Deck 17: Dynamic Capital Structures and Corporate Valuation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

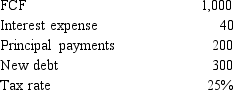

Volunteer Enterprises has the following information for the current year. Calculate its free cash flow to equity.

A) $1,070

B) $1,177

C) $1,295

D) $1,424

E) $1,567

A) $1,070

B) $1,177

C) $1,295

D) $1,424

E) $1,567

Question

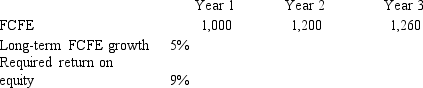

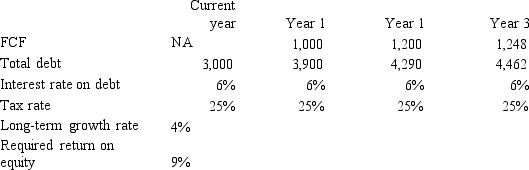

Epsilon Consultants has the following projected free cash flows to equity and other information. It has no non-operating assets. Calculate Epsilon's intrinsic value of equity using the FCFE model.

A) $28,440

B) $31,284

C) $34,413

D) $37,854

E) $41,640

A) $28,440

B) $31,284

C) $34,413

D) $37,854

E) $41,640

Question

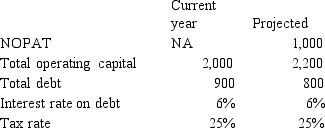

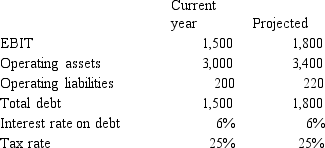

Gamma Pharmaceuticals has the following financial information for the current year and projected for next year. Calculate Gamma's projected free cash flow to equity.

A) $549

B) $604

C) $664

D) $730

E) $803

A) $549

B) $604

C) $664

D) $730

E) $803

Question

Raymond Supply, a national hardware chain, is considering purchasing a smaller chain, Strauss & Glazer Parts (SGP). Raymond's analysts project that the merger will result in the following incremental free cash flows, tax shields, and horizon values:

Assume that all cash flows occur at the end of the year. SGP is currently financed with 30% debt at a rate of 10%. The acquisition would be made immediately, and if it is undertaken, SGP would retain its current $15 million of debt and issue enough new debt to continue at the 30% target level. The interest rate would remain the same. SGP's pre-merger beta is 2.0, and its post-merger tax rate would be 34%. The risk-free rate is 8% and the market risk premium is 4%. Using the compressed adjusted present value approach, what is the value of SGP to Raymond?

A) $53.40 million

B) $61.96 million

C) $64.64 million

D) $76.96 million

E) $79.64 million

Assume that all cash flows occur at the end of the year. SGP is currently financed with 30% debt at a rate of 10%. The acquisition would be made immediately, and if it is undertaken, SGP would retain its current $15 million of debt and issue enough new debt to continue at the 30% target level. The interest rate would remain the same. SGP's pre-merger beta is 2.0, and its post-merger tax rate would be 34%. The risk-free rate is 8% and the market risk premium is 4%. Using the compressed adjusted present value approach, what is the value of SGP to Raymond?

A) $53.40 million

B) $61.96 million

C) $64.64 million

D) $76.96 million

E) $79.64 million

Question

Question

Question

Question

Question

Question

Question

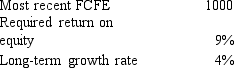

Eta Edibles had free cash flow to equity, required return, and long-term growth rate as indicated below. Eta has no non-operating assets. Calculate Eta's intrinsic value of equity using the FCFE model.

A) $18,909

B) $20,800

C) $22,880

D) $25,168

E) $27,685

A) $18,909

B) $20,800

C) $22,880

D) $25,168

E) $27,685

Question

Theta Therapeutics has the following information and projections. Use the FCFE model to calculate the intrinsic value of Theta's equity.

A) $14,156

B) $15,572

C) $17,129

D) $18,842

E) $20,726

A) $14,156

B) $15,572

C) $17,129

D) $18,842

E) $20,726

Question

Question

Question

Question

Question

Zeta Technologies has the following projections. It has no non-operating assets. Calculate Zeta's intrinsic value of equity using the FCFE model.

A) $21,165

B) $23,282

C) $25,610

D) $28,171

E) $30,988

A) $21,165

B) $23,282

C) $25,610

D) $28,171

E) $30,988

Question

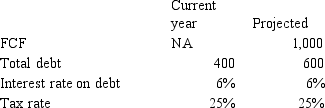

Alpha Manufacturing has the following financial information for the current year and projected for next year. Calculate its projected free cash flow to equity.

A) $893

B) $983

C) $1,081

D) $1,189

E) $1,308

A) $893

B) $983

C) $1,081

D) $1,189

E) $1,308

Question

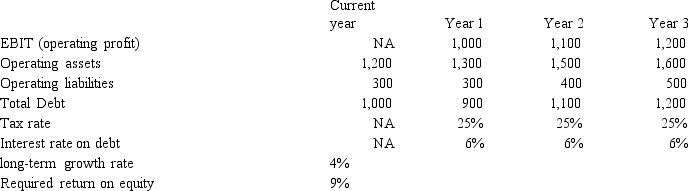

Gators Incorporated has the following information for the current year and projected for next year. Calculate its projected free cash flow to equity.

A) $1,066

B) $1,173

C) $1,290

D) $1,419

E) $1,561

A) $1,066

B) $1,173

C) $1,290

D) $1,419

E) $1,561

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 17: Dynamic Capital Structures and Corporate Valuation

1

In the compressed adjusted present value model, the appropriate discount rate for the tax shield is the WACC.

False

2

Which of the following statements concerning the compressed adjusted present value (APV) model is NOT CORRECT?

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity in the compressed apv model is greater than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc in the compressed apv model is greater than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm is independent of the amount of debt it uses.

E) the tax shields should be discounted at the unlevered cost of equity.

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity in the compressed apv model is greater than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc in the compressed apv model is greater than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm is independent of the amount of debt it uses.

E) the tax shields should be discounted at the unlevered cost of equity.

D

3

Which of the following statements concerning the compressed adjusted present value (APV) model is NOT CORRECT?

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity is greater in the compressed apv model than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc is greater in the compressed apv model than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm increases with the amount of debt.

E) the tax shields should be discounted at the cost of debt.

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity is greater in the compressed apv model than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc is greater in the compressed apv model than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm increases with the amount of debt.

E) the tax shields should be discounted at the cost of debt.

E

4

MM showed that in a world with taxes, a firm's optimal capital structure would be almost 100% debt.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

In the compressed adjusted present value model, the appropriate discount rate for the tax shield is the unlevered cost of equity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

Refer to data for Glassmaker Corporation. According to the compressed adjusted present value model, what discount rate should you use to discount Glassmaker's free cash flows and interest tax savings?

A) 10.01%

B) 10.06%

C) 11.29%

D) 11.44%

E) 13.49%

A) 10.01%

B) 10.06%

C) 11.29%

D) 11.44%

E) 13.49%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements about valuing a firm using the compressed adjusted present value (CAPV) approach is most CORRECT?

A) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the cost of debt.

B) the horizon value is calculated by discounting the expected earnings at the wacc.

C) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the wacc.

D) the horizon value must always be more than 20 years in the future.

E) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the levered cost of equity.

A) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the cost of debt.

B) the horizon value is calculated by discounting the expected earnings at the wacc.

C) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the wacc.

D) the horizon value must always be more than 20 years in the future.

E) the horizon value is calculated by discounting the free cash flows beyond the horizon date and any tax savings at the levered cost of equity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

In the compressed adjusted present value model, the appropriate discount rate for the tax shield is the after-tax cost of debt.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Refer to data for Kitto Electronics. According to the compressed adjusted present value model, what is Kitto's unlevered value?

A) $1,296,000

B) $1,440,000

C) $1,600,000

D) $1,760,000

E) $1,936,000

A) $1,296,000

B) $1,440,000

C) $1,600,000

D) $1,760,000

E) $1,936,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements concerning the compressed adjusted present value (APV) model is NOT CORRECT?

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity using the compressed apv model is greater than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc in the compressed apv model is less than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm increases with the amount of debt.

E) the tax shields should be discounted at the unlevered cost of equity.

A) the value of a growing tax shield is greater than the value of a constant tax shield.

B) for a given d/s, the levered cost of equity using the compressed apv model is greater than the levered cost of equity under mm's original (with tax) assumptions.

C) for a given d/s, the wacc in the compressed apv model is less than the wacc under mm's original (with tax) assumptions.

D) the total value of the firm increases with the amount of debt.

E) the tax shields should be discounted at the unlevered cost of equity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Refer to data for Glassmaker Corporation.Using the compressed adjusted present value model, what will Glassmaker's value of equity be if it successfully implements its planned changes in operations and capital structure? (Round your answer to the closest thousand dollars.)

A) $16,019,000

B) $17,111,000

C) $18,916,000

D) $22,111,000

E) $22,916,000

A) $16,019,000

B) $17,111,000

C) $18,916,000

D) $22,111,000

E) $22,916,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

The present value of the free cash flows discounted at the unlevered cost of equity is the value of the firm's operations if it had no debt.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

Using the data for Sallie's Sandwiches and the compressed adjusted present value model, what is the appropriate rate for use in discounting the free cash flows and the interest tax savings?

A) 12.0%

B) 13.9%

C) 14.4%

D) 16.0%

E) 16.9%

A) 12.0%

B) 13.9%

C) 14.4%

D) 16.0%

E) 16.9%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

According to MM, in a world without taxes the optimal capital structure for a firm is approximately 100% debt financing.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

MM showed that in a world without taxes, a firm's value is not affected by its capital structure.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Refer to data for Glassmaker Corporation. What is Glassmaker's WACC, based on its current capital structure?

A) 9.02%

B) 9.50%

C) 9.83%

D) 10.01%

E) 11.29%

A) 9.02%

B) 9.50%

C) 9.83%

D) 10.01%

E) 11.29%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

In a world with no taxes, MM show that a firm's capital structure does not affect the firm's value. However, when taxes are considered, MM show a positive relationship between debt and value, i.e., its value rises as its debt is increased.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements about valuing a firm using the compressed adjusted present value (CAPV) approach is most CORRECT?

A) the value of equity is calculated by discounting the horizon value, the tax shields, and the free cash flows at the cost of equity.

B) the value of operations is calculated by discounting the horizon value, the tax shields, and the free cash flows before the horizon date at the unlevered cost of equity.

C) the value of equity is calculated by discounting the horizon value and the free cash flows at the cost of equity.

D) the capv approach stands for the accounting pre-valuation approach.

E) the value of operations is calculated by discounting the horizon value, the tax shields, and the free cash flows at the cost of equity.

A) the value of equity is calculated by discounting the horizon value, the tax shields, and the free cash flows at the cost of equity.

B) the value of operations is calculated by discounting the horizon value, the tax shields, and the free cash flows before the horizon date at the unlevered cost of equity.

C) the value of equity is calculated by discounting the horizon value and the free cash flows at the cost of equity.

D) the capv approach stands for the accounting pre-valuation approach.

E) the value of operations is calculated by discounting the horizon value, the tax shields, and the free cash flows at the cost of equity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

Using the data for Sallie's Sandwiches and the compressed adjusted present value model, what is the total value (in millions)?

A) $72.37

B) $73.99

C) $74.49

D) $75.81

E) $76.45

A) $72.37

B) $73.99

C) $74.49

D) $75.81

E) $76.45

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

If the capital structure is stable, and free cash flows are expected to be growing at a constant rate at the horizon date, then the compressed adjusted present value model calculates the horizon value by discounting the post-horizon free cash flows and post-horizon expected future tax shields at the weighted average cost of capital.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Suppose a company issued 30-year bonds 4 years ago, when the yield curve was inverted. Since then long-term rates (10 years or longer) have remained constant, but the yield curve has resumed its normal upward slope. Under such conditions, a bond refunding would almost certainly be profitable.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

Volunteer Enterprises has the following information for the current year. Calculate its free cash flow to equity.

A) $1,070

B) $1,177

C) $1,295

D) $1,424

E) $1,567

A) $1,070

B) $1,177

C) $1,295

D) $1,424

E) $1,567

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

Epsilon Consultants has the following projected free cash flows to equity and other information. It has no non-operating assets. Calculate Epsilon's intrinsic value of equity using the FCFE model.

A) $28,440

B) $31,284

C) $34,413

D) $37,854

E) $41,640

A) $28,440

B) $31,284

C) $34,413

D) $37,854

E) $41,640

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

Gamma Pharmaceuticals has the following financial information for the current year and projected for next year. Calculate Gamma's projected free cash flow to equity.

A) $549

B) $604

C) $664

D) $730

E) $803

A) $549

B) $604

C) $664

D) $730

E) $803

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

Raymond Supply, a national hardware chain, is considering purchasing a smaller chain, Strauss & Glazer Parts (SGP). Raymond's analysts project that the merger will result in the following incremental free cash flows, tax shields, and horizon values:

Assume that all cash flows occur at the end of the year. SGP is currently financed with 30% debt at a rate of 10%. The acquisition would be made immediately, and if it is undertaken, SGP would retain its current $15 million of debt and issue enough new debt to continue at the 30% target level. The interest rate would remain the same. SGP's pre-merger beta is 2.0, and its post-merger tax rate would be 34%. The risk-free rate is 8% and the market risk premium is 4%. Using the compressed adjusted present value approach, what is the value of SGP to Raymond?

A) $53.40 million

B) $61.96 million

C) $64.64 million

D) $76.96 million

E) $79.64 million

Assume that all cash flows occur at the end of the year. SGP is currently financed with 30% debt at a rate of 10%. The acquisition would be made immediately, and if it is undertaken, SGP would retain its current $15 million of debt and issue enough new debt to continue at the 30% target level. The interest rate would remain the same. SGP's pre-merger beta is 2.0, and its post-merger tax rate would be 34%. The risk-free rate is 8% and the market risk premium is 4%. Using the compressed adjusted present value approach, what is the value of SGP to Raymond?

A) $53.40 million

B) $61.96 million

C) $64.64 million

D) $76.96 million

E) $79.64 million

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

The rate used to discount projected merger cash flows should be the cost of capital of the new consolidated firm because it incorporates the actual capital structure of the new firm.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

The market value of Firm L's debt is $200,000 and its yield is 9%. The firm's equity has a market value of $300,000, its earnings are growing at a rate of 5%, and its tax rate is 40%. A similar firm with no debt has a cost of equity of 12%. Using the compressed adjusted present value model, what is Firm L's cost of equity?

A) 11.4%

B) 12.0%

C) 12.6%

D) 13.3%

E) 14.0%

A) 11.4%

B) 12.0%

C) 12.6%

D) 13.3%

E) 14.0%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

Refer to data for Kitto Electronics. Using the compressed adjusted present value model, what is the value of Kitto's tax shield?

A) $156,385

B) $164,616

C) $173,280

D) $182,400

E) $192,000

A) $156,385

B) $164,616

C) $173,280

D) $182,400

E) $192,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

The market value of Firm L's debt is $200,000 and its yield is 9%. The firm's equity has a market value of $300,000, its earnings are growing at a 5% rate, and its tax rate is 40%. A similar firm with no debt has a cost of equity of 12%. Using the compressed adjusted present value model, what would Firm L's total value be if it had no debt?

A) $358,421

B) $377,286

C) $397,143

D) $417,000

E) $437,850

A) $358,421

B) $377,286

C) $397,143

D) $417,000

E) $437,850

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

The appropriate discount rate to use when analyzing a refunding decision is the after-tax cost of new debt, in part because there is relatively little risk of not realizing the interest savings.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

If the firm uses the after-tax cost of new debt as the discount rate when analyzing a refunding decision, and if the NPV of refunding is positive, then the value of the firm will be maximized if it immediately calls the outstanding debt and replaces it with an issue that has a lower coupon rate.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Eta Edibles had free cash flow to equity, required return, and long-term growth rate as indicated below. Eta has no non-operating assets. Calculate Eta's intrinsic value of equity using the FCFE model.

A) $18,909

B) $20,800

C) $22,880

D) $25,168

E) $27,685

A) $18,909

B) $20,800

C) $22,880

D) $25,168

E) $27,685

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

Theta Therapeutics has the following information and projections. Use the FCFE model to calculate the intrinsic value of Theta's equity.

A) $14,156

B) $15,572

C) $17,129

D) $18,842

E) $20,726

A) $14,156

B) $15,572

C) $17,129

D) $18,842

E) $20,726

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following factors would increase the likelihood that a company would call its outstanding bonds at this time?

A) a provision in the bond indenture lowers the call price on specific dates, and yesterday was one of those dates.

B) the flotation costs associated with issuing new bonds rise.

C) the firm's cfo believes that interest rates are likely to decline in the future.

D) the firm's cfo believes that corporate tax rates are likely to be increased in the future.

E) the yield to maturity on the company's outstanding bonds increases due to a weakening of the firm's financial situation.

A) a provision in the bond indenture lowers the call price on specific dates, and yesterday was one of those dates.

B) the flotation costs associated with issuing new bonds rise.

C) the firm's cfo believes that interest rates are likely to decline in the future.

D) the firm's cfo believes that corporate tax rates are likely to be increased in the future.

E) the yield to maturity on the company's outstanding bonds increases due to a weakening of the firm's financial situation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

When a firm refunds a debt issue, the firm's stockholders gain and its bondholders lose. This points out the risk of a call provision to bondholders and explains why a non-callable bond will typically command a higher price than an otherwise similar callable bond.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

A local firm has debt worth $200,000, with a yield of 9%, and equity worth $300,000. It is growing at a 5% rate, and its tax rate is 40%. A similar firm with no debt has a cost of equity of 12%. Using the compressed adjusted present value model, what is the value of your firm's tax shield, i.e., how much value does the use of debt add?

A) $92,571

B) $102,857

C) $113,143

D) $124,457

E) $136,903

A) $92,571

B) $102,857

C) $113,143

D) $124,457

E) $136,903

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Refer to data for Kitto Electronics. Using the compressed adjusted present value model, what is Kitto's value of equity?

A) $1,492,000

B) $1,529,300

C) $1,567,533

D) $1,606,721

E) $1,646,889

A) $1,492,000

B) $1,529,300

C) $1,567,533

D) $1,606,721

E) $1,646,889

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

Zeta Technologies has the following projections. It has no non-operating assets. Calculate Zeta's intrinsic value of equity using the FCFE model.

A) $21,165

B) $23,282

C) $25,610

D) $28,171

E) $30,988

A) $21,165

B) $23,282

C) $25,610

D) $28,171

E) $30,988

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Alpha Manufacturing has the following financial information for the current year and projected for next year. Calculate its projected free cash flow to equity.

A) $893

B) $983

C) $1,081

D) $1,189

E) $1,308

A) $893

B) $983

C) $1,081

D) $1,189

E) $1,308

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

Gators Incorporated has the following information for the current year and projected for next year. Calculate its projected free cash flow to equity.

A) $1,066

B) $1,173

C) $1,290

D) $1,419

E) $1,561

A) $1,066

B) $1,173

C) $1,290

D) $1,419

E) $1,561

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

Five years ago, NorthWest Water (NWW) issued $50,000,000 face value of 30-year bonds carrying a 14% (annual payment) coupon. NWW is now considering refunding these bonds. It has been amortizing $3 million of flotation costs on these bonds over their 30-year life. The company could sell a new issue of 25-year bonds at an annual interest rate of 11.67% in today's market. A call premium of 14% would be required to retire the old bonds, and flotation costs on the new issue would amount to $3 million. NWW's marginal tax rate is 40%. The new bonds would be issued when the old bonds are called.

Refer to the data for NorthWest Water (NWW). What is the NPV if NWW refunds its bonds today?

A) $1,746,987

B) $1,838,933

C) $1,935,719

D) $2,037,599

E) $2,241,359

Refer to the data for NorthWest Water (NWW). What is the NPV if NWW refunds its bonds today?

A) $1,746,987

B) $1,838,933

C) $1,935,719

D) $2,037,599

E) $2,241,359

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

Five years ago, the State of Oklahoma issued $2,000,000 of 7% coupon, 20-year semiannual payment, tax-exempt bonds. The bonds had 5 years of call protection, but now the state can call the bonds if it chooses to do so. The call premium would be 5% of the face amount. Today 15-year, 5%, semiannual payment bonds can be sold at par, but flotation costs on this issue would be 2%. What is the net present value of the refunding? Because these are tax-exempt bonds, taxes are not relevant.

A) $278,606

B) $292,536

C) $307,163

D) $322,521

E) $338,647

A) $278,606

B) $292,536

C) $307,163

D) $322,521

E) $338,647

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Five years ago, NorthWest Water (NWW) issued $50,000,000 face value of 30-year bonds carrying a 14% (annual payment) coupon. NWW is now considering refunding these bonds. It has been amortizing $3 million of flotation costs on these bonds over their 30-year life. The company could sell a new issue of 25-year bonds at an annual interest rate of 11.67% in today's market. A call premium of 14% would be required to retire the old bonds, and flotation costs on the new issue would amount to $3 million. NWW's marginal tax rate is 40%. The new bonds would be issued when the old bonds are called.

Refer to the data for NorthWest Water (NWW). What is the required after-tax refunding investment outlay, i.e., the cash outlay at the time of the refunding?

A) $5,049,939

B) $5,315,725

C) $5,595,500

D) $5,890,000

E) $6,200,000

Refer to the data for NorthWest Water (NWW). What is the required after-tax refunding investment outlay, i.e., the cash outlay at the time of the refunding?

A) $5,049,939

B) $5,315,725

C) $5,595,500

D) $5,890,000

E) $6,200,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

Stanovich Enterprises has 10-year, 12.0% semiannual coupon bonds outstanding. Each bond is now eligible to be called at a call price of $1,060. If the bonds are called, the company must replace them with new 10-year bonds. The flotation cost of issuing new bonds is estimated to be $45 per bond. How low would the yield to maturity on the new bonds have to be in order for it to be profitable to call the bonds today, i.e., what is the nominal annual "breakeven rate"?

A) 9.29%

B) 9.78%

C) 10.29%

D) 10.81%

E) 11.35%

A) 9.29%

B) 9.78%

C) 10.29%

D) 10.81%

E) 11.35%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

10 years ago, the City of Melrose issued $3,000,000 of 8% coupon, 30-year, semiannual payment, tax-exempt muni bonds. The bonds had 10 years of call protection, but now the bonds can be called if the city chooses to do so. The call premium would be 6% of the face amount. New 20-year, 6%, semiannual payment bonds can be sold at par, but flotation costs on this issue would be 2% of the amount of bonds sold. What is the net present value of the refunding? Note that cities pay no income taxes, hence taxes are not relevant.

A) $453,443

B) $476,115

C) $499,921

D) $524,917

E) $551,163

A) $453,443

B) $476,115

C) $499,921

D) $524,917

E) $551,163

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

Palmer Company has $5,000,000 of 15-year maturity bonds outstanding. Each bond has a maturity value of $1,000, an annual coupon of 12.0%. The bonds can be called at any time with a premium of $50 per bond. If the bonds are called, the company must pay flotation costs of $10 per new refunding bond. Ignore tax considerations?assume that the firm's tax rate is zero.??The company's decision of whether to call the bonds depends critically on the current interest rate on newly issued bonds. What is the breakeven interest rate, the rate below which it would be profitable to call in the bonds?

A) 9.57%

B) 10.07%

C) 10.60%

D) 11.16%

E) 11.72%

A) 9.57%

B) 10.07%

C) 10.60%

D) 11.16%

E) 11.72%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements is most CORRECT?

A) the key benefits associated with refunding debt are the reduction in the firm's debt ratio and the creation of more reserve borrowing capacity.

B) the mechanics of finding the npv of a refunding decision are fairly straightforward. however, the decision of when to refund is not always clear because it requires a forecast of future interest rates.

C) if a firm with a positive npv refunding project delays refunding and interest rates rise, the firm can still obtain the entire npv by locking in a low coupon rate when the rates are low, even though it actually refunds the debt after rates have risen.

D) suppose a firm is considering refunding and interest rates rise during time when the analysis is being done. the rise in rates would tend to lower the expected price of the new bonds, which would make them cheaper to the firm and thus increase the expected interest savings.

E) if new debt is used to refund old debt, the correct discount rate to use in the refunding analysis is the before-tax cost of new debt.

A) the key benefits associated with refunding debt are the reduction in the firm's debt ratio and the creation of more reserve borrowing capacity.

B) the mechanics of finding the npv of a refunding decision are fairly straightforward. however, the decision of when to refund is not always clear because it requires a forecast of future interest rates.

C) if a firm with a positive npv refunding project delays refunding and interest rates rise, the firm can still obtain the entire npv by locking in a low coupon rate when the rates are low, even though it actually refunds the debt after rates have risen.

D) suppose a firm is considering refunding and interest rates rise during time when the analysis is being done. the rise in rates would tend to lower the expected price of the new bonds, which would make them cheaper to the firm and thus increase the expected interest savings.

E) if new debt is used to refund old debt, the correct discount rate to use in the refunding analysis is the before-tax cost of new debt.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Five years ago, NorthWest Water (NWW) issued $50,000,000 face value of 30-year bonds carrying a 14% (annual payment) coupon. NWW is now considering refunding these bonds. It has been amortizing $3 million of flotation costs on these bonds over their 30-year life. The company could sell a new issue of 25-year bonds at an annual interest rate of 11.67% in today's market. A call premium of 14% would be required to retire the old bonds, and flotation costs on the new issue would amount to $3 million. NWW's marginal tax rate is 40%. The new bonds would be issued when the old bonds are called.

Refer to the data for NorthWest Water (NWW). The amortization of flotation costs reduces taxes and thus provides an annual cash flow. What will the net increase or decrease in the annual flotation cost tax savings be if refunding takes place?

A) $6,480

B) $7,200

C) $8,000

D) $8,800

E) $9,680

Refer to the data for NorthWest Water (NWW). The amortization of flotation costs reduces taxes and thus provides an annual cash flow. What will the net increase or decrease in the annual flotation cost tax savings be if refunding takes place?

A) $6,480

B) $7,200

C) $8,000

D) $8,800

E) $9,680

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Five years ago, NorthWest Water (NWW) issued $50,000,000 face value of 30-year bonds carrying a 14% (annual payment) coupon. NWW is now considering refunding these bonds. It has been amortizing $3 million of flotation costs on these bonds over their 30-year life. The company could sell a new issue of 25-year bonds at an annual interest rate of 11.67% in today's market. A call premium of 14% would be required to retire the old bonds, and flotation costs on the new issue would amount to $3 million. NWW's marginal tax rate is 40%. The new bonds would be issued when the old bonds are called.

Refer to the data for NorthWest Water (NWW). What will the after-tax annual interest savings for NWW be if the refunding takes place?

A) $664,050

B) $699,000

C) $768,900

D) $845,790

E) $930,369

Refer to the data for NorthWest Water (NWW). What will the after-tax annual interest savings for NWW be if the refunding takes place?

A) $664,050

B) $699,000

C) $768,900

D) $845,790

E) $930,369

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Holland Auto Parts is considering a merger with Workman Car Parts. Workman's market-determined beta is 0.9, and the firm currently is financed with 20% debt, at an interest rate of 8%, and its tax rate is 25%. If Holland acquires Workman, it will increase the debt to 60%, at an interest rate of 9%, and the tax rate will increase to 35%. The risk-free rate is 6% and the market risk premium is 4%. Using the Compressed APV Model, what will Workman's required rate of return on equity be after it is acquired?

A) 7.4%

B) 8.9%

C) 9.3%

D) 9.6%

E) 9.7%

A) 7.4%

B) 8.9%

C) 9.3%

D) 9.6%

E) 9.7%

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.