Deck 11: Consolidation: Intragroup Transactions

Full screen (f)

Question

Question

Question

Question

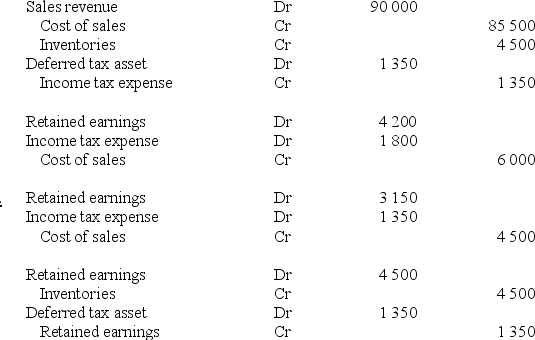

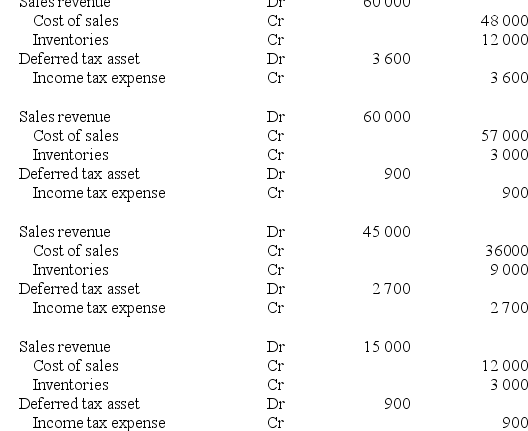

During the year ended 30 June 2017, a subsidiary sold inventories to a parent for $90 000. The inventories had previously cost the subsidiary entity $72 000. By 30 June 2017 the parent had sold 75% of the inventories to a party outside the group. The remaining inventories were sold externally in July 2017. The company tax rate is 30%. Which of the following is the adjustment entry in the consolidation worksheet at 30 June 2018?

Question

Question

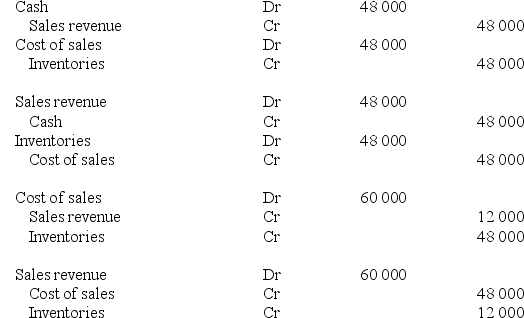

In May 2017, a parent sold inventories to a subsidiary entity for $60 000. The inventories had previously cost the parent entity $48 000. The entire inventory is still held by the subsidiary at reporting date, 30 June 2017. Ignoring tax effects, which of the following is the adjustment entry in the consolidation worksheet at reporting date?

Question

Question

Question

Question

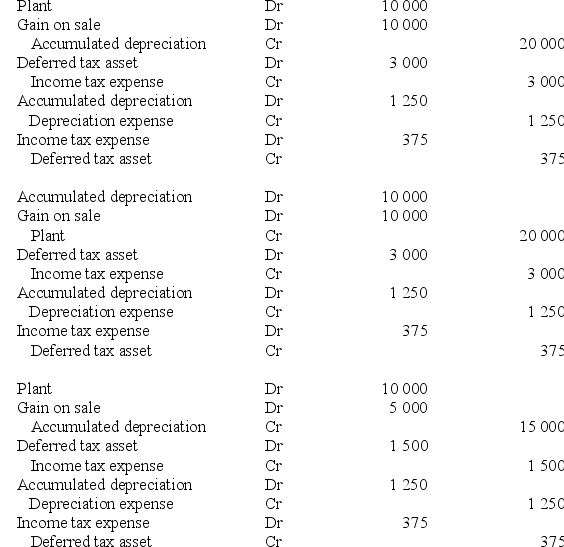

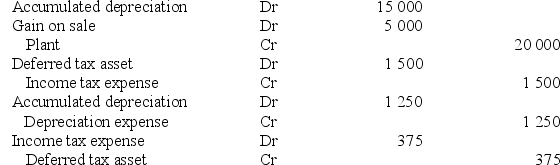

Abra Ltd sold an item of plant to its subsidiary Cadabra Ltd on 1 January 2017 for $50 000. The asset had cost Abra Ltd $60 000 when acquired on 1 January 2015. At that time the useful life of the plant was assessed at 6 years. Rounded to the nearest dollar, the consolidation elimination entries at 30 June 2017 in relation to the sale of plant are which of the following?

Question

Question

Question

Question

Question

Question

Question

Question

Question

A subsidiary sold inventories to its parent for $60 000. The inventories had previously cost the subsidiary $48 000. By reporting date, the parent had sold 75% of the inventories to a party outside the group. The company tax rate is 30%. Which of the following are the adjustment entries in the consolidation worksheet at reporting date?

Question

Question

Question

Question

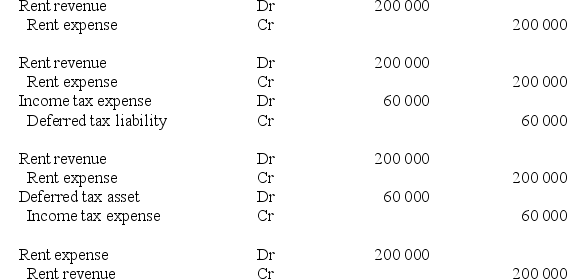

During the year ended 30 June 2017, a parent entity rents a warehouse from a subsidiary entity for $200 000. The company tax rate is 30%. Which of the following is the consolidation adjustment entry needed at reporting date to eliminate the transaction?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 11: Consolidation: Intragroup Transactions

1

Knights Ltd purchased inventories from its subsidiary, Gidley Ltd, for $20 000. The goods originally cost Gidley Ltd $12 000. The company tax rate is 30%. Assuming that all of the inventories were still on hand at the end of the year, which of the following consolidation adjustment entries is required?

A) Dr Tax expense $2400; Cr Deferred tax liability $2400

B) Dr Tax expense $2400; Cr Deferred tax asset $2400

C) Dr Deferred tax asset $2400; Cr Tax expense $2400

D) Dr Deferred tax liability $2400; Cr Tax expense $2400

A) Dr Tax expense $2400; Cr Deferred tax liability $2400

B) Dr Tax expense $2400; Cr Deferred tax asset $2400

C) Dr Deferred tax asset $2400; Cr Tax expense $2400

D) Dr Deferred tax liability $2400; Cr Tax expense $2400

C

2

Sky Limited, a subsidiary entity, sold a non-current asset at a profit to its parent entity, Dive Limited. The adjustment necessary on consolidation to reflect the tax effect of this transaction will result in a(n):

A) increase in deferred tax assets.

B) increase in deferred tax liabilities.

C) increase in income tax expense.

D) decrease in deferred tax assets.

A) increase in deferred tax assets.

B) increase in deferred tax liabilities.

C) increase in income tax expense.

D) decrease in deferred tax assets.

A

3

During the year ended 30 June 2017, a subsidiary sold inventories to its parent at a before-tax profit of $20 000. The inventories originally cost the subsidiary $87 000. At 30 June 2017 all the inventory was still on hand and it was sold to an external party in July 2017. Ignoring tax effects, the consolidation adjustment entry to eliminate this transaction during the year ended 30 June 2018 would include which of the following line items?

A) Dr Cost of sales $20 000

B) Cr Cost of sales $20 000

C) Dr Cost of sales $87 000

D) Cr Cost of sales $87 000

A) Dr Cost of sales $20 000

B) Cr Cost of sales $20 000

C) Dr Cost of sales $87 000

D) Cr Cost of sales $87 000

B

4

During the year ended 30 June 2017, a subsidiary sold inventories to a parent for $90 000. The inventories had previously cost the subsidiary entity $72 000. By 30 June 2017 the parent had sold 75% of the inventories to a party outside the group. The remaining inventories were sold externally in July 2017. The company tax rate is 30%. Which of the following is the adjustment entry in the consolidation worksheet at 30 June 2018?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Adam Ltd sold an item of plant to its subsidiary Eve Ltd on 1 January 2017 for $50 000. The asset had cost Adam Ltd $60 000 when acquired on 1 January 2015. At that time, the remaining useful life of the plant was assessed at 5 years. The adjustment necessary on consolidation to reflect the tax effect of the depreciation adjustment for the year ended 30 June 2017 will result in a decrease in:

A) deferred tax assets.

B) deferred tax liabilities.

C) income tax expense.

D) current tax liability.

A) deferred tax assets.

B) deferred tax liabilities.

C) income tax expense.

D) current tax liability.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

In May 2017, a parent sold inventories to a subsidiary entity for $60 000. The inventories had previously cost the parent entity $48 000. The entire inventory is still held by the subsidiary at reporting date, 30 June 2017. Ignoring tax effects, which of the following is the adjustment entry in the consolidation worksheet at reporting date?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Ali Ltd sold an item of plant to its subsidiary Baba Ltd on 1 January 2017 for $100 000. The asset had cost Ali Ltd $120 000 when acquired on 1 January 2015. At that time the remaining useful life of the plant was assessed at 5 years. The adjustment necessary on consolidation as at 30 June 2018 in relation to the sale of plant will result in:

A) an increase in retained earnings and a decrease in current year profit.

B) a decrease in retained earnings and an increase in current year profit.

C) an increase in retained earnings and an increase in current year profit.

D) a decrease in retained earnings and a decrease in current year profit.

A) an increase in retained earnings and a decrease in current year profit.

B) a decrease in retained earnings and an increase in current year profit.

C) an increase in retained earnings and an increase in current year profit.

D) a decrease in retained earnings and a decrease in current year profit.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

A subsidiary entity sold goods to its parent entity for $100 000. The inventories originally cost the subsidiary $125 000. At reporting date, the parent still held all of the inventories. Which of the following adjustments must be included as part of the consolidation entry to eliminate this transaction?

A) Cr Inventory $100 000

B) Cr Inventory $125 000

C) Dr Inventory $25 000

D) Dr Inventory $225 000

A) Cr Inventory $100 000

B) Cr Inventory $125 000

C) Dr Inventory $25 000

D) Dr Inventory $225 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Unrealised profit in the opening inventories of a financial period is adjusted in the consolidation worksheet by a:

A) debit to retained earnings.

B) credit to retained earnings.

C) credit to inventories.

D) debit to inventories.

A) debit to retained earnings.

B) credit to retained earnings.

C) credit to inventories.

D) debit to inventories.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Abra Ltd sold an item of plant to its subsidiary Cadabra Ltd on 1 January 2017 for $50 000. The asset had cost Abra Ltd $60 000 when acquired on 1 January 2015. At that time the useful life of the plant was assessed at 6 years. Rounded to the nearest dollar, the consolidation elimination entries at 30 June 2017 in relation to the sale of plant are which of the following?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following intragroup transactions do not affect the carrying amounts of assets and liabilities?

A) Management fees paid

B) Sale of plant at a profit

C) Sale of land for an amount greater than its carrying amount

D) Sale of inventories at a loss

A) Management fees paid

B) Sale of plant at a profit

C) Sale of land for an amount greater than its carrying amount

D) Sale of inventories at a loss

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

A parent sold some inventories to its subsidiary for $55 000. The goods had originally cost the parent $40 000. At the end of the year all of the inventories were still on hand. The consolidation adjustment entry to eliminate this transaction will include the following line items?

A) Cr Cost of sales $15 000

B) Cr Cost of sales $40 000

C) Cr Cost of sales $95 000

D) Cr Cost of sales $55 000

A) Cr Cost of sales $15 000

B) Cr Cost of sales $40 000

C) Cr Cost of sales $95 000

D) Cr Cost of sales $55 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

A subsidiary sold inventories to its parent for $40 000. The inventories originally cost the subsidiary $32 000. At balance sheet date, the parent had 20% of the inventories still on hand. The consolidation adjustment entry (excluding tax effects) will eliminate unrealised profit amounting to:

A) $6400.

B) $1600.

C) $8000.

D) $9600.

A) $6400.

B) $1600.

C) $8000.

D) $9600.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

When an entity sells a non-current asset at a profit to another entity within the same group, which of the following adjustments is necessary on consolidation?

A) Dr Asset Cr Cash

B) Dr Cash Cr Asset

C) Dr Gain on sale Cr Asset

D) Dr Asset Cr Gain on sale

A) Dr Asset Cr Cash

B) Dr Cash Cr Asset

C) Dr Gain on sale Cr Asset

D) Dr Asset Cr Gain on sale

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

A subsidiary sold inventories to its parent for $50 000. The inventories originally cost the subsidiary $38 000. At balance sheet date, the parent had sold 50% of the inventories to an external party. The company tax rate is 30%. Which of the following is the deferred tax item that is recognised on consolidation?

A) Cr Deferred tax liability $3600

B) Cr Deferred tax liability $1800

C) Dr Deferred tax asset $3600

D) Dr Deferred tax asset $1800

A) Cr Deferred tax liability $3600

B) Cr Deferred tax liability $1800

C) Dr Deferred tax asset $3600

D) Dr Deferred tax asset $1800

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

A subsidiary sold inventories to its parent in year 1 at a before-tax profit of $15 000. At balance sheet date, the parent had not sold the inventories to an external party. The company tax rate is 30%. The year 1 consolidation worksheet will contain which of the following adjustment entries for inventories?

A) Dr Inventories $15 000

B) Dr Inventories $10 500

C) Cr Inventories $15 000

D) Cr Inventories $10 500

A) Dr Inventories $15 000

B) Dr Inventories $10 500

C) Cr Inventories $15 000

D) Cr Inventories $10 500

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

A subsidiary sold a quantity of inventories to its parent entity at a before-tax profit of $12 000. The original cost of the inventories to the subsidiary was $41 000. At the end of the year all of the inventories were still on hand. The consolidation adjustment entry to eliminate this transaction will include which of the following line items?

A) Cr Inventories $12 000

B) Cr Inventories $53 000

C) Cr Inventories $41 000

D) Cr Inventories $29 000

A) Cr Inventories $12 000

B) Cr Inventories $53 000

C) Cr Inventories $41 000

D) Cr Inventories $29 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

AASB 10/IFRS 10 Consolidated Financial Statements requires that intragroup transactions be:

A) eliminated on consolidation to the extent of the parent's interest in the subsidiary.

B) eliminated in the books of the parent and subsidiary to the extent of the parent's interest in the subsidiary.

C) eliminated in full in the books of the parent and subsidiary.

D) eliminated in full on consolidation.

A) eliminated on consolidation to the extent of the parent's interest in the subsidiary.

B) eliminated in the books of the parent and subsidiary to the extent of the parent's interest in the subsidiary.

C) eliminated in full in the books of the parent and subsidiary.

D) eliminated in full on consolidation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

A subsidiary sold inventories to its parent for $60 000. The inventories had previously cost the subsidiary $48 000. By reporting date, the parent had sold 75% of the inventories to a party outside the group. The company tax rate is 30%. Which of the following are the adjustment entries in the consolidation worksheet at reporting date?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

Thurston Limited sold inventories to its parent entity, Cowboys Ltd, at a before-tax profit of $8000. The inventories originally cost Thurston Limited $32 000. At balance sheet date, Cowboys Limited had sold 90% of the inventory to an external party. The consolidation adjustment entry (excluding tax effects) will eliminate unrealised profit amounting to:

A) $800.

B) $7200.

C) $3200.

D) $24 000.

A) $800.

B) $7200.

C) $3200.

D) $24 000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

The effect of an intragroup sale of inventories at a profit, where the inventories have been sold to external parties prior to the end of the reporting period, is that both profit and the inventories asset are overstated.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

The effect of an intragroup sale of inventories in a prior period, where the inventories are still on hand at the end of that prior period, is that a debit consolidation adjustment is made to opening retained earnings.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

During the year ended 30 June 2017, a parent entity rents a warehouse from a subsidiary entity for $200 000. The company tax rate is 30%. Which of the following is the consolidation adjustment entry needed at reporting date to eliminate the transaction?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

A parent entity sold a depreciable non-current asset to a subsidiary entity for $5600. The asset originally cost $6000 and at the date of sale accumulated depreciation was $1000. The amount of the unrealised gain on sale to be eliminated is:

A) $5600.

B) $1000.

C) $600.

D) $400.

A) $5600.

B) $1000.

C) $600.

D) $400.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

The effect of an intragroup sale of inventories in a prior period, where the inventory is still on hand at the end of the prior period but is sold in the current period, is that a credit adjustment is made to income tax expense in the subsequent period.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

When an entity sells a non-current asset at a profit to another entity within the same group, which of the following adjustments is necessary on consolidation?

A) Dr Gain on sale, CR Asset

B) Dr Asset, CR Cash

C) Dr Gain on sale, CR Cash

D) Dr Asset, DR Gain on sale

A) Dr Gain on sale, CR Asset

B) Dr Asset, CR Cash

C) Dr Gain on sale, CR Cash

D) Dr Asset, DR Gain on sale

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

When a depreciable non-current asset is sold between entities within a group, any gain recognised on the sale is eliminated and realised through consolidation adjustments which result in increased depreciation expenses in future periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

The effect of an intragroup sale of inventories in a prior period, where the inventories are still on hand at the end of the current period, is that a credit adjustment is made to inventory in the current period.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

Where there is an intragroup sale of inventories and the inventories have been sold to external parties prior to the end of the reporting period, no adjustment is required on consolidation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

If an interim dividend is paid by a subsidiary to its parent, the consolidation entry to eliminate the transaction is which of the following?

A) Dr Interim dividend paid; Cr Dividend revenue

B) Dr Dividend revenue; Cr Interim dividend paid

C) Dr Dividend revenue; Cr Dividend payable

D) Dr Interim dividend paid; Cr Cash

A) Dr Interim dividend paid; Cr Dividend revenue

B) Dr Dividend revenue; Cr Interim dividend paid

C) Dr Dividend revenue; Cr Dividend payable

D) Dr Interim dividend paid; Cr Cash

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

When a non-depreciable non-current asset such as land is sold between entities within a group, the adjustment in relation to any gain or loss recognised on the transfer is carried forward until the asset is disposed of to an external party.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

On 16 May 2017, Zebra Ltd sold equipment to its subsidiary Nando Ltd for $100 000, this asset having a carrying amount at time of sale of $80 000. The equipment was regarded by Zebra Ltd as a depreciable non-current asset, being depreciated at 10% p.a. on cost, whereas Nando Ltd records the machinery as inventory. The asset was sold by Nando Ltd before 30 June 2017. The worksheet entry for the year ended 30 June 2017 would include which of the following adjustments?

A) Dr Cost of sales 20 000

B) Cr Cost of sales 20 000

C) Dr Inventory 20 000

D) Cr Inventory 20 000

A) Dr Cost of sales 20 000

B) Cr Cost of sales 20 000

C) Dr Inventory 20 000

D) Cr Inventory 20 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

When a depreciable non-current asset is sold between entities within a group, any gain recognised on the sale is eliminated and realised through future use of the asset by the group.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

The effect of an intragroup sale of inventories at a profit where the inventories are still on hand at the end of the reporting period is that both profit and the inventory asset are overstated.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

Unite Ltd provided a loan of $1 000 000 to its subsidiary Inspire Ltd. Interest of $100 000 was charged during the year ended 30 June 2018. On consolidation, which of the following adjustments is needed at 30 June 2018 in relation to the interest charged?

A) No adjustment needed

B) Dr Interest revenue $100 000 Cr Interest expense $100 000

C) Dr Interest expense $100 000 Cr Interest revenue $100 000

D) Dr Retained earnings $100 000 Cr Cash $100 000

A) No adjustment needed

B) Dr Interest revenue $100 000 Cr Interest expense $100 000

C) Dr Interest expense $100 000 Cr Interest revenue $100 000

D) Dr Retained earnings $100 000 Cr Cash $100 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

Chancellor Limited provided a loan of $1 500 000 to its subsidiary Park Limited. On consolidation, which of the following adjustments is needed in relation to this intragroup loan?

A) No adjustment needed

B) Dr Loan receivable from subsidiaries $1 500 000 Cr Loan payable to parent $1 500 000

C) Dr Loan payable from parent $1 500 000 Cr Loan receivable from subsidiaries $1 500 000

D) Dr Loan payable to parent $1 500 000 Cr Cash $1 500 000

A) No adjustment needed

B) Dr Loan receivable from subsidiaries $1 500 000 Cr Loan payable to parent $1 500 000

C) Dr Loan payable from parent $1 500 000 Cr Loan receivable from subsidiaries $1 500 000

D) Dr Loan payable to parent $1 500 000 Cr Cash $1 500 000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

The elimination of the full effects of intragroup transactions is required in the preparation of consolidated financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following items is an example of an intragroup service?

A) A subsidiary sells inventory to its parent entity.

B) An intragroup transfer of non-current assets results in an unrealised profit.

C) One entity in a group acquires a depreciable asset from another entity in the same group.

D) One entity in a group rents a building to another entity in the group.

A) A subsidiary sells inventory to its parent entity.

B) An intragroup transfer of non-current assets results in an unrealised profit.

C) One entity in a group acquires a depreciable asset from another entity in the same group.

D) One entity in a group rents a building to another entity in the group.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

If an entity sells a non-current asset at a profit to another entity within the same group, which of the following consolidation adjustments is necessary to reflect the tax effect?

A) Dr Deferred tax asset

B) Dr Deferred tax liability

C) Dr Tax expense

D) Cr Deferred tax asset

A) Dr Deferred tax asset

B) Dr Deferred tax liability

C) Dr Tax expense

D) Cr Deferred tax asset

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

A consolidation worksheet adjustment to eliminate the effect of interest revenue and interest expense relating to intragroup loans has which of the following tax effects?

A) No tax effect

B) Increase in current tax liability

C) Increase in deferred tax liability

D) Decrease in deferred tax asset

A) No tax effect

B) Increase in current tax liability

C) Increase in deferred tax liability

D) Decrease in deferred tax asset

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

When a depreciable non-current asset is sold between entities within a group, any gain recognised on the sale is eliminated and realised through the future use of the asset by the group. This results in reduced depreciation and income tax expenses in future periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

When an interest bearing loan is advanced by a parent to a subsidiary, there is no tax effect consolidation entry required as assets and liabilities are reduced equally.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Where an intragroup sale of an asset has been made and the asset was classified as inventories in the selling entity's books, but subsequently classified as plant in the buying entity's books, all depreciation recognised in the buying entity's books must be eliminated on consolidation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

When a dividend is declared, but unpaid at the end of a financial year, credit consolidation adjustments are required against both the dividend declared and dividend receivable account.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Pre-acquisition dividends are accounted for in the parent's books as a reduction in the investment in the subsidiary.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

When an interest bearing loan is advanced by a parent to a subsidiary, a credit is required on consolidation against the loan payable and interest revenue accounts.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Elimination consolidation entries relating to intragroup services do not need to be carried forward to future periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Where an intragroup sale of an asset at a profit has been made and the asset was classified as plant in the selling entity's books, but subsequently classified as inventories in the buying entity's books, a credit adjustment is required against cost of sales in the year of sale.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Tax effect consolidation entries are not required when intragroup services are provided to entities within a group.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Where a dividend is declared in a prior period and paid in a current period, the credit in the consolidation elimination entry is made against the dividend declared/paid account.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.