Deck 10: Leases

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

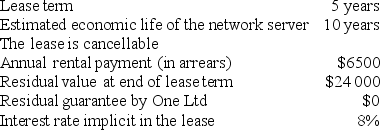

On 1 July 2021, One Ltd leased a network server from Short Ltd. The server had cost Short Ltd $32 000 on the same day. The lease agreement cost Short Ltd $1390 to set up and included the following:  The journal entry recorded by the lessor to recognise the initial direct costs incurred would be:

The journal entry recorded by the lessor to recognise the initial direct costs incurred would be:

A) DR Lease expense $1390 CR Cash $1390

B) DR Deferred initial direct costs - equipment $1390 CR Cash $1390

C) DR Lease expense $1390 CR Deferred initial direct costs - equipment $1390

D) DR Cash $1390 CR Deferred initial direct costs - equipment $1390

The journal entry recorded by the lessor to recognise the initial direct costs incurred would be:A) DR Lease expense $1390 CR Cash $1390

B) DR Deferred initial direct costs - equipment $1390 CR Cash $1390

C) DR Lease expense $1390 CR Deferred initial direct costs - equipment $1390

D) DR Cash $1390 CR Deferred initial direct costs - equipment $1390

Question

Question

Question

Question

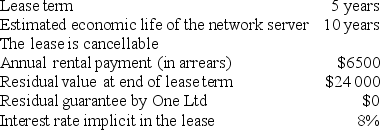

On 1 July 2021, One Ltd leased a network server from Short Ltd. The server had cost Short Ltd $32 000 on the same day. The lease agreement cost Short Ltd $1390 to set up and included the following:  The journal entry recorded by the lessor for the annual recognition of the initial direct costs would be:

The journal entry recorded by the lessor for the annual recognition of the initial direct costs would be:

A) DR Deferred initial direct costs - equipment $278 CR Lease expense $278

B) DR Lease expense $278 CR Cash $278

C) DR Cash $278 CR Deferred initial direct costs - equipment $278

D) DR Lease expense $278 CR Deferred initial direct costs - equipment $278

The journal entry recorded by the lessor for the annual recognition of the initial direct costs would be:A) DR Deferred initial direct costs - equipment $278 CR Lease expense $278

B) DR Lease expense $278 CR Cash $278

C) DR Cash $278 CR Deferred initial direct costs - equipment $278

D) DR Lease expense $278 CR Deferred initial direct costs - equipment $278

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/25

Play

Full screen (f)

Deck 10: Leases

1

The new accounting standard for leases, AASB 16/IFRS 16, has introduced:

A) a single lessee accounting model for all leases with a term of more than 12 months.

B) a multi lessee accounting model for all leases with a term of more than 12 months.

C) a single lessee accounting model for all leases with a term of less than 12 months.

D) a multi lessee accounting model for all leases with a term of less than 12 months.

A) a single lessee accounting model for all leases with a term of more than 12 months.

B) a multi lessee accounting model for all leases with a term of more than 12 months.

C) a single lessee accounting model for all leases with a term of less than 12 months.

D) a multi lessee accounting model for all leases with a term of less than 12 months.

A

2

On 30 June 2021, Monty Ltd leased a motor vehicle to Taylor Ltd. Monty Ltd had purchased the motor vehicle on that day for its fair value of $68 346. The lease agreement cost Monty $1659 to have drawn up and requires Taylor to reimburse Monty for annual insurance costs of $1500. The amount recorded as a lease receivable by Monty Ltd at the inception of the lease is:

A) $66 846.

B) $69 849.

C) $70 005.

D) $71 505.

A) $66 846.

B) $69 849.

C) $70 005.

D) $71 505.

C

3

Barry Limited and Allen Limited enter into a finance lease agreement with the following terms:

-lease term is 4 years

-estimated economic life of the leased asset is 5 years

-4 × annual rental payments of $15 000 each payable in advance

-residual value at the end of the lease term is not guaranteed by the lessee

-interest rate implicit in the lease is 8%.

On inception date, the present value of the lease payments is:

A) $53 656.

B) $38 656.

C) $49 682.

D) $60 000.

-lease term is 4 years

-estimated economic life of the leased asset is 5 years

-4 × annual rental payments of $15 000 each payable in advance

-residual value at the end of the lease term is not guaranteed by the lessee

-interest rate implicit in the lease is 8%.

On inception date, the present value of the lease payments is:

A) $53 656.

B) $38 656.

C) $49 682.

D) $60 000.

$53 656.

4

Which of the following is included within the scope of AASB 16/IFRS 16?

A) Lease agreements for motion picture films.

B) Lease agreements to explore for minerals.

C) Lease agreement for an oil refinery.

D) Lease agreements for biological assets.

A) Lease agreements for motion picture films.

B) Lease agreements to explore for minerals.

C) Lease agreement for an oil refinery.

D) Lease agreements for biological assets.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is not an example of a risk of ownership of an asset?

A) Gains on the future sale of the asset.

B) Changing economic conditions.

C) Idle capacity.

D) Technical obsolescence.

A) Gains on the future sale of the asset.

B) Changing economic conditions.

C) Idle capacity.

D) Technical obsolescence.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is an appropriate journal entry for the initial recognition by a financier lessor of a finance lease arrangement?

A) DR Leased asset: CR Cash

B) DR Lease receivable: CR Asset

C) DR Lease receivable: CR Lease liability

D) DR Leased asset: CR Cash/accounts payable

A) DR Leased asset: CR Cash

B) DR Lease receivable: CR Asset

C) DR Lease receivable: CR Lease liability

D) DR Leased asset: CR Cash/accounts payable

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

7

When negotiating operating leases, any initial direct costs incurred by lessors are to be:

A) recognised as an expense over the lease term.

B) initially capitalised into a separate deferred costs account.

C) added to the carrying amount of the underlying asset.

D) all of the above.

A) recognised as an expense over the lease term.

B) initially capitalised into a separate deferred costs account.

C) added to the carrying amount of the underlying asset.

D) all of the above.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

8

The rewards of ownership of an asset include the possibilities of gains related to:

I. Realisation of a residual value.

II. Benefits obtained from profitable operation over the underlying asset's economic life.

III. Appreciation in the asset's value.

A) I only.

B) I and II only.

C) I, II and III.

D) III only.

I. Realisation of a residual value.

II. Benefits obtained from profitable operation over the underlying asset's economic life.

III. Appreciation in the asset's value.

A) I only.

B) I and II only.

C) I, II and III.

D) III only.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

9

At the inception date of the lease, the fair value of the asset measures:

A) the present value of the total benefits remaining with the lessor.

B) the present value of the total benefits associated with the asset.

C) the total of the lease payments over the term of the lease.

D) none of these options.

A) the present value of the total benefits remaining with the lessor.

B) the present value of the total benefits associated with the asset.

C) the total of the lease payments over the term of the lease.

D) none of these options.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

10

At the commencement of the lease agreement the lessor recognises the balance of the lease receivable as the:

A) the nominal value of the lease payments receivable from the lessee.

B) the present value of the lease payments receivable from the lessee.

C) the present value of the residual value of the asset.

D) the present value of the lease payments receivable from the lessee and the present value of the unguaranteed residual value.

A) the nominal value of the lease payments receivable from the lessee.

B) the present value of the lease payments receivable from the lessee.

C) the present value of the residual value of the asset.

D) the present value of the lease payments receivable from the lessee and the present value of the unguaranteed residual value.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is an appropriate journal entry for the initial recognition by a manufacturer/dealer lessor?

A) DR Leased asset: CR Cash

B) DR Cash: CR Sales revenue

C) DR Lease liability: CR Leased asset

D) DR Leased receivable: CR Sales revenue

A) DR Leased asset: CR Cash

B) DR Cash: CR Sales revenue

C) DR Lease liability: CR Leased asset

D) DR Leased receivable: CR Sales revenue

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

12

According to AASB 16/IFRS 16 Leases, because lease payments are received from the lessee over the lease term, the receipts need to be divided into the following components:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

13

A finance lease is defined in AASB 16/IFRS 16 as:

A) a lease that is not classified as an operating lease.

B) a lease that does not transfer substantially all the risks and rewards incidental to ownership of an underlying asset.

C) a rental agreement of less than 12 months' duration.

D) a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset.

A) a lease that is not classified as an operating lease.

B) a lease that does not transfer substantially all the risks and rewards incidental to ownership of an underlying asset.

C) a rental agreement of less than 12 months' duration.

D) a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

14

AASB 16/IFRS 16 defines a lease as:

A) a contract, or part of a contract, that conveys the right to transfer ownership of an asset (the underlying asset) for a period of time in exchange for consideration.

B) a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.

C) a contract that conveys the right for the lessor to obtain substantially all of the economic benefits of the identified asset.

D) a contract, or part of a contract, that conveys the right to transfer a liability for a period of time in exchange for an asset.

A) a contract, or part of a contract, that conveys the right to transfer ownership of an asset (the underlying asset) for a period of time in exchange for consideration.

B) a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.

C) a contract that conveys the right for the lessor to obtain substantially all of the economic benefits of the identified asset.

D) a contract, or part of a contract, that conveys the right to transfer a liability for a period of time in exchange for an asset.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is an appropriate journal entry for the recognition by a lessor of the first payment received under an operating lease arrangement?

A) DR Lease expense: CR Cash

B) DR Leased liability: CR Lease income

C) DR Cash: CR Lease income

D) DR Lease expense: CR Deferred initial direct costs

A) DR Lease expense: CR Cash

B) DR Leased liability: CR Lease income

C) DR Cash: CR Lease income

D) DR Lease expense: CR Deferred initial direct costs

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not one of the steps in the classification process of a finance lease?

A) Analyse the lease to determine what risks and rewards are transferred from the lessor to the lessee.

B) Identify the potential risks and rewards associated with the ownership of the asset.

C) Assess whether the risks and rewards have been substantially passed to the lessee.

D) Determine what risks and rewards stay with the owner of the asset.

A) Analyse the lease to determine what risks and rewards are transferred from the lessor to the lessee.

B) Identify the potential risks and rewards associated with the ownership of the asset.

C) Assess whether the risks and rewards have been substantially passed to the lessee.

D) Determine what risks and rewards stay with the owner of the asset.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

17

Nichols Ltd manufactures specialised machinery for both sale and lease. On 1 July 2021, Nichols leased a machine to Pontine Ltd. The costs incurred by Nichols to set up the lease agreement were $1690. The machine cost Nichols Ltd $210 000 to manufacture, and its fair value at the inception of the lease was $232 890. The interest rate implicit in the lease is 10%, which is in line with current market rates. Under the terms of the lease, Pontine Ltd has guaranteed $22 000 of the asset's expected residual value of $40 000 at the end of the 5-year lease term. Pontine Ltd agreed to pay an annual lease payment of $55 000 with the first payment due at the end of the first year. The debit to the sales revenue account in Nichols' books is:

A) $198 823.

B) $210 000.

C) $222 154.

D) $232 890.

A) $198 823.

B) $210 000.

C) $222 154.

D) $232 890.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

18

Barry Limited and Allen Limited enter into a finance lease agreement with the following terms:

-lease term is 4 years

-estimated economic life of the leased asset is 5 years

-4 × annual rental payments of $15 000 each payable in advance

-residual value at the end of the lease term is not guaranteed by the lessee

-interest rate implicit in the lease is 8%.

The journal entry recorded by the lessor when the first lease payment is received would be:

A) DR Cash 15 000 CR Lease receivable 15 000

B) DR Lease receivable 15000 CR Asset 15 000

C) DR Cash 15 000 CR Interest revenue 5 175

CR Lease receivable 9 825

D) DR Cash 15 000 CR Reimbursement revenue 15 000

-lease term is 4 years

-estimated economic life of the leased asset is 5 years

-4 × annual rental payments of $15 000 each payable in advance

-residual value at the end of the lease term is not guaranteed by the lessee

-interest rate implicit in the lease is 8%.

The journal entry recorded by the lessor when the first lease payment is received would be:

A) DR Cash 15 000 CR Lease receivable 15 000

B) DR Lease receivable 15000 CR Asset 15 000

C) DR Cash 15 000 CR Interest revenue 5 175

CR Lease receivable 9 825

D) DR Cash 15 000 CR Reimbursement revenue 15 000

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

19

The preface to AASB 16/IFRS 16 Leases states that the new standard will:

A) enhance disclosures required of entities.

B) provide a greater transparency of a lessee's financial leverage and capital employed.

C) result in a more faithful representation of a lessee's assets and liabilities.

D) all of the above options.

A) enhance disclosures required of entities.

B) provide a greater transparency of a lessee's financial leverage and capital employed.

C) result in a more faithful representation of a lessee's assets and liabilities.

D) all of the above options.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

20

AASB 16/IFRS 16 requires manufacturer and dealer lessors to recognise selling profit or loss:

A) at the commencement of the lease.

B) at the end of the lease.

C) systematically over the lease term.

D) 50% at commencement of the lease and 50% at the end of the lease.

A) at the commencement of the lease.

B) at the end of the lease.

C) systematically over the lease term.

D) 50% at commencement of the lease and 50% at the end of the lease.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

21

On 1 July 2021, One Ltd leased a network server from Short Ltd. The server had cost Short Ltd $32 000 on the same day. The lease agreement cost Short Ltd $1390 to set up and included the following: The journal entry recorded by the lessor to recognise the initial direct costs incurred would be:

A) DR Lease expense $1390 CR Cash $1390

B) DR Deferred initial direct costs - equipment $1390 CR Cash $1390

C) DR Lease expense $1390 CR Deferred initial direct costs - equipment $1390

D) DR Cash $1390 CR Deferred initial direct costs - equipment $1390

The journal entry recorded by the lessor to recognise the initial direct costs incurred would be:A) DR Lease expense $1390 CR Cash $1390

B) DR Deferred initial direct costs - equipment $1390 CR Cash $1390

C) DR Lease expense $1390 CR Deferred initial direct costs - equipment $1390

D) DR Cash $1390 CR Deferred initial direct costs - equipment $1390

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

22

AASB 16/IFRS 16 Leases requires lessors to account for lease receipts from operating leases as:

A) income, on a straight-line basis over the lease term.

B) revenue, on a reducing balance basis over the lease term.

C) income, on inception date of the lease.

D) revenue, at the end of the lease term.

A) income, on a straight-line basis over the lease term.

B) revenue, on a reducing balance basis over the lease term.

C) income, on inception date of the lease.

D) revenue, at the end of the lease term.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

23

In relation to finance leases, the following information must be disclosed separately in the financial statements of lessors:

I. The undiscounted lease payments to be received on an annual basis.

II. A reconciliation of the undiscounted lease payments to the net investment in the lease.

III. A reconciliation of the discounted unguaranteed residual value.

IV. The depreciation charge for each class of right-of-use asset.

A) I, II and III only.

B) I, III and IV only.

C) II, III and IV only.

D) II and IV only.

I. The undiscounted lease payments to be received on an annual basis.

II. A reconciliation of the undiscounted lease payments to the net investment in the lease.

III. A reconciliation of the discounted unguaranteed residual value.

IV. The depreciation charge for each class of right-of-use asset.

A) I, II and III only.

B) I, III and IV only.

C) II, III and IV only.

D) II and IV only.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

24

Under AASB 16/IFRS 16 Leases, lessees are required to disclose which of the following?

I. Interest expense on lease liabilities

II. Income from subleasing right-of-use assets

III. Gains or losses arising from sale and leaseback transaction

IV. Expenses relating to short-term leases

A) I, II and III only.

B) I, III and IV only.

C) II, III and IV only.

D) I, II, III and IV only.

I. Interest expense on lease liabilities

II. Income from subleasing right-of-use assets

III. Gains or losses arising from sale and leaseback transaction

IV. Expenses relating to short-term leases

A) I, II and III only.

B) I, III and IV only.

C) II, III and IV only.

D) I, II, III and IV only.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

25

On 1 July 2021, One Ltd leased a network server from Short Ltd. The server had cost Short Ltd $32 000 on the same day. The lease agreement cost Short Ltd $1390 to set up and included the following: The journal entry recorded by the lessor for the annual recognition of the initial direct costs would be:

A) DR Deferred initial direct costs - equipment $278 CR Lease expense $278

B) DR Lease expense $278 CR Cash $278

C) DR Cash $278 CR Deferred initial direct costs - equipment $278

D) DR Lease expense $278 CR Deferred initial direct costs - equipment $278

The journal entry recorded by the lessor for the annual recognition of the initial direct costs would be:A) DR Deferred initial direct costs - equipment $278 CR Lease expense $278

B) DR Lease expense $278 CR Cash $278

C) DR Cash $278 CR Deferred initial direct costs - equipment $278

D) DR Lease expense $278 CR Deferred initial direct costs - equipment $278

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 25 flashcards in this deck.