Deck 2: Financing Company Operations

Full screen (f)

Question

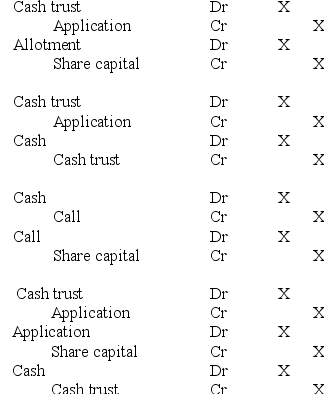

When shares are issued fully payable on application, the journal entries to record the issue (assuming the minimum subscription is reached) are

Question

Question

Question

Question

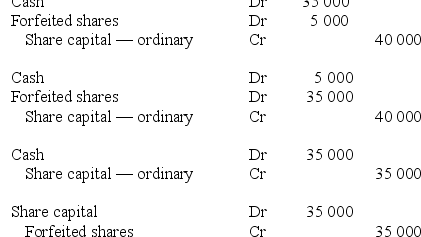

A company's share capital consists of 100 000 ordinary shares issued at $4 and paid to $2 per share. On 1 February, a first call of $1 was made on the ordinary shares. By 28 February, call money was received on 90 000 shares. On 31 March, the shares on which calls were outstanding were forfeited. The company's constitution provided for any surplus on resale to be returned to the shareholders whose shares were forfeited. On 15 April, the forfeited shares were reissued as paid to $4.00 for a payment of $3.50 per share. The entry to record the reissue of the forfeited shares is:

Question

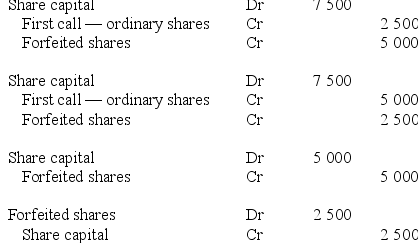

A company's share capital consists of 50 000 ordinary shares issued at $2 and paid to $1 per share. On 1 September, a first call of 50c was made on the ordinary shares. By 30 September, call money was received on 45 000 shares. On 31 October, the shares on which calls were outstanding were forfeited. The company's constitution provided for any surplus on resale to be returned to the shareholders whose shares were forfeited. The entry to record the forfeiture of shares is:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

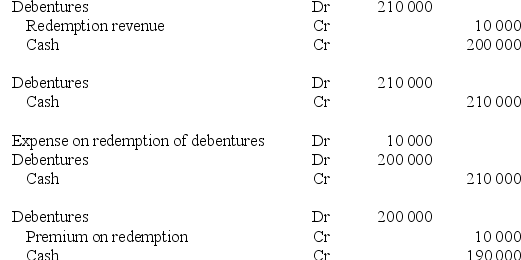

On 1 July 2017, a company redeemed its $200 000 debenture liability using its available cash on hand. The terms of the debenture issue provided that a premium of 5% was to be paid on redemption of the debentures. Which of the following is the entry to record the redemption?

Question

Question

Bellvista Limited issued 20 000 share options to subscribe for ordinary shares. The exercise price on the options was $5 per share. If all options were exercised by the due date, the following journal entry would be recorded for the issue of the shares.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/62

Play

Full screen (f)

Deck 2: Financing Company Operations

1

When shares are issued fully payable on application, the journal entries to record the issue (assuming the minimum subscription is reached) are

D

2

ABC Ltd was registered as a company on 1 July 2017. On 4 July 2017, ABC Ltd issued a prospectus offering 250 000 ordinary shares at an issue price of $3.50 each, payable $2.50 on application and $1.00 on allotment. Applications closed on 1 August 2017 with the company having received applications for 300 000 shares. The shares were allotted on 15 August 2017, with the over-subscription amount being refunded to unsuccessful applicants. All allotment money was received by 31 August 2017. Following the allotment, the balance in the share capital account would be:

A) $750 000 credit.

B) $875 000 credit.

C) $625 000 credit.

D) $1 050 000 credit.

A) $750 000 credit.

B) $875 000 credit.

C) $625 000 credit.

D) $1 050 000 credit.

B

3

The appropriate account to record any excess application money received and retained by a company to reduce allotment money due and in payment of future calls, is the:

A) calls in arrears account.

B) forfeited shares account.

C) share capital account.

D) calls in advance account.

A) calls in arrears account.

B) forfeited shares account.

C) share capital account.

D) calls in advance account.

D

4

In respect to the issue of shares by companies, which of the following statements is incorrect?

A) Companies can convert ordinary shares into preference shares.

B) Companies can only issue ordinary shares.

C) Companies can issue any specified number of shares at any price.

D) Companies can issue both ordinary and preference shares.

A) Companies can convert ordinary shares into preference shares.

B) Companies can only issue ordinary shares.

C) Companies can issue any specified number of shares at any price.

D) Companies can issue both ordinary and preference shares.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

5

A company's share capital consists of 100 000 ordinary shares issued at $4 and paid to $2 per share. On 1 February, a first call of $1 was made on the ordinary shares. By 28 February, call money was received on 90 000 shares. On 31 March, the shares on which calls were outstanding were forfeited. The company's constitution provided for any surplus on resale to be returned to the shareholders whose shares were forfeited. On 15 April, the forfeited shares were reissued as paid to $4.00 for a payment of $3.50 per share. The entry to record the reissue of the forfeited shares is:

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

6

A company's share capital consists of 50 000 ordinary shares issued at $2 and paid to $1 per share. On 1 September, a first call of 50c was made on the ordinary shares. By 30 September, call money was received on 45 000 shares. On 31 October, the shares on which calls were outstanding were forfeited. The company's constitution provided for any surplus on resale to be returned to the shareholders whose shares were forfeited. The entry to record the forfeiture of shares is:

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

7

According to the Corporations Act, when a company issues shares to the public, the issue price, terms and rights of the shares are determined by:

A) the Australian Securities Exchange.

B) the company's directors.

C) the Australian Investments and Securities Commission.

D) the company's auditors.

A) the Australian Securities Exchange.

B) the company's directors.

C) the Australian Investments and Securities Commission.

D) the company's auditors.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

8

ABC Limited issued a prospectus offering 100 000 ordinary shares at an issue price of $2.50 each, payable $1.50 per share on application. The company received applications for 110 000 shares. Which of the following entries correctly records the application money?

A) DR Application $165 000 CR Cash trust $165 000

B) DR Cash trust $250 000 CR Application $250 000

C) DR Cash trust $165 000 CR Application $165 000

D) DR Cash trust $275 000 CR Application $275 000

A) DR Application $165 000 CR Cash trust $165 000

B) DR Cash trust $250 000 CR Application $250 000

C) DR Cash trust $165 000 CR Application $165 000

D) DR Cash trust $275 000 CR Application $275 000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

9

The journal entry to record further receipts of cash due on the allotment of shares will include which of the following line items?

A) DR Allotment

B) DR Share capital

C) CR Allotment

D) CR Cash

A) DR Allotment

B) DR Share capital

C) CR Allotment

D) CR Cash

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

10

When a company requests a further payment from shareholders of the unpaid amounts on their shares, it:

A) makes a call on the shares.

B) makes a further allotment of those shares.

C) converts the shares into debentures.

D) forfeits the shares.

A) makes a call on the shares.

B) makes a further allotment of those shares.

C) converts the shares into debentures.

D) forfeits the shares.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

11

A company forfeited 10 000 shares that had been paid to $2 but on which a $1 call was outstanding. The company's constitution provided for any surplus on reissue to be returned to the forfeiting shareholders. The forfeited shares were reissued as paid to $4.00 for a payment of $3.50 per share. Costs of reissue amounted to $2000. The amount of the surplus repaid to the shareholders whose shares were forfeited is:

A) $15 000.

B) $13 000.

C) $10 000.

D) $38 000.

A) $15 000.

B) $13 000.

C) $10 000.

D) $38 000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

12

Before a company issues shares to the public, the company must:

A) register the prospectus with the Australian Accounting Standards Board.

B) first offer the shares to the existing shareholders.

C) register the prospectus with the Australian Securities Exchange.

D) provide a disclosure document with an application form attached.

A) register the prospectus with the Australian Accounting Standards Board.

B) first offer the shares to the existing shareholders.

C) register the prospectus with the Australian Securities Exchange.

D) provide a disclosure document with an application form attached.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is the appropriate journal entry to record the cash collected from applicants for shares before the shares are actually issued?

A) Increase cash trust account: increase share capital account

B) Increase application account: decrease share capital account

C) Increase share capital account: decrease cash trust account

D) Increase cash trust account: increase application account

A) Increase cash trust account: increase share capital account

B) Increase application account: decrease share capital account

C) Increase share capital account: decrease cash trust account

D) Increase cash trust account: increase application account

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

14

The journal entry to record the amount receivable when a call is made by the company is:

A) DR Call CR Share capital

B) DR Allotment CR Share capital

C) DR Share capital CR Call

D) DR Cash trust CR Call

A) DR Call CR Share capital

B) DR Allotment CR Share capital

C) DR Share capital CR Call

D) DR Cash trust CR Call

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

15

XYZ Ltd was registered as a company on 1 July 2017. On 4 July 2017, ABC Ltd issued a prospectus offering 200 000 ordinary shares at an issue price of $5.00 each, payable $3.00 on application and $2.00 on allotment. Applications closed on 1 August 2017 with the company having received applications for 220 000 shares. After application but prior to allotment, the balance in the application account would be:

A) $600 000 credit.

B) $1 000 000 credit.

C) $660 000 debit.

D) $660 000 credit.

A) $600 000 credit.

B) $1 000 000 credit.

C) $660 000 debit.

D) $660 000 credit.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

16

Smith Ltd was registered as a company on 1 July 2017. On 4 July 2017, Smith Ltd issued a prospectus offering 300 000 ordinary shares at an issue price of $4.00 each, payable $2.00 on application and $2.00 on allotment. Applications closed on 1 August 2017 with the company having received applications for 330 000 shares. The shares were allotted on 15 August 2017, with the over-subscription amount being refunded to unsuccessful applicants. All allotment money was received by 31 August 2017. Following the allotment, the amount transferred from the cash trust account to the cash account would be:

A) $600 000.

B) $1 320 000.

C) $1 200 000.

D) $660 000.

A) $600 000.

B) $1 320 000.

C) $1 200 000.

D) $660 000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

17

After the completion of all steps in the issue of shares, the company's statement of financial position will show which of the following changes?

A) Assets increased, liabilities increased

B) Assets decreased, equity increased

C) Assets decreased, liabilities decreased

D) Assets increased; equity increased

A) Assets increased, liabilities increased

B) Assets decreased, equity increased

C) Assets decreased, liabilities decreased

D) Assets increased; equity increased

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

18

Interest paid to shareholders on calls in advance is:

A) credited to retained earnings.

B) recorded as an expense.

C) debited to retained earnings.

D) recorded as revenue.

A) credited to retained earnings.

B) recorded as an expense.

C) debited to retained earnings.

D) recorded as revenue.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

19

If the minimum number of applications specified in the disclosure document is not received, all application money must be refunded to applicants. The minimum number of applications must be received within:

A) 4 months after the date of the disclosure document.

B) 1 month after the receipt of the first application money by the company.

C) 13 months after the date of the disclosure document.

D) 75 days from the date that ASIC gives its approval of the disclosure document.

A) 4 months after the date of the disclosure document.

B) 1 month after the receipt of the first application money by the company.

C) 13 months after the date of the disclosure document.

D) 75 days from the date that ASIC gives its approval of the disclosure document.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

20

If a company's constitution does not contain rules governing the forfeiture of shares, then the company:

A) may forfeit shares but not reissue them.

B) cannot forfeit shares.

C) may forfeit shares and reissue them at a later date.

D) can register the shares in the name of another shareholder, but cannot receive payment from that shareholder.

A) may forfeit shares but not reissue them.

B) cannot forfeit shares.

C) may forfeit shares and reissue them at a later date.

D) can register the shares in the name of another shareholder, but cannot receive payment from that shareholder.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

21

Dividends declared after the reporting period:

A) meet the criteria for recognition as a liability.

B) satisfy the criteria for recognition as an expense.

C) are recognised in the statement of financial position as they meet the definition of equity.

D) do not meet the AASB 132/IAS 32 recognition criteria for liabilities.

A) meet the criteria for recognition as a liability.

B) satisfy the criteria for recognition as an expense.

C) are recognised in the statement of financial position as they meet the definition of equity.

D) do not meet the AASB 132/IAS 32 recognition criteria for liabilities.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

22

In relation to a revaluation surplus, an entity:

A) cannot use this surplus for the payment of future dividends.

B) can transfer this surplus to retained earnings when the asset is derecognised or used.

C) cannot transfer this surplus to any other reserve account.

D) can transfer the surplus to the current period profit or loss when the asset is disposed of.

A) cannot use this surplus for the payment of future dividends.

B) can transfer this surplus to retained earnings when the asset is derecognised or used.

C) cannot transfer this surplus to any other reserve account.

D) can transfer the surplus to the current period profit or loss when the asset is disposed of.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

23

The costs of issuing shares effectively:

A) reduce the proceeds from the share issue.

B) increase the proceeds from the share issue.

C) are borne by the underwriters of the share issue.

D) are recognised as a deferred asset on the statement of financial position.

A) reduce the proceeds from the share issue.

B) increase the proceeds from the share issue.

C) are borne by the underwriters of the share issue.

D) are recognised as a deferred asset on the statement of financial position.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

24

When making a transfer from a general reserve to retained earnings, which of the following journals could be used?

A) DR General reserve CR Retained earnings

B) DR Retained earnings CR General reserve

C) DR Share capital CR General reserve

D) DR General reserve CR Share capital

A) DR General reserve CR Retained earnings

B) DR Retained earnings CR General reserve

C) DR Share capital CR General reserve

D) DR General reserve CR Share capital

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

25

Brown Limited was incorporated on 1 July 2017. A prospectus offering 200 000 shares at $3.00 each was released and closed fully subscribed. The share issue was underwritten by a broker for $25 000 and other costs of the share issue amounted to $13 000. The net share capital on the statement of financial position is:

A) $575 000.

B) $162 000.

C) $587 000.

D) $562 000.

A) $575 000.

B) $162 000.

C) $587 000.

D) $562 000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

26

On 1 July 2017, a company redeemed its $200 000 debenture liability using its available cash on hand. The terms of the debenture issue provided that a premium of 5% was to be paid on redemption of the debentures. Which of the following is the entry to record the redemption?

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

27

Reserves that are not required by accounting standards are known as:

A) specific reserves.

B) general reserves.

C) current reserves.

D) retained reserves.

A) specific reserves.

B) general reserves.

C) current reserves.

D) retained reserves.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

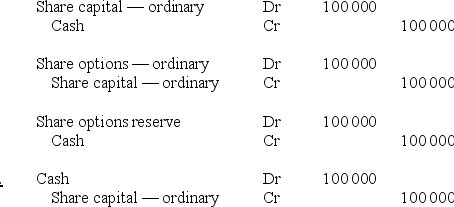

28

Bellvista Limited issued 20 000 share options to subscribe for ordinary shares. The exercise price on the options was $5 per share. If all options were exercised by the due date, the following journal entry would be recorded for the issue of the shares.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

29

A bonus issue of shares to existing shareholders has which of the following impacts on the equity of a company?

A) Total equity increases.

B) Total equity decreases.

C) No overall change in total equity.

D) Only the amount of issued share capital changes.

A) Total equity increases.

B) Total equity decreases.

C) No overall change in total equity.

D) Only the amount of issued share capital changes.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

30

According to ASX Listing Rule 7.1, the proportion of existing capital that a listed company can issue in any one year without the prior approval of the ordinary shareholders is:

A) 5%.

B) 10%.

C) 15%.

D) 20%.

A) 5%.

B) 10%.

C) 15%.

D) 20%.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

31

If the balance in a forfeited shares account is refundable to the owners of those shares, then the account is classified as a component of:

A) revenue.

B) liabilities.

C) equity.

D) expense.

A) revenue.

B) liabilities.

C) equity.

D) expense.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

32

According to the Corporations Act, dividends may:

A) only be paid to shareholders once a year.

B) only be paid out of the current year's profits of a company.

C) be declared and paid to shareholders irrespective of whether a company has accumulated losses.

D) be paid if the company has an excess of assets over liabilities.

A) only be paid to shareholders once a year.

B) only be paid out of the current year's profits of a company.

C) be declared and paid to shareholders irrespective of whether a company has accumulated losses.

D) be paid if the company has an excess of assets over liabilities.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following journal entries shows the correct accounting treatment for share issue costs?

A) Dr Deferred asset: Cr Cash

B) Dr Cash: Cr Deferred asset

C) Dr Share capital: Cr: Cash

D) Dr Cash: Cr Share capital

A) Dr Deferred asset: Cr Cash

B) Dr Cash: Cr Deferred asset

C) Dr Share capital: Cr: Cash

D) Dr Cash: Cr Share capital

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

34

It is possible for a company to issue different types of preference shares provided that the rights of each type are specified in its constitution.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

35

A share option is an instrument that gives the holder the right but not the obligation to:

A) buy a certain number of shares in the company by a specified date at a stipulated price.

B) sell a variable number of shares in the company by a specified date at a stipulated price.

C) receive a certain dividend declared by the company by a specified date.

D) receive a bonus issue of shares in a proportion as notified by the company.

A) buy a certain number of shares in the company by a specified date at a stipulated price.

B) sell a variable number of shares in the company by a specified date at a stipulated price.

C) receive a certain dividend declared by the company by a specified date.

D) receive a bonus issue of shares in a proportion as notified by the company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

36

For a company, retained earnings represent:

A) contributed capital from shareholders.

B) profits retained by the company before tax is paid to the government.

C) net cash retained by the company before any payment of dividends to shareholders.

D) profits retained by the company after payment of dividends, and after any transfer to and from reserves.

A) contributed capital from shareholders.

B) profits retained by the company before tax is paid to the government.

C) net cash retained by the company before any payment of dividends to shareholders.

D) profits retained by the company after payment of dividends, and after any transfer to and from reserves.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

37

The appropriate accounting entry to record the declaration of a bonus share issue out of the Revaluation Surplus account is which of the following?

A) DR Bonus dividend CR Revaluation surplus

B) DR Revaluation surplus CR Cash

C) DR Revaluation surplus CR Share capital

D) DR Cash CR Share capital

A) DR Bonus dividend CR Revaluation surplus

B) DR Revaluation surplus CR Cash

C) DR Revaluation surplus CR Share capital

D) DR Cash CR Share capital

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is correct in relation to the payment of dividends?

A) Dividends can only be paid if a company has generated a profit in the current period.

B) The payment of dividends is regulated by the Corporations Act.

C) A company can only pay an interim dividend if its constitution allows it.

D) Preference dividends must be paid on a cumulative basis.

A) Dividends can only be paid if a company has generated a profit in the current period.

B) The payment of dividends is regulated by the Corporations Act.

C) A company can only pay an interim dividend if its constitution allows it.

D) Preference dividends must be paid on a cumulative basis.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following statements is not correct in relation to cumulative preference shares?

A) Holders of cumulative preference shares are guaranteed a dividend every year.

B) Undeclared cumulative preference share dividends accumulate, or carry forward, to future periods.

C) The accumulated amount of any cumulative preference share dividend plus the current year's preference dividend must be paid before any dividend can be paid to ordinary shareholders.

D) Cumulative preference share dividends that are not declared in the year they are due are called dividends in arrears.

A) Holders of cumulative preference shares are guaranteed a dividend every year.

B) Undeclared cumulative preference share dividends accumulate, or carry forward, to future periods.

C) The accumulated amount of any cumulative preference share dividend plus the current year's preference dividend must be paid before any dividend can be paid to ordinary shareholders.

D) Cumulative preference share dividends that are not declared in the year they are due are called dividends in arrears.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

40

Underwriting and other share issue costs paid to a stockbroker or financial institution should be reported in the statement of financial position as a/an:

A) liability.

B) asset.

C) increase in share capital.

D) decrease in share capital.

A) liability.

B) asset.

C) increase in share capital.

D) decrease in share capital.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

41

Only fully paid-up preference shares can be redeemed by a company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

42

Prior to the allotment/issue of shares, the balance in the application account represents a liability of the company to the applicants.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

43

Underwriting commission fees are treated as expenses as they are not considered to be an integral part of the equity issue transaction.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

44

If a company makes a renounceable rights issue, the shareholders are not allowed to sell their rights, but must either accept or reject the offer to purchase additional shares in the company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

45

Share splits and share consolidations are only allowed if a company's constitution contains specific provisions relating to such transactions.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

46

If a company uses its surplus cash reserves to buy-back its own shares, the total equity of the company will increase by the equivalent amount of cash spent.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

47

In accordance with AASB 138/IAS 38 Intangible Assets, company formation costs such as professional legal and accounting advice qualifies for recognition as an asset.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

48

Many investors may wish to purchase debentures or notes offering the ability to be converted into fully paid shares at the maturity date, in lieu of a cash payment.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

49

A rights issue gives all existing shareholders the right to an additional number of shares in proportion to their current shareholding.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

50

Where share options are issued and subsequently lapse, the cost of the lapsed options is transferred to a Lapsed Options Reserve account.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

51

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

52

If a company forfeits shares and the company's constitution is silent in relation to reissue of the shares, the company is entitled to keep any balance in the account after reissue, payment of unpaid calls and interest and administrative costs.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

53

Share options issued at no cost to the recipient are accounted for in the same way as a rights issue.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

54

According to the Corporations Act, dividends can only be paid out of the profits earned by a company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

55

Share issue costs such as professional adviser's fees and brokerage fees must be reported as an expense in the income statement.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

56

Redeemable preference shares are always considered to be compound financial instruments that contain both equity and liability components.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

57

If a company has not reached a minimum subscription level within 90 days of the date of the disclosure document, the money paid in by applicants must be refunded by the company within 1 month in accordance with the requirements of ss 724(1) and (2) of the Corporations Act.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

58

In the case of a share issue being oversubscribed, any amount kept by the company for future calls is credited to a Calls in Advance account, which is reported in the equity section of the statement of financial position.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

59

Debentures may be issued at a nominal value, a premium or a discount.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

60

Any unpaid calls are accounted for as a receivable in a company's financial statements.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

61

The Reserves accounts of a company are disclosed in the statement of financial position as liabilities.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

62

The statement of changes in equity shows the movement between the beginning and ending balance for the period for each equity account.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 62 flashcards in this deck.