Deck 11: Currency Risk Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/12

Play

Full screen (f)

Deck 11: Currency Risk Management

1

An asset manager has a mandate to manage a European equity portfolio for a U.S. pension client. The portfolio size is $100 million. The benchmark is some European equity index with a 50% currency hedging target. But the currency management is delegated to a currency overlay manager. The geographical breakdown of the portfolio on January 1 is as indicated below:

a. Assume that the currency overlay manager is neutral on currencies (that is, does not have specific forecasts on exchange rate). What would you expect the currency overlay manager to do on this portfolio?

b. Assume now that the currency overlay manager is bullish on the euro and pound but bearish on the Swiss franc (relative to the dollar). What kind of actions are you expecting from the currency overlay manager?

a. Assume that the currency overlay manager is neutral on currencies (that is, does not have specific forecasts on exchange rate). What would you expect the currency overlay manager to do on this portfolio?

b. Assume now that the currency overlay manager is bullish on the euro and pound but bearish on the Swiss franc (relative to the dollar). What kind of actions are you expecting from the currency overlay manager?

a. The currency overlay manager should try to align this portfolio with the benchmark. The target should be a 50% hedge ratio for all currencies. Hence, the currency overlay manager should sell forward (using forward or futures contracts) £5 million, €10 million, and SFr 700,000 against dollars.

This attitude assumes that the currency overlay manager is not responsible for the deviations of the portfolio's country weights relative to the benchmark's country weights. A more complex strategy would be to try to align the portfolio's currency weights with those of the benchmark. For example, assumes that Swiss equity have only a 2% weight in the European equity benchmark, while they have a 2.6% (2.6% F=1/38) in the portfolio; then the currency overlay manager could decide that the portfolio is overly exposed to the SFr and sell forward more

Swiss francs. In the benchmark, with a 50% hedge ratio, Swiss francs should only represent

1% =50% *2% of the portfolio. Hence, the SFr exposure of the portfolio should only be 1% of $38 million or $0.38 million. Given the 1.4 SFr/$ exchange rate, the SFr exposure should only

be SFr 532,000 = $0.38 million/1.4 SFr/$. So, the currency overlay manager would sell forward SFr 868,000 = SFr 1.4 million -SFr 532,000.

b. If the currency overlay has some specific forecasts, he will deviate from the neutral actions outlined above. For example, the currency overlay manager would sell forward less pounds and euros than outlined above and more Swiss francs. Active currency strategies could also involve currency options and dynamic strategies.

This attitude assumes that the currency overlay manager is not responsible for the deviations of the portfolio's country weights relative to the benchmark's country weights. A more complex strategy would be to try to align the portfolio's currency weights with those of the benchmark. For example, assumes that Swiss equity have only a 2% weight in the European equity benchmark, while they have a 2.6% (2.6% F=1/38) in the portfolio; then the currency overlay manager could decide that the portfolio is overly exposed to the SFr and sell forward more

Swiss francs. In the benchmark, with a 50% hedge ratio, Swiss francs should only represent

1% =50% *2% of the portfolio. Hence, the SFr exposure of the portfolio should only be 1% of $38 million or $0.38 million. Given the 1.4 SFr/$ exchange rate, the SFr exposure should only

be SFr 532,000 = $0.38 million/1.4 SFr/$. So, the currency overlay manager would sell forward SFr 868,000 = SFr 1.4 million -SFr 532,000.

b. If the currency overlay has some specific forecasts, he will deviate from the neutral actions outlined above. For example, the currency overlay manager would sell forward less pounds and euros than outlined above and more Swiss francs. Active currency strategies could also involve currency options and dynamic strategies.

2

Back in 1990, East Germany was in the process of merging into West Germany. Its national currency was to be replaced by the Deutsche mark (DM). A U.S. dollar-based investor has a portfolio worth DM 100 million in German bonds. The current spot exchange rate is 2 DM/$. The current one-year market interest rates are 6% in DM and 10% in dollars. One-year currency options are quoted in Chicago with a strike price of 50 U.S. cents per DM; a call DM is quoted at 1 U.S. cent and a put

DM is quoted at 1.2 U.S. cents; these option prices are for one DM.

You are worried that the integration of East and West Germany will cause inflation in Germany and a drop in the DM. So, you consider using forward contracts or options to hedge the currency risk.

a. What is the one-year forward exchange rate DM/$?

b. Simulate the dollar value of your portfolio assuming that its DM value stays at DM 100 million; use DM/$ spot exchange rates equal in one year to: 1.6, 1.8, 2, 2.2, and 2.4. First consider a currency forward hedge, then a currency-option insurance.

c. What could make your forward hedge imperfect?

DM is quoted at 1.2 U.S. cents; these option prices are for one DM.

You are worried that the integration of East and West Germany will cause inflation in Germany and a drop in the DM. So, you consider using forward contracts or options to hedge the currency risk.

a. What is the one-year forward exchange rate DM/$?

b. Simulate the dollar value of your portfolio assuming that its DM value stays at DM 100 million; use DM/$ spot exchange rates equal in one year to: 1.6, 1.8, 2, 2.2, and 2.4. First consider a currency forward hedge, then a currency-option insurance.

c. What could make your forward hedge imperfect?

a. The one-year forward exchange rate is: DM/$.

b. I need to buy DM puts. As the premium is paid in dollars, there is no exchange risk on the option premium. Assuming that I can finance the premium at a dollar interest rate of 0%, I would buy 100 million DM puts at a cost of:

Premium = ($0.012 per DM put) * (100 million DM puts) = $1.2 million.

c. Basis risk and cross-hedge risk.

b. I need to buy DM puts. As the premium is paid in dollars, there is no exchange risk on the option premium. Assuming that I can finance the premium at a dollar interest rate of 0%, I would buy 100 million DM puts at a cost of:

Premium = ($0.012 per DM put) * (100 million DM puts) = $1.2 million.

c. Basis risk and cross-hedge risk.

3

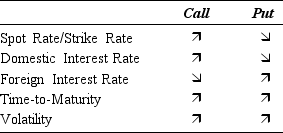

What are the major determinants of the value of a currency option (call and put)?

a. Briefly justify each determinant and its direction.

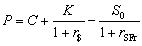

b. What is the relation between a currency put and a currency call (put-call parity)?

c. In what circumstances would an American-type option be exercised before expiration?

(You may provide an example to illustrate your answers.)

a. Briefly justify each determinant and its direction.

b. What is the relation between a currency put and a currency call (put-call parity)?

c. In what circumstances would an American-type option be exercised before expiration?

(You may provide an example to illustrate your answers.)

a. The main determinants of the value of a currency option are listed below. As an illustration, we consider options quoted in dollar (domestic currency) on the Swiss franc (foreign currency). For example, a call SFr gives the option to buy one SFr at a prespecified dollar value (for example, 0.7 $/SFr).

b. Let's denote

b. Let's denote

C the dollar premium of a call on the SFr with a strike K ($/SFr)

P the dollar premium of a put on the SFr with a strike K ($/SFr)

So the spot exchange rate ($/SFr)

rSFr the Swiss franc interest rate

r$ the U.S. dollar interest rate

By arbitrage, we must have the put-call parity: .

.

c. An American call SFr is likely to be exercised before maturity when it is in-the-money and the SFr interest rate is high (relative to the $ interest rate).

An American put SFr is likely to be exercised before maturity when it is in-the-money and the $ interest rate is high (relative to the SFr interest rate).

b. Let's denoteC the dollar premium of a call on the SFr with a strike K ($/SFr)

P the dollar premium of a put on the SFr with a strike K ($/SFr)

So the spot exchange rate ($/SFr)

rSFr the Swiss franc interest rate

r$ the U.S. dollar interest rate

By arbitrage, we must have the put-call parity:

.c. An American call SFr is likely to be exercised before maturity when it is in-the-money and the SFr interest rate is high (relative to the $ interest rate).

An American put SFr is likely to be exercised before maturity when it is in-the-money and the $ interest rate is high (relative to the SFr interest rate).

4

An Italian investor owns a portfolio of South Korean stocks worth 1.25 billion won. The current spot and one-month forward exchange rates are 1,250 won/€ (one won =0.0008 euro). Interest rates are equal in both countries. You are worried that some rumor about the bankruptcy of a major local bank could lead to a strong depreciation of the won. You have observed that Korean stocks tend to react negatively to a depreciation of the local currency (won). A broker tells you that a regression of Korean stock returns (measured in won) on the €/won percentage exchange rate movements has a slope of +0.50. In other words, Korean stocks tend to go down by 0.5% when the won depreciates

by 1%.

a. Discuss what your currency hedge ratio should be.

b. A month later, your Korean stock portfolio has gone down to 1.1875 billion won and the spot and forward exchange rates are now 0.00072 €/won. Analyze the return on your hedged portfolio.

by 1%.

a. Discuss what your currency hedge ratio should be.

b. A month later, your Korean stock portfolio has gone down to 1.1875 billion won and the spot and forward exchange rates are now 0.00072 €/won. Analyze the return on your hedged portfolio.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

5

A German corporation finalized a sale to a Thai client on April 15. The German corporation will deliver some gardening equipment on May 31 and will be paid 345 million baht on June 30. The current spot exchange rate is 40 baht/euro. The German corporation is worried about a depreciation

of the baht in the coming two months and wishes to sell those baht forward against euros.

a. Give some reasons why the German corporation should use forward rather than futures currency contracts.

b. Exactly what contract should the German corporation arrange with its bank?

of the baht in the coming two months and wishes to sell those baht forward against euros.

a. Give some reasons why the German corporation should use forward rather than futures currency contracts.

b. Exactly what contract should the German corporation arrange with its bank?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

6

A Japanese investor holds a portfolio of British stocks worth £10 million. The current three-month dollar/pound forward exchange rate is $/£ = 1.65, and the current three-month yen/dollar forward exchange rate is ¥/$ =100. What position should the Japanese investor take to hedge the pound/yen exchange risk?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

7

An American investor holds a British bond portfolio worth £100 million. The portfolio has a duration of 7. She fears a temporary depreciation of the pound but wishes to retain the bonds. To cover this risk, she decides to sell pounds forward. She has observed that the British government tends to adopt a "leaning-against-the-wind" policy. When the pound depreciates, British interest rates tend to rise to defend the currency. A regression of "variations in long-term British yields" on "percentage $/£ exchange rate movements" has a slope coefficient of -0.1. In other words, British yields tend to

go up by 10 basis points (0.1%) when the pound depreciates by 1% relative to the dollar.

a. What should be the optimal hedge ratio used by the investor if she wishes to reduce the uncertainty caused by exchange risk? (The investor uses only forward currency contracts to hedge this risk, not bond futures contracts.)

b. Detail the factors that could make this hedge imperfect if the depreciation of the pound materializes.

go up by 10 basis points (0.1%) when the pound depreciates by 1% relative to the dollar.

a. What should be the optimal hedge ratio used by the investor if she wishes to reduce the uncertainty caused by exchange risk? (The investor uses only forward currency contracts to hedge this risk, not bond futures contracts.)

b. Detail the factors that could make this hedge imperfect if the depreciation of the pound materializes.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

8

An American investor believes that the dollar will depreciate and buys one call option on the euro at an exercise price of 110 cents per euro. The option premium is 1 cent per euro, or $625 per contract of 62,500 euros (Philadelphia):

a. For what range of exchange rates should the investor exercise the call option at expiration?

b. For what range of exchange rates will the investor realize a net profit, taking the original cost

into account?

c. If the investor had purchased a put with the same exercise price and premium, instead of a call, how would you answer the previous two questions?

a. For what range of exchange rates should the investor exercise the call option at expiration?

b. For what range of exchange rates will the investor realize a net profit, taking the original cost

into account?

c. If the investor had purchased a put with the same exercise price and premium, instead of a call, how would you answer the previous two questions?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

9

An Italian importer will be paid $1 million in three months (March). He must decide whether to sell $1 million forward or to buy currency options for that amount.

The current market prices are as follows:

Exchange rates: Spot $/€ = 1.10

Three-month forward: $/€ = 1.11

Call euro March 110 U.S. cents: 1.5 U.S. cents per €.

Put euro March 110 U.S. cents: 1.0 U.S. cents per €.

What are the differences between the strategies of selling currency forward and buying currency options?

The current market prices are as follows:

Exchange rates: Spot $/€ = 1.10

Three-month forward: $/€ = 1.11

Call euro March 110 U.S. cents: 1.5 U.S. cents per €.

Put euro March 110 U.S. cents: 1.0 U.S. cents per €.

What are the differences between the strategies of selling currency forward and buying currency options?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

10

On April 1, an Australian investor decides to hedge a U.S. portfolio worth $10 million against exchange risk using AUD call options. The spot exchange rate is AUD/$ = 2.5 or $/AUD = 0.40.

The Australian investor can buy November calls AUD with a strike price of 0.40 U.S. cents per

AUD at a premium of 0.8 U.S. cent per AUD. The size of one contract is AUD 125,000. The delta

of the option is estimated at 0.5.

a. How many AUD calls should our investor buy to hedge the U.S. portfolio against the AUD/$ currency risk?

b. A few days later the U.S. dollar has dropped to AUD/$ = 2.463 ($/AUD =0.406) and the dollar value of the portfolio has remained unchanged at $10 million. The November 40 AUD call is now worth 1.2 cents per AUD and has a delta estimated at 0.7. What is the result of the hedge?

c. How should the hedge be adjusted?

The Australian investor can buy November calls AUD with a strike price of 0.40 U.S. cents per

AUD at a premium of 0.8 U.S. cent per AUD. The size of one contract is AUD 125,000. The delta

of the option is estimated at 0.5.

a. How many AUD calls should our investor buy to hedge the U.S. portfolio against the AUD/$ currency risk?

b. A few days later the U.S. dollar has dropped to AUD/$ = 2.463 ($/AUD =0.406) and the dollar value of the portfolio has remained unchanged at $10 million. The November 40 AUD call is now worth 1.2 cents per AUD and has a delta estimated at 0.7. What is the result of the hedge?

c. How should the hedge be adjusted?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

11

An American portfolio manager wishes to increases her exposure to Japanese stocks by $10 million without taking much foreign exchange risk. The spot exchange rate is ¥100 per dollar. She considers several alternatives:

Exchange Traded Funds (ETFs) are listed on the Tokyo stock exchange. The ETF is a traded fund that tracks the TOPIX index. Each share has a value of ¥1,000.

Futures contracts are available on the TOPIX index. Each contract is for ¥1,000 times the index. The current futures price of the TOPIX index is 1,000. The margin deposit per contract is ¥50,000.

At-the-money call options on the TOPIX index are available. Each contract is for ¥1,000 times the index. The premium on the call is ¥60 per index or ¥60,000 per contract.

What strategy could she adopt using those contracts?

Exchange Traded Funds (ETFs) are listed on the Tokyo stock exchange. The ETF is a traded fund that tracks the TOPIX index. Each share has a value of ¥1,000.

Futures contracts are available on the TOPIX index. Each contract is for ¥1,000 times the index. The current futures price of the TOPIX index is 1,000. The margin deposit per contract is ¥50,000.

At-the-money call options on the TOPIX index are available. Each contract is for ¥1,000 times the index. The premium on the call is ¥60 per index or ¥60,000 per contract.

What strategy could she adopt using those contracts?

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

12

Today is April 1st and you're French. You hold $1 million worth of American securities. You fear a depreciation of the dollar. The spot exchange rate is 0.80 $/€ or 1.25 €/$. The forward rate maturing July 1 is 1.255 €/$. Currency options on the euro are traded in Chicago. They are options on 1 euro, maturing July 1 and whose prices (premium and strike) are given in U.S. cents in the following table:

If you hedge using a forward contract, the bank requires no deposit. If you buy options, you must sell some of your U.S. securities in order to buy these options. You assume that your securities will keep exactly the same value on July 1.

a. You decide to hedge. What will be the euro value of your portfolio on July 1?

b. You decide to insure your portfolio using currency options. Do you need to buy/sell calls €/

puts €?

c. Assume that you use options with a strike of 80 U.S. cents. How many options do you need to insure perfectly your portfolio?

d. Same question with options with a strike of 85?

e. Simulate the results of your hedge and insurance with the two options if the spot exchange rate on July 1 is equal to 0.70 $/€, 0.80 $/€, and 0.90 $/€. Fill the following table with the value of the portfolio in euros:

Portfolio Value in Euros on July 1:

f. What is the best choice if you think that the chances of the depreciation of the $ are very weak but still exist.

If you hedge using a forward contract, the bank requires no deposit. If you buy options, you must sell some of your U.S. securities in order to buy these options. You assume that your securities will keep exactly the same value on July 1.

a. You decide to hedge. What will be the euro value of your portfolio on July 1?

b. You decide to insure your portfolio using currency options. Do you need to buy/sell calls €/

puts €?

c. Assume that you use options with a strike of 80 U.S. cents. How many options do you need to insure perfectly your portfolio?

d. Same question with options with a strike of 85?

e. Simulate the results of your hedge and insurance with the two options if the spot exchange rate on July 1 is equal to 0.70 $/€, 0.80 $/€, and 0.90 $/€. Fill the following table with the value of the portfolio in euros:

Portfolio Value in Euros on July 1:

f. What is the best choice if you think that the chances of the depreciation of the $ are very weak but still exist.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 12 flashcards in this deck.