Deck 8: Alternative Investments

Full screen (f)

Question

Question

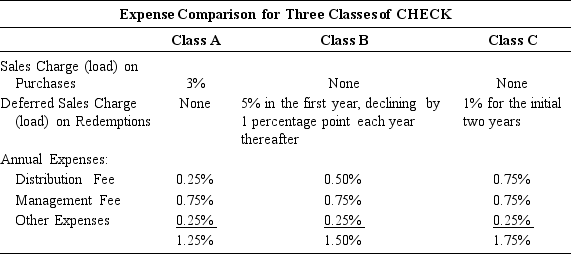

An investor is considering the purchase of CHECK Fund for his portfolio. Like many U.S.-based mutual funds today, CHECK has more than one class of shares. Although all classes hold the same portfolio of securities, each class has a different expense structure. This particular mutual fund

has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing CHECK is five years. He expects equity investments with risk characteristics similar to CHECK to earn 8% per year, and he decides to make his selection of fund share class based on an assumed 8% return each year, gross of any of the expenses given in the table above.

The time horizon associated with the investor's objective in purchasing CHECK is five years. He expects equity investments with risk characteristics similar to CHECK to earn 8% per year, and he decides to make his selection of fund share class based on an assumed 8% return each year, gross of any of the expenses given in the table above.

a. Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of NAV.

b. Suppose that, as a result of an unforeseen liquidity need, the investor needs to liquidate his investment at the end of the first year. Assume an 8% rate of return has been earned. Determine the relative performance of the three fund classes, and interpret the results.

has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing CHECK is five years. He expects equity investments with risk characteristics similar to CHECK to earn 8% per year, and he decides to make his selection of fund share class based on an assumed 8% return each year, gross of any of the expenses given in the table above.a. Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of NAV.

b. Suppose that, as a result of an unforeseen liquidity need, the investor needs to liquidate his investment at the end of the first year. Assume an 8% rate of return has been earned. Determine the relative performance of the three fund classes, and interpret the results.

Question

Question

Question

Question

Question

Question

Question

Question

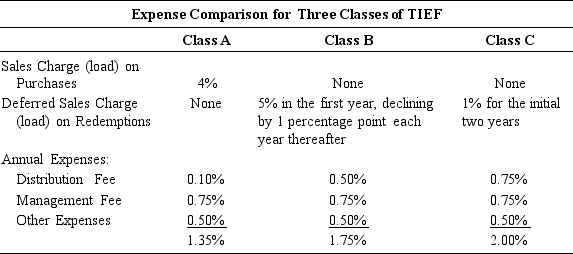

An investor is considering the purchase of Tata International Equity Fund (TIEF) for his portfolio. Like many U.S.-based mutual funds today, TIEF has more than one class of shares. Although all classes hold the same portfolio of securities, each class has a different expense structure. This particular mutual fund has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing TIEF is three years; he decides to specify it as just over three years. He expects equity investments with risk characteristics similar to TIEF to earn 10% per year, and he decides to make his selection of fund share class based on an assumed 10% return each year, gross of any of the expenses given in the table above.

The time horizon associated with the investor's objective in purchasing TIEF is three years; he decides to specify it as just over three years. He expects equity investments with risk characteristics similar to TIEF to earn 10% per year, and he decides to make his selection of fund share class based on an assumed 10% return each year, gross of any of the expenses given in the table above.

Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of net asset value (NAV).

The time horizon associated with the investor's objective in purchasing TIEF is three years; he decides to specify it as just over three years. He expects equity investments with risk characteristics similar to TIEF to earn 10% per year, and he decides to make his selection of fund share class based on an assumed 10% return each year, gross of any of the expenses given in the table above.Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of net asset value (NAV).

Question

Question

Question

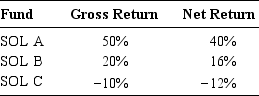

The SOL Group specializes in hedge funds invested on the Paf stock market. Over the year 1999, the Paf stock market index went up by 20%. The SOL Group had three hedge funds with very different investment strategies. As expected, the 1999 returns on the three funds were quite different. Here are the performances of the three funds before and after management fees set at 20% of gross profits:

The average gross performance of the three funds is exactly equal to the performance on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was closed. At the start of 2000, the SOL group launched an aggressive publicity campaign among portfolio managers, stressing the remarkable return on SOL A. If potential clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL Group mentioned the only other fund, SOL B, and claimed that their average gross performance during 1999 was 35%.

The average gross performance of the three funds is exactly equal to the performance on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was closed. At the start of 2000, the SOL group launched an aggressive publicity campaign among portfolio managers, stressing the remarkable return on SOL A. If potential clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL Group mentioned the only other fund, SOL B, and claimed that their average gross performance during 1999 was 35%.

What do you think of this publicity campaign?

The average gross performance of the three funds is exactly equal to the performance on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was closed. At the start of 2000, the SOL group launched an aggressive publicity campaign among portfolio managers, stressing the remarkable return on SOL A. If potential clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL Group mentioned the only other fund, SOL B, and claimed that their average gross performance during 1999 was 35%.What do you think of this publicity campaign?

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/14

Play

Full screen (f)

Deck 8: Alternative Investments

1

An investor estimates that investing €5 million in a particular venture capital project can return

$40 million at the end of five years if it succeeds; however, she realizes that the project may fail at any time between now and the end of the fifth year. The investor is considering an equity investment in the project and her cost of equity for a project with this level of risk is 15%. In the table below are the investor's estimates of certain probabilities of failure for the project. First, 0.30 is the probability of failure in year one. The probability that project fails in the second year, given that it has survived through year one, is 0.25; and so forth:

a. Determine the expected net present value of the project.

b. Recommend whether the project should be undertaken.

$40 million at the end of five years if it succeeds; however, she realizes that the project may fail at any time between now and the end of the fifth year. The investor is considering an equity investment in the project and her cost of equity for a project with this level of risk is 15%. In the table below are the investor's estimates of certain probabilities of failure for the project. First, 0.30 is the probability of failure in year one. The probability that project fails in the second year, given that it has survived through year one, is 0.25; and so forth:

a. Determine the expected net present value of the project.

b. Recommend whether the project should be undertaken.

a. The probability that the project survives to the end of the first year is (1 - 0.30) = 0.70. The probability that it survives to the end of second year is the product of the probability it survives the first year times the probability it survives the second year, or (1 -0.30) (1 - 0.25). Using this pattern, the probability that the firm survives to the end of the fifth year is (1- 0.30) (1 - 0.25)

(1 -0.20)3= (0.70) (0.75) (0.80)3 = 0.2688 or 26.88%.

There are two ways to compute the probability-weighted net present value.

A first approach is to weight each cash flow by its probability of occurrence. The initial investment of 1 million is certain (probability of 100%), the cash flow in five years has a probability of 26.88%. Hence the NPV is equal to: A second approach is to compute the NPV assuming first failure and then no failure, and to weight these NPVs by the probability of occurrence.

- The net present value of the project given that it survives to the end of the fifth year and thus earns €40 million equals €14.8871 million = -€5 million + €40 million/1.155.

- The net present value of project given that it fails is -€5 million.

Thus the project's expected NPV is a probability-weighted average of these two amounts, or (0.2688)(€14.8871 million) + (0.7312)( -€5 million) = €345,644.

Both approaches yield the same NPV.

b. Based on its positive net present value, the recommendation is to undertake the investment.

(1 -0.20)3= (0.70) (0.75) (0.80)3 = 0.2688 or 26.88%.

There are two ways to compute the probability-weighted net present value.

A first approach is to weight each cash flow by its probability of occurrence. The initial investment of 1 million is certain (probability of 100%), the cash flow in five years has a probability of 26.88%. Hence the NPV is equal to: A second approach is to compute the NPV assuming first failure and then no failure, and to weight these NPVs by the probability of occurrence.

- The net present value of the project given that it survives to the end of the fifth year and thus earns €40 million equals €14.8871 million = -€5 million + €40 million/1.155.

- The net present value of project given that it fails is -€5 million.

Thus the project's expected NPV is a probability-weighted average of these two amounts, or (0.2688)(€14.8871 million) + (0.7312)( -€5 million) = €345,644.

Both approaches yield the same NPV.

b. Based on its positive net present value, the recommendation is to undertake the investment.

2

An investor is considering the purchase of CHECK Fund for his portfolio. Like many U.S.-based mutual funds today, CHECK has more than one class of shares. Although all classes hold the same portfolio of securities, each class has a different expense structure. This particular mutual fund

has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing CHECK is five years. He expects equity investments with risk characteristics similar to CHECK to earn 8% per year, and he decides to make his selection of fund share class based on an assumed 8% return each year, gross of any of the expenses given in the table above.

a. Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of NAV.

b. Suppose that, as a result of an unforeseen liquidity need, the investor needs to liquidate his investment at the end of the first year. Assume an 8% rate of return has been earned. Determine the relative performance of the three fund classes, and interpret the results.

has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing CHECK is five years. He expects equity investments with risk characteristics similar to CHECK to earn 8% per year, and he decides to make his selection of fund share class based on an assumed 8% return each year, gross of any of the expenses given in the table above.a. Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of NAV.

b. Suppose that, as a result of an unforeseen liquidity need, the investor needs to liquidate his investment at the end of the first year. Assume an 8% rate of return has been earned. Determine the relative performance of the three fund classes, and interpret the results.

a. To address this question, we compute the terminal value of $1 invested at the end of year five

(or rather a day after the fifth year). The share class with the highest terminal value net of all expenses would be the most appropriate for this investor, as all classes are based on the same portfolio and thus have the same portfolio risk characteristics.

Class A. $1 *(1 - 0.03) = $0.97 is the amount available for investment at t = 0, after paying the front-end sales charge. Because this amount grows at 8% for five years, reduced by annual expenses of 0.0125, the terminal value per $1 invested after five years is $0.97 * 1.085 *(1 - 0.0125)5 =$1.3384.

Class B. Ignoring any deferred sales charge, after five years, $1 invested grows to $1 * 1.085 *

(1- 0.015)5 = $1.3624. According to the table, the deferred sales charge would be 1% at any

time during year five; therefore, the terminal value is $1.3624 * 0.99 =$1.3488.

Class C. After 5 years, $1 invested grows to $1 *1.085 * (1-0.0175)5 = $1.3452. There is no deferred sales charge in the fifth year, so $1.3452 is the terminal value.

In summary, the ranking by terminal value after five years is Class B ($1.3488), Class C ($1.3452), and Class A ($1.3384). Class B appears to be the most appropriate for this investor with a long-time horizon.

b. For Class A shares, the terminal value per $1 invested is $0.97 *1.08 * (1 -0.0125) = $1.0345. For Class B shares, it is as $1 * 1.08 * (1 -0.015) * (1 - 0.05) =$1.0106, reflecting a 5% redemption charge. For Class C shares, it is $1* 1.08 * (1 -0.0175) * (1 - 0.01) = $1.0505, reflecting a 1% redemption charge.

Thus, the ranking is Class C ($1.0505), Class A ($1.0345), and Class B ($1.0106). Although Class B is appropriate given a five-year investment horizon, it is a costly choice if the fund shares need to be liquidated soon after investment. That eventuality would need to be assessed by the investor we are discussing. Class B, like Class A, is more attractive, the longer the holding period, in general. Class A is more attractive than Class B if the shares are held for a very long time because annual expenses are lower. Because Class C has the higher annual expenses, however, it becomes less attractive the longer the holding period, in general.

(or rather a day after the fifth year). The share class with the highest terminal value net of all expenses would be the most appropriate for this investor, as all classes are based on the same portfolio and thus have the same portfolio risk characteristics.

Class A. $1 *(1 - 0.03) = $0.97 is the amount available for investment at t = 0, after paying the front-end sales charge. Because this amount grows at 8% for five years, reduced by annual expenses of 0.0125, the terminal value per $1 invested after five years is $0.97 * 1.085 *(1 - 0.0125)5 =$1.3384.

Class B. Ignoring any deferred sales charge, after five years, $1 invested grows to $1 * 1.085 *

(1- 0.015)5 = $1.3624. According to the table, the deferred sales charge would be 1% at any

time during year five; therefore, the terminal value is $1.3624 * 0.99 =$1.3488.

Class C. After 5 years, $1 invested grows to $1 *1.085 * (1-0.0175)5 = $1.3452. There is no deferred sales charge in the fifth year, so $1.3452 is the terminal value.

In summary, the ranking by terminal value after five years is Class B ($1.3488), Class C ($1.3452), and Class A ($1.3384). Class B appears to be the most appropriate for this investor with a long-time horizon.

b. For Class A shares, the terminal value per $1 invested is $0.97 *1.08 * (1 -0.0125) = $1.0345. For Class B shares, it is as $1 * 1.08 * (1 -0.015) * (1 - 0.05) =$1.0106, reflecting a 5% redemption charge. For Class C shares, it is $1* 1.08 * (1 -0.0175) * (1 - 0.01) = $1.0505, reflecting a 1% redemption charge.

Thus, the ranking is Class C ($1.0505), Class A ($1.0345), and Class B ($1.0106). Although Class B is appropriate given a five-year investment horizon, it is a costly choice if the fund shares need to be liquidated soon after investment. That eventuality would need to be assessed by the investor we are discussing. Class B, like Class A, is more attractive, the longer the holding period, in general. Class A is more attractive than Class B if the shares are held for a very long time because annual expenses are lower. Because Class C has the higher annual expenses, however, it becomes less attractive the longer the holding period, in general.

3

There are several ETFs listed on the American Stock Exchange (AMEX). One of them is iShares-Switzerland. This ETF tracks the Morgan Stanley Capital International (MSCI)-Switzerland index, which is based on several stocks that trade on the Swiss Exchange. The Swiss Exchange is open from 9 a.m.to 5:30 p.m. Swiss time and the AMEX is open from 9:30 a.m. to 4 p.m. U.S. Eastern Standard Time (EST). The U.S. EST lags the Swiss time by six hours. Discuss whether the ETF price and its NAV would fluctuate or stay the same during the time period when the AMEX is open.

When the AMEX market opens at 9:30 a.m., the time in Switzerland is 3:30 p.m. and the Swiss exchange is still open. The ETF shares in the United States would open at a price based on the NAV in Switzerland at that time and the prevailing dollar to Swiss franc exchange rate. From 9:30 a.m. to

11:30 a.m., both the AMEX and Swiss exchange are open, and the NAV in Switzerland would continue to change. The price of the ETF in dollars would also be changing consistent with the changes in NAV and exchange rate. Subsequently, from 11:30 a.m. to 4 p.m., the AMEX is open but the Swiss exchange is closed. So, the NAV in Swiss francs would remain the same. However, the price of the ETF in the United States would change based on the changes in expectations about the future stock prices in Switzerland and the changing exchange rate.

11:30 a.m., both the AMEX and Swiss exchange are open, and the NAV in Switzerland would continue to change. The price of the ETF in dollars would also be changing consistent with the changes in NAV and exchange rate. Subsequently, from 11:30 a.m. to 4 p.m., the AMEX is open but the Swiss exchange is closed. So, the NAV in Swiss francs would remain the same. However, the price of the ETF in the United States would change based on the changes in expectations about the future stock prices in Switzerland and the changing exchange rate.

4

A hedge fund has a capital of €100 million and invests in a market neutral long/short strategy on the European equity market. Shares can be borrowed from a primary broker. The arrangement with the primary broker is that the hedge fund deposits as guarantee securities with an equivalent market value at time of lending, plus an additional cash margin deposit equal to 10% of the value of the shares. The primary broker keeps any interest earned on the margin and charges a fee equal to an annual rate of 0.5% of the value of the shares borrowed. The hedge fund believes that European value stocks will outperform European growth stocks. The hedge fund expects that value stocks will outperform growth stocks by 5% over the year. The hedge fund wishes to retain a cash cushion of €10 million

for unforeseen events. The short-term euro interest rate is 3%.

a. What market-neutral strategy would you suggest that would take full advantage of this scenario?

b. What is the expected return according to the funds' expectations?

c. Assume now that the European stock index appreciates by 20% over the year, but that value stocks underperform growth stocks by 10%. Compute a likely market value of the fund at year's end.

for unforeseen events. The short-term euro interest rate is 3%.

a. What market-neutral strategy would you suggest that would take full advantage of this scenario?

b. What is the expected return according to the funds' expectations?

c. Assume now that the European stock index appreciates by 20% over the year, but that value stocks underperform growth stocks by 10%. Compute a likely market value of the fund at year's end.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

5

Survivorship bias is a serious potential problem in drawing conclusions from historical track records. Show why the following statements can be misleading:

a. "There are today 100 Type-A hedge funds in operation. Their average return over the past two years is 20%. Hence, they have outperformed the stock market (return of 15%)" [actually, some 50 funds disappeared during these two years].

b. "The Poupou commodity index has been back-calculated from 1970 to 1990 using the leading commodity futures contracts; by leading we mean those that have been most active. The Poupou commodity index had a remarkable performance from 1970 to 1995" [actually, several commodity futures contracts have been removed from the commodity exchange or have experienced a drop in trading activity].

a. "There are today 100 Type-A hedge funds in operation. Their average return over the past two years is 20%. Hence, they have outperformed the stock market (return of 15%)" [actually, some 50 funds disappeared during these two years].

b. "The Poupou commodity index has been back-calculated from 1970 to 1990 using the leading commodity futures contracts; by leading we mean those that have been most active. The Poupou commodity index had a remarkable performance from 1970 to 1995" [actually, several commodity futures contracts have been removed from the commodity exchange or have experienced a drop in trading activity].

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

6

G.O. Bug wants to invest $12,000 in gold. In December, the spot price of gold is $400 per ounce. Bug is very confident that gold will appreciate by at least 10% before the end of January and is willing to assume fairly risky positions to maximize the return on this forecast. Bug is considering several alternatives:

Gold bullion. Bug could buy 30 ounces, or roughly 1 kilogram.

Gold futures. Bug could buy February futures. These contracts trade at $413 per ounce, with an initial margin of $1,500 per contract of 100 ounces. Therefore, Bug could buy eight contracts (12,000/1,500).

Gold options. Bug considers two February call options with different strike prices. Each option contract covers 100 ounces. The February 410 call quotes at $8 per ounce; the February 430 call quotes at $4 per ounce. Therefore, Bug could buy fifteen contracts of the first option or thirty contracts of the second option.

Two gold mines. Mines A and B have the same stock price: $10 per share. A British broker has estimated the gold of both mines using a discounted cash flow model as well as historical regression analysis. Mine A is a rich mine with a gold equal to 2; mine B has much higher production costs with a gold equal to 5. Bug could buy 1,200 shares of one of the gold mines.

Bug quickly rules out investing directly in bullion, which does not offer enough leverage.

a. Assuming that Bug's expectations are realized by the end of February, compute the realized returns on the various alternative strategies considered. Simulate various values of the spot price of gold in February (320, 360, 380, 400, 420, and 480).

b. Which investment strategy would you suggest to Bug?

Gold bullion. Bug could buy 30 ounces, or roughly 1 kilogram.

Gold futures. Bug could buy February futures. These contracts trade at $413 per ounce, with an initial margin of $1,500 per contract of 100 ounces. Therefore, Bug could buy eight contracts (12,000/1,500).

Gold options. Bug considers two February call options with different strike prices. Each option contract covers 100 ounces. The February 410 call quotes at $8 per ounce; the February 430 call quotes at $4 per ounce. Therefore, Bug could buy fifteen contracts of the first option or thirty contracts of the second option.

Two gold mines. Mines A and B have the same stock price: $10 per share. A British broker has estimated the gold of both mines using a discounted cash flow model as well as historical regression analysis. Mine A is a rich mine with a gold equal to 2; mine B has much higher production costs with a gold equal to 5. Bug could buy 1,200 shares of one of the gold mines.

Bug quickly rules out investing directly in bullion, which does not offer enough leverage.

a. Assuming that Bug's expectations are realized by the end of February, compute the realized returns on the various alternative strategies considered. Simulate various values of the spot price of gold in February (320, 360, 380, 400, 420, and 480).

b. Which investment strategy would you suggest to Bug?

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

7

Let's assume that you are a U.S. investor who wants to invest $10,000 in gold. The current price of gold is $400, and you expect it to go up by 10% in the very short-term. You consider buying shares of gold mines; you are debating whether to invest in Bel Or or Schoen Gold. Your broker gives you the following information:

The gold is obtained by running a regression of the percentage price movements in the gold mine stock on the percentage price movements in gold bullion. It indicates the stock market price sensitivity to gold.

a. Explain why a gold mine with a high production cost should have a value that is more sensitive to gold price movements than a gold mine with low production costs.

b. Which mine would you buy and why?

c. What is your expected return, given this scenario?

The gold is obtained by running a regression of the percentage price movements in the gold mine stock on the percentage price movements in gold bullion. It indicates the stock market price sensitivity to gold.

a. Explain why a gold mine with a high production cost should have a value that is more sensitive to gold price movements than a gold mine with low production costs.

b. Which mine would you buy and why?

c. What is your expected return, given this scenario?

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

8

An investor wants to evaluate an apartment building using the income approach. She gathers the following data on the apartment complex; all income items are on an annual basis.

Two apartment buildings have recently been sold in the area. Building A had a sales price of $5 million with an annual net operating income of $500,000. Building B had a sales price of $1 million with an operating income of $95,000. Except for size, both buildings have characteristics (location, age, quality, . . .) similar to that of the apartment building under consideration.

According to the income approach, what is the value of the apartment complex?

Two apartment buildings have recently been sold in the area. Building A had a sales price of $5 million with an annual net operating income of $500,000. Building B had a sales price of $1 million with an operating income of $95,000. Except for size, both buildings have characteristics (location, age, quality, . . .) similar to that of the apartment building under consideration.

According to the income approach, what is the value of the apartment complex?

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

9

A hedge fund currently has assets of $500 million. The annual fee structure of this fund consists of a fixed fee of 1% of portfolio assets plus a 20% incentive fee. The fund applies the incentive fee to the gross return each year in excess of the portfolio's previous high watermark, which is the maximum fund value in the past two years. The fund is closed to new investors and the maximum value that the fund has achieved in the past two years was $520 million. Compute the fee that the manager will earn, in dollars, if the return on the fund in the coming year turns out to be:

a. 30%

b. 2%

c. -2%

a. 30%

b. 2%

c. -2%

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

10

An investor is considering the purchase of Tata International Equity Fund (TIEF) for his portfolio. Like many U.S.-based mutual funds today, TIEF has more than one class of shares. Although all classes hold the same portfolio of securities, each class has a different expense structure. This particular mutual fund has three classes of shares: A, B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor's objective in purchasing TIEF is three years; he decides to specify it as just over three years. He expects equity investments with risk characteristics similar to TIEF to earn 10% per year, and he decides to make his selection of fund share class based on an assumed 10% return each year, gross of any of the expenses given in the table above.

Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of net asset value (NAV).

The time horizon associated with the investor's objective in purchasing TIEF is three years; he decides to specify it as just over three years. He expects equity investments with risk characteristics similar to TIEF to earn 10% per year, and he decides to make his selection of fund share class based on an assumed 10% return each year, gross of any of the expenses given in the table above.Based on only the above information, determine the class of shares that is most appropriate for this investor. Assume that expense percentages given will be constant at the given values. Assume that the deferred sales charges are computed on the basis of net asset value (NAV).

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

11

An analyst is evaluating a real estate investment project using the discounted cash flow approach.

The net purchase price is $10 million, which is financed 20% by equity and 80% by a five-year mortgage loan. The loan carries an interest rate of 7%. Annual interest expenses on the $8 million loan are $560,000 and the loan is repaid in full after the fifth year.

The net operating income for the first year is estimated at $800,000 and is expected to grow annually at a 3% growth rate. Using straight-line depreciation over 50 years, the annual tax depreciation of the real estate project is equal to $200,000. It is expected that the property will be sold in five years

(just after the end of the fifth year) at a net price of $11 million.

The marginal income tax rate for this project is 30%. The capital gains tax rate is 20%.

The investor's cost of equity for projects with level of risk comparable to this real estate investment project is 15%.

a. Compute the after-tax cash flows resulting from the operating income for each of the first

five years.

b. Compute the after-tax cash flow for the fifth year, taking into account the resale value.

c. Compute the expected net present value (NPV) of the project and its internal rate of return (IRR).

d. State whether the investor should decide to invest in the project.

e. Compute the expected NPV and IRR of the project if the resale price is expected to be only

$10 million.

f. State whether the investor should decide to invest in this project under this new scenario.

The net purchase price is $10 million, which is financed 20% by equity and 80% by a five-year mortgage loan. The loan carries an interest rate of 7%. Annual interest expenses on the $8 million loan are $560,000 and the loan is repaid in full after the fifth year.

The net operating income for the first year is estimated at $800,000 and is expected to grow annually at a 3% growth rate. Using straight-line depreciation over 50 years, the annual tax depreciation of the real estate project is equal to $200,000. It is expected that the property will be sold in five years

(just after the end of the fifth year) at a net price of $11 million.

The marginal income tax rate for this project is 30%. The capital gains tax rate is 20%.

The investor's cost of equity for projects with level of risk comparable to this real estate investment project is 15%.

a. Compute the after-tax cash flows resulting from the operating income for each of the first

five years.

b. Compute the after-tax cash flow for the fifth year, taking into account the resale value.

c. Compute the expected net present value (NPV) of the project and its internal rate of return (IRR).

d. State whether the investor should decide to invest in the project.

e. Compute the expected NPV and IRR of the project if the resale price is expected to be only

$10 million.

f. State whether the investor should decide to invest in this project under this new scenario.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

12

A real estate company has prepared a simple hedonic model to value houses in a specific downtown area. A summary list of the houses' characteristics that can affect pricing are:

The number of main rooms.

The surface of the garden (if any).

The construction material (wood or brick).

The distance to a subway station.

A detailed statistical analysis of a large number of recent transactions in the area allowed to derive the following slope coefficients:

A typical house in the area has 5 main rooms, a garden of 500 square meters, constructed with bricks, and a distance of 300 meters to the nearest subway station. The transaction price for a typical house was €250,000.

a. You wish to value a house that has 7 rooms, a small garden of 100 square meters, constructed in wood, and a distance of 100 meters to the nearest subway station. What is the appraisal value based on this sales comparison approach of hedonistic price estimation?

b. You wish to value a house that has 7 rooms, a garden of 1,000 square meters, constructed in brick, and a distance of 1 kilometer to the nearest subway station. What is the appraisal value based on this sales comparison approach of hedonistic price estimation?

The number of main rooms.

The surface of the garden (if any).

The construction material (wood or brick).

The distance to a subway station.

A detailed statistical analysis of a large number of recent transactions in the area allowed to derive the following slope coefficients:

A typical house in the area has 5 main rooms, a garden of 500 square meters, constructed with bricks, and a distance of 300 meters to the nearest subway station. The transaction price for a typical house was €250,000.

a. You wish to value a house that has 7 rooms, a small garden of 100 square meters, constructed in wood, and a distance of 100 meters to the nearest subway station. What is the appraisal value based on this sales comparison approach of hedonistic price estimation?

b. You wish to value a house that has 7 rooms, a garden of 1,000 square meters, constructed in brick, and a distance of 1 kilometer to the nearest subway station. What is the appraisal value based on this sales comparison approach of hedonistic price estimation?

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

13

The SOL Group specializes in hedge funds invested on the Paf stock market. Over the year 1999, the Paf stock market index went up by 20%. The SOL Group had three hedge funds with very different investment strategies. As expected, the 1999 returns on the three funds were quite different. Here are the performances of the three funds before and after management fees set at 20% of gross profits:

The average gross performance of the three funds is exactly equal to the performance on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was closed. At the start of 2000, the SOL group launched an aggressive publicity campaign among portfolio managers, stressing the remarkable return on SOL A. If potential clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL Group mentioned the only other fund, SOL B, and claimed that their average gross performance during 1999 was 35%.

What do you think of this publicity campaign?

The average gross performance of the three funds is exactly equal to the performance on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was closed. At the start of 2000, the SOL group launched an aggressive publicity campaign among portfolio managers, stressing the remarkable return on SOL A. If potential clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL Group mentioned the only other fund, SOL B, and claimed that their average gross performance during 1999 was 35%.What do you think of this publicity campaign?

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

14

Exchange traded funds (ETFs) are usually considered to have many interesting properties. In the list below, indicate which statements DO NOT apply to ETFs:

a. ETFs allow to invest in a diversified portfolio.

b. ETFs are cost effective.

c. ETFs will never drop in value.

d. ETFs benefit from some attractive tax characteristics.

e. ETFs can be traded at any time during market opening.

f. ETFs are designed to take advantage of the manager's stock picking ability.

a. ETFs allow to invest in a diversified portfolio.

b. ETFs are cost effective.

c. ETFs will never drop in value.

d. ETFs benefit from some attractive tax characteristics.

e. ETFs can be traded at any time during market opening.

f. ETFs are designed to take advantage of the manager's stock picking ability.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 14 flashcards in this deck.