Deck 12: Global Performance Evaluation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/10

Play

Full screen (f)

Deck 12: Global Performance Evaluation

1

You are a Swedish investor owning a portfolio of Swedish and American stocks. Their respective benchmarks are the OMX index and the S&P index. There have been no movements during the year (cash flows, sales, or purchase). Dividends of SKr 20,000 have been paid on Swedish stocks. Valuation and performance analysis is done in Swedish krona (SKr). Here are the valuations at the start and the end of the year:

a. What is the total value of the portfolio in SKr on January 1 and on December 31?

b. What is the total return on the portfolio?

c. Decompose this return into capital gain, yield, and currency contribution.

d. What is the contribution of security selection?

a. What is the total value of the portfolio in SKr on January 1 and on December 31?

b. What is the total return on the portfolio?

c. Decompose this return into capital gain, yield, and currency contribution.

d. What is the contribution of security selection?

a. The total SKr value of the portfolios on January 1 is:

SKr 600,000+ $100,000 * 6 SKr/$=SKr (600,000 + 600,000) = SKr 1,200,000.

The total SKr value of the portfolios on December 31 is:

SKr 660,000 + $140,000 *5.5 SKr/$ + SKr 20,000 =SKr (660,000 + 770,000 + 20,000)

= SKr 1,450,000.

b. The total return on the portfolio, measured in SKr is equal to: c. The capital gains amounts to:

660,000 - 600,000 = SKr 60,000 on the Swedish stocks or 10%,

$140,000 - $100,000 = $40,000 on the U.S. stocks or 40%.

If we use the SKr 6/$ exchange rate, this is (40,000)(6) = SKr 240,000. The total capital gain is then SKr 300,000 or 25%. Notice that this corresponds to a capital gain in local currency equal

to 0.5 * 10% + 0.5 * 40% =25%.

Also note that:

The dollar return on U.S. stock is 40% = 40,000/100,000.

The SKr return on U.S. stocks is 28.33% = (770,000 - 600,000)/600,000.

The yield comes from the dividends paid on Swedish stocks and can be calculated as follows:

Yield on Swedish stocks=SKr 20,000/SKr 600,000 = 3.33%.

Portfolio yield = Portfolio weights of Swedish stocks * yield of Swedish stocks

= 0.5*3.33% = 1.67%.

The currency contribution can be calculated as follows:

Currency contribution of U.S. investments =SKr return on U.S. stocks - $ return on U.S. stocks

= 28.33% -40% = -11.67%.

Portfolio currency contribution = Portfolio weights of U.S. stocks * currency contribution

= 0.5* (-11.67%) = -5.84%.

The total return of the portfolio can be decomposed as follows:

Total return of the portfolio =Capital gain + Yield +Currency contribution

= 25% + 1.67% -5.84%= 20.83%.

d. If the same amounts had been invested respectively in the OMX index and in the S&P index, returns would have been the following:

20% on the Swedish index.

25% on the U.S. index.

Portfolio-weighted market return in local currency = 0.5 *0.20 + 0.5 * 0.25 = 0.225 =22.5%.

We would have obtained 22.5% in local currency while our realized capital gain was 25%. Hence, security selection contributed positively for 2.5%. The Swedish portfolio only achieved a 10% capital gain, while the OMX index showed a 20% growth. However, the U.S. stock portfolio achieved a 40% capital gain (in dollars), while the S&P index showed a 25% appreciation.

Hence, the capital gain itself can be broken down into:

SKr 600,000+ $100,000 * 6 SKr/$=SKr (600,000 + 600,000) = SKr 1,200,000.

The total SKr value of the portfolios on December 31 is:

SKr 660,000 + $140,000 *5.5 SKr/$ + SKr 20,000 =SKr (660,000 + 770,000 + 20,000)

= SKr 1,450,000.

b. The total return on the portfolio, measured in SKr is equal to: c. The capital gains amounts to:

660,000 - 600,000 = SKr 60,000 on the Swedish stocks or 10%,

$140,000 - $100,000 = $40,000 on the U.S. stocks or 40%.

If we use the SKr 6/$ exchange rate, this is (40,000)(6) = SKr 240,000. The total capital gain is then SKr 300,000 or 25%. Notice that this corresponds to a capital gain in local currency equal

to 0.5 * 10% + 0.5 * 40% =25%.

Also note that:

The dollar return on U.S. stock is 40% = 40,000/100,000.

The SKr return on U.S. stocks is 28.33% = (770,000 - 600,000)/600,000.

The yield comes from the dividends paid on Swedish stocks and can be calculated as follows:

Yield on Swedish stocks=SKr 20,000/SKr 600,000 = 3.33%.

Portfolio yield = Portfolio weights of Swedish stocks * yield of Swedish stocks

= 0.5*3.33% = 1.67%.

The currency contribution can be calculated as follows:

Currency contribution of U.S. investments =SKr return on U.S. stocks - $ return on U.S. stocks

= 28.33% -40% = -11.67%.

Portfolio currency contribution = Portfolio weights of U.S. stocks * currency contribution

= 0.5* (-11.67%) = -5.84%.

The total return of the portfolio can be decomposed as follows:

Total return of the portfolio =Capital gain + Yield +Currency contribution

= 25% + 1.67% -5.84%= 20.83%.

d. If the same amounts had been invested respectively in the OMX index and in the S&P index, returns would have been the following:

20% on the Swedish index.

25% on the U.S. index.

Portfolio-weighted market return in local currency = 0.5 *0.20 + 0.5 * 0.25 = 0.225 =22.5%.

We would have obtained 22.5% in local currency while our realized capital gain was 25%. Hence, security selection contributed positively for 2.5%. The Swedish portfolio only achieved a 10% capital gain, while the OMX index showed a 20% growth. However, the U.S. stock portfolio achieved a 40% capital gain (in dollars), while the S&P index showed a 25% appreciation.

Hence, the capital gain itself can be broken down into:

2

On December 31, 1997, Long-Term Capital Management L.P. ("LTCM" or "Management Company") distributed approximately $2.7 billion of capital to investors in the fund that LTCM managed. Following a high return for 1997 (25.3% gross of fees and 17.1% net of fees) the fund's NAV (Net Asset Value) had swelled to $7.5 billion, and the share of the fund held by LTCM principals and employees had grown to $1.9 billion.

LTCM had notified investors in September, 1997 that it would be reducing investor capital in the fund at year-end. In a letter to investors, LTCM explained that it had decided to return to "non-strategic" investors the capital that was contributed between 1995 and 1997. The firm explained its reasoning in a letter to shareholders dated:

"As previously reported, the Fund has for some time been closed to new investment from non-Management Company investors with the exception of compelling cases of strategic value that would accrue from additional investment. From inception, the Fund has implemented its investment strategies subject to a constraint on its level of risk and subject to the requirement of maintaining adequate liquidity capital. The Management Company believes that these two constraints are not binding currently and the Fund has excess capital. This has occurred, primarily, because of a substantial increase in the capital base from the larger-than-expected, past realized rates of return, and high reinvestment rates elected by the Fund's investors. Therefore, it has become necessary to reduce the amount of capital significantly to bring the Fund's capital base more in line with its risk and liquidity needs."

The fund had set a risk target of an annual standard deviation (sigma) of NAV equal to 20% of NAV (approximately that of a U.S. stock portfolio). The expected profit (increase in NAV) for 1998 is $750 million (a daily expected profit of $3 million multiplied by 250 trading days per year).

Looking back, the daily sigma of NAV was $45 million, which translated in an annual sigma of

$710 million. This figure was estimated over past daily movements in NAV. The annual sigma is computed by multiplying the daily sigma by the square root of the number of trading days in a year (approximately 250 trading days). The mathematical arbitrage models used give a slightly higher theoretical figure equal to a daily sigma of $60 million, or annual sigma of $950 million. So the annual risk was well below the target of 20%. The empirical measure was less than 10% of NAV (710/7500) and the theoretical measure was 12.8% (950/7500). Because new arbitrage opportunities were hard to find, it was decided to get back to the risk target on NAV by reducing the capital base rather than expanding the arbitrage portfolio.

a. How much capital could LTCM reimburse to satisfy its 20% risk target (use the data from the mathematical arbitrage model)?

LTCM did calculate VaR. You will base your calculation on the theoretical sigma measures (daily sigma of $60 and annual sigma of $950). Remember that in a normal distribution, there is 5/100 chances to be below E(R) - 1.645 , where E(R) is the expected value and is the sigma. There is 1/100 chances to be below E(R) - 2.326 and 1/1000 chances to be below E(R) - 3.10 .

b. What is the daily VaR at 5% and 1%?

c. What is the annual VaR at 5% and 1%? Interpret your results.

d. Assume that the portfolio of LTCM is made up of 10 arbitrages, which each have a daily sigma of $19 million. They are all uncorrelated. What is the daily sigma for the fund?

e. It turns out that in periods of crisis the return on all arbitrages are perfectly correlated. Also the expected return becomes zero (instead of 750 million). What is the new daily sigma for the fund? What is the new annual sigma?

f. Under the assumptions of Question 5, what is the annual VaR at 1%?

LTCM had notified investors in September, 1997 that it would be reducing investor capital in the fund at year-end. In a letter to investors, LTCM explained that it had decided to return to "non-strategic" investors the capital that was contributed between 1995 and 1997. The firm explained its reasoning in a letter to shareholders dated:

"As previously reported, the Fund has for some time been closed to new investment from non-Management Company investors with the exception of compelling cases of strategic value that would accrue from additional investment. From inception, the Fund has implemented its investment strategies subject to a constraint on its level of risk and subject to the requirement of maintaining adequate liquidity capital. The Management Company believes that these two constraints are not binding currently and the Fund has excess capital. This has occurred, primarily, because of a substantial increase in the capital base from the larger-than-expected, past realized rates of return, and high reinvestment rates elected by the Fund's investors. Therefore, it has become necessary to reduce the amount of capital significantly to bring the Fund's capital base more in line with its risk and liquidity needs."

The fund had set a risk target of an annual standard deviation (sigma) of NAV equal to 20% of NAV (approximately that of a U.S. stock portfolio). The expected profit (increase in NAV) for 1998 is $750 million (a daily expected profit of $3 million multiplied by 250 trading days per year).

Looking back, the daily sigma of NAV was $45 million, which translated in an annual sigma of

$710 million. This figure was estimated over past daily movements in NAV. The annual sigma is computed by multiplying the daily sigma by the square root of the number of trading days in a year (approximately 250 trading days). The mathematical arbitrage models used give a slightly higher theoretical figure equal to a daily sigma of $60 million, or annual sigma of $950 million. So the annual risk was well below the target of 20%. The empirical measure was less than 10% of NAV (710/7500) and the theoretical measure was 12.8% (950/7500). Because new arbitrage opportunities were hard to find, it was decided to get back to the risk target on NAV by reducing the capital base rather than expanding the arbitrage portfolio.

a. How much capital could LTCM reimburse to satisfy its 20% risk target (use the data from the mathematical arbitrage model)?

LTCM did calculate VaR. You will base your calculation on the theoretical sigma measures (daily sigma of $60 and annual sigma of $950). Remember that in a normal distribution, there is 5/100 chances to be below E(R) - 1.645 , where E(R) is the expected value and is the sigma. There is 1/100 chances to be below E(R) - 2.326 and 1/1000 chances to be below E(R) - 3.10 .

b. What is the daily VaR at 5% and 1%?

c. What is the annual VaR at 5% and 1%? Interpret your results.

d. Assume that the portfolio of LTCM is made up of 10 arbitrages, which each have a daily sigma of $19 million. They are all uncorrelated. What is the daily sigma for the fund?

e. It turns out that in periods of crisis the return on all arbitrages are perfectly correlated. Also the expected return becomes zero (instead of 750 million). What is the new daily sigma for the fund? What is the new annual sigma?

f. Under the assumptions of Question 5, what is the annual VaR at 1%?

a. To satisfy a risk target of 20%, the needed capital X was such that:

20% = Sigmaannual/Needed capital = 950/X,

X = $4.750 billion.

So, LTCM could reimburse an excess capital of $7.5 - $4.75 = $2.75 billion.

b. The daily expected profit is $3 million and the daily dollar standard deviation is $60.

Vardaily @ 5% = 3 - 1.645 * 60 = $95.7 million.

Vardaily @ 1% = 3 - 2.326 * 60 = $136.6 million.

c. The annual expected profit is $750 million and the annual dollar standard deviation is $950.

Varannual(5%) = 750 - 1.645 *950 = $812.75 million.

Varannual(1%) =750 - 2.326 *950 =$1459.7 million.

LTCM had only a 1% probability to lose more than $1.46 billion.

d. The total variance is 10 times the variance of each trade, so the daily sigma is: .

The annual sigma is equal to the daily sigma times the square root of the number of trading days in a year (250 days): .

.

e. The risks are additive if the correlation is equal to one. So, the daily sigma is now: The annual sigma is: f. VaRannual(1%) = 0 - 2.326 =3004 = $ 6.987 billion.

In reality, LTCM got into serious problems in 1998 because it turned out that the risk on many

of its positions became strongly correlated. LTCM was profiting on its arbitrage because it was providing liquidity (it was pocketing the liquidity premium). When liquidity dried up in the summer of 1998 following the Russian crisis, all LTCM trades showed a loss. (See Case: Long-Term Capital Management, L.P. (C), Harvard Business School, Case 9-200-009, November 5, 1999.)

20% = Sigmaannual/Needed capital = 950/X,

X = $4.750 billion.

So, LTCM could reimburse an excess capital of $7.5 - $4.75 = $2.75 billion.

b. The daily expected profit is $3 million and the daily dollar standard deviation is $60.

Vardaily @ 5% = 3 - 1.645 * 60 = $95.7 million.

Vardaily @ 1% = 3 - 2.326 * 60 = $136.6 million.

c. The annual expected profit is $750 million and the annual dollar standard deviation is $950.

Varannual(5%) = 750 - 1.645 *950 = $812.75 million.

Varannual(1%) =750 - 2.326 *950 =$1459.7 million.

LTCM had only a 1% probability to lose more than $1.46 billion.

d. The total variance is 10 times the variance of each trade, so the daily sigma is: .

The annual sigma is equal to the daily sigma times the square root of the number of trading days in a year (250 days):

.e. The risks are additive if the correlation is equal to one. So, the daily sigma is now: The annual sigma is: f. VaRannual(1%) = 0 - 2.326 =3004 = $ 6.987 billion.

In reality, LTCM got into serious problems in 1998 because it turned out that the risk on many

of its positions became strongly correlated. LTCM was profiting on its arbitrage because it was providing liquidity (it was pocketing the liquidity premium). When liquidity dried up in the summer of 1998 following the Russian crisis, all LTCM trades showed a loss. (See Case: Long-Term Capital Management, L.P. (C), Harvard Business School, Case 9-200-009, November 5, 1999.)

3

You are provided below with annual return, standard deviation of returns, and tracking error to the relevant benchmark for three portfolios. Calculate the Sharpe ratio and information ratio for the three portfolios and rank them according to each measure.

Sharpe ratio calculations:

Portfolio Rank 2

Portfolio Rank 3

Portfolio Rank 1

Information ratio calculations:

Portfolio 1 = 100%. Rank 1

Portfolio Rank 3

Portfolio Rank 2

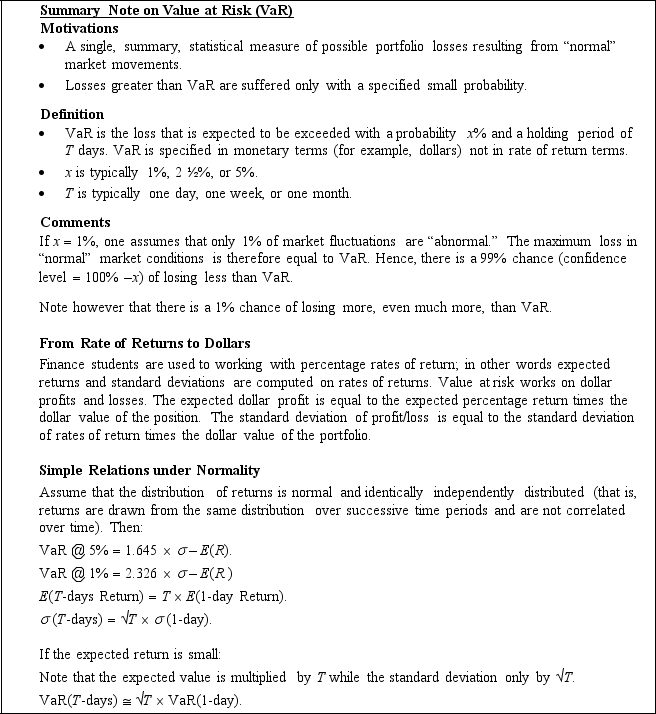

The next three problems deal with Value at Risk, which is not detailed in this textbook. A brief summary note on Value at Risk is given below.

Portfolio Rank 2

Portfolio Rank 3

Portfolio Rank 1

Information ratio calculations:

Portfolio 1 = 100%. Rank 1

Portfolio Rank 3

Portfolio Rank 2

The next three problems deal with Value at Risk, which is not detailed in this textbook. A brief summary note on Value at Risk is given below.

4

You have to compute the VaR (Value at Risk) of a portfolio with a probability of 5% (confidence level of 95%). Your portfolio is worth $100 million evenly invested in two assets (50 million in asset 1 and 50 million in asset 2). Here are some statistics for monthly returns of the two assets:

E(R1) = E(R2) = 0%

(R1) = 5%

(R2) = 7%

Correlation = 0.5.

You make the hypothesis that the distributions are normal.

You know that in a normal distribution 5% of the observations lie below -1.645* .

a. What is the monthly VaR of the portfolio with a 5% probability?

b. What is the one-year VaR of the portfolio with a 5% probability?

E(R1) = E(R2) = 0%

(R1) = 5%

(R2) = 7%

Correlation = 0.5.

You make the hypothesis that the distributions are normal.

You know that in a normal distribution 5% of the observations lie below -1.645* .

a. What is the monthly VaR of the portfolio with a 5% probability?

b. What is the one-year VaR of the portfolio with a 5% probability?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

5

You have to compute the VaR of a portfolio with a probability of 5% and 1% (confidence level of 95% and 99%). Your portfolio is worth $100 million evenly invested in two assets ($50 million in asset 1 and $50 million in asset 2). Here are some statistics for monthly returns of the two assets:

E(R1)=E(R2) =0.5%

(R1) = 8%

(R2) = 12%

Correlation = 0.4.

You make the hypothesis that the distributions are normal. We know that in a normal distribution with expected return E(R) and standard deviation , 5% of the observations lie below [E(R) - 1.645 * ] and 1% of the observations lie below [E(R) - 2.326 * ].

a. What is the one-month VaR of the portfolio with a 5% probability?

b. What is the one-month VaR of the portfolio with a 1% probability?

c. What is the one-year VaR of the portfolio with a 5% probability?

E(R1)=E(R2) =0.5%

(R1) = 8%

(R2) = 12%

Correlation = 0.4.

You make the hypothesis that the distributions are normal. We know that in a normal distribution with expected return E(R) and standard deviation , 5% of the observations lie below [E(R) - 1.645 * ] and 1% of the observations lie below [E(R) - 2.326 * ].

a. What is the one-month VaR of the portfolio with a 5% probability?

b. What is the one-month VaR of the portfolio with a 1% probability?

c. What is the one-year VaR of the portfolio with a 5% probability?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

6

A client invested $100 at the start of the month. Assume that the manager tracks an assigned benchmark index. The benchmark is at 100 at the start of the period. After 10 days the portfolio gained 10% (value =$110), just like the index, and the client added an extra $20 (total portfolio value =$130). From day 10 to 30, the portfolio, and the index, lost 9.09% [final portfolio value of $130 *

(1-0.0909)= $118.18].

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its benchmark?

(1-0.0909)= $118.18].

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its benchmark?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

7

A Japanese pension fund wants to invest ¥1 billion in U.S. equity. Its board of trustees must decide whether to invest in a commingled index fund tracking the S&P index or give the money to an active manager. The board learns that this active manager turns the portfolios over about twice a year. Given the size of the account, the overall transaction costs are likely to be an average of 0.75% of each transaction's value. The active manager charges 0.5% in annual management fees, and the indexer charges 0.15%. By how much should the active manager outperform the index to cover the extra costs in the form of fees and transaction costs on the annual turnover?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

8

You are a Swedish investor owning a portfolio of Swedish and American stocks. Their respective benchmarks are the OMX index and the S&P index. There have been no movements during the

year (cash flows, sales, or purchases, dividends paid). Valuation and performance analysis is done in Swedish krona (SKr). Here are the valuations at the start and the end of the year:

a. What is the total return on the portfolio?

b. Decompose this return into capital gain, yield, and currency contribution.

c. What is the contribution of security selection?

year (cash flows, sales, or purchases, dividends paid). Valuation and performance analysis is done in Swedish krona (SKr). Here are the valuations at the start and the end of the year:

a. What is the total return on the portfolio?

b. Decompose this return into capital gain, yield, and currency contribution.

c. What is the contribution of security selection?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

9

A client has €1 million invested in European equity at the start of the quarter. After one month the portfolio value is €1.1 million and the client who needs cash withdraws €200,000. At the end of the quarter the portfolio is worth €900,000. Over the quarter, the European equity index, used as a benchmark, gained 15%.

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its benchmark?

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its benchmark?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

10

You are an American investor holding some German stocks. Over the month, the value of your

stock portfolio goes from €5 million to €5.2 million. The exchange rates move from $1 per euro

to $0.98 per euro.

a. What is your rate of return in euros?

b. What is your rate of return in dollars?

c. Is the difference between the dollar return and the euro return exactly equal to the percentage movement in the exchange rate? If not, why?

stock portfolio goes from €5 million to €5.2 million. The exchange rates move from $1 per euro

to $0.98 per euro.

a. What is your rate of return in euros?

b. What is your rate of return in dollars?

c. Is the difference between the dollar return and the euro return exactly equal to the percentage movement in the exchange rate? If not, why?

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 10 flashcards in this deck.