodwill traceable to the withdrawing partner may be recorded.

B) goodwill traceable to the original partnership is allocated among the partners according to their respective interests in capital.

C) the goodwill traceable to the withdrawing partner represents the difference between the partner's capital balance and the consideration he or she receives.

D) none of the above.

A) only the goodwill traceable to the withdrawing partner may be recorded.

B) goodwill traceable to the original partnership is allocated among the partners according to their respective interests in capital.

C) the goodwill traceable to the withdrawing partner represents the difference between the partner's capital balance and the consideration he or she receives.

D) none of the above.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

9

Under the bonus method, when a new partner is admitted to the partnership, the total capital of the new partnership is equal to:

A) the book value of the previous partnership plus the fair market value of the consideration paid to the existing partnership by the incoming partner

B) the book value of the previous partnership plus any necessary asset write ups from book value to market value plus the fair market value of the consideration paid to the existing partnership by the incoming partner

C) the book value of the previous partnership minus any asset write downs from book to market value plus the fair market value of the consideration paid to the existing partnership by the incoming partner

D) the fair market value of the new partnership as implied by the value of the incoming partner's consideration in exchange for an ownership percentage in the new partnership

A) the book value of the previous partnership plus the fair market value of the consideration paid to the existing partnership by the incoming partner

B) the book value of the previous partnership plus any necessary asset write ups from book value to market value plus the fair market value of the consideration paid to the existing partnership by the incoming partner

C) the book value of the previous partnership minus any asset write downs from book to market value plus the fair market value of the consideration paid to the existing partnership by the incoming partner

D) the fair market value of the new partnership as implied by the value of the incoming partner's consideration in exchange for an ownership percentage in the new partnership

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

10

The following is the priority sequence in which liquidation proceeds will be distributed for a partnership:

A) partnership drawings, partnership liabilities, partnership loans, partnership capital balances.

B) partnership liabilities, partnership loans, partnership capital balances.

C) partnership liabilities, partnership loans, partnership drawings, partnership capital balances.

D) partnership liabilities, partnership capital balances, partnership loans.

A) partnership drawings, partnership liabilities, partnership loans, partnership capital balances.

B) partnership liabilities, partnership loans, partnership capital balances.

C) partnership liabilities, partnership loans, partnership drawings, partnership capital balances.

D) partnership liabilities, partnership capital balances, partnership loans.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following characterizes the bonus method, compared to the goodwill method, when unrecorded intangibles are traceable to the previous partners?

A) The intangibles are actually recorded.

B) The legal significance of a change in ownership structure of the partnership is emphasized.

C) This method generally produces more equitable results if the former partners do not share profits and losses in the same relationship to each other as they did before a new partner was admitted.

D) The market value concept rather than the historical cost concept is emphasized.

A) The intangibles are actually recorded.

B) The legal significance of a change in ownership structure of the partnership is emphasized.

C) This method generally produces more equitable results if the former partners do not share profits and losses in the same relationship to each other as they did before a new partner was admitted.

D) The market value concept rather than the historical cost concept is emphasized.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following results in dissolution of a partnership?

A) contribution of additional assets to the partnership by an existing partner

B) receipt of a draw by an existing partner

C) winding up of the partnership and the distribution of remaining assets to the partners

D) withdrawal of a partner from a partnership

A) contribution of additional assets to the partnership by an existing partner

B) receipt of a draw by an existing partner

C) winding up of the partnership and the distribution of remaining assets to the partners

D) withdrawal of a partner from a partnership

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

13

The admission of a new partner under the bonus method will result in a bonus to

A) the old partners only.

B) the new partner only.

C) either the new partner or the old partners, but not both.

D) none of the above.

A) the old partners only.

B) the new partner only.

C) either the new partner or the old partners, but not both.

D) none of the above.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

14

Assume that the capital of an existing partnership is $90,000 and all existing assets reflect fair market values. If an incoming partner acquires a 40% interest in the partnership for $55,000, the goodwill traceable to the incoming partner is

A) $15,000

B) $5,000

C) $3,000

D) $2,000

A) $15,000

B) $5,000

C) $3,000

D) $2,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

15

If a bonus is traceable to the previous partners rather than an incoming partner, it is allocated among the partners according to the

A) profit-sharing percentages of the previous partnership.

B) profit-sharing percentages of the new partnership.

C) capital percentages of the previous partners.

D) capital percentages of the new partnership.

A) profit-sharing percentages of the previous partnership.

B) profit-sharing percentages of the new partnership.

C) capital percentages of the previous partners.

D) capital percentages of the new partnership.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

16

The fair market value of a partnership can be implied by

A) adding the incoming partner's market value of consideration to the book value of the existing partnership.

B) the tax basis of the old partner's assets added to the incoming partner's consideration.

C) The incoming partner's market value of consideration divided by the incoming partner's percentage share in profit and loss.

D) The incoming partner's market value of consideration divided by the incoming partner's percentage ownership share in the new partnership.

A) adding the incoming partner's market value of consideration to the book value of the existing partnership.

B) the tax basis of the old partner's assets added to the incoming partner's consideration.

C) The incoming partner's market value of consideration divided by the incoming partner's percentage share in profit and loss.

D) The incoming partner's market value of consideration divided by the incoming partner's percentage ownership share in the new partnership.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

17

Scenario 14-1

Callie is admitted to the Adams & Beal Partnership under the bonus method. Callie contributes cash of $20,000 and non-cash assets with a market value of $30,000 and book value of $15,000 in exchange for a 20% ownership interest in the new partnership. Prior to the admission of Callie, the capital of the existing partnership was $130,000 and an appraisal showed the partnership net assets were fairly stated.

Refer to Scenario 14-1. Adams & Beal shared profits and losses at a ratio of 80/20, respectively. Which of the following bonus amounts would be recorded?

A) $14,000 to Callie capital

B) $2,800 increase to Beal capital

C) $2,800 decrease to Beal capital

D) $7,000 increase to Adams capital

Callie is admitted to the Adams & Beal Partnership under the bonus method. Callie contributes cash of $20,000 and non-cash assets with a market value of $30,000 and book value of $15,000 in exchange for a 20% ownership interest in the new partnership. Prior to the admission of Callie, the capital of the existing partnership was $130,000 and an appraisal showed the partnership net assets were fairly stated.

Refer to Scenario 14-1. Adams & Beal shared profits and losses at a ratio of 80/20, respectively. Which of the following bonus amounts would be recorded?

A) $14,000 to Callie capital

B) $2,800 increase to Beal capital

C) $2,800 decrease to Beal capital

D) $7,000 increase to Adams capital

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

18

If goodwill is traceable to the previous partners, it is

A) allocated among the previous partners according to their interest in capital.

B) allocated among the previous partners only if there are no other assets to be revalued.

C) allocated among the previous partners according to their original profit-and-loss-sharing percentages.

D) not possible for goodwill to also be traceable to the incoming partner.

A) allocated among the previous partners according to their interest in capital.

B) allocated among the previous partners only if there are no other assets to be revalued.

C) allocated among the previous partners according to their original profit-and-loss-sharing percentages.

D) not possible for goodwill to also be traceable to the incoming partner.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

19

Assume that the capital of an existing partnership is $130,000 and that existing assets are overvalued by $10,000. If an incoming partner acquires a 25% interest in the partnership for $37,000, goodwill traceable to the incoming partner is ____.

A) $1,000

B) $9,667

C) $3,000

D) $5,000

A) $1,000

B) $9,667

C) $3,000

D) $5,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

20

If goodwill is traceable to the incoming partner, the new partner's capital balance equals

A) the fair market value of consideration paid by the incoming partner

B) the book value of the older partnership divided by the existing partners' ownership percentage in the new partnership minus the book value of the old partnership.

C) incoming partner's ownership percentage multiplied by the capital of the new partnership

D) none of the above.

A) the fair market value of consideration paid by the incoming partner

B) the book value of the older partnership divided by the existing partners' ownership percentage in the new partnership minus the book value of the old partnership.

C) incoming partner's ownership percentage multiplied by the capital of the new partnership

D) none of the above.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

21

Lee, Alverez, and Tyne have a partnership. Their capital balances are $50,000, $70,000 and $30,000, respectively. The partner profit percentages are 30%, 40%, and 30%, respectively. They are considering on what basis to admit Patton, a prospective new partner. Based on appraisal analysis, the net assets of the partnership are worth $180,000. Patton is willing to put up cash of $30,000, plus a machine with book value of $12,000 and a fair value of $20,000.

Required:

Calculate, using the goodwill method, what the partnership balances will be if the existing partners recognize the differential between fair value and book value of the partnership's net assets as goodwill. What will Patton's percentage of partnership capital be, assuming the above deal goes through?

Required:

Calculate, using the goodwill method, what the partnership balances will be if the existing partners recognize the differential between fair value and book value of the partnership's net assets as goodwill. What will Patton's percentage of partnership capital be, assuming the above deal goes through?

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

22

The partnership of Able, Bower, and Cramer was liquidated. The partners have shared profits and losses in the ratio of 2:4:4. Prior to liquidation, their capital balances were the following*:

* Deficit shown in parentheses

Cash totaled $20,000, with liabilities amounting to $30,000. A review of the individual partners' personal financial status reveals the following:

Required:

Prepare a worksheet to liquidate the partnership.

* Deficit shown in parenthesesCash totaled $20,000, with liabilities amounting to $30,000. A review of the individual partners' personal financial status reveals the following:

Required:Prepare a worksheet to liquidate the partnership.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

23

Partners Able, Baker, and Chapman have the following personal assets, personal liabilities, and partnership capital balances: Assume profits and losses are allocated equally.

After applying the doctrine of marshaling of assets, the capital balances for Able, Baker, and Chapman, respectively, would be

A) $50,000, $(2,000), and $58,000.

B) $48,000, 0, and $58,000.

C) $49,000, 0, and $57,000.

D) $34,000, 0, and $54,000.

Assume profits and losses are allocated equally.After applying the doctrine of marshaling of assets, the capital balances for Able, Baker, and Chapman, respectively, would be

A) $50,000, $(2,000), and $58,000.

B) $48,000, 0, and $58,000.

C) $49,000, 0, and $57,000.

D) $34,000, 0, and $54,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

24

Smith, Thompson and Nickels have a partnership. Their capital balances are $90,000, $130,000 and $150,000, respectively. They share profits and losses 25%, 35% and 40%, respectively. Foster wants to become a partner with a 10 percent share in partnership capital with a $60,000 cash contribution to the partnership. Appraisal of the partnership reveals that the assets of the partnership are fairly valued.

Required:

Calculate Smith, Thompson, and Nickel's ending capital balances under the:

a.

Bonus Method

b.

Goodwill Method

Required:

Calculate Smith, Thompson, and Nickel's ending capital balances under the:

a.

Bonus Method

b.

Goodwill Method

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

25

Scenario 14-2

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. How much would Able receive upon liquidation of the partnership assuming profits and losses are allocated equally?

A) $70,000

B) $90,000

C) $75,000

D) $55,000

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. How much would Able receive upon liquidation of the partnership assuming profits and losses are allocated equally?

A) $70,000

B) $90,000

C) $75,000

D) $55,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

26

If a partnership has only non-cash assets, all liabilities have been properly disbursed, and no additional liquidation expenses are expected, the maximum potential loss to the partnership in the liquidation process is:

A) the fair market value of the non-cash assets

B) the book value of the non-cash assets

C) the estimated proceeds from the sale of the assets less the book value of the non-cash assets

D) none of the above

A) the fair market value of the non-cash assets

B) the book value of the non-cash assets

C) the estimated proceeds from the sale of the assets less the book value of the non-cash assets

D) none of the above

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

27

Partners Thomas, Adams and Jones have capital balances of $24,000, $45,000, and $90,000 respectively. They split profits in the ratio of 3:3:4, respectively. Under a predistribution plan, one of the partners will get the following total amount in liquidation before any other partners get anything:

A) $22,500

B) $30,000

C) $40,000

D) $75,000

A) $22,500

B) $30,000

C) $40,000

D) $75,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

28

Scenario 14-2

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. If all outside creditors and loans to partners had been paid, how would the balance of the assets be distributed assuming that Chapman had already received assets with a value of $30,000 assuming profits and losses are allocated equally?

A) Each of the partners would receive $25,000.

B) Each of the partners would receive $40,000.

C) Able: $70,000, Baker: $30,000, Chapman: $20,000

D) Able: $55,000, Baker: $15,000, Chapman: $5,000

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. If all outside creditors and loans to partners had been paid, how would the balance of the assets be distributed assuming that Chapman had already received assets with a value of $30,000 assuming profits and losses are allocated equally?

A) Each of the partners would receive $25,000.

B) Each of the partners would receive $40,000.

C) Able: $70,000, Baker: $30,000, Chapman: $20,000

D) Able: $55,000, Baker: $15,000, Chapman: $5,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

29

Under the doctrine of marshaling of assets, unsatisfied partnership creditors

A) must first proceed against the partner with the largest capital balance.

B) may attach to the assets of an individual partner before individual creditors have been satisfied.

C) may proceed against any personally solvent partner.

D) may proceed against any personally solvent partner but only to the extent of their capital balance in the partnership.

A) must first proceed against the partner with the largest capital balance.

B) may attach to the assets of an individual partner before individual creditors have been satisfied.

C) may proceed against any personally solvent partner.

D) may proceed against any personally solvent partner but only to the extent of their capital balance in the partnership.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

30

Long-term partners, Pop, Ping, and Pam have capital balances of $60,000, $45,000 and $30,000, respectively. They share in profits and losses 50%-to-30%-to-20%, respectively. All assets are valued fairly. Pam decides to retire from the partnership. Calculate the remaining partners' capital balances after the Pam withdrawal under the following situations:

a.

Pam sells the interest to Ping for $25,000.

b.

Pam sells the interest to the partnership for $25,000; bonus method is used

c.

Pam sells the interest to the partnership for $40,000; goodwill attributable only to the exiting partner is recorded

a.

Pam sells the interest to Ping for $25,000.

b.

Pam sells the interest to the partnership for $25,000; bonus method is used

c.

Pam sells the interest to the partnership for $40,000; goodwill attributable only to the exiting partner is recorded

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

31

Wright, Smith, and Young are partners with present capital balances of $60,000, $35,000, and $30,000, respectively. The partners share profits and losses according to the following percentages: 40% for Wright, 30% for Smith, and 30% for Young. Locke is to join the partnership upon contributing $40,000 to the partnership in exchange for a 20% interest in capital and a 20% interest in profits and losses. The existing assets of the original partnership are undervalued by $20,000. The original partners will share the balance of profits and losses in proportion to their original percentages.

Required:

Calculate the capital balances for each individual in the new partnership, assuming use of the bonus and goodwill methods.

Required:

Calculate the capital balances for each individual in the new partnership, assuming use of the bonus and goodwill methods.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements is correct regarding a partner's debit capital balances?

A) The partner should make contributions to reduce the debit balance to whatever extent possible.

B) If contributions are not possible, the other partners with credit capital balances will be allocated a portion of the debit balance based on their proportionate profit-and-loss-sharing percentages.

C) Partners who absorb another's debit capital balance have a legal claim against the deficient partner.

D) All of these statements are correct.

A) The partner should make contributions to reduce the debit balance to whatever extent possible.

B) If contributions are not possible, the other partners with credit capital balances will be allocated a portion of the debit balance based on their proportionate profit-and-loss-sharing percentages.

C) Partners who absorb another's debit capital balance have a legal claim against the deficient partner.

D) All of these statements are correct.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

33

Allen, Branden & Caylin are in the process of liquidating their partnership. They have the following capital balances and profit and loss percentages: The partnership balance sheet shows cash of $5,000, non-cash assets of $14,000, and no liabilities. Assuming no liquidation expenses, what safe payment could be made?

A) $5,000 split between Branden & Caylin by a ratio of 5/8 and 3/8, respectively.

B) $5,000 to Branden only

C) $1,000 to Allen, $2,500 to Branden, and $1,500 to Caylin

D) $18,000 to Branden only

A) $5,000 split between Branden & Caylin by a ratio of 5/8 and 3/8, respectively.

B) $5,000 to Branden only

C) $1,000 to Allen, $2,500 to Branden, and $1,500 to Caylin

D) $18,000 to Branden only

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

34

A partner's maximum loss absorbable is calculated by

A) dividing the partner's capital balance by his or her profit-and-loss-sharing percentage.

B) multiplying the partner's capital balance by his or her profit-and-loss-sharing percentage.

C) multiplying distributable assets by the partner's profit-sharing percentage.

D) dividing the partner's capital balance by his or her percentage interest in capital.

A) dividing the partner's capital balance by his or her profit-and-loss-sharing percentage.

B) multiplying the partner's capital balance by his or her profit-and-loss-sharing percentage.

C) multiplying distributable assets by the partner's profit-sharing percentage.

D) dividing the partner's capital balance by his or her percentage interest in capital.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

35

The doctrine of marshaling of assets

A) is applicable only if the partnership is insolvent.

B) allows partners to first contribute personal assets to unsatisfied partnership creditors.

C) is applicable if either the partnership is insolvent or individual partners are insolvent.

D) provides that when the Uniform Partnership Act is adopted, amounts owed to personal creditors and to the partnership for debit capital balances are shared proportionately from the personal assets of the partners.

A) is applicable only if the partnership is insolvent.

B) allows partners to first contribute personal assets to unsatisfied partnership creditors.

C) is applicable if either the partnership is insolvent or individual partners are insolvent.

D) provides that when the Uniform Partnership Act is adopted, amounts owed to personal creditors and to the partnership for debit capital balances are shared proportionately from the personal assets of the partners.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

36

Partners Dalton, Edwards, and Finley have capital balances of $40,000, 90,000 and $30,000, respectively, immediately prior to liquidation. Total remaining assets have a book value of $160,000, the liabilities having been paid. Among these remaining assets is a machine with a fair value of $35,000. The partners split profits and losses equally. Edwards covets the machine and is willing to accept it for $35,000 in lieu of cash. The other partners have no designs on specific assets, only cash in liquidation. How much cash, in addition to the machine, would be first distributed to Edwards, before any of the other partners received anything?

A) $15,000

B) $50,000

C) $166,667

D) $300,000

A) $15,000

B) $50,000

C) $166,667

D) $300,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

37

Oak, Pine, and Maple are partners with present capital balances of $42,000, $39,000, and $90,000, respectively. The partners share profits and losses according to the following percentages: 20% for Oak, 20% for Pine, and 60% for Maple. The existing assets of the original partnership have market values equal to book values except for the following:

Accounts Receivable:

overvalued by $10,000

Land:

undervalued by $30,000

Pine has agreed to sell her interest to the partnership for $45,000.

Required:

Calculate the capital balances for each individual in the new partnership, assuming use of the bonus and goodwill methods. The goodwill method should recognize the goodwill traceable to all partners.

Accounts Receivable:

overvalued by $10,000

Land:

undervalued by $30,000

Pine has agreed to sell her interest to the partnership for $45,000.

Required:

Calculate the capital balances for each individual in the new partnership, assuming use of the bonus and goodwill methods. The goodwill method should recognize the goodwill traceable to all partners.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

38

Martel, Tusk, and Davis are partners with present capital balances of $40,000, $50,000, and $20,000, respectively. The partners share profits and losses according to the following percentages: 60% for Martel, 30% for Tusk, and 10% for Davis. Frank is to join the partnership upon contributing $40,000 to the partnership in exchange for a 25% interest in capital and a 20% interest in profits and losses. An appraisal of the existing partnerships' assets reveals the following:

Required:

Calculate the capital balances for each individual in the new partnership assuming use of the bonus and goodwill methods.

Required:Calculate the capital balances for each individual in the new partnership assuming use of the bonus and goodwill methods.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

39

Partner T is personally insolvent, owing $400,000. Personal assets will only bring $150,000 when liquidated. At the same time, T has a credit capital balance in the partnership of $85,000. The capital amounts of the other partners total a (credit) balance of $200,000. Under the doctrine of marshaling of assets, the personal creditors of T can collect up to ____.

A) $150,000

B) $235,000

C) $400,000

D) $435,000

A) $150,000

B) $235,000

C) $400,000

D) $435,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

40

Scenario 14-2

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. How would the first $100,000 of available assets be distributed assuming profits and losses are allocated equally?

A) $70,000 to outside liabilities, $20,000 to Able, and the balance equally among the partners

B) $70,000 to outside liabilities and $30,000 to Able

C) $70,000 to outside liabilities, $25,000 to Able, and $5,000 to Chapman

D) $40,000 to Able, $20,000 to Chapman, and the balance equally among the partners

Assume that a partnership had assets with a book value of $240,000 and a market value of $195,000, outside liabilities of $70,000, loans payable to partner Able of $20,000, and capital balances for partners Able, Baker, and Chapman of $70,000, $30,000, and $50,000.

Refer to Scenario 14-2. How would the first $100,000 of available assets be distributed assuming profits and losses are allocated equally?

A) $70,000 to outside liabilities, $20,000 to Able, and the balance equally among the partners

B) $70,000 to outside liabilities and $30,000 to Able

C) $70,000 to outside liabilities, $25,000 to Able, and $5,000 to Chapman

D) $40,000 to Able, $20,000 to Chapman, and the balance equally among the partners

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

41

The partnership of Alt, Brown, and Carns has total assets and liabilities of $30,000 and $25,000, respectively. Information relating to the partners is as follows:

Required:

a.

Assuming that the Uniform Partnership Act is applicable, indicate how the partners' personal assets would be distributed.

b.

Assuming that federal bankruptcy laws are applicable, indicate how the partners' personal assets would be distributed.

c.

Assume that the partnership had a deficit of $10,000, allocated among Alt, Brown, and Carns as follows: $2,000 surplus, $7,000 deficit, and $5,000 deficit, respectively. Indicate how the deficit would be satisfied when bankruptcy laws are applicable.

Required: a.

Assuming that the Uniform Partnership Act is applicable, indicate how the partners' personal assets would be distributed.

b.

Assuming that federal bankruptcy laws are applicable, indicate how the partners' personal assets would be distributed.

c.

Assume that the partnership had a deficit of $10,000, allocated among Alt, Brown, and Carns as follows: $2,000 surplus, $7,000 deficit, and $5,000 deficit, respectively. Indicate how the deficit would be satisfied when bankruptcy laws are applicable.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

42

Merz, Dechter, and Flowers are partners in a partnership and share profits and losses 40%, 40%, and 20%, respectively. The partners have agreed to liquidate the partnership and anticipate that liquidation expenses will total $14,000. Prior to the liquidation, the partnership balance sheet reflects the following book values:

Required:

Assuming that the actual liquidation expenses are $20,000 and that noncash assets are sold for $160,000, determine how the assets will be distributed. Flowers has net personal assets of $10,000.

Required:Assuming that the actual liquidation expenses are $20,000 and that noncash assets are sold for $160,000, determine how the assets will be distributed. Flowers has net personal assets of $10,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

43

The Tyler, Russell, and Colby partnership is liquidating. The three partners share profits and losses equally. The following is the post-closing trial balance for the partnership:

Required:

Draft a predistribution plan for the partnership liquidation and provide a schedule of payments.

Required:Draft a predistribution plan for the partnership liquidation and provide a schedule of payments.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

44

Rogers, Davis, and Smukalla have capital balances of $50,000, $26,100, and $10,900, respectively. The partners share profits/losses equally.

Required:

Calculate Rogers' new capital balance resulting from each of the following independent situations:

Situation 1:Smukalla sells his interest in the partnership to Rogers for $25,000.

Situation 2:Meyers purchases a one-fourth interest from the partnership for $35,000. The bonus method is used to account for the incoming partner.

Situation 3:The same as Situation 2 except that the goodwill method is used to account for the incoming partner.

Situation 4:Davis sells her interest to the partnership for $30,000. The total amount of suggested goodwill is to be recorded.

Required:

Calculate Rogers' new capital balance resulting from each of the following independent situations:

Situation 1:Smukalla sells his interest in the partnership to Rogers for $25,000.

Situation 2:Meyers purchases a one-fourth interest from the partnership for $35,000. The bonus method is used to account for the incoming partner.

Situation 3:The same as Situation 2 except that the goodwill method is used to account for the incoming partner.

Situation 4:Davis sells her interest to the partnership for $30,000. The total amount of suggested goodwill is to be recorded.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

45

The ALPHA, BETA, AND DELTA partnership has total assets of $260,000. Capital balances for partners ALPHA, BETA, and DELTA are $50,000, $30,000, and $50,000, respectively. The profit/loss percentages for partners ALPHA, BETA, and DELTA are 30%, 40%, and 30%, respectively. Included in the liabilities is a $9,000 loan payable to ALPHA. The partnership has elected to liquidate over the next several months. Liquidation expenses are estimated to be $15,000.

Required:

Assuming assets with a book value of $80,000 were sold for $60,000, and that $160,000 cash is available, how should the available cash be distributed?

Required:

Assuming assets with a book value of $80,000 were sold for $60,000, and that $160,000 cash is available, how should the available cash be distributed?

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

46

On July 1, 20X9, the Crawford Company has the following balance sheet:

As of July 1, 20X9, the partners have personal net worth as follows:

The personal net worth of each partner does not include any amounts due to or from the partnership.

Required:

Assume the other assets are sold for $103,000 after incurring liquidation expenses of $4,000. After liquidation of the partnership, determine how much is available to Lake's unsatisfied personal creditors based on the following:

a.

Application of the Uniform Partnership Act

b.

Application of common law

As of July 1, 20X9, the partners have personal net worth as follows:The personal net worth of each partner does not include any amounts due to or from the partnership.

Required:

Assume the other assets are sold for $103,000 after incurring liquidation expenses of $4,000. After liquidation of the partnership, determine how much is available to Lake's unsatisfied personal creditors based on the following:

a.

Application of the Uniform Partnership Act

b.

Application of common law

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

47

Luc, Denis, and Rollande have capital balances of $30,000, $70,000, and $15,000, respectively. The partners share profits/losses 2:6:2. All assets book values equal market except as noted. The partnership agreement states the bonus method is to be used to account for partner sale of interest to the partnership.

Required:

Calculate Luc's new capital balance resulting from each of the following independent situations:

Situation 1:Rollande sells his interest to the partnership for $25,000. Bonus method is used.

Situation 2:Rollande sells his interest to Luc for $25,000.

Situation 3:Martel purchases a 20% interest from the partnership for $35,000. The bonus method is used to account for the incoming partner.

Situation 4:The same as Situation 3 except that the goodwill method is used to account for the incoming partner.

Required:

Calculate Luc's new capital balance resulting from each of the following independent situations:

Situation 1:Rollande sells his interest to the partnership for $25,000. Bonus method is used.

Situation 2:Rollande sells his interest to Luc for $25,000.

Situation 3:Martel purchases a 20% interest from the partnership for $35,000. The bonus method is used to account for the incoming partner.

Situation 4:The same as Situation 3 except that the goodwill method is used to account for the incoming partner.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

48

The Nice, Rice, and Dice Partnership has not been successful. The partners have determined they must liquidate their partnership. The partners have agreed to liquidate the partnership and anticipate that liquidation expenses will total $1,000. Prior to the liquidation, the partnership balance sheet reflects the following book values:

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner's personal net worth reveals the following:

The following transactions occur:

a.

Assets having a book value of $40,000 are sold for $22,000 cash

b.

Liabilities are paid, where possible

c.

Partners contribute from their personal net worth, according to UPA requirements and Marshaling of Assets concepts

Required:

Prepare liquidation schedule and determine how the available assets will be distributed using a schedule of safe payments.

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner's personal net worth reveals the following: The following transactions occur: a.

Assets having a book value of $40,000 are sold for $22,000 cash

b.

Liabilities are paid, where possible

c.

Partners contribute from their personal net worth, according to UPA requirements and Marshaling of Assets concepts

Required:

Prepare liquidation schedule and determine how the available assets will be distributed using a schedule of safe payments.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 48 flashcards in this deck.