Deck 2: Foreign Exchange Parity Relations

Full screen (f)

Question

Question

The Japanese balance of payments from 1987 to 1993 is as follows. All numbers are reported in billions of U.S. dollars. The last line gives the real effective exchange rate index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

Question

Question

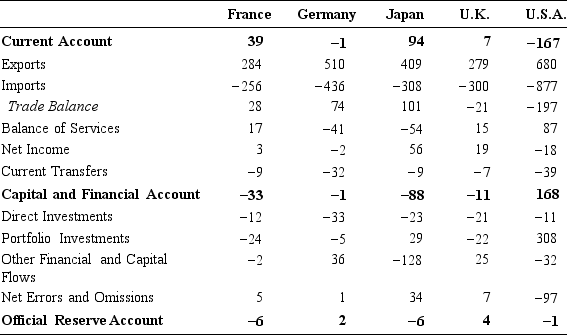

The exhibit below presents the 1997 balance of payments statistics for France, Germany, Japan, the United Kingdom, and the United States. The various balance of payments items have been aggregated using the presentation outlined in Chapter 2.

EXHIBIT: 1997 Balance of Payments of Five Major Countries

Billions of U.S. Dollars

Source: Adapted from International Monetary Fund, International Financial Statistics, 1998

Source: Adapted from International Monetary Fund, International Financial Statistics, 1998

Yearbook.

a. Provide an analysis of the U.S. balance of payments.

b. Provide an analysis of the British balance of payments.

c. Provide an analysis of the French balance of payments.

d. Provide a brief analysis of the Japanese balance of payments.

e. Provide a brief analysis of the German balance of payments.

EXHIBIT: 1997 Balance of Payments of Five Major Countries

Billions of U.S. Dollars

Source: Adapted from International Monetary Fund, International Financial Statistics, 1998Yearbook.

a. Provide an analysis of the U.S. balance of payments.

b. Provide an analysis of the British balance of payments.

c. Provide an analysis of the French balance of payments.

d. Provide a brief analysis of the Japanese balance of payments.

e. Provide a brief analysis of the German balance of payments.

Question

Question

Question

Question

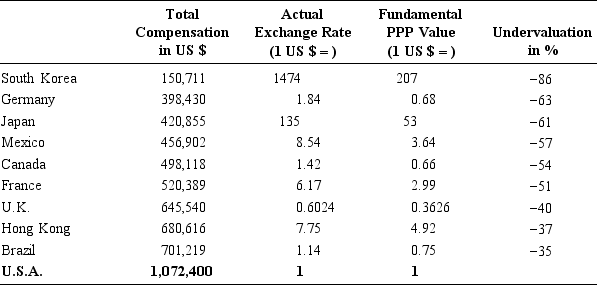

Fundamental Value Based on Absolute PPP. Ideally, one would like to compare directly the price

of goods in two countries to see if an exchange rate conforms to absolute PPP, or whether it is overvalued or undervalued in real terms. As mentioned in Chapter 2, this can only be done for some individual goods that are clearly comparable ("law of one price"), and the estimation for different goods can lead to opposing conclusions. In Chapter 2, we provide an analysis based on the well-known Big Mac report of The Economist. Of course, the Big Mac is a very particular product and a fundamental PPP value can be computed on a wide range of products. The results are often conflicting. For example, one can look at production prices rather than consumption prices. Some studies are conducted by looking at labor costs. Rather than looking at unit labor costs for unskilled workers, as is often done, the exhibit below reports the average annual remuneration of the chief executive officer (CEO) of industrial companies with annual revenues of $250 million to $500 million in ten selected areas of the world. The figures are also from April 1998. They include all forms of compensation, such as bonuses, perks, and stock options, but are not adjusted for different taxes or costs of living.

The first column gives the total CEO compensation measured in U.S. dollars using the actual exchange rate, which is indicated in the second column. The third column gives the fundamental PPP value of each currency, implied by the national CEO compensations. It is the exchange rate with the dollar that would make CEO compensation identical in all countries. The fourth column gives the actual overvaluation (if positive) or undervaluation (if negative) of the local currency relative to its fundamental value in terms of CEO compensation.

EXHIBIT: Determining a Fundamental PPP Value Based on CEOs' Remuneration

Source: Total compensation data comes from Towers Perrin, 1998.

Source: Total compensation data comes from Towers Perrin, 1998.

What conclusions can you draw from this exhibit?

of goods in two countries to see if an exchange rate conforms to absolute PPP, or whether it is overvalued or undervalued in real terms. As mentioned in Chapter 2, this can only be done for some individual goods that are clearly comparable ("law of one price"), and the estimation for different goods can lead to opposing conclusions. In Chapter 2, we provide an analysis based on the well-known Big Mac report of The Economist. Of course, the Big Mac is a very particular product and a fundamental PPP value can be computed on a wide range of products. The results are often conflicting. For example, one can look at production prices rather than consumption prices. Some studies are conducted by looking at labor costs. Rather than looking at unit labor costs for unskilled workers, as is often done, the exhibit below reports the average annual remuneration of the chief executive officer (CEO) of industrial companies with annual revenues of $250 million to $500 million in ten selected areas of the world. The figures are also from April 1998. They include all forms of compensation, such as bonuses, perks, and stock options, but are not adjusted for different taxes or costs of living.

The first column gives the total CEO compensation measured in U.S. dollars using the actual exchange rate, which is indicated in the second column. The third column gives the fundamental PPP value of each currency, implied by the national CEO compensations. It is the exchange rate with the dollar that would make CEO compensation identical in all countries. The fourth column gives the actual overvaluation (if positive) or undervaluation (if negative) of the local currency relative to its fundamental value in terms of CEO compensation.

EXHIBIT: Determining a Fundamental PPP Value Based on CEOs' Remuneration

Source: Total compensation data comes from Towers Perrin, 1998.What conclusions can you draw from this exhibit?

Question

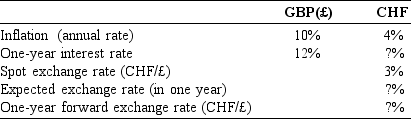

Here are some statistics:

Based on the linear approximation of international parity relations, replace the question marks with the appropriate answers.

Based on the linear approximation of international parity relations, replace the question marks with the appropriate answers.

Based on the linear approximation of international parity relations, replace the question marks with the appropriate answers. Question

Question

Question

The Japanese balance of payments from 1994 to 1997 is as follows. All numbers are reported in billions of U.S. dollars. The last line gives the real effective exchange rate index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 2: Foreign Exchange Parity Relations

1

Should real interest rates be equal across countries? Can a financial arbitrage take place in case of significant and persistent real interest rate differences? To answer this question:

a. First assume that exchange rates are fully predictable and follow purchasing power parity (PPP).

b. Then assume that they are uncertain but that PPP holds.

c. Finally, assume that exchange rates are uncertain and that PPP does not hold.

a. First assume that exchange rates are fully predictable and follow purchasing power parity (PPP).

b. Then assume that they are uncertain but that PPP holds.

c. Finally, assume that exchange rates are uncertain and that PPP does not hold.

Not necessarily. This can be shown by observing that no risk-free arbitrage can exploit differences in real interest rates. Let's start with a simple world and progressively add more complex realities. Assume that the real rates on euros and U.S. dollars are respectively 2% and 4%. Let's use the linear approximation:

a. Exchange rate is fully predictable and PPP holds.

Differences in real interest rates can be arbitraged away. One can simply borrow in €, transfer the € in $ at the spot exchange rate and lend the $. It can easily be seen that this strategy yields exactly the real interest rate differential (2%) without any capital investment.

Since the exchange rate is fully predictable and follows PPP, we know for sure that its future depreciation is exactly equal to the (certain) expected inflation differential. The net result on the investment strategy is the real interest rate differential.

b. Exchange rate is uncertain but PPP holds.

We know that the future exchange rate will exactly reflect the observed future inflation differential (PPP) but we are not sure about future inflation rates. The interest rate differential is equal to the real interest rate differential plus the expected inflation differential, while the exchange rate depreciation will be equal to the ex-post realized inflation differential. The deviation between expected and realized inflation makes the above arbitrage uncertain. However, the deviation is likely to be small for short horizons, so arbitrage will insure that the short-term real interest rate differential is small.

c. PPP does not hold.

Real exchange rates can be very volatile in the short run. No riskless arbitrage can take place to take advantage of real interest rate differentials.

a. Exchange rate is fully predictable and PPP holds.

Differences in real interest rates can be arbitraged away. One can simply borrow in €, transfer the € in $ at the spot exchange rate and lend the $. It can easily be seen that this strategy yields exactly the real interest rate differential (2%) without any capital investment.

Since the exchange rate is fully predictable and follows PPP, we know for sure that its future depreciation is exactly equal to the (certain) expected inflation differential. The net result on the investment strategy is the real interest rate differential.

b. Exchange rate is uncertain but PPP holds.

We know that the future exchange rate will exactly reflect the observed future inflation differential (PPP) but we are not sure about future inflation rates. The interest rate differential is equal to the real interest rate differential plus the expected inflation differential, while the exchange rate depreciation will be equal to the ex-post realized inflation differential. The deviation between expected and realized inflation makes the above arbitrage uncertain. However, the deviation is likely to be small for short horizons, so arbitrage will insure that the short-term real interest rate differential is small.

c. PPP does not hold.

Real exchange rates can be very volatile in the short run. No riskless arbitrage can take place to take advantage of real interest rate differentials.

2

The Japanese balance of payments from 1987 to 1993 is as follows. All numbers are reported in billions of U.S. dollars. The last line gives the real effective exchange rate index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

a. The various accounts are given below:

b. The Japanese trade balance, which has been constantly positive over the time period, worsened from 1987 to 1990 and improved from then on. The current account tracked the trade balance. This surplus was mostly used to invest abroad (negative capital and financial account).

b. The Japanese trade balance, which has been constantly positive over the time period, worsened from 1987 to 1990 and improved from then on. The current account tracked the trade balance. This surplus was mostly used to invest abroad (negative capital and financial account).

The decrease in the current account from 1988 to 1990 led to a drop in official reserves (positive reserve account) and a weakening of the yen. Its real effective exchange rate depreciated from 135 to 114. This improvement in the terms of trade led to an increase of the Japanese trade balance in the early 1990s. In 1991 and 1992, the increased current account surplus was used to

increase foreign investments by the Japanese (the capital and financial account deficit increased from 41 billion in 1990 to 117 billion in 1992). In 1993, the current account increased to

131 billion but net foreign investments accounted to only 104 billion. Hence, Japanese reserves increased by 27 billion (a negative official reserve account). This led to a strong appreciation

of the yen.

b. The Japanese trade balance, which has been constantly positive over the time period, worsened from 1987 to 1990 and improved from then on. The current account tracked the trade balance. This surplus was mostly used to invest abroad (negative capital and financial account).The decrease in the current account from 1988 to 1990 led to a drop in official reserves (positive reserve account) and a weakening of the yen. Its real effective exchange rate depreciated from 135 to 114. This improvement in the terms of trade led to an increase of the Japanese trade balance in the early 1990s. In 1991 and 1992, the increased current account surplus was used to

increase foreign investments by the Japanese (the capital and financial account deficit increased from 41 billion in 1990 to 117 billion in 1992). In 1993, the current account increased to

131 billion but net foreign investments accounted to only 104 billion. Hence, Japanese reserves increased by 27 billion (a negative official reserve account). This led to a strong appreciation

of the yen.

3

The spot exchange rate is CHF/$ =2.00. The one-year interest rate is equal to 4% in Switzerland and 8% in the United States. What should the current value of the forward exchange rate be?

According to the interest rate parity relation, the forward discount (or premium) is equal to the interest rate differential. With F being the current value of the one-year forward exchange rate,

we have: CHF/$.

we have: CHF/$.

4

The exhibit below presents the 1997 balance of payments statistics for France, Germany, Japan, the United Kingdom, and the United States. The various balance of payments items have been aggregated using the presentation outlined in Chapter 2.

EXHIBIT: 1997 Balance of Payments of Five Major Countries

Billions of U.S. Dollars

Source: Adapted from International Monetary Fund, International Financial Statistics, 1998

Yearbook.

a. Provide an analysis of the U.S. balance of payments.

b. Provide an analysis of the British balance of payments.

c. Provide an analysis of the French balance of payments.

d. Provide a brief analysis of the Japanese balance of payments.

e. Provide a brief analysis of the German balance of payments.

EXHIBIT: 1997 Balance of Payments of Five Major Countries

Billions of U.S. Dollars

Source: Adapted from International Monetary Fund, International Financial Statistics, 1998Yearbook.

a. Provide an analysis of the U.S. balance of payments.

b. Provide an analysis of the British balance of payments.

c. Provide an analysis of the French balance of payments.

d. Provide a brief analysis of the Japanese balance of payments.

e. Provide a brief analysis of the German balance of payments.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

Should nominal interest rates be equal across countries? Why or why not?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

In 1994, the United States was experiencing a fairly strong economic recovery, ahead of other nations. Fears of an overheating economy led to sudden inflationary fears for the next few years.

a. Would you expect U.S. interest rates to rise or drop?

b. Would you expect the dollar to depreciate or appreciate?

c. Would you expect a foreign bond portfolio to be a good investment compared to a U.S. dollar portfolio under this scenario?

a. Would you expect U.S. interest rates to rise or drop?

b. Would you expect the dollar to depreciate or appreciate?

c. Would you expect a foreign bond portfolio to be a good investment compared to a U.S. dollar portfolio under this scenario?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

Exchange Rate Dynamics. Britain and Europe have no inflation, a constant money supply and (annualized) interest rates equal to 2% for all maturities. The exchange rate is equal to one pound per euro; this is its PPP value and the price indexes can be assumed to be equal to one in both countries.

Suddenly and unexpectedly, Britain increases its money supply by 5%. This is a one-time but permanent shock. Immediately upon the announcement, the British interest rate drops from 2% to 1% for all maturities (excess liquidity induces a drop in the real interest rate). It is expected that it will take three years for the shock in money supply to translate fully into a price increase. There is no effect on the real sector, nor any effect on Europe. Assume that the Eurozone is the domestic country. What will be the exchange rate dynamics?

Suddenly and unexpectedly, Britain increases its money supply by 5%. This is a one-time but permanent shock. Immediately upon the announcement, the British interest rate drops from 2% to 1% for all maturities (excess liquidity induces a drop in the real interest rate). It is expected that it will take three years for the shock in money supply to translate fully into a price increase. There is no effect on the real sector, nor any effect on Europe. Assume that the Eurozone is the domestic country. What will be the exchange rate dynamics?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

Fundamental Value Based on Absolute PPP. Ideally, one would like to compare directly the price

of goods in two countries to see if an exchange rate conforms to absolute PPP, or whether it is overvalued or undervalued in real terms. As mentioned in Chapter 2, this can only be done for some individual goods that are clearly comparable ("law of one price"), and the estimation for different goods can lead to opposing conclusions. In Chapter 2, we provide an analysis based on the well-known Big Mac report of The Economist. Of course, the Big Mac is a very particular product and a fundamental PPP value can be computed on a wide range of products. The results are often conflicting. For example, one can look at production prices rather than consumption prices. Some studies are conducted by looking at labor costs. Rather than looking at unit labor costs for unskilled workers, as is often done, the exhibit below reports the average annual remuneration of the chief executive officer (CEO) of industrial companies with annual revenues of $250 million to $500 million in ten selected areas of the world. The figures are also from April 1998. They include all forms of compensation, such as bonuses, perks, and stock options, but are not adjusted for different taxes or costs of living.

The first column gives the total CEO compensation measured in U.S. dollars using the actual exchange rate, which is indicated in the second column. The third column gives the fundamental PPP value of each currency, implied by the national CEO compensations. It is the exchange rate with the dollar that would make CEO compensation identical in all countries. The fourth column gives the actual overvaluation (if positive) or undervaluation (if negative) of the local currency relative to its fundamental value in terms of CEO compensation.

EXHIBIT: Determining a Fundamental PPP Value Based on CEOs' Remuneration

Source: Total compensation data comes from Towers Perrin, 1998.

What conclusions can you draw from this exhibit?

of goods in two countries to see if an exchange rate conforms to absolute PPP, or whether it is overvalued or undervalued in real terms. As mentioned in Chapter 2, this can only be done for some individual goods that are clearly comparable ("law of one price"), and the estimation for different goods can lead to opposing conclusions. In Chapter 2, we provide an analysis based on the well-known Big Mac report of The Economist. Of course, the Big Mac is a very particular product and a fundamental PPP value can be computed on a wide range of products. The results are often conflicting. For example, one can look at production prices rather than consumption prices. Some studies are conducted by looking at labor costs. Rather than looking at unit labor costs for unskilled workers, as is often done, the exhibit below reports the average annual remuneration of the chief executive officer (CEO) of industrial companies with annual revenues of $250 million to $500 million in ten selected areas of the world. The figures are also from April 1998. They include all forms of compensation, such as bonuses, perks, and stock options, but are not adjusted for different taxes or costs of living.

The first column gives the total CEO compensation measured in U.S. dollars using the actual exchange rate, which is indicated in the second column. The third column gives the fundamental PPP value of each currency, implied by the national CEO compensations. It is the exchange rate with the dollar that would make CEO compensation identical in all countries. The fourth column gives the actual overvaluation (if positive) or undervaluation (if negative) of the local currency relative to its fundamental value in terms of CEO compensation.

EXHIBIT: Determining a Fundamental PPP Value Based on CEOs' Remuneration

Source: Total compensation data comes from Towers Perrin, 1998.What conclusions can you draw from this exhibit?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

Here are some statistics:

Based on the linear approximation of international parity relations, replace the question marks with the appropriate answers.

Based on the linear approximation of international parity relations, replace the question marks with the appropriate answers. Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

The ¥/€ spot exchange rate is 130 yen per euro. Inflation rates in Japan and Germany are similar. Over the past year the ¥/€ rate moved from 110 to 130. Is this good news or bad news for Japanese firms competing with German firms in the automobile market?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

The current Swiss franc/U.S. dollar spot exchange rate is 2 Swiss francs per dollar, or CHF/$ = 2.

The expected inflation over the coming year is 2% in Switzerland and 5% in the United States.

What is the expected value for the spot exchange rate a year from now, according to purchasing power parity?

The expected inflation over the coming year is 2% in Switzerland and 5% in the United States.

What is the expected value for the spot exchange rate a year from now, according to purchasing power parity?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

The Japanese balance of payments from 1994 to 1997 is as follows. All numbers are reported in billions of U.S. dollars. The last line gives the real effective exchange rate index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.

b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and official reserve account for each year.b. Use these numbers to describe what has happened in terms of Japanese financial transactions with the rest of the world.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

Under a system of fixed exchange rates, a nation can try to remedy its balance of payments deficit by:

a. Applying expansionary macroeconomic policy to drive prices up and interest rates down.

b. Applying restrictive macroeconomic policy to keep prices down and interest rates up.

c. Reducing its income from investments abroad.

d. Building up its reserves of foreign currencies and reserve balances with the International Monetary Fund.

a. Applying expansionary macroeconomic policy to drive prices up and interest rates down.

b. Applying restrictive macroeconomic policy to keep prices down and interest rates up.

c. Reducing its income from investments abroad.

d. Building up its reserves of foreign currencies and reserve balances with the International Monetary Fund.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

Paf is a small country. Its currency is the pif and the exchange rate with the U.S. dollar was 2 pifs

per dollar in 1980. The inflation indexes in 1980 were equal to 100 in the United States and in Paf. Twenty years later, the inflation indexes were equal to 400 in the United States and 200 in Paf. The current exchange rate is 0.9 pifs per dollar.

a. What should the current exchange rate be if PPP prevailed?

b. Is the Pif over/undervalued according to PPP?

per dollar in 1980. The inflation indexes in 1980 were equal to 100 in the United States and in Paf. Twenty years later, the inflation indexes were equal to 400 in the United States and 200 in Paf. The current exchange rate is 0.9 pifs per dollar.

a. What should the current exchange rate be if PPP prevailed?

b. Is the Pif over/undervalued according to PPP?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

Under a system of fixed exchange rates, a nation experiencing an excess of imports over exports can try to remedy this situation by:

a. Adopting tariffs and quotas.

b. Reducing its income from investments abroad.

c. Applying an expansionary macroeconomic policy to drive prices up and interest rates down.

d. Building up its reserves of foreign currencies and reserve balances with the International Monetary Fund.

a. Adopting tariffs and quotas.

b. Reducing its income from investments abroad.

c. Applying an expansionary macroeconomic policy to drive prices up and interest rates down.

d. Building up its reserves of foreign currencies and reserve balances with the International Monetary Fund.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

Because of the relative rise in local production costs brought about by the appreciation of the yen, many Japanese corporations have decided to transfer production abroad. What should be the immediate and future impact on the Japanese balance of payments?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.