Deck 4: Complex Financial Instruments

Full screen (f)

Question

Question

Question

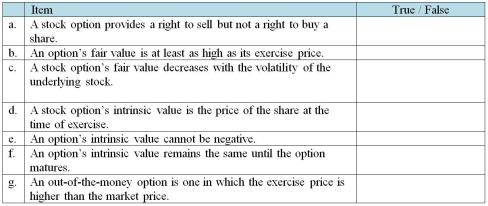

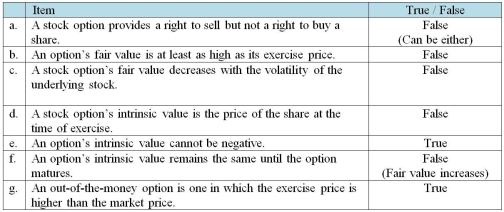

Indicate whether the following statements are true or false with respect to characteristics of stock options.

Question

Question

Question

Question

Question

Question

Question

Question

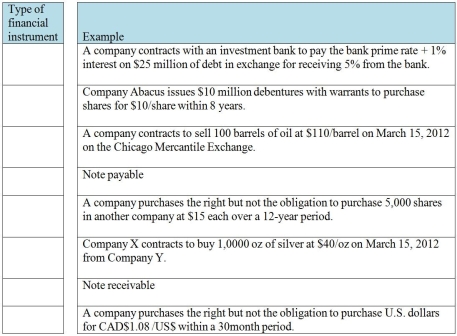

In the table below,choose the financial instrument that best explains the example on the right side. Types of financial instrument to select from: Financial asset,financial liability,equity,compound instrument,basic option,swap,forward,future,warrant,put option,or call option.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

LMN Company reported the following amounts on its balance sheet at July 31,2013:

Liabilities

Equity

Equity

Additional information

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Liabilities

Equity Additional information1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Question

Question

Question

Question

Question

LMN Company reported the following amounts on its balance sheet at July 31,2013:

Liabilities

Equity

Equity

Preferred shares,no par,3,000,000 shares authorized,10,000

Preferred shares,no par,3,000,000 shares authorized,10,000

Common shares,no par,1,000,000 shares authorized,180,000

Common shares,no par,1,000,000 shares authorized,180,000

Additional information

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Liabilities

Equity Preferred shares,no par,3,000,000 shares authorized,10,000 Common shares,no par,1,000,000 shares authorized,180,000 Additional information1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/89

Play

Full screen (f)

Deck 4: Complex Financial Instruments

1

Which of the following is an example of a "forward"?

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

C

2

What is a "call" option?

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

C

3

Indicate whether the following statements are true or false with respect to characteristics of stock options.

4

Which of the following is an example of a "future"?

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

5

What is a "warrant"?

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

6

What is a "future"?

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is not a financial instrument?

A)Stock warrants.

B)Preferred shares.

C)Deferred tax asset.

D)Options.

A)Stock warrants.

B)Preferred shares.

C)Deferred tax asset.

D)Options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

8

Explain how bonds issued with warrants alleviate adverse selection problem.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is an example of a "warrant"?

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

10

What is a "put" option?

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

11

In the table below,choose the financial instrument that best explains the example on the right side. Types of financial instrument to select from: Financial asset,financial liability,equity,compound instrument,basic option,swap,forward,future,warrant,put option,or call option.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

12

How should warrants on the company's own common shares be accounted for?

A)Fair value.

B)Fair value through profit or loss.

C)Amortized cost.

D)Historical cost.

A)Fair value.

B)Fair value through profit or loss.

C)Amortized cost.

D)Historical cost.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is correct about financial instruments?

A)Accounting for financial instruments has been consistent.

B)There is no economic substance to financial instruments.

C)They are often designed to circumvent accounting standards.

D)All financial instruments are accounted for at fair value.

A)Accounting for financial instruments has been consistent.

B)There is no economic substance to financial instruments.

C)They are often designed to circumvent accounting standards.

D)All financial instruments are accounted for at fair value.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is an example of a "swap"?

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

A)Right to buy 100 shares of CIBC over the next 5 years.

B)Commitment to buy 100 barrels of oil next month at $125/barrel.

C)Commitment to buy $100,000 US dollars in 4 months at US$=1.10.

D)Pay interest at prime +3% in exchange for receiving interest at 5%.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

15

What is an option?

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

A)A contract that gives the holder the right to sell an instrument at a pre-specified price.

B)A contract that is derived from some other underlying quantity,index,asset or event.

C)A contract that gives the holder the right to acquire an instrument at a pre-specified price.

D)A contract that gives the holder the right to buy or sell something at a specified price.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not an underlying?

A)Price of oil on New York Exchange.

B)Bank of Canada interest rate.

C)Conversion into 10 common shares.

D)US dollar exchange rate.

A)Price of oil on New York Exchange.

B)Bank of Canada interest rate.

C)Conversion into 10 common shares.

D)US dollar exchange rate.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

17

Which statement is correct about accounting for financial instruments?

A)All financial instruments are accounted for at fair value through profit or loss.

B)All are accounted for in accordance to their economic substance.

C)All financial instruments are accounted for at amortized cost.

D)All financial instruments are accounted for at fair value through OCI.

A)All financial instruments are accounted for at fair value through profit or loss.

B)All are accounted for in accordance to their economic substance.

C)All financial instruments are accounted for at amortized cost.

D)All financial instruments are accounted for at fair value through OCI.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

18

What is a "forward"?

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

19

What is a "swap"?

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

A)A contract in which two parties agree to exchange cash flows (e.g. interest cash flows).

B)A contract in which one party commits upfront to buy or sell commonly traded items at a defined price and maturity date.

C)A contract in which one party commits upfront to buy or sell something at a defined price at a defined future date.

D)A contact that gives the right,but not the obligation,to buy a share at a specified price over a specified period of time.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

20

Explain how convertible bonds alleviate moral hazard.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

21

Assume that MAK agrees to purchase US$500,000 for C$550,000 on January 15,2013. The exchange rate at year end is US$1 = C$0.95 and the January 15,2013 exchange rate is US$1 = C$0.97. What journal entry is required at year end?

A)0

B)$65,000 loss.

C)$75,000 gain.

D)$75,000 loss.

A)0

B)$65,000 loss.

C)$75,000 gain.

D)$75,000 loss.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

22

Sorrentino Corporation issued call options on 20,000 shares of BWC Inc. on October 21,2012. These options give the holder the right to buy BWC shares at $35 per share until May 17,2013. For issuing these options,Sorrentino received $20,000. On December 31,2012 (Sorrentino's fiscal year-end),the options traded on the Montreal Exchange for $2.00 per option. On May 17,2013,BWC's share price increased to $38 and the option holders exercised their options. Sorrentino had no holdings of BWC shares.

Requirement:

For Sorrentino Corporation,record the journal entries related to these call options.

Requirement:

For Sorrentino Corporation,record the journal entries related to these call options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

23

How should employee stock options be accounted for?

A)Historical cost.

B)Fair value through profit or loss.

C)Amortized cost.

D)Fair value.

A)Historical cost.

B)Fair value through profit or loss.

C)Amortized cost.

D)Fair value.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

24

How are derivative contracts generally accounted for?

A)Fair value.

B)Fair value through profit or loss.

C)Amortized cost.

D)Historical cost.

A)Fair value.

B)Fair value through profit or loss.

C)Amortized cost.

D)Historical cost.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

25

Which is a derivative on the company's own common shares?

A)Interest rate swap contract.

B)Foreign exchange forward contract.

C)Employee stock option.

D)Commodity futures contract.

A)Interest rate swap contract.

B)Foreign exchange forward contract.

C)Employee stock option.

D)Commodity futures contract.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

26

On August 15,2011,Madison Company issued 80,000 options on the shares of MVC (Middefield Valley Corporation). Each option gives the option holder the right to buy one share of MVC at $70 per share until March 16,2012. Madison received $800,000 for issuing these options. At the company's year-end of December 31,2011,the options contracts traded on the Montreal Exchange at $9.50 per contract. On March 16,2012,MVC shares closed at $63 per share,so none of the options was exercised.

Requirement:

Record the journal entries related to these call options.

Requirement:

Record the journal entries related to these call options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

27

On December 15,a company enters into a foreign currency forward to buy €300,000 at C$I.60 per euro in 30 days. The exchange rate on the day of the company's year-end of December 31 was C$1.59: €l.

Requirement:

Record the journal entries related to this forward contract.

Requirement:

Record the journal entries related to this forward contract.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

28

Assume that Millan agrees to purchase US$100,000 for C$84,745 on January 15,2013. The exchange rate at year end is US$1 = C$1.20 and the January 15,2013 exchange rate is US$1 = C$1.19. What journal entry is required at year end?

A)$701 loss.

B)$701 gain.

C)$711 loss.

D)$711 gain.

A)$701 loss.

B)$701 gain.

C)$711 loss.

D)$711 gain.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

29

Assume that Barun agrees to purchase US$500,000 for C$550,000 on January 15,2013. The exchange rate at year end is US$1 = C$0.95 and the January 15,2013 exchange rate is US$1 = C$0.97. What journal entry is required at Jan 15,2013?

A)$10,000 gain.

B)$10,000 loss.

C)$75,000 gain.

D)$75,000 loss.

A)$10,000 gain.

B)$10,000 loss.

C)$75,000 gain.

D)$75,000 loss.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

30

Assume that Signh agrees to purchase US$100,000 for C$84,745 on January 15,2013. The exchange rate at year end is US$1 = C$1.20 and the January 15,2013 exchange rate is US$1 = C$1.19. What journal entry is required at January 15,2013?

A)$701 loss.

B)$701 gain.

C)$711 loss.

D)$711 gain.

A)$701 loss.

B)$701 gain.

C)$711 loss.

D)$711 gain.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

31

Assume that Aero agrees to purchase US$50,000 for C$52,000 on January 15,2013. The exchange rate at year end is US$1 = C$0.98 and the January 15,2013 exchange rate is US$1 = C$0.97. What journal entry is required at Jan 15,2013?

A)$500 loss.

B)$500 gain.

C)$3,500 loss.

D)$3,500 gain.

A)$500 loss.

B)$500 gain.

C)$3,500 loss.

D)$3,500 gain.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

32

Roman Corporation issued call options on 5,000 shares of POMPEI Inc. on October 21,2012. These options give the holder the right to buy POMPEI shares at $35 per share until May 17,2013. For issuing these options,Roman received $15,000. On December 31,2012 (Roman's fiscal year-end),the options traded on the Montreal Exchange for $3.50 per option. On May 17,2013,POMPEI's share price increased to $40 and the option holders exercised their options. Roman had no holdings of POMPEI shares.

Requirement:

For Roman Corporation,record the journal entries related to these call options.

Requirement:

For Roman Corporation,record the journal entries related to these call options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

33

On December 15,a company enters into a foreign currency forward to buy €100,000 at C$I.60 per euro in 30 days. The exchange rate on the day of the company's year-end of December 31 was C$1.55: €l.

Requirement:

Record the journal entries related to this forward contract.

Requirement:

Record the journal entries related to this forward contract.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

34

Assume that Aero agrees to purchase US$50,000 for C$52,000 on January 15,2013. The exchange rate at year end is US$1 = C$0.98 and the January 15,2013 exchange rate is US$1 = C$0.97. What journal entry is required at year end?

A)$3,000 loss.

B)$3,000 gain.

C)$3,500 loss.

D)$3,500 gain.

A)$3,000 loss.

B)$3,000 gain.

C)$3,500 loss.

D)$3,500 gain.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

35

A company pays $5,000 to purchase futures contracts to buy 50 oz of silver at $40/oz. At the company's year-end,the price of silver rose and the value of the company's futures contracts increased to $6,000.

Requirement:

Record the journal entries related to these futures.

Requirement:

Record the journal entries related to these futures.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

36

Assume that Ariel agrees to purchase US$500,000 for C$550,000 on January 15,2013. The exchange rate at year end is US$1=C$0.95 and the January 15,2013 exchange rate is US$1=C$0.97. What journal entry is required when the contract is initiated?

A)0

B)$65,000 loss.

C)$75,000 gain.

D)$75,000 loss.

A)0

B)$65,000 loss.

C)$75,000 gain.

D)$75,000 loss.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

37

A company pays $7,000 to purchase futures contracts to buy 200 oz of gold at $1,600/oz. At the company's year-end,the price of gold was $1,625 and the value of the company's futures contracts increased to $10,000.

Requirement:

Record the journal entries related to these futures.

Requirement:

Record the journal entries related to these futures.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

38

Naples Corporation issued call options on 20,000 shares of VESPUS Inc. on October 21,2012. These options give the holder the right to buy VESPUS shares at $35 per share until May 17,2013. For issuing these options,Naples received $60,000. On December 31,2012 (Naples's fiscal year-end),the options traded on the Montreal Exchange for $3.50 per option. On May 17,2013,VESPUS's share price increased to $40 and the option holders exercised their options. Naples had no holdings of VESPUS shares.

Requirement:

For Naples Corporation,record the journal entries related to these call options.

Requirement:

For Naples Corporation,record the journal entries related to these call options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

39

On August 15,2011,Madison Company issued 10,000 options on the shares of MVC (Middefield Valley Corporation). Each option gives the option holder the right to buy one share of MVC at $70 per share until March 16,2012. Madison received $100,000 for issuing these options. At the company's year-end of December 31,2011,the options contracts traded on the Montreal Exchange at $9.50 per contract. On March 16,2012,MVC shares closed at $63 per share,so none of the options was exercised.

Requirement:

Record the journal entries related to these call options.

Requirement:

Record the journal entries related to these call options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

40

Which is a derivative on the company's own common shares?

A)Accounts payable.

B)Warrants on common shares.

C)Commodity futures contract.

D)Warranty provision.

A)Accounts payable.

B)Warrants on common shares.

C)Commodity futures contract.

D)Warranty provision.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

41

A company issues convertible bonds with face value of $7,000,000 and receives proceeds of $8,500,000. Each $1,000 bond can be converted,at the option of the holder,into 100 common shares. The underwriter estimated the market value of the bonds alone,excluding the conversion rights,to be approximately $7,300,000.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

42

Which statement best explains the accounting for compound instruments?

A)Once separated,each component is accounted for at fair value through profit or loss.

B)Once separated,each component is accounted for in accordance with its substance.

C)Once separated,each component is accounted for amortized cost.

D)Once separated,each component is accounted for at historical cost.

A)Once separated,each component is accounted for at fair value through profit or loss.

B)Once separated,each component is accounted for in accordance with its substance.

C)Once separated,each component is accounted for amortized cost.

D)Once separated,each component is accounted for at historical cost.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

43

A company had a debt-to-equity ratio of 1.55 before issuing convertible bonds. This ratio included $500,000 in equity. The company issued convertible bonds. The value reported for the bonds on the balance sheet is $180,000 and the conversion rights are valued at $22,000.

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

44

A company issued 105,000 preferred shares and received proceeds of $7,000,000. These shares have a par value of $50 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

45

Which method is used under ASPE to account for compound instruments?

A)Fair value method.

B)Proportional method.

C)Book value method.

D)Zero common equity method.

A)Fair value method.

B)Proportional method.

C)Book value method.

D)Zero common equity method.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

46

A company issued 95,000 preferred shares and received proceeds of $6,000,000. These shares have a par value of $48 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $64 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $8 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $64 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $8 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

47

A company had a debt-to-equity ratio of 1.64 before issuing convertible bonds. This ratio included $500,000 in equity. The company issued convertible bonds. The value reported for the bonds on the balance sheet is $180,000 and the conversion rights are valued at $22,000.

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

48

A company issued 100,000 preferred shares and received proceeds of $5,750,000. These shares have a par value of $50 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

49

LMN Company reported the following amounts on its balance sheet at July 31,2013:

Liabilities

Equity

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Liabilities

Equity Additional information1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 5 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

50

On January 1,2013,Wayward Co. issued a $22 million,8%,6-year convertible bond with annual coupon payments. Each $1,000 bond was convertible into 35 shares of Wayward's common shares. Moonbeam Investments purchased the entire bond issue for $22.7 million on January 1,2013. Moonbeam estimated that without the conversion feature,the bonds would have sold for $21,013,098 (to yield 9%).

On January 1,2015,Moonbeam converted bonds with a par value of $8.8 million. At the time of conversion,the shares were selling at $30 each.

Requirements:

a. Prepare the journal entry to record the issuance of convertible bonds.

b. Prepare the journal entry to record the conversion according to IFRS (book value method).

c. Prepare the journal entry to record the conversion according ASPE (market value method).

On January 1,2015,Moonbeam converted bonds with a par value of $8.8 million. At the time of conversion,the shares were selling at $30 each.

Requirements:

a. Prepare the journal entry to record the issuance of convertible bonds.

b. Prepare the journal entry to record the conversion according to IFRS (book value method).

c. Prepare the journal entry to record the conversion according ASPE (market value method).

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

51

A company issues convertible bonds with face value of $10,000,000 and receives proceeds of $10,500,000. Each $1,000 bond can be converted,at the option of the holder,into 800 common shares. The underwriter estimated the market value of the bonds alone,excluding the conversion rights,to be approximately $8,300,000.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

52

A company issued 105,000 preferred shares and received proceeds of $6,100,000. These shares have a par value of $50 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

53

How would the liability portion of the compound instrument be recorded?

A)Once separated,this component is accounted for at fair value through profit or loss.

B)Once separated,this component is accounted for in accordance with its substance.

C)Once separated,this component is accounted for amortized cost.

D)Once separated,this component is accounted for at historical cost.

A)Once separated,this component is accounted for at fair value through profit or loss.

B)Once separated,this component is accounted for in accordance with its substance.

C)Once separated,this component is accounted for amortized cost.

D)Once separated,this component is accounted for at historical cost.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

54

LMN Company reported the following amounts on its balance sheet at July 31,2013:

Liabilities

Equity

Preferred shares,no par,3,000,000 shares authorized,10,000

Common shares,no par,1,000,000 shares authorized,180,000

Additional information

1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Liabilities

Equity Preferred shares,no par,3,000,000 shares authorized,10,000 Common shares,no par,1,000,000 shares authorized,180,000 Additional information1. The bonds pay interest each July 31. Each $1,000 bond is convertible into 10 common shares. The bonds were originally issued to yield 10%. On July 31,2014,all the bonds were converted after the final interest payment was made. LMN uses the book value method to record bond conversions as recommended under IFRS.

2. No other share or bond transactions occurred during the year.

Requirement:

a. Prepare the journal entry to record the bond interest payment on July 31,2014.

b. Calculate the total number of common shares outstanding after the bonds' conversion on July 31,2014.

c. Prepare the journal entry to record the bond conversion.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

55

Which method is used under IFRS to account for compound instruments?

A)Fair value method.

B)Proportional method.

C)Incremental method.

D)Zero common equity method.

A)Fair value method.

B)Proportional method.

C)Incremental method.

D)Zero common equity method.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

56

Which statement best describes the "zero common equity method"?

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the least reliably measured amount.

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the least reliably measured amount.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

57

A company issues convertible bonds with face value of $5,000,000 and receives proceeds of $6,500,000. Each $1,000 bond can be converted,at the option of the holder,into 80 common shares. The underwriter estimated the market value of the bonds alone,excluding the conversion rights,to be approximately $6,300,000.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Requirement:

Record the journal entry for the issuance of these bonds based on IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

58

Which method is used under ASPE to account for compound instruments?

A)Incremental method.

B)Fair value method.

C)Proportional method.

D)Book value method.

A)Incremental method.

B)Fair value method.

C)Proportional method.

D)Book value method.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

59

A company had a debt-to-equity ratio of 1.65 before issuing convertible bonds. This ratio included $450,000 in equity. The company issued convertible bonds. The value reported for the bonds on the balance sheet is $200,000 and the conversion rights are valued at $25,000.

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Requirement:

After the issuance of the convertible bonds,what is the value of the debt-to-equity ratio?

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

60

A company issued 75,000 preferred shares and received proceeds of $7,000,000. These shares have a par value of $50 per share and pay cumulative dividends of 6%. Buyers of the preferred shares also received a detachable warrant with each share purchased. Each warrant gives the holder the right to buy one common share at $35 per share within 10 years.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

The underwriter estimated that the market value of the preferred shares alone,excluding the conversion rights,is approximately $55 per share. Shortly after the issuance of the preferred shares,the detachable warrants traded at $5 each.

Requirement:

Record the journal entry for the issuance of these shares and warrants under IFRS.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

61

Which statement best describes the "proportional method"?

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the least reliably measured amount.

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the least reliably measured amount.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

62

How would exercise of the conversion option,that was part of the initial compound instrument,be recorded?

A)Common stock is recorded at an amount equal to the fair value of the options at date of conversion.

B)Common stock is recorded at an amount equal to the price determined by the Black-Sholes model.

C)Common stock is recorded at an amount equal to the market price of the shares on conversion date.

D)Common stock is recorded at an amount equal to the cash received plus the contributed surplus initially recorded.

A)Common stock is recorded at an amount equal to the fair value of the options at date of conversion.

B)Common stock is recorded at an amount equal to the price determined by the Black-Sholes model.

C)Common stock is recorded at an amount equal to the market price of the shares on conversion date.

D)Common stock is recorded at an amount equal to the cash received plus the contributed surplus initially recorded.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

63

Which statement is not correct for the "proportional method"?

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the most reliably measured amount.

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the most reliably measured amount.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

64

How is the subsequent conversion of bonds into common shares recorded under IFRS?

A)Book value.

B)Market value.

C)Fair value.

D)Historical value.

A)Book value.

B)Market value.

C)Fair value.

D)Historical value.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

65

Price Farms granted 290,000 stock options to its employees. The options expire 45 years after the grant date of January 1,2011,when the share price was $23. Employees still employed by Price five years after the grant date may exercise the option to purchase shares at $45 each; that is,the options vest to the employees after five years. A consultant estimated the value of each option at the date of grant to be $1.50 each.

Requirement:

Record the journal entries relating to the issuance of stock options.

Requirement:

Record the journal entries relating to the issuance of stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

66

AnnuG Inc. granted 200,000 stock options to its employees. The options expire 45 years after the grant date of January 1,2011,when the share price was $23. Employees still employed by the company six years after the grant date may exercise the option to purchase shares at $45 each; that is,the options vest to the employees after five years. A consultant estimated the value of each option at the date of grant to be $2.50 each.

Requirement:

Record the journal entries relating to the issuance of stock options.

Requirement:

Record the journal entries relating to the issuance of stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

67

Explain the meaning of and the difference between the book value and market value to record the conversion of bonds into common shares.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

68

McMillan Manufacturing issued 60,000 stock options to its employees. The company granted the stock options at-the-money,when the share price was $40. These options have no vesting conditions. By year-end,the share price had increased to $42. McMillan's management estimates the value of these options at the grant date to be $1.10 each.

Requirement:

Record the issuance of the stock options.

Requirement:

Record the issuance of the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

69

Windy Lake Lodge issued 24,000 at-the-money stock options to its management on January 1,2012. These options vest on January 1,2015. Windy Lake's share price was $19 on the grant date and $22 on the vesting date. Estimates of the fair value of the options showed that they were worth $3 on the grant date and $11 on the vesting date. On the vesting date,management exercised all 24,000 options. Windy Lake has a December 31 year-end.

Requirement:

Record all of the journal entries relating to the stock options.

Requirement:

Record all of the journal entries relating to the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

70

Which statement best describes the "incremental method"?

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the most reliably measured amount.

A)Under this method of accounting,for a convertible bond,all of the bond value would be counted as a liability.

B)Under this method of accounting,for a convertible bond,the issuing entity would record a liability for the estimated value of the bond without the conversion feature.

C)Under this method of accounting,for a convertible bond,an estimate would be made of the fair value of all components and allocated proportionally to all components.

D)Under this method of accounting,the common share component is considered the most reliably measured amount.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

71

Princeton Inc. granted 290,000 stock options to its employees. The options expire 45 years after the grant date of January 1,2011,when the share price was $23. Employees still employed by the company four years after the grant date may exercise the option to purchase shares at $45 each; that is,the options vest to the employees after five years. A consultant estimated the value of each option at the date of grant to be $2.50 each.

Requirement:

Record the journal entries relating to the issuance of stock options.

Requirement:

Record the journal entries relating to the issuance of stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

72

Which statement is correct about the accounting for employee stock options?

A)The expense is recorded over the period of vesting.

B)The expense is recorded over the period to expiry.

C)The expense is recorded immediately upon grant date.

D)No expense is recorded for accounting purposes.

A)The expense is recorded over the period of vesting.

B)The expense is recorded over the period to expiry.

C)The expense is recorded immediately upon grant date.

D)No expense is recorded for accounting purposes.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

73

How is the subsequent conversion of bonds into common shares recorded under IFRS?

A)Book value.

B)Market value.

C)Fair value.

D)Historical value.

A)Book value.

B)Market value.

C)Fair value.

D)Historical value.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

74

Nappy Lodge issued 15,000 at-the-money stock options to its management on January 1,2012. These options vest on January 1,2015. Nappy's share price was $20 on the grant date and $25 on the vesting date. Estimates of the fair value of the options showed that they were worth $3 on the grant date and $11 on the vesting date. On the vesting date,management exercised all 24,000 options. Nappy has a December 31 year-end.

Requirement:

Record all of the journal entries relating to the stock options.

Requirement:

Record all of the journal entries relating to the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

75

How would exercise of warrants,that were part of the original compound instrument,be recorded?

A)Common stock is recorded at an amount equal to the fair value of the options at date of conversion.

B)Common stock is recorded at an amount equal to the cash received plus the contributed surplus initially recorded

C)Common stock is recorded at an amount equal to the market price of the shares on conversion date.

D)Common stock is recorded at an amount equal to the price determined by the Black-Sholes model.

A)Common stock is recorded at an amount equal to the fair value of the options at date of conversion.

B)Common stock is recorded at an amount equal to the cash received plus the contributed surplus initially recorded

C)Common stock is recorded at an amount equal to the market price of the shares on conversion date.

D)Common stock is recorded at an amount equal to the price determined by the Black-Sholes model.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

76

Breezy Lodge issued 25,000 at-the-money stock options to its management on January 1,2012. These options vest on January 1,2015. Breezy's share price was $18 on the grant date and $25 on the vesting date. Estimates of the fair value of the options showed that they were worth $4 on the grant date and $11 on the vesting date. On the vesting date,management exercised all 24,000 options. Breezy has a December 31 year-end.

Requirement:

Record all of the journal entries relating to the stock options.

Requirement:

Record all of the journal entries relating to the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

77

Which method must be used under IFRS to account for employee stock options?

A)Intrinsic value of options.

B)Time value of options.

C)Market value of the shares.

D)Fair value of the options.

A)Intrinsic value of options.

B)Time value of options.

C)Market value of the shares.

D)Fair value of the options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

78

O'Neil Manufacturing issued 200,000 stock options to its employees. The company granted the stock options at-the-money,when the share price was $40. These options have no vesting conditions. By year-end,the share price had increased to $42. O'Neil's management estimates the value of these options at the grant date to be $1.75 each.

Requirement:

Record the issuance of the stock options.

Requirement:

Record the issuance of the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

79

How would the equity portion of the compound instrument be recorded?

A)Once separated,this component is accounted for at fair value through profit or loss.

B)Once separated,this component is accounted for in accordance with its substance.

C)Once separated,this component is accounted for amortized cost.

D)Once separated,this component is accounted for at historical cost.

A)Once separated,this component is accounted for at fair value through profit or loss.

B)Once separated,this component is accounted for in accordance with its substance.

C)Once separated,this component is accounted for amortized cost.

D)Once separated,this component is accounted for at historical cost.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

80

O'Neil Motor Parts issued 110,000 stock options to its employees. The company granted the stock options at-the-money,when the share price was $40. These options have no vesting conditions. By year-end,the share price had increased to $42. O'Neil's management estimates the value of these options at the grant date to be $1.60 each.

Requirement:

Record the issuance of the stock options.

Requirement:

Record the issuance of the stock options.

Unlock Deck

Unlock for access to all 89 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 89 flashcards in this deck.