Deck 4: The Income Statement

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which of the following is true?

The results of operations of a component of an entity that either has been disposed of or classified as held for sale shall be reported in discontinued operations if:

A) Only I is true.

B) Only II is true.

C) I and II are true, but III is not.

D) I, II, and III are all true.

The results of operations of a component of an entity that either has been disposed of or classified as held for sale shall be reported in discontinued operations if:

A) Only I is true.

B) Only II is true.

C) I and II are true, but III is not.

D) I, II, and III are all true.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The changes in account balances of the Clearwater Corporation during 2011 are presented below:

Assuming there are no changes in retained earnings except for net income and a dividend payment of $19,500, the net income for 2011 should be

A) $6,000.

B) $13,500.

C) $19,500.

D) $25,500.

Assuming there are no changes in retained earnings except for net income and a dividend payment of $19,500, the net income for 2011 should be

A) $6,000.

B) $13,500.

C) $19,500.

D) $25,500.

Question

The following amounts are from Cooper Co.'s 2011 income statement:

What amount would Cooper show for income from continuing operations on a multiple-step format income statement?

A) $52,000

B) $57,000

C) $68,000

D) $96,000

What amount would Cooper show for income from continuing operations on a multiple-step format income statement?

A) $52,000

B) $57,000

C) $68,000

D) $96,000

Question

Orchard Corporation's capital stock at December 31 consisted of the following:

Orchard's common stock, which is listed on a major stock exchange, was quoted at $4 per share on December 31. Orchard's net income for the year ended December 31 was $50,000. The yearly preferred dividend was declared. No capital stock transactions occurred. What was the price earnings ratio on Orchard's common stock at December 31?

A) 6 to 1

B) 8 to 1

C) 10 to 1

D) 16 to 1

Orchard's common stock, which is listed on a major stock exchange, was quoted at $4 per share on December 31. Orchard's net income for the year ended December 31 was $50,000. The yearly preferred dividend was declared. No capital stock transactions occurred. What was the price earnings ratio on Orchard's common stock at December 31?

A) 6 to 1

B) 8 to 1

C) 10 to 1

D) 16 to 1

Question

Question

Neptune Company's income statement for the year ended December 31, 2011, included the following items:

The office space is used equally by Neptune's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Neptune's multiple-step income statement?

A) $870,000

B) $975,000

C) $1,230,000

D) $1,500,000

The office space is used equally by Neptune's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Neptune's multiple-step income statement?

A) $870,000

B) $975,000

C) $1,230,000

D) $1,500,000

Question

Romulan Corporation incurred the following losses during 2011:

Ignoring income taxes, what amount of loss should Romulan report as extraordinary on its annual income statement?

A) $100,000

B) $150,000

C) $270,000

D) $520,000

Ignoring income taxes, what amount of loss should Romulan report as extraordinary on its annual income statement?

A) $100,000

B) $150,000

C) $270,000

D) $520,000

Question

Question

On December 31, 2011 and 2012, Taft Corporation had 100,000 shares of common stock and 50,000 shares of noncumulative and nonconvertible preferred stock issued and outstanding. Additional information:

The price-earnings ratio on common stock at December 31, 2012, was

A) 10 to 1.

B) 12 to 1.

C) 14 to 1.

D) 16 to 1.

The price-earnings ratio on common stock at December 31, 2012, was

A) 10 to 1.

B) 12 to 1.

C) 14 to 1.

D) 16 to 1.

Question

Question

The financial statements of Cresent Corporation for 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, by what amount will 2011 operating income be overstated or understated?

A) $9,200 overstated

B) $9,200 understated

C) $18,800 understated

D) $18,800 overstated

Assuming that none of the errors were detected or corrected, by what amount will 2011 operating income be overstated or understated?

A) $9,200 overstated

B) $9,200 understated

C) $18,800 understated

D) $18,800 overstated

Question

Galaxy Incorporated's financial statements for the years 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, and that no additional errors were made in 2013, by what amount will current assets at December 31, 2013, be overstated or understated?

A) $0

B) $3,000 overstated

C) $9,000 understated

D) $9,000 overstated

Assuming that none of the errors were detected or corrected, and that no additional errors were made in 2013, by what amount will current assets at December 31, 2013, be overstated or understated?

A) $0

B) $3,000 overstated

C) $9,000 understated

D) $9,000 overstated

Question

Question

Burns Company reported the following results from operations for 2011:

Income before extraordinary items was

A) $54,400.

B) $65,200.

C) $76,000.

D) $83,200.

Income before extraordinary items was

A) $54,400.

B) $65,200.

C) $76,000.

D) $83,200.

Question

Yeager Company incurred the following infrequent losses during 2011:

In its 2011 income statement how much should Yeager report as total infrequent losses that are not considered extraordinary?

A) $750,000

B) $840,000

C) $1,290,000

D) $1,430,000

In its 2011 income statement how much should Yeager report as total infrequent losses that are not considered extraordinary?

A) $750,000

B) $840,000

C) $1,290,000

D) $1,430,000

Question

Question

The following information is available for Avalon Company for 2011:

What amount should Avalon report as cost of goods sold for 2011?

A) $510,000

B) $550,000

C) $610,000

D) $650,000

What amount should Avalon report as cost of goods sold for 2011?

A) $510,000

B) $550,000

C) $610,000

D) $650,000

Question

Voyager Corporation separates operating expenses in two categories: (1) selling, and (2) general and administrative. The adjusted trial balance at December 31, 2011, included the following expenses and loss accounts:

One-half of the rented premises is occupied by the sales department. Voyager's total selling expenses for 2011 are

A) $720,000.

B) $740,000.

C) $800,000.

D) $960,000.

One-half of the rented premises is occupied by the sales department. Voyager's total selling expenses for 2011 are

A) $720,000.

B) $740,000.

C) $800,000.

D) $960,000.

Question

The financial statements of Cresent Corporation for 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, by what amount will 2012 operating income be overstated or understated?

A) $13,400 overstated

B) $27,800 understated

C) $35,800 understated

D) $40,600 understated

Assuming that none of the errors were detected or corrected, by what amount will 2012 operating income be overstated or understated?

A) $13,400 overstated

B) $27,800 understated

C) $35,800 understated

D) $40,600 understated

Question

Question

The following expenses were recognized by Kalob Company, a retailer, during 2011:

What should Kalob report as general and administrative expenses for 2011?

A) $210,000

B) $284,000

C) $330,000

D) $404,000

What should Kalob report as general and administrative expenses for 2011?

A) $210,000

B) $284,000

C) $330,000

D) $404,000

Question

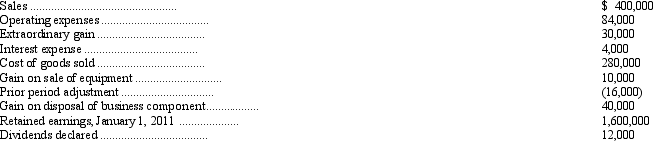

Jaguar Corp. reported the following pretax amounts for the year ending December 31, 2011:

The income tax rate applicable to Jaguar is 30 percent. Prepare a partial income statement for the year ending December 31, 2011, beginning with "Income from continuing operations before income taxes." Include the presentation of earnings per share, assuming 50,000 shares were outstanding during the year.

The income tax rate applicable to Jaguar is 30 percent. Prepare a partial income statement for the year ending December 31, 2011, beginning with "Income from continuing operations before income taxes." Include the presentation of earnings per share, assuming 50,000 shares were outstanding during the year.

Question

Question

Question

Question

Question

Huntington Company has two divisions, A and B. The operations and cash flows of these two divisions are clearly distinguishable. On July 1, 2012, the company decided to dispose of the assets and liabilities of Division B. It is probable that the disposal will be completed early next year. The revenues and expenses of Huntington Company for 2012 and for the preceding two years are as follows:

During the latter part of 2012, Huntington disposed of a portion of Division B and recognized a pretax loss of $10,000 on the disposal. The income tax rate for Huntington Company is 40%.

Prepare the comparative income statements for Huntington Company for the years 2010, 2011, and 2012.

During the latter part of 2012, Huntington disposed of a portion of Division B and recognized a pretax loss of $10,000 on the disposal. The income tax rate for Huntington Company is 40%.

Prepare the comparative income statements for Huntington Company for the years 2010, 2011, and 2012.

Question

Question

Question

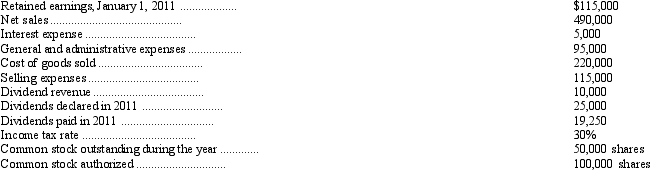

The following data are available from the records of Jazz, Inc.:

Prepare a single-step income statement and a retained earnings statement for Jazz, Inc. for the year ended December 31, 2011.

Prepare a single-step income statement and a retained earnings statement for Jazz, Inc. for the year ended December 31, 2011.

Question

The following data are available for Carlton Products, a partnership:

Compute the purchases and the net income for the partnership for 2010, 2011, and 2012, assuming that the firm sells its merchandise at 25 percent above cost.

Compute the purchases and the net income for the partnership for 2010, 2011, and 2012, assuming that the firm sells its merchandise at 25 percent above cost.

Question

Question

Elwood P. Dowd Company has two divisions, J and K. The operations and cash flows of these two divisions are clearly distinguishable. On July 1, 2012, the company decided to dispose of the assets and liabilities of Division K. It is probable that the disposal will be completed early next year. The revenues and expenses of Dowd Company for 2009 and for the preceding two years are as follows:

During the latter part of 2012, Dowd disposed of a portion of Division K and recognized a pretax loss of $8,000 on the disposal. The income tax rate for Dowd Company is 40%.

Prepare the comparative income statements for Dowd Company for the years 2010, 2011, and 2012.

During the latter part of 2012, Dowd disposed of a portion of Division K and recognized a pretax loss of $8,000 on the disposal. The income tax rate for Dowd Company is 40%.

Prepare the comparative income statements for Dowd Company for the years 2010, 2011, and 2012.

Question

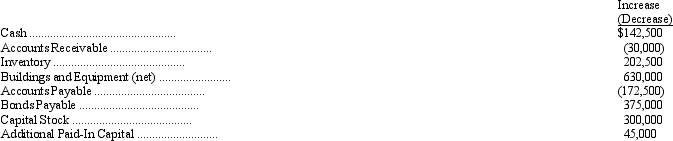

The changes in the account balances and the following additional information are taken from the accounts of the Rainbow Co.

Dividends for 2012 were $82,500. There were no transactions in 2012 affecting retained earnings other than the dividends and net income. Calculate the 2012 net income.

Dividends for 2012 were $82,500. There were no transactions in 2012 affecting retained earnings other than the dividends and net income. Calculate the 2012 net income.

Question

Question

Question

Question

Question

Question

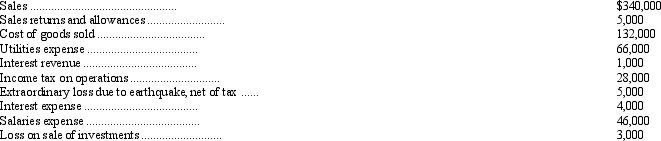

The following pretax amounts pertain to the Brooke Corp. for the year ended December 31, 2011.

The effective corporate tax rate is 30 percent. The company had 10,000 shares of common stock outstanding for the entire year.

The effective corporate tax rate is 30 percent. The company had 10,000 shares of common stock outstanding for the entire year.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/82

Play

Full screen (f)

Deck 4: The Income Statement

1

Generally, recognition criteria are met and revenues are recognized

A) at the point of sale.

B) when cause and effect are associated.

C) at the point of cash collection.

D) at appropriate points throughout the operating cycle.

A) at the point of sale.

B) when cause and effect are associated.

C) at the point of cash collection.

D) at appropriate points throughout the operating cycle.

A

2

Under the general rule of revenue recognition, revenue is recognized when

A) marketability and market price are assured.

B) a contractual agreement exists, and cash collection is assured.

C) the earnings process is complete, and a valid promise of payment has been received.

D) all related expenses have been incurred.

A) marketability and market price are assured.

B) a contractual agreement exists, and cash collection is assured.

C) the earnings process is complete, and a valid promise of payment has been received.

D) all related expenses have been incurred.

C

3

A material loss should be presented separately as a component of income from continuing operations when it is

A) infrequent in occurrence and unusual in nature.

B) infrequent in occurrence but not unusual in nature.

C) a cumulative effect-type change in accounting principle.

D) an extraordinary item.

A) infrequent in occurrence and unusual in nature.

B) infrequent in occurrence but not unusual in nature.

C) a cumulative effect-type change in accounting principle.

D) an extraordinary item.

B

4

Which of the following most likely would be considered a discontinued operation?

A) Production or marketing functions are shifted from one location to another.

B) A sporting goods manufacturer has a bicycle division that meets FASB's definition of a component of the entity and decides to outsource the manufacture of its bicycles.

C) The unprofitable brands of a beauty products component of an entity that manufactures and sells consumer products are discontinued.

D) An entity that is a franchiser in the quick-service restaurant business also operates company-owned restaurants that are unprofitable in a certain region and, as a result, the entity decides to exit both the quick-service business as well as the company-owned restaurants in that region.

A) Production or marketing functions are shifted from one location to another.

B) A sporting goods manufacturer has a bicycle division that meets FASB's definition of a component of the entity and decides to outsource the manufacture of its bicycles.

C) The unprofitable brands of a beauty products component of an entity that manufactures and sells consumer products are discontinued.

D) An entity that is a franchiser in the quick-service restaurant business also operates company-owned restaurants that are unprofitable in a certain region and, as a result, the entity decides to exit both the quick-service business as well as the company-owned restaurants in that region.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

5

In contrast with a multiple-step income statement, a single-step income statement does not show the amount of

A) gross profit.

B) cost of goods sold.

C) income taxes on continuing operations.

D) earnings per share.

A) gross profit.

B) cost of goods sold.

C) income taxes on continuing operations.

D) earnings per share.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

6

A wholesale bakery would normally recognize revenue when

A) the product is available for sale to a customer.

B) cash is received from the customer.

C) goods are delivered to the customer.

D) management chooses to do so.

A) the product is available for sale to a customer.

B) cash is received from the customer.

C) goods are delivered to the customer.

D) management chooses to do so.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

7

Under which of the following conditions would hurricane damage be considered an extraordinary item for financial reporting purposes?

A) Under any circumstances hurricane damage should be classified as an extraordinary item.

B) Only if hurricanes are unusual in nature and infrequent in occurrence in the geographic area

C) Only if hurricanes are normal in the geographic area but do not occur frequently

D) Only if hurricanes occur frequently in the geographic area but have been insured against

A) Under any circumstances hurricane damage should be classified as an extraordinary item.

B) Only if hurricanes are unusual in nature and infrequent in occurrence in the geographic area

C) Only if hurricanes are normal in the geographic area but do not occur frequently

D) Only if hurricanes occur frequently in the geographic area but have been insured against

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

8

The transaction approach to determining income is a concept in which

A) income is measured as the amount that an entity could consume during a period and be as well off at the end of that period as it was at the beginning.

B) market values adjusted for the effects of inflation or deflation are used to calculate income.

C) the financial statement effects of business events are classified as revenues, gains, expenses, and losses, which are used to measure and define income.

D) income equals the change in market value of the firm's outstanding common stock for the period.

A) income is measured as the amount that an entity could consume during a period and be as well off at the end of that period as it was at the beginning.

B) market values adjusted for the effects of inflation or deflation are used to calculate income.

C) the financial statement effects of business events are classified as revenues, gains, expenses, and losses, which are used to measure and define income.

D) income equals the change in market value of the firm's outstanding common stock for the period.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements regarding discontinued operations is true?

A) The assets and liabilities of a disposal group classified as held for sale by an entity may be offset and shown as a single item on the balance sheet of the entity.

B) The assets and liabilities of a disposal group of an entity must be shown separately in the asset and liabilities sections of the balance sheet of the entity and cannot be offset.

C) An adjustment in a subsequent period to the selling price of a component of an entity sold must be reported as a retroactive adjustment in the prior-period financial statements of the entity in which the discontinued operation was reported.

D) The gain or loss on disposal of a component of an entity classified as a discontinued operation need not be disclosed separately from the loss from operations of the discontinued segment.

A) The assets and liabilities of a disposal group classified as held for sale by an entity may be offset and shown as a single item on the balance sheet of the entity.

B) The assets and liabilities of a disposal group of an entity must be shown separately in the asset and liabilities sections of the balance sheet of the entity and cannot be offset.

C) An adjustment in a subsequent period to the selling price of a component of an entity sold must be reported as a retroactive adjustment in the prior-period financial statements of the entity in which the discontinued operation was reported.

D) The gain or loss on disposal of a component of an entity classified as a discontinued operation need not be disclosed separately from the loss from operations of the discontinued segment.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

10

The amount of income reported for tax purposes

A) is normally greater than the net income reported to stockholders.

B) must be computed according to GAAP.

C) is used to compute earnings per share.

D) may differ from the amount of income determined for financial reporting purposes.

A) is normally greater than the net income reported to stockholders.

B) must be computed according to GAAP.

C) is used to compute earnings per share.

D) may differ from the amount of income determined for financial reporting purposes.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

11

On a multiple-step income statement, gains or losses on sale of equipment would be shown

A) before gross profit on sales.

B) after gross profit on sales but before income from continuing operations.

C) after income from continuing operations but before income from extraordinary items.

D) after income before extraordinary items but before net income.

A) before gross profit on sales.

B) after gross profit on sales but before income from continuing operations.

C) after income from continuing operations but before income from extraordinary items.

D) after income before extraordinary items but before net income.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

12

When a business segment is discontinued during the year, the gain or loss on disposal

A) is reported as an extraordinary item.

B) should include only the loss or income from operating the discontinued segment for the current period.

C) excludes only the gain or loss on disposal of the segment.

D) should be shown net of applicable income taxes.

A) is reported as an extraordinary item.

B) should include only the loss or income from operating the discontinued segment for the current period.

C) excludes only the gain or loss on disposal of the segment.

D) should be shown net of applicable income taxes.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is not true regarding restructuring charges?

A) Restructuring charges reflect a loss in asset values of assets no longer consistent with a company's strategic plan.

B) Severance pay for employees working at terminated operations may be a component of restructuring charges.

C) Restructuring charges may include plant closing costs.

D) Restructuring charges are reported as extraordinary items.

A) Restructuring charges reflect a loss in asset values of assets no longer consistent with a company's strategic plan.

B) Severance pay for employees working at terminated operations may be a component of restructuring charges.

C) Restructuring charges may include plant closing costs.

D) Restructuring charges are reported as extraordinary items.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

14

A flood destroyed the home office building of a company located in an inland city. This should be reported as a(n)

A) extraordinary loss.

B) prior period adjustment.

C) loss from continuing operations.

D) loss from discontinued operations.

A) extraordinary loss.

B) prior period adjustment.

C) loss from continuing operations.

D) loss from discontinued operations.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

15

Financial statement elements relating to income are defined in FASB Concepts Statement 6 as follows:

A) Gains are increases in equity from ongoing major or central operations of an entity.

B) Expenses are outflows of assets or liabilities incurred from peripheral or incidental transactions of an entity.

C) Revenues are inflows or other enhancements of assets or settlements of liabilities from ongoing major or central operations.

D) Losses are all decreases in equity other than from transactions with owners.

A) Gains are increases in equity from ongoing major or central operations of an entity.

B) Expenses are outflows of assets or liabilities incurred from peripheral or incidental transactions of an entity.

C) Revenues are inflows or other enhancements of assets or settlements of liabilities from ongoing major or central operations.

D) Losses are all decreases in equity other than from transactions with owners.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

16

A change from the straight-line method of depreciation to an accelerated method should be accounted for as a(n)

A) change in an accounting principle.

B) change in an accounting estimate.

C) prior period adjustment.

D) accounting error.

A) change in an accounting principle.

B) change in an accounting estimate.

C) prior period adjustment.

D) accounting error.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

17

Costs that can be reasonably associated with specific revenues but not with specific products should be

A) charged to expense in the period incurred.

B) allocated to specific products based on the best estimate of the production processing time.

C) expensed in the period in which the related revenue is recognized.

D) capitalized and then amortized over a period not to exceed 60 months.

A) charged to expense in the period incurred.

B) allocated to specific products based on the best estimate of the production processing time.

C) expensed in the period in which the related revenue is recognized.

D) capitalized and then amortized over a period not to exceed 60 months.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following approaches to income measurement underlies financial accounting and reporting?

A) Transaction approach

B) Economic approach

C) Valuation approach

D) Physical capital maintenance approach

A) Transaction approach

B) Economic approach

C) Valuation approach

D) Physical capital maintenance approach

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

19

A single-step income statement is a format that

A) compares the current year's income with last year's income.

B) recognizes subtotals at intermediate stages such as gross margin.

C) combines revenues and gains and subtracts from them expenses and losses, resulting in income from operations.

D) reports sales revenue, cost of goods sold, gross margin, and all other expenses.

A) compares the current year's income with last year's income.

B) recognizes subtotals at intermediate stages such as gross margin.

C) combines revenues and gains and subtracts from them expenses and losses, resulting in income from operations.

D) reports sales revenue, cost of goods sold, gross margin, and all other expenses.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

20

The normal ordering of items in the income statement would be best illustrated by which of the following?

A) Extraordinary items, cumulative effects, income from continuing operations, discontinued operations, net income

B) Income from continuing operations, discontinued operations, extraordinary items, cumulative effects, net income

C) Income from continuing operations, extraordinary items, cumulative effects, discontinued operations, net income

D) Discontinued operations, income from continuing operations, extraordinary items, cumulative effects, net income

A) Extraordinary items, cumulative effects, income from continuing operations, discontinued operations, net income

B) Income from continuing operations, discontinued operations, extraordinary items, cumulative effects, net income

C) Income from continuing operations, extraordinary items, cumulative effects, discontinued operations, net income

D) Discontinued operations, income from continuing operations, extraordinary items, cumulative effects, net income

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

21

Bad debts are recognized according to which of the following expense recognition principles?

A) Direct matching

B) Immediate recognition

C) Systematic and rational allocation

D) Critical event recognition

A) Direct matching

B) Immediate recognition

C) Systematic and rational allocation

D) Critical event recognition

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is correct?

A) Discontinued operations are shown as the last category after income from continuing operations.

B) The discontinued operations section of the income statement consists only of the gain or loss on disposal of the discontinued component net of the tax effect.

C) The discontinued operations section of the income statement consists only of the income or loss from operating the discontinued component net of the tax effect.

D) The discontinued operations section of the income statement consists of the income or loss from operating the discontinued component net of the tax effect as well as the gain or loss on disposal of the discontinued component net of the tax effect.

A) Discontinued operations are shown as the last category after income from continuing operations.

B) The discontinued operations section of the income statement consists only of the gain or loss on disposal of the discontinued component net of the tax effect.

C) The discontinued operations section of the income statement consists only of the income or loss from operating the discontinued component net of the tax effect.

D) The discontinued operations section of the income statement consists of the income or loss from operating the discontinued component net of the tax effect as well as the gain or loss on disposal of the discontinued component net of the tax effect.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

23

Most forecasting exercises begin with a forecast of

A) sales.

B) total assets.

C) net income.

D) cash.

A) sales.

B) total assets.

C) net income.

D) cash.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

24

All of the following components are shown in the income statement net of applicable income taxes except

A) gain or loss on sale of plant assets.

B) cumulative effect of a change in accounting principle.

C) discontinued operations.

D) extraordinary gain or loss.

A) gain or loss on sale of plant assets.

B) cumulative effect of a change in accounting principle.

C) discontinued operations.

D) extraordinary gain or loss.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following would not be reflected in the income statement?

A) An extraordinary item

B) Cumulative effect of a change in depreciation methods

C) Loss on disposal of a segment of a business

D) Correction of an error in previously issued financial statements

A) An extraordinary item

B) Cumulative effect of a change in depreciation methods

C) Loss on disposal of a segment of a business

D) Correction of an error in previously issued financial statements

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

26

All of the following are a component of comprehensive income except

A) foreign currency translation adjustment.

B) unrealized gains and losses on trading securities.

C) deferred gains and losses on derivative financial instruments.

D) change in the minimum pension liability.

A) foreign currency translation adjustment.

B) unrealized gains and losses on trading securities.

C) deferred gains and losses on derivative financial instruments.

D) change in the minimum pension liability.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

27

A company that changes from the declining-balance method of depreciation for previously recorded assets to the straight-line method should report the change as a(n)

A) change in accounting principle.

B) change in accounting estimate.

C) prior period adjustment.

D) extraordinary item.

A) change in accounting principle.

B) change in accounting estimate.

C) prior period adjustment.

D) extraordinary item.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

28

Changes in accounting principles generally are reported as

A) adjustments to prior period statements.

B) extraordinary items.

C) adjustments to current period statements only.

D) adjustments to current and/or prior period statements.

A) adjustments to prior period statements.

B) extraordinary items.

C) adjustments to current period statements only.

D) adjustments to current and/or prior period statements.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

29

The term "comprehensive income" as defined by the FASB

A) must be reported on the face of the income statement.

B) includes all changes in equity during a period except those resulting from investments by and distributions to owners.

C) is the net change in owners' equity for the period.

D) is synonymous with the term "net income."

A) must be reported on the face of the income statement.

B) includes all changes in equity during a period except those resulting from investments by and distributions to owners.

C) is the net change in owners' equity for the period.

D) is synonymous with the term "net income."

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following is true?

The results of operations of a component of an entity that either has been disposed of or classified as held for sale shall be reported in discontinued operations if:

A) Only I is true.

B) Only II is true.

C) I and II are true, but III is not.

D) I, II, and III are all true.

The results of operations of a component of an entity that either has been disposed of or classified as held for sale shall be reported in discontinued operations if:

A) Only I is true.

B) Only II is true.

C) I and II are true, but III is not.

D) I, II, and III are all true.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

31

If a company anticipates a 40% increase in sales volume, then it is most likely that the company will need about a 40% increase in

A) property, plant, and equipment.

B) accounts payable.

C) bank loans payable.

D) operating profit.

A) property, plant, and equipment.

B) accounts payable.

C) bank loans payable.

D) operating profit.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following items is reported only in current and future periods?

A) Prior period adjustment

B) Change in estimate

C) Change in accounting principle

D) Effects of changing prices

A) Prior period adjustment

B) Change in estimate

C) Change in accounting principle

D) Effects of changing prices

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following principles best describes the rationale for matching administrative and selling expenses with revenues of the current period?

A) Direct matching

B) Systematic and rational allocation

C) Immediate recognition

D) Partial recognition

A) Direct matching

B) Systematic and rational allocation

C) Immediate recognition

D) Partial recognition

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is an application of the principle of systematic and rational allocation?

A) Sales commissions

B) Office salaries

C) Telephone expense

D) Depreciation expense

A) Sales commissions

B) Office salaries

C) Telephone expense

D) Depreciation expense

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

35

All of the following represent the likely options for financing business expansion except

A) sale of preferred stock.

B) sale of common stock.

C) internal financing through use of retained earnings.

D) an unrealized gain on available-for-sale securities.

A) sale of preferred stock.

B) sale of common stock.

C) internal financing through use of retained earnings.

D) an unrealized gain on available-for-sale securities.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following events would be considered an extraordinary item?

A) An airline experienced a significant loss due to a strike by employees of the company who provide its aircraft maintenance.

B) A food cannery was faced with a large loss of inventory of canned soups due to government condemnation because of possible botulism contamination; the company had never experienced a similar situation in its history.

C) A company, located on an island which has experienced severe flooding three times in the past 25 years, was subjected to a heavy loss of physical plant due to flooding.

D) A medical corporation was required to pay damages equal to three times its average net income to a patient. The corporation had experienced suits of this nature in the past, but the amount of the losses had never exceeded 5 percent of the corporation's average net income.

A) An airline experienced a significant loss due to a strike by employees of the company who provide its aircraft maintenance.

B) A food cannery was faced with a large loss of inventory of canned soups due to government condemnation because of possible botulism contamination; the company had never experienced a similar situation in its history.

C) A company, located on an island which has experienced severe flooding three times in the past 25 years, was subjected to a heavy loss of physical plant due to flooding.

D) A medical corporation was required to pay damages equal to three times its average net income to a patient. The corporation had experienced suits of this nature in the past, but the amount of the losses had never exceeded 5 percent of the corporation's average net income.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

37

According to the FASB conceptual framework, the concept of "earnings"

A) includes changes in market values of investments in marketable securities classified as available-for-sale.

B) includes foreign currency translation adjustments.

C) includes gains and losses resulting from the sale of a productive asset to another party in an arm's-length transaction.

D) is the same as comprehensive income.

A) includes changes in market values of investments in marketable securities classified as available-for-sale.

B) includes foreign currency translation adjustments.

C) includes gains and losses resulting from the sale of a productive asset to another party in an arm's-length transaction.

D) is the same as comprehensive income.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

38

Accrual-basis net income is most useful for

A) determining the amount of income tax a company should pay.

B) predicting the short-term performance of an enterprise.

C) predicting the long-term performance of an enterprise.

D) determining the amount of dividends a company should pay.

A) determining the amount of income tax a company should pay.

B) predicting the short-term performance of an enterprise.

C) predicting the long-term performance of an enterprise.

D) determining the amount of dividends a company should pay.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is not an acceptable basis for the recognition of expenses?

A) Systematic and rational allocation

B) Direct matching

C) Immediate recognition

D) Cash disbursement

A) Systematic and rational allocation

B) Direct matching

C) Immediate recognition

D) Cash disbursement

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

40

The allowance for doubtful accounts, which appears as a deduction from accounts receivable on a balance sheet, is an application of the

A) going-concern assumption.

B) revenue recognition principle.

C) matching principle.

D) materiality constraint.

A) going-concern assumption.

B) revenue recognition principle.

C) matching principle.

D) materiality constraint.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

41

The changes in account balances of the Clearwater Corporation during 2011 are presented below:

Assuming there are no changes in retained earnings except for net income and a dividend payment of $19,500, the net income for 2011 should be

A) $6,000.

B) $13,500.

C) $19,500.

D) $25,500.

Assuming there are no changes in retained earnings except for net income and a dividend payment of $19,500, the net income for 2011 should be

A) $6,000.

B) $13,500.

C) $19,500.

D) $25,500.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

42

The following amounts are from Cooper Co.'s 2011 income statement:

What amount would Cooper show for income from continuing operations on a multiple-step format income statement?

A) $52,000

B) $57,000

C) $68,000

D) $96,000

What amount would Cooper show for income from continuing operations on a multiple-step format income statement?

A) $52,000

B) $57,000

C) $68,000

D) $96,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

43

Orchard Corporation's capital stock at December 31 consisted of the following:

Orchard's common stock, which is listed on a major stock exchange, was quoted at $4 per share on December 31. Orchard's net income for the year ended December 31 was $50,000. The yearly preferred dividend was declared. No capital stock transactions occurred. What was the price earnings ratio on Orchard's common stock at December 31?

A) 6 to 1

B) 8 to 1

C) 10 to 1

D) 16 to 1

Orchard's common stock, which is listed on a major stock exchange, was quoted at $4 per share on December 31. Orchard's net income for the year ended December 31 was $50,000. The yearly preferred dividend was declared. No capital stock transactions occurred. What was the price earnings ratio on Orchard's common stock at December 31?

A) 6 to 1

B) 8 to 1

C) 10 to 1

D) 16 to 1

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following accounting changes requires the restatement of financial statements presented for prior years?

A) A change in depreciation method from the straight-line method to the double-declining-balance method

B) A change from the LIFO to the FIFO inventory valuation method

C) A change from the FIFO to the LIFO inventory valuation method

D) A change in the useful life used in the depreciation calculations for a company's manufacturing equipment

A) A change in depreciation method from the straight-line method to the double-declining-balance method

B) A change from the LIFO to the FIFO inventory valuation method

C) A change from the FIFO to the LIFO inventory valuation method

D) A change in the useful life used in the depreciation calculations for a company's manufacturing equipment

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

45

Neptune Company's income statement for the year ended December 31, 2011, included the following items:

The office space is used equally by Neptune's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Neptune's multiple-step income statement?

A) $870,000

B) $975,000

C) $1,230,000

D) $1,500,000

The office space is used equally by Neptune's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Neptune's multiple-step income statement?

A) $870,000

B) $975,000

C) $1,230,000

D) $1,500,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

46

Romulan Corporation incurred the following losses during 2011:

Ignoring income taxes, what amount of loss should Romulan report as extraordinary on its annual income statement?

A) $100,000

B) $150,000

C) $270,000

D) $520,000

Ignoring income taxes, what amount of loss should Romulan report as extraordinary on its annual income statement?

A) $100,000

B) $150,000

C) $270,000

D) $520,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

47

International Accounting Standard 8 requires

A) a restatement of prior years' income for a change in accounting principle.

B) the reporting of the cumulative effect of a change in accounting principle as part of net income in the year of the change.

C) the reporting of the cumulative effect of a change in accounting principle as a direct adjustment to beginning retained earnings in the year of the change.

D) the amortization of the cumulative effect of a change in accounting principle over the future periods expected to be affected by the change.

A) a restatement of prior years' income for a change in accounting principle.

B) the reporting of the cumulative effect of a change in accounting principle as part of net income in the year of the change.

C) the reporting of the cumulative effect of a change in accounting principle as a direct adjustment to beginning retained earnings in the year of the change.

D) the amortization of the cumulative effect of a change in accounting principle over the future periods expected to be affected by the change.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

48

On December 31, 2011 and 2012, Taft Corporation had 100,000 shares of common stock and 50,000 shares of noncumulative and nonconvertible preferred stock issued and outstanding. Additional information:

The price-earnings ratio on common stock at December 31, 2012, was

A) 10 to 1.

B) 12 to 1.

C) 14 to 1.

D) 16 to 1.

The price-earnings ratio on common stock at December 31, 2012, was

A) 10 to 1.

B) 12 to 1.

C) 14 to 1.

D) 16 to 1.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

49

Neptune Company's gross sales in 2011 were $3,930,000. Assuming sales returns and allowances were $74,000, sales discounts were $35,000, and freight-out was $28,000, what were Neptune's net sales in 2011?

A) $3,793,000

B) $3,821,000

C) $3,856,000

D) $3,930,000

A) $3,793,000

B) $3,821,000

C) $3,856,000

D) $3,930,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

50

The financial statements of Cresent Corporation for 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, by what amount will 2011 operating income be overstated or understated?

A) $9,200 overstated

B) $9,200 understated

C) $18,800 understated

D) $18,800 overstated

Assuming that none of the errors were detected or corrected, by what amount will 2011 operating income be overstated or understated?

A) $9,200 overstated

B) $9,200 understated

C) $18,800 understated

D) $18,800 overstated

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

51

Galaxy Incorporated's financial statements for the years 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, and that no additional errors were made in 2013, by what amount will current assets at December 31, 2013, be overstated or understated?

A) $0

B) $3,000 overstated

C) $9,000 understated

D) $9,000 overstated

Assuming that none of the errors were detected or corrected, and that no additional errors were made in 2013, by what amount will current assets at December 31, 2013, be overstated or understated?

A) $0

B) $3,000 overstated

C) $9,000 understated

D) $9,000 overstated

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

52

On June 30, 2011, Osborn Company's operating facilities in Nebraska were destroyed by an earthquake. The loss of $700,000 was not covered by insurance. Osborn's tax rate for 2011 is 40 percent. In Osborn's income statement for the year ended September 30, 2011, this event should be reported as an extraordinary loss of

A) $0.

B) $280,000.

C) $420,000.

D) $700,000.

A) $0.

B) $280,000.

C) $420,000.

D) $700,000.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

53

Burns Company reported the following results from operations for 2011:

Income before extraordinary items was

A) $54,400.

B) $65,200.

C) $76,000.

D) $83,200.

Income before extraordinary items was

A) $54,400.

B) $65,200.

C) $76,000.

D) $83,200.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

54

Yeager Company incurred the following infrequent losses during 2011:

In its 2011 income statement how much should Yeager report as total infrequent losses that are not considered extraordinary?

A) $750,000

B) $840,000

C) $1,290,000

D) $1,430,000

In its 2011 income statement how much should Yeager report as total infrequent losses that are not considered extraordinary?

A) $750,000

B) $840,000

C) $1,290,000

D) $1,430,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

55

Jupiter Manufacturing Company sold plant assets at a gain of $205,000 less related taxes of $62,500. Assuming the gain is not considered unusual or infrequent, Jupiter's income statement for the period should report

A) a prior period adjustment net of applicable taxes, $142,500.

B) an extraordinary item net of applicable taxes, $142,500.

C) a gain of $205,000 and an increase in income tax expense of $62,500.

D) operating income net of applicable taxes, $142,500.

A) a prior period adjustment net of applicable taxes, $142,500.

B) an extraordinary item net of applicable taxes, $142,500.

C) a gain of $205,000 and an increase in income tax expense of $62,500.

D) operating income net of applicable taxes, $142,500.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

56

The following information is available for Avalon Company for 2011:

What amount should Avalon report as cost of goods sold for 2011?

A) $510,000

B) $550,000

C) $610,000

D) $650,000

What amount should Avalon report as cost of goods sold for 2011?

A) $510,000

B) $550,000

C) $610,000

D) $650,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

57

Voyager Corporation separates operating expenses in two categories: (1) selling, and (2) general and administrative. The adjusted trial balance at December 31, 2011, included the following expenses and loss accounts:

One-half of the rented premises is occupied by the sales department. Voyager's total selling expenses for 2011 are

A) $720,000.

B) $740,000.

C) $800,000.

D) $960,000.

One-half of the rented premises is occupied by the sales department. Voyager's total selling expenses for 2011 are

A) $720,000.

B) $740,000.

C) $800,000.

D) $960,000.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

58

The financial statements of Cresent Corporation for 2011 and 2012 contained the following errors:

Assuming that none of the errors were detected or corrected, by what amount will 2012 operating income be overstated or understated?

A) $13,400 overstated

B) $27,800 understated

C) $35,800 understated

D) $40,600 understated

Assuming that none of the errors were detected or corrected, by what amount will 2012 operating income be overstated or understated?

A) $13,400 overstated

B) $27,800 understated

C) $35,800 understated

D) $40,600 understated

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

59

Byron Inc. decided on August 1, 2011, to dispose of a component of its business. The component was sold on November 30, 2011. Byron's income for 2011 included income of $250,000 from operating the discontinued segment from January 1 to the sale date. Byron incurred a loss on the November 30 sale of $220,000. Ignoring income taxes, what amount should be reported in the 2011 income statement as the net income or loss under "Discontinued Operations"?

A) $220,000 loss

B) $30,000 loss

C) $30,000 income

D) $250,000 income

A) $220,000 loss

B) $30,000 loss

C) $30,000 income

D) $250,000 income

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

60

The following expenses were recognized by Kalob Company, a retailer, during 2011:

What should Kalob report as general and administrative expenses for 2011?

A) $210,000

B) $284,000

C) $330,000

D) $404,000

What should Kalob report as general and administrative expenses for 2011?

A) $210,000

B) $284,000

C) $330,000

D) $404,000

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

61

Jaguar Corp. reported the following pretax amounts for the year ending December 31, 2011:

The income tax rate applicable to Jaguar is 30 percent. Prepare a partial income statement for the year ending December 31, 2011, beginning with "Income from continuing operations before income taxes." Include the presentation of earnings per share, assuming 50,000 shares were outstanding during the year.

The income tax rate applicable to Jaguar is 30 percent. Prepare a partial income statement for the year ending December 31, 2011, beginning with "Income from continuing operations before income taxes." Include the presentation of earnings per share, assuming 50,000 shares were outstanding during the year.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

62

Greene Enterprises, Inc., has two operating divisions, one manufactures machinery and the other is a trucking operation that has been used to ship finished product for the manufacturing operation. Both divisions are considered separate components as defined by SFAS No. 144. The management of Greene Enterprises wants to focus on the manufacturing operation and accordingly adopted a formal plan to sell the trucking division on November 15, 2011. The sale was completed on April 30, 2012. At December 31, 2011, the trucking component was considered as held for sale.

On December 31, 2011, the company's fiscal year-end, the book value of the assets of the trucking division was $250,000. On that date, the fair value of the assets, less costs to sell, was $200,000. The before-tax operating loss of the division for the year was $140,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $400,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

On December 31, 2011, the company's fiscal year-end, the book value of the assets of the trucking division was $250,000. On that date, the fair value of the assets, less costs to sell, was $200,000. The before-tax operating loss of the division for the year was $140,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $400,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following is true regarding Statement of Financial Accounting Standards No. 144, "Accounting for the Impairment or Disposal of Long-Lived Assets," accounting and reporting standards for discontinued operations?

A) A component of a business always represents the same concept as a segment of a business used in reporting disaggregated information.

B) Discontinued operations should follow extraordinary items on the face of the income statement.

C) A test for, and recognition of, an impairment loss would be necessary for a component that had not been sold by year-end if the fair value of the component was determined to be less than the book value.

D) The gain or loss recognized for reported in the discontinued operation section of the income statement includes only the gain or loss on disposal of the component and not the income or loss from operating the discontinued operation.

A) A component of a business always represents the same concept as a segment of a business used in reporting disaggregated information.

B) Discontinued operations should follow extraordinary items on the face of the income statement.

C) A test for, and recognition of, an impairment loss would be necessary for a component that had not been sold by year-end if the fair value of the component was determined to be less than the book value.

D) The gain or loss recognized for reported in the discontinued operation section of the income statement includes only the gain or loss on disposal of the component and not the income or loss from operating the discontinued operation.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

64

The forecast of income for future periods begins with a forecast of sales. An accurate projection of sales is essential to the determination of the amount of assets needed to do business and the level of financing required.

What factors should be considered in preparing the forecast of sales?

What factors should be considered in preparing the forecast of sales?

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

65

Panther Corp. purchased a patent on January 2, 2006, for $700,000. The original life of the patent was estimated to be 14 years. In December of 2011, the company received information that the patent would be obsolete within 4 years. Accordingly, the company decided to write off the unamortized portion of the patent cost over 5 years beginning in 2011.

How would the change in useful life be reflected in the accounts for 2011 and subsequent years?

How would the change in useful life be reflected in the accounts for 2011 and subsequent years?

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

66

Huntington Company has two divisions, A and B. The operations and cash flows of these two divisions are clearly distinguishable. On July 1, 2012, the company decided to dispose of the assets and liabilities of Division B. It is probable that the disposal will be completed early next year. The revenues and expenses of Huntington Company for 2012 and for the preceding two years are as follows:

During the latter part of 2012, Huntington disposed of a portion of Division B and recognized a pretax loss of $10,000 on the disposal. The income tax rate for Huntington Company is 40%.

Prepare the comparative income statements for Huntington Company for the years 2010, 2011, and 2012.

During the latter part of 2012, Huntington disposed of a portion of Division B and recognized a pretax loss of $10,000 on the disposal. The income tax rate for Huntington Company is 40%.

Prepare the comparative income statements for Huntington Company for the years 2010, 2011, and 2012.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

67

The revenue principle states that revenue should be recognized at a point when

A) an exchange transaction involving goods and services has occurred and the earnings process is essentially complete.

B) an order for shipment of a definite amount of merchandise has been received.

C) a contract between buyer and seller has been signed by both parties.

D) the seller has shipped merchandise to a customer under the terms that the customer need not pay for the merchandise until it is sold.

A) an exchange transaction involving goods and services has occurred and the earnings process is essentially complete.

B) an order for shipment of a definite amount of merchandise has been received.

C) a contract between buyer and seller has been signed by both parties.

D) the seller has shipped merchandise to a customer under the terms that the customer need not pay for the merchandise until it is sold.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

68

Blocker Enterprises, Inc., has two operating divisions, one manufactures farm machinery and the other manufactures office furniture. Both divisions are considered separate components as defined by SFAS No. 144. The management of Blocker Enterprises wants to focus on the manufacturing of farm machinery and accordingly adopted a formal plan to sell the office furniture division on September 20, 2011. The sale was completed on March 10, 2012. At December 31, 2011, the office furniture component was considered as held for sale.

On December 31, 2011, the company's fiscal year-end, the book value of the assets of the office furniture division was $1,000,000. On that date, the fair value of the assets, less costs to sell, was $800,000. The before-tax operating loss of the division for the year was $130,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $350,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

On December 31, 2011, the company's fiscal year-end, the book value of the assets of the office furniture division was $1,000,000. On that date, the fair value of the assets, less costs to sell, was $800,000. The before-tax operating loss of the division for the year was $130,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $350,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

69

The following data are available from the records of Jazz, Inc.:

Prepare a single-step income statement and a retained earnings statement for Jazz, Inc. for the year ended December 31, 2011.

Prepare a single-step income statement and a retained earnings statement for Jazz, Inc. for the year ended December 31, 2011.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

70

The following data are available for Carlton Products, a partnership:

Compute the purchases and the net income for the partnership for 2010, 2011, and 2012, assuming that the firm sells its merchandise at 25 percent above cost.

Compute the purchases and the net income for the partnership for 2010, 2011, and 2012, assuming that the firm sells its merchandise at 25 percent above cost.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following categories of expenses is subject to immediate recognition on the income statement?

A) Utilities expense for the production line of a manufacturer

B) Repairs and maintenance expense incurred on production equipment of a manufacturer

C) The salary of the production foreman

D) The salary of the company president

A) Utilities expense for the production line of a manufacturer

B) Repairs and maintenance expense incurred on production equipment of a manufacturer

C) The salary of the production foreman

D) The salary of the company president

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

72

Elwood P. Dowd Company has two divisions, J and K. The operations and cash flows of these two divisions are clearly distinguishable. On July 1, 2012, the company decided to dispose of the assets and liabilities of Division K. It is probable that the disposal will be completed early next year. The revenues and expenses of Dowd Company for 2009 and for the preceding two years are as follows:

During the latter part of 2012, Dowd disposed of a portion of Division K and recognized a pretax loss of $8,000 on the disposal. The income tax rate for Dowd Company is 40%.

Prepare the comparative income statements for Dowd Company for the years 2010, 2011, and 2012.

During the latter part of 2012, Dowd disposed of a portion of Division K and recognized a pretax loss of $8,000 on the disposal. The income tax rate for Dowd Company is 40%.

Prepare the comparative income statements for Dowd Company for the years 2010, 2011, and 2012.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

73

The changes in the account balances and the following additional information are taken from the accounts of the Rainbow Co.

Dividends for 2012 were $82,500. There were no transactions in 2012 affecting retained earnings other than the dividends and net income. Calculate the 2012 net income.

Dividends for 2012 were $82,500. There were no transactions in 2012 affecting retained earnings other than the dividends and net income. Calculate the 2012 net income.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

74

A classic definition of income states that income is the amount one could consume at the end of a period and still be as well off as at the beginning of the period. Embedded in this definition of income is the concept of capital maintenance. Conceptually, income can occur only after the beginning capital has been recovered. When accountants adopt different measuring units, they are attempting to maintain different concepts of capital.

Identify the type of capital maintained when the measuring unit is (a) nominal dollars, (b) constant dollars, and (c) current costs. When would nominal cost and constant dollar measurements provide equivalent results?

Identify the type of capital maintained when the measuring unit is (a) nominal dollars, (b) constant dollars, and (c) current costs. When would nominal cost and constant dollar measurements provide equivalent results?

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following would be treated as an extraordinary item?

A) Expropriation of an entity's operations in a foreign country

B) The write-down of inventory due to obsolescence

C) A loss resulting from a strike by workers against an entity

D) The write-off of accounts receivable not expected to be collected

A) Expropriation of an entity's operations in a foreign country

B) The write-down of inventory due to obsolescence

C) A loss resulting from a strike by workers against an entity

D) The write-off of accounts receivable not expected to be collected

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

76

Landon, Inc., has several operating divisions. In September 2011, the management of Landon decided on a formal plan to sell one of its divisions. This division is considered a separate component as defined by SFAS No. 144.

The sale was completed on December 10, 2011, at which time the division was sold for $900,000. The book value of the assets of the division was $1,000,000. The before-tax operating loss of the division for the period January 1, 2011 to the date of disposal was $130,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $350,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

The sale was completed on December 10, 2011, at which time the division was sold for $900,000. The book value of the assets of the division was $1,000,000. The before-tax operating loss of the division for the period January 1, 2011 to the date of disposal was $130,000. The company's tax rate is 40%. The after-tax income from continuing operations for 2011 was $350,000.

Prepare a partial income statement for 2011 beginning with income from continuing operations. Ignore EPS disclosures.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

77

All of the following would appear on a single-step income statement except

A) cost of goods sold.

B) extraordinary items.

C) discontinued operations.

D) gross profit.

A) cost of goods sold.

B) extraordinary items.

C) discontinued operations.

D) gross profit.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

78

An example of direct matching of an expense with revenues would be

A) depreciation expense.

B) office salaries expense.

C) direct labor costs incurred to produce inventory sold during a period.

D) advertising expense.

A) depreciation expense.

B) office salaries expense.

C) direct labor costs incurred to produce inventory sold during a period.

D) advertising expense.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

79

The following pretax amounts pertain to the Brooke Corp. for the year ended December 31, 2011.

The effective corporate tax rate is 30 percent. The company had 10,000 shares of common stock outstanding for the entire year.

The effective corporate tax rate is 30 percent. The company had 10,000 shares of common stock outstanding for the entire year.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

80

Provo Water Products had sales during 2011 of $895,000. Provo's gross profit percentage is 55 percent. Purchases of inventory during 2011 totaled $466,250 and a count of inventory on hand at the end of the year totaled $189,500. Selling expenses are 18 percent of sales and general and administrative expenses are equal to 80 percent of selling expenses. Provo's income tax rate is 30 percent and the company has 60,000 shares of common stock outstanding.

Prepare an income statement, including earnings per share data, for the year ended December 31, 2011.

Prepare an income statement, including earnings per share data, for the year ended December 31, 2011.

Unlock Deck

Unlock for access to all 82 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 82 flashcards in this deck.