Deck 1: Currency Exchange Rates

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 1: Currency Exchange Rates

1

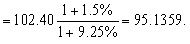

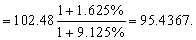

The bid-ask rates are as follows:

Spot exchange rate:

¥/$ 102.40-48

Interest rates:

One-year interest rate in ¥ 11/2 - 5/8

One-year interest rate in $ 91/8 - 1/4

What is the quotation for the one-year ¥/$ forward exchange rate?

Spot exchange rate:

¥/$ 102.40-48

Interest rates:

One-year interest rate in ¥ 11/2 - 5/8

One-year interest rate in $ 91/8 - 1/4

What is the quotation for the one-year ¥/$ forward exchange rate?

The bid forward exchange rate is:

¥/$ The ask forward exchange rate is:

The ask forward exchange rate is:

¥/$ Therefore, the quotation for the one-year ¥/$ forward exchange rate is 95.1359-95.4367.

Therefore, the quotation for the one-year ¥/$ forward exchange rate is 95.1359-95.4367.

¥/$

The ask forward exchange rate is:¥/$

Therefore, the quotation for the one-year ¥/$ forward exchange rate is 95.1359-95.4367. 2

A Turkish clothing company is buying material in Mexico. It needs to pay 1 million Mexican pesos. The exchange rates published in a local newspaper are as follows:

One U.S. dollar is worth 1356 Turkish liras.

One U.S. dollar is worth 129.64 Mexican pesos.

The Turkish company calls its local banker, who advises that it needs to do two foreign exchange transactions: One selling liras to buy dollars, and the other buying pesos with these dollars. The company is surprised that its banker does not engage directly in a single transaction from liras to pesos. Why would the bid-ask spread be much larger on the lira/peso transaction than the sum of the bid-ask spread of the two lira/dollar and peso/dollar transactions?

One U.S. dollar is worth 1356 Turkish liras.

One U.S. dollar is worth 129.64 Mexican pesos.

The Turkish company calls its local banker, who advises that it needs to do two foreign exchange transactions: One selling liras to buy dollars, and the other buying pesos with these dollars. The company is surprised that its banker does not engage directly in a single transaction from liras to pesos. Why would the bid-ask spread be much larger on the lira/peso transaction than the sum of the bid-ask spread of the two lira/dollar and peso/dollar transactions?

For each currency, there exists a "wholesale" foreign exchange market only against the U.S. dollar. This rule suffers very few exceptions, such as other European currencies against the euro, or some Asian currencies against the yen. This is motivated by liquidity.

A market between the Turkish lira and the Mexican peso would see very few daily transactions, if any. Hence, liquidity would be very limited. Any bank making a firm bid-ask quote would have to take a huge spread as it may take several days to unwind a position. In reality, all transactions involving the lira (and another foreign currency) are done against the U.S dollar. So, there are two transactions; first the lira against the dollar and then the foreign currency against the dollar (except of course when the foreign currency is the dollar itself). Similarly, any transaction involving the peso is done against the U.S. dollar. Because there are quite a few daily transactions involving the lira against all other currencies, the bid-ask spread on the lira/dollar exchange rate is fairly low. It is better to have to pay two small spreads than a single large one.

A market between the Turkish lira and the Mexican peso would see very few daily transactions, if any. Hence, liquidity would be very limited. Any bank making a firm bid-ask quote would have to take a huge spread as it may take several days to unwind a position. In reality, all transactions involving the lira (and another foreign currency) are done against the U.S dollar. So, there are two transactions; first the lira against the dollar and then the foreign currency against the dollar (except of course when the foreign currency is the dollar itself). Similarly, any transaction involving the peso is done against the U.S. dollar. Because there are quite a few daily transactions involving the lira against all other currencies, the bid-ask spread on the lira/dollar exchange rate is fairly low. It is better to have to pay two small spreads than a single large one.

3

A French company knows that it will have to pay 10 million Swiss francs in three months. The current spot exchange rate is 0.6000 €/SFr. The three-month forward rate is 0.603 €/SFr. The treasurer is worried that the euro will depreciate in the next few weeks.

a. What action can be taken?

b. Three months later, the spot exchange rate turns out to be 0.620 €/SF; was it a wise decision?

a. What action can be taken?

b. Three months later, the spot exchange rate turns out to be 0.620 €/SF; was it a wise decision?

If the treasurer is worried that the euro might depreciate in the next three months, he will certainly be willing to hedge his foreign exchange position right away by trading this risk against the premium included in the forward exchange rate.

a. He will therefore buy 10 million Swiss francs on the three-month forward market at the rate of 0.603 €/SFr. The transaction will be contracted as of the current date but delivery and settlement will only take place three months later. The forward premium is equal to 0.5% for three months, or 2% annualized.

b. Since the spot exchange rate on the day of delivery (0.620 €/SFr) happens to be higher than the contract's forward rate (0.603 €/SFr), this decision can retrospectively be regarded as a wise one. The treasurer paid 10 M* 0.603 =6.03 million euros on the forward market instead of 10 M * 0.620 =6.20 million if he had paid on the spot market. 0.17 million euros were saved through this strategy.

a. He will therefore buy 10 million Swiss francs on the three-month forward market at the rate of 0.603 €/SFr. The transaction will be contracted as of the current date but delivery and settlement will only take place three months later. The forward premium is equal to 0.5% for three months, or 2% annualized.

b. Since the spot exchange rate on the day of delivery (0.620 €/SFr) happens to be higher than the contract's forward rate (0.603 €/SFr), this decision can retrospectively be regarded as a wise one. The treasurer paid 10 M* 0.603 =6.03 million euros on the forward market instead of 10 M * 0.620 =6.20 million if he had paid on the spot market. 0.17 million euros were saved through this strategy.

4

Here are some quotes of the Japanese yen/U.S. dollar spot exchange rate given simultaneously on the phone by three banks:

Bank A: 121.15-121.30

Bank B: 121.22-121.35

Bank C: 121.20-121.25

Are these quotes reasonable? Do you have an arbitrage opportunity?

Bank A: 121.15-121.30

Bank B: 121.22-121.35

Bank C: 121.20-121.25

Are these quotes reasonable? Do you have an arbitrage opportunity?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

If the exchange rate value of the euro goes from U.S. $1.15 to U.S. $1.05, then:

a. The euro has appreciated, and Europeans will find U.S. goods cheaper.

b. The euro has appreciated, and Europeans will find U.S. goods more expensive.

c. The euro has depreciated, and Europeans will find U.S. goods more expensive.

d. The euro has depreciated, and Europeans will find U.S. goods cheaper.

a. The euro has appreciated, and Europeans will find U.S. goods cheaper.

b. The euro has appreciated, and Europeans will find U.S. goods more expensive.

c. The euro has depreciated, and Europeans will find U.S. goods more expensive.

d. The euro has depreciated, and Europeans will find U.S. goods cheaper.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

A foreign exchange trader quotes the dollar value of one euro as $/€ = 1.1510-1.1520.

These are direct bid-ask rates for a New York trader. What would be the implicit indirect

quotes for €/$?

These are direct bid-ask rates for a New York trader. What would be the implicit indirect

quotes for €/$?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

The euro is quoted as $/€ = 1.1420-1.1425, and the Canadian dollar is quoted as C$/US$ = 1.3540-1.3545. What is the implicit C$/€ quotation?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

The bid-ask rates are as follows:

Spot exchange rate:

CHF/USD: 1.5500-1.5540

Interest rates:

One-month CHF 31/2 - 5/8

One-year CHF 41/4 - 1/2

One-month USD 61/8 - 1/4

One-year USD 61/2 - 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange rates?

Spot exchange rate:

CHF/USD: 1.5500-1.5540

Interest rates:

One-month CHF 31/2 - 5/8

One-year CHF 41/4 - 1/2

One-month USD 61/8 - 1/4

One-year USD 61/2 - 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange rates?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

The euro is quoted as €/$ = 0.79610-0.79650, and the Australian dollar is quoted as A$/$ = 1.5675-1.5685. What is the implicit A$/€ quotation?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

You are a foreign exchange dealer. You see the following quote on your Reuter's screen:

a. The spot exchange rate of the Swedish krona is equal to 5.7 SKr per U.S. dollar. The three-month interest rates are 12% in SKr and 8% in dollars. What is the three-month forward exchange that you should quote?

b. In the language of currency traders would the Swedish krona be considered as "strong" or "weak" relative to the U.S. dollar?

c. Compute the annualized discount or premium on the dollar relative to the krona.

d. After a careful look at your screen, you discover that the spot exchange rate is really 5.7000-5.7015. The 12-month interest rates are 121/4 -1/2% in SKr and 81/4-1/2% in U.S. dollars. What should be the bid-ask quote on the one-year forward SKr/$ rate?

e. A Swedish exporting firm expects to be paid $1 million in three months. Please simulate the

SKr value of this payment if in three months, the spot exchange rate is equal to SKr/$ = 5 and

SKr/$ = 6. What would be the value of this payment if the firm had hedged against currency movements using the forward rate calculated in (a)?

a. The spot exchange rate of the Swedish krona is equal to 5.7 SKr per U.S. dollar. The three-month interest rates are 12% in SKr and 8% in dollars. What is the three-month forward exchange that you should quote?

b. In the language of currency traders would the Swedish krona be considered as "strong" or "weak" relative to the U.S. dollar?

c. Compute the annualized discount or premium on the dollar relative to the krona.

d. After a careful look at your screen, you discover that the spot exchange rate is really 5.7000-5.7015. The 12-month interest rates are 121/4 -1/2% in SKr and 81/4-1/2% in U.S. dollars. What should be the bid-ask quote on the one-year forward SKr/$ rate?

e. A Swedish exporting firm expects to be paid $1 million in three months. Please simulate the

SKr value of this payment if in three months, the spot exchange rate is equal to SKr/$ = 5 and

SKr/$ = 6. What would be the value of this payment if the firm had hedged against currency movements using the forward rate calculated in (a)?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

Here are some quotes of the Swiss franc/U.S. dollar spot exchange rate given simultaneously on the phone by three banks:

Bank A: 1.3435-1.3440

Bank B: 1.3435-1.3445

Bank C: 1.3445-1.3450

Are these quotes reasonable? Do you have an arbitrage opportunity?

Bank A: 1.3435-1.3440

Bank B: 1.3435-1.3445

Bank C: 1.3445-1.3450

Are these quotes reasonable? Do you have an arbitrage opportunity?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

The bid-ask rates are as follows:

Spot exchange rate:

CHF/USD: 1.4100-1.4140

Interest rates:

One-month CHF 11/2 - 5/8

One-year CHF 11/4 - 1/2

One-month USD 51/8 - 1/4

One-year USD 51/2 - 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange rates?

Spot exchange rate:

CHF/USD: 1.4100-1.4140

Interest rates:

One-month CHF 11/2 - 5/8

One-year CHF 11/4 - 1/2

One-month USD 51/8 - 1/4

One-year USD 51/2 - 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange rates?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

Here are some quotes for spot exchange rates and three-month interest rates:

Spot exchange rates:

$/€ 1.1865-1.1870

¥/$ 108.10-108.20

Interest rates:

Three-month euro-$ 5-51/4

Three-month euro-€ 31/4-31/2

Three-month euro-¥ 11/4-11/2

What should the quotes be for:

a. The ¥/€ spot exchange rate?

b. The €/$ three-month forward exchange rate?

c. The ¥/€ three-month forward exchange rate?

Spot exchange rates:

$/€ 1.1865-1.1870

¥/$ 108.10-108.20

Interest rates:

Three-month euro-$ 5-51/4

Three-month euro-€ 31/4-31/2

Three-month euro-¥ 11/4-11/2

What should the quotes be for:

a. The ¥/€ spot exchange rate?

b. The €/$ three-month forward exchange rate?

c. The ¥/€ three-month forward exchange rate?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

You visit the foreign exchange trading room of a major bank. A trader asks for quotations of the British pound from various correspondents and hears the following quotes:

From Bank A: 1.6580-1.6585

From Bank B: 1.6582-1.6587

What do they mean?

From Bank A: 1.6580-1.6585

From Bank B: 1.6582-1.6587

What do they mean?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

You noticed that the exchange rate between the Korean won and the U.S. dollar has changed considerably. The won/dollar exchange rate has moved from 800 won per dollar to 1000 won per dollar.

a. Has the Korean won appreciated or depreciated with respect to the dollar? By what percentage?

b. By what percentage has the value of the dollar changed with respect to the won?

a. Has the Korean won appreciated or depreciated with respect to the dollar? By what percentage?

b. By what percentage has the value of the dollar changed with respect to the won?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

The spot $/€ is equal to 1.1795. The one-year interest rates on the Eurocurrency market are 4% in euros and 5% in U.S. dollars. The one-month interest rates are 3% in euros and 4% in U.S. dollars.

a. What is the one-year forward exchange rate?

b. What is the one-month forward exchange rate?

a. What is the one-year forward exchange rate?

b. What is the one-month forward exchange rate?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.