Deck 22: Accounting in a Global Market

Full screen (f)

Question

Heiner Company. converts its foreign subsidiary financial statements using the translation process. The company's subsidiary in the Czech Republic reported the following for 2011: revenues and expenses of 25,000,000 and 18,500,000 koruna, respectively, earned or incurred evenly throughout the year, dividends of 1,500,000 koruna were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $148,500.

B) $227,500.

C) $175,000.

D) $195,000.

Translated net income for 2011 is

A) $148,500.

B) $227,500.

C) $175,000.

D) $195,000.

Question

Question

Albright Distributing Inc. converts its foreign subsidiary financial statements using the translation process. Their German subsidiary reported the following for 2011: revenues and expenses of 10,050,000 and 7,800,000 marks, respectively, earned or incurred evenly throughout the year, dividends of 2,000,000 marks were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $641,250.

B) $607,500.

C) $131,250.

D) $97,500.

Translated net income for 2011 is

A) $641,250.

B) $607,500.

C) $131,250.

D) $97,500.

Question

Maxim Importing Company. converts its foreign subsidiary financial statements using the translation process. The company's French subsidiary reported the following for 2011: revenues and expenses of 10,500,000 and 6,505,000 francs, respectively, earned or incurred evenly throughout the year, dividends of 500,000 francs were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $733,950.

B) $805,860.

C) $838,950.

D) $910,860.

Translated net income for 2011 is

A) $733,950.

B) $805,860.

C) $838,950.

D) $910,860.

Question

Question

Question

Question

Tokyo Enterprises, a subsidiary of Worldwide Enterprises based in Dallas, reported the following information at the end of its first year of operations (all in yen): assets--110,000,000; expenses--41,000,000; liabilities--97,500,000; capital stock--5,500,000; revenues--48,000,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $21,000 debit adjustment

B) $76,000 debit adjustment

C) $21,000 credit adjustment

D) $76,000 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $21,000 debit adjustment

B) $76,000 debit adjustment

C) $21,000 credit adjustment

D) $76,000 credit adjustment

Question

Question

Question

Question

Question

Question

Question

Question

European Trading Company. converts its foreign subsidiary financial statements using the translation process. The company's Swiss subsidiary reported the following for 2011: revenues and expenses of 14,119,000 and 7,985,000 Swiss francs, respectively, earned or incurred evenly throughout the year, dividends of 2,000,000 Swiss francs were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $846,264.

B) $699,852.

C) $1,202,264.

D) $1,091,852.

Translated net income for 2011 is

A) $846,264.

B) $699,852.

C) $1,202,264.

D) $1,091,852.

Question

Question

Question

Question

Question

Question

Sarkozy Enterprises, a subsidiary of Obama Company based in New York, reported the following information at the end of its first year of operations (all in French francs): assets--4,790,000; expenses--6,500,000; liabilities--2,950,000; capital stock--1,200;000, revenues--7,140,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $1,287 debit adjustment

B) $1,287 credit adjustment

C) $6,080 debit adjustment

D) $6,080 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $1,287 debit adjustment

B) $1,287 credit adjustment

C) $6,080 debit adjustment

D) $6,080 credit adjustment

Question

Question

Fleming Company. converts its foreign subsidiary financial statements using the translation process. The company's subsidiary in Denmark reported the following for 2011: revenues and expenses of 80,000 and 54,000 kroner, respectively, earned or incurred evenly throughout the year, dividends of 32,000 kroner were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $70,200.

B) $78,000.

C) $(16,200).

D) $(8,400).

Translated net income for 2011 is

A) $70,200.

B) $78,000.

C) $(16,200).

D) $(8,400).

Question

Question

Question

Brown Enterprises, a subsidiary of Biden Company based in Delaware, reported the following information at the end of its first year of operations (all in British pounds): assets--483,000; expenses--360,000; liabilities--105,000; capital stock--90,000, revenues--648,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $34,020 debit adjustment

B) $34,020 credit adjustment

C) $11,520 debit adjustment

D) $11,520 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $34,020 debit adjustment

B) $34,020 credit adjustment

C) $11,520 debit adjustment

D) $11,520 credit adjustment

Question

Question

Question

Churchill Enterprises, a subsidiary of Roosevelt Company based in New York, reported the following information at the end of its first year of operations (all in British pounds): assets--338,000; expenses--360,000; liabilities--101,000; capital stock--80;000, revenues--517,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $26,280 debit adjustment

B) $26,280 credit adjustment

C) $6,280 credit adjustment

D) $6,280 debit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $26,280 debit adjustment

B) $26,280 credit adjustment

C) $6,280 credit adjustment

D) $6,280 debit adjustment

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Rome Enterprises, a subsidiary of La Italia Company based in New York, reported the following information at the end of its first year of operations (all in euros): assets--1,320,000; expenses--340,000; liabilities--880,000; capital stock--80,000, revenues--400,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $25,200 debit adjustment

B) $34,800 debit adjustment

C) $34,800 credit adjustment

D) $25,200 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $25,200 debit adjustment

B) $34,800 debit adjustment

C) $34,800 credit adjustment

D) $25,200 credit adjustment

Question

On July 15, 2011, United Manufacturing Inc., a New York based conglomerate, purchased, Sky Inc., a Korean-based company. Sky Inc.'s balance sheet on the date of purchase is as follows:

Question

Question

Question

Sunset Technological, Inc., a U.S. multinational producer of computer hardware, has subsidiaries located throughout the world. Sunset Technology purchased Werner Technology Company, a Swiss producer of computer hardware components, on January 1, 2010. Werner's financial statements are prepared and submitted in Swiss francs to Sunset's headquarters. Werner's adjusted trial balance at December 31, 2011, is presented below:

Werner Technology Company

Adjusted Trial Balance

December 31, 2011

(in Swiss Francs)

Relevant exchange rates for 2011 and 2010 are as follows:

The statement of retained earnings for the year ended December 31, 2010, is as follows (in U.S. dollars):

Required:

Prepare a translated statement of income and retained earnings, and a translated statement of financial position in U.S. dollars for Werner Technology for 2011.

Werner Technology Company

Adjusted Trial Balance

December 31, 2011

(in Swiss Francs)

Relevant exchange rates for 2011 and 2010 are as follows:

The statement of retained earnings for the year ended December 31, 2010, is as follows (in U.S. dollars):

Required:

Prepare a translated statement of income and retained earnings, and a translated statement of financial position in U.S. dollars for Werner Technology for 2011.

Question

Reagan Corporation, a U.S. company, owns a 100% interest in its subsidiary, Thatcher Limited., located in the United Kingdom. Thatcher began operations on January 1, 2010. All revenues and expenses are received and paid in British pounds. The subsidiary maintains its accounting records in British pounds. In light of these facts, management of the U.S. parent has determined that the British pound is the functional currency of the subsidiary.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below in British pounds:

The following are relevant exchange rates for the year 2011:

£1 = $1.51 at the beginning of 2010, at which time the common stock

was issued.

£1 = $1.55 weighted average for 2011.

£1 = $1.58 at the date the dividends were declared and paid.

£1 = $1.53 at the end of 2011.

£1 = $1.56 at the beginning of 2011.

The balance of the cumulative translation account at January 1, 2011, was $1,157.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended for Thatcher, Limited.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below in British pounds:

The following are relevant exchange rates for the year 2011:

£1 = $1.51 at the beginning of 2010, at which time the common stock

was issued.

£1 = $1.55 weighted average for 2011.

£1 = $1.58 at the date the dividends were declared and paid.

£1 = $1.53 at the end of 2011.

£1 = $1.56 at the beginning of 2011.

The balance of the cumulative translation account at January 1, 2011, was $1,157.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended for Thatcher, Limited.

Question

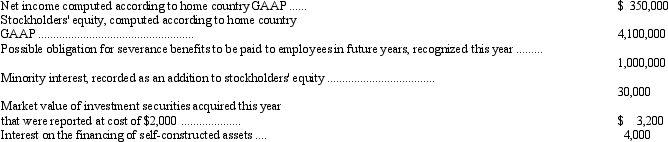

Financial information for Toro Enterprises at the end of 2011 is as follows:

Relevant exchange rates are as follows:

In addition, the computed retained earnings balance from the prior year's translated financial statements is $2,405,000 at the end of 2011.

Prepare a translated trial balance for Toro Enterprises.

Relevant exchange rates are as follows:

In addition, the computed retained earnings balance from the prior year's translated financial statements is $2,405,000 at the end of 2011.

Prepare a translated trial balance for Toro Enterprises.

Question

The following financial information is for Olaf Company, a non-U.S. firm with shares listed on a U.S. stock exchange:

If Olaf Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $3,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of Olaf's reported stockholders' equity and net income to U.S. GAAP.

If Olaf Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $3,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of Olaf's reported stockholders' equity and net income to U.S. GAAP.

Question

The following financial information is for DC Company, a non-U.S. firm with shares listed on a U.S. stock exchange:

If DC Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $4,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of DC's reported stockholders' equity and net income to U.S. GAAP.

If DC Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $4,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of DC's reported stockholders' equity and net income to U.S. GAAP.

Question

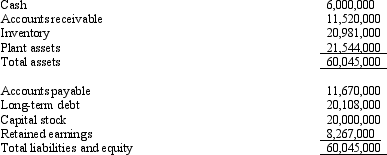

Mankato, Inc., purchased Kyoto Manufacturing Company, a Japanese company, on January 4, 2011. On the date of purchase, the exchange rate for 1 Japanese yen was U.S. $0.007. The balance sheet for Kyoto Manufacturing Co.,on the date of purchase is shown below:

Kyoto Manufacturing Co.

Balance Sheet

January 4, 2011

(in Japanese yen)

Required:

Prepare a translated balance sheet as of January 4, 2011.

Kyoto Manufacturing Co.

Balance Sheet

January 4, 2011

(in Japanese yen)

Required:

Prepare a translated balance sheet as of January 4, 2011.

Question

Question

Question

Question

The following financial information is available for Paul Company, a hypothetical non-U.S. firm with shares listed on a U.S. stock exchange:

If Paul were following U.S. GAAP, development costs would be expensed when incurred.

According to U.S. GAAP, the possible obligation for severance benefits would not be recognized until it had become probable.

Prepare a reconciliation of Paul's reported stockholders' equity and net income to the amounts of these items under U.S. GAAP.

If Paul were following U.S. GAAP, development costs would be expensed when incurred.

According to U.S. GAAP, the possible obligation for severance benefits would not be recognized until it had become probable.

Prepare a reconciliation of Paul's reported stockholders' equity and net income to the amounts of these items under U.S. GAAP.

Question

Question

Question

Question

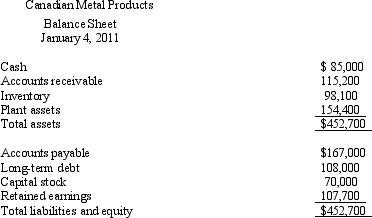

Northern Metalworks, Inc., purchased Canadian Metal Products, a Canadian company, on January 4, 2011. On the date of purchase, the exchange rate for 1 Canadian dollar was U.S. $0.79. Canadian Metal Products balance sheet on the date of purchase is shown below:

Required:

Prepare a translated balance sheet as of January 4, 2011.

Required:

Prepare a translated balance sheet as of January 4, 2011.

Question

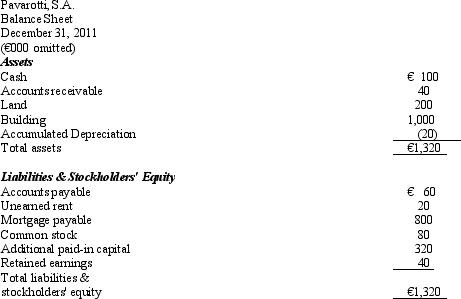

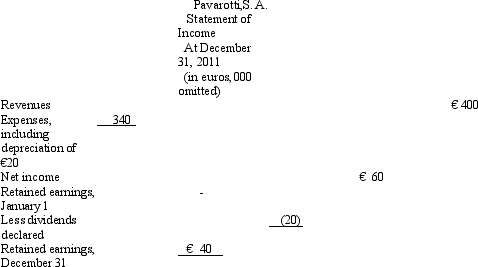

Domingo Company, a U.S. company, owns a 100% interest in its subsidiary, Pavarotti, S.A., located in Italy. Pavarotti, S.A., began operations on January 1, 2011. The subsidiary's operations consist of leasing space in an office building. The building, which cost one million euros, was financed primarily by Italian banks. All revenues and expenses are received and paid in euros. The subsidiary also maintains its accounting records in euros. In light of these facts, management of the U.S. parent has determined that the euro is the functional currency of the subsidiary.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below, in euros:

The following are relevant exchange rates for the year 2011:

€1 = $1.50 at the beginning of 2011, at which time the common stock

was issued and the land and building were financed by the mortgage.

€1 = $1.55 weighted average for 2011.

€1 = $1.58 at the date the dividends were declared and paid and

the unearned rent was received.

€1 = $1.62 at the end of 2011.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below, in euros:

The following are relevant exchange rates for the year 2011:

€1 = $1.50 at the beginning of 2011, at which time the common stock

was issued and the land and building were financed by the mortgage.

€1 = $1.55 weighted average for 2011.

€1 = $1.58 at the date the dividends were declared and paid and

the unearned rent was received.

€1 = $1.62 at the end of 2011.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/60

Play

Full screen (f)

Deck 22: Accounting in a Global Market

1

Heiner Company. converts its foreign subsidiary financial statements using the translation process. The company's subsidiary in the Czech Republic reported the following for 2011: revenues and expenses of 25,000,000 and 18,500,000 koruna, respectively, earned or incurred evenly throughout the year, dividends of 1,500,000 koruna were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $148,500.

B) $227,500.

C) $175,000.

D) $195,000.

Translated net income for 2011 is

A) $148,500.

B) $227,500.

C) $175,000.

D) $195,000.

B

2

Foreign currency translation adjustments arising from translation of the financial statements of a foreign subsidiary are reported in

A) stockholders' equity of the foreign subsidiary.

B) revenue or expenses of the foreign subsidiary.

C) consolidated net income of the parent company and the foreign subsidiary.

D) stockholders' equity of the parent company.

A) stockholders' equity of the foreign subsidiary.

B) revenue or expenses of the foreign subsidiary.

C) consolidated net income of the parent company and the foreign subsidiary.

D) stockholders' equity of the parent company.

D

3

Albright Distributing Inc. converts its foreign subsidiary financial statements using the translation process. Their German subsidiary reported the following for 2011: revenues and expenses of 10,050,000 and 7,800,000 marks, respectively, earned or incurred evenly throughout the year, dividends of 2,000,000 marks were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $641,250.

B) $607,500.

C) $131,250.

D) $97,500.

Translated net income for 2011 is

A) $641,250.

B) $607,500.

C) $131,250.

D) $97,500.

B

4

Maxim Importing Company. converts its foreign subsidiary financial statements using the translation process. The company's French subsidiary reported the following for 2011: revenues and expenses of 10,500,000 and 6,505,000 francs, respectively, earned or incurred evenly throughout the year, dividends of 500,000 francs were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $733,950.

B) $805,860.

C) $838,950.

D) $910,860.

Translated net income for 2011 is

A) $733,950.

B) $805,860.

C) $838,950.

D) $910,860.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

5

Complete the following statement by choosing the best response:

If the functional currency of a foreign subsidiary is the local currency of the country in which the foreign subsidiary operates, then

A) the foreign subsidiary's financial statements are translated into U.S. dollars.

B) the foreign subsidiary's financial statements must be remeasured into U.S. dollars.

C) only the foreign subsidiary's assets and liabilities must be remeasured into U.S. dollars

D) only retained earnings must be remeasured into U.S. dollars.

If the functional currency of a foreign subsidiary is the local currency of the country in which the foreign subsidiary operates, then

A) the foreign subsidiary's financial statements are translated into U.S. dollars.

B) the foreign subsidiary's financial statements must be remeasured into U.S. dollars.

C) only the foreign subsidiary's assets and liabilities must be remeasured into U.S. dollars

D) only retained earnings must be remeasured into U.S. dollars.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is not correct regarding the translation of a foreign entity's accounts?

A) Translation uses the historical rate at the date a foreign subsidiary was acquired for the paid-in capital amounts.

B) Translation uses the current rate method.

C) Translation should be used in a translating the accounts of a foreign entity operating in a highly inflationary economy.

D) Foreign currency translation adjustments are displayed under the accumulated comprehensive income section of the translated balance sheet.

A) Translation uses the historical rate at the date a foreign subsidiary was acquired for the paid-in capital amounts.

B) Translation uses the current rate method.

C) Translation should be used in a translating the accounts of a foreign entity operating in a highly inflationary economy.

D) Foreign currency translation adjustments are displayed under the accumulated comprehensive income section of the translated balance sheet.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is not a short-term convergence topic that the IASB must address in order to eliminate the reconciliation of accounts prepared under different sets of standards of different countries?

A) Segment reporting

B) Accounting for income taxes

C) Accounting for impairments of assets

D) Accounting for research and development costs

A) Segment reporting

B) Accounting for income taxes

C) Accounting for impairments of assets

D) Accounting for research and development costs

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

8

Tokyo Enterprises, a subsidiary of Worldwide Enterprises based in Dallas, reported the following information at the end of its first year of operations (all in yen): assets--110,000,000; expenses--41,000,000; liabilities--97,500,000; capital stock--5,500,000; revenues--48,000,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $21,000 debit adjustment

B) $76,000 debit adjustment

C) $21,000 credit adjustment

D) $76,000 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $21,000 debit adjustment

B) $76,000 debit adjustment

C) $21,000 credit adjustment

D) $76,000 credit adjustment

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

9

The SEC currently requires foreign companies that list shares on U.S. exchanges to provide

A) both complete U.S. GAAP financial statements and a reconciliation of their reported income under non-U.S. GAAP to the reported income under U.S. GAAP.

B) only complete U.S. GAAP financial statements; the SEC will not accept under any circumstances only a reconciliation of an entity's reported income under non-U.S. GAAP to reported income under U.S. GAAP.

C) complete U.S. GAAP financial statements or a reconciliation of their reported income under non-U.S. GAAP to reported income under U.S. GAAP.

D) only a reconciliation of their reported income under non-U.S. GAAP to reported income under U.S. GAAP; the SEC will not accept under any circumstances only a complete set of U.S. GAAP financial statements.

A) both complete U.S. GAAP financial statements and a reconciliation of their reported income under non-U.S. GAAP to the reported income under U.S. GAAP.

B) only complete U.S. GAAP financial statements; the SEC will not accept under any circumstances only a reconciliation of an entity's reported income under non-U.S. GAAP to reported income under U.S. GAAP.

C) complete U.S. GAAP financial statements or a reconciliation of their reported income under non-U.S. GAAP to reported income under U.S. GAAP.

D) only a reconciliation of their reported income under non-U.S. GAAP to reported income under U.S. GAAP; the SEC will not accept under any circumstances only a complete set of U.S. GAAP financial statements.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is theleast likely means a company might choose to meet the needs of international investors?

A) Translation of financial statements or annual reports into the language of the user.

B) Denomination of the financial statements in the currency of the country where the financial statements will be used.

C) Partial or complete restatement of financial statements to the accounting principles of the financial statement users' country.

D) Mutual recognition in which one country accepts the financial statements of another country for regulatory purposes such as listing on stock exchanges or filing annual reports.

A) Translation of financial statements or annual reports into the language of the user.

B) Denomination of the financial statements in the currency of the country where the financial statements will be used.

C) Partial or complete restatement of financial statements to the accounting principles of the financial statement users' country.

D) Mutual recognition in which one country accepts the financial statements of another country for regulatory purposes such as listing on stock exchanges or filing annual reports.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is not a short-term convergence topic that the FASB must address in order to eliminate the reconciliation of accounts prepared under different sets of standards of different countries?

A) Segment reporting

B) Accounting for income taxes

C) Accounting for research and development costs

D) Accounting for the impairment of assets

A) Segment reporting

B) Accounting for income taxes

C) Accounting for research and development costs

D) Accounting for the impairment of assets

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements is correct?

A) Capital stock of a foreign subsidiary is translated at the historical rate, that is, the rate prevailing on the date the subsidiary was acquired.

B) Dividends are translated at the average exchange rate for the year.

C) Retained earnings are translated at the average exchange rate for the year.

D) Assets and liabilities are translated at the historical rate prevailing when the subsidiary was acquired.

A) Capital stock of a foreign subsidiary is translated at the historical rate, that is, the rate prevailing on the date the subsidiary was acquired.

B) Dividends are translated at the average exchange rate for the year.

C) Retained earnings are translated at the average exchange rate for the year.

D) Assets and liabilities are translated at the historical rate prevailing when the subsidiary was acquired.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is not a long-term, joint FASB-IASB project?

A) Accounting for income taxes

B) Fair value measurement

C) Derecognition

D) Accounting and reporting for intangible assets

A) Accounting for income taxes

B) Fair value measurement

C) Derecognition

D) Accounting and reporting for intangible assets

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements most accurately reflects the approach the FASB and IASB have identified for reaching convergence of U.S. and international accounting standards?

A) Convergence will be achieved primarily by modifying FASB standards to conform with IASB standards.

B) Convergence will be achieved primarily by modifying IASB standards to conform with FASB standards.

C) FASB and IASB will create new standards rather than trying to eliminate differences between standards that are in need of significant improvement.

D) FASB and IASB will try to eliminate differences between standards by eliminating differences between existing standards of the two standard-setting bodies that can be easily resolved and will then work jointly on more complex issues.

A) Convergence will be achieved primarily by modifying FASB standards to conform with IASB standards.

B) Convergence will be achieved primarily by modifying IASB standards to conform with FASB standards.

C) FASB and IASB will create new standards rather than trying to eliminate differences between standards that are in need of significant improvement.

D) FASB and IASB will try to eliminate differences between standards by eliminating differences between existing standards of the two standard-setting bodies that can be easily resolved and will then work jointly on more complex issues.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is the primary factor in determining the functional currency of a foreign subsidiary?

A) How the costs for the foreign entity's product are determined

B) The denomination of the foreign entity's financing

C) The location of the primary sales market that influences the price of the foreign entity's product

D) Management's assessment of all relevant factors

A) How the costs for the foreign entity's product are determined

B) The denomination of the foreign entity's financing

C) The location of the primary sales market that influences the price of the foreign entity's product

D) Management's assessment of all relevant factors

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

16

European Trading Company. converts its foreign subsidiary financial statements using the translation process. The company's Swiss subsidiary reported the following for 2011: revenues and expenses of 14,119,000 and 7,985,000 Swiss francs, respectively, earned or incurred evenly throughout the year, dividends of 2,000,000 Swiss francs were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $846,264.

B) $699,852.

C) $1,202,264.

D) $1,091,852.

Translated net income for 2011 is

A) $846,264.

B) $699,852.

C) $1,202,264.

D) $1,091,852.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

17

The foreign currency translation adjustments amount is a(n)

A) account in the parent company's general ledger.

B) account in the foreign subsidiary's general ledger.

C) balancing amount for translation.

D) balancing amount for remeasurement.

A) account in the parent company's general ledger.

B) account in the foreign subsidiary's general ledger.

C) balancing amount for translation.

D) balancing amount for remeasurement.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

18

Current generally accepted accounting principles require that the translation of a foreign subsidiary's accounting records should be accomplished by the

A) monetary/nonmonetary method.

B) current rate method.

C) current/noncurrent method.

D) functional currency method.

A) monetary/nonmonetary method.

B) current rate method.

C) current/noncurrent method.

D) functional currency method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

19

The primary purpose of the Security and Exchange Commission's Form 20-F is to

A) explain in detail the differences between the internal controls established under the accounting and auditing principles of a foreign country and those of the United States.

B) determine the fee a foreign company must pay to register its financial statements with the Securities and Exchange Commission.

C) explain in detail the differences between net income computed under the accounting principles of a foreign country and U.S. GAAP.

D) explain in detail the differences between total assets measured using the accounting principles of a foreign country and U.S. GAAP.

A) explain in detail the differences between the internal controls established under the accounting and auditing principles of a foreign country and those of the United States.

B) determine the fee a foreign company must pay to register its financial statements with the Securities and Exchange Commission.

C) explain in detail the differences between net income computed under the accounting principles of a foreign country and U.S. GAAP.

D) explain in detail the differences between total assets measured using the accounting principles of a foreign country and U.S. GAAP.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

20

A translation adjustment resulting from the translation process is disclosed on the financial statements as

A) a separate component of stockholders' equity.

B) a below-the-line item on the income statement.

C) an adjustment to retained earnings.

D) a part of income from operations on the income statement.

A) a separate component of stockholders' equity.

B) a below-the-line item on the income statement.

C) an adjustment to retained earnings.

D) a part of income from operations on the income statement.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

21

Under international accounting standards, revenue is recognized

A) only when a sale and delivery have occurred.

B) upon the increase in the fair value of biological assets (e.g., cattle) without waiting for the assets to be sold.

C) upon the increase in the fair value of agricultural produce (e.g., harvested wheat) without waiting for the assets to be sold

D) upon the increase in the fair value of both biological assets (e.g., cattle) and agricultural produce (e.g., harvested wheat) without waiting for the assets to be sold.

A) only when a sale and delivery have occurred.

B) upon the increase in the fair value of biological assets (e.g., cattle) without waiting for the assets to be sold.

C) upon the increase in the fair value of agricultural produce (e.g., harvested wheat) without waiting for the assets to be sold

D) upon the increase in the fair value of both biological assets (e.g., cattle) and agricultural produce (e.g., harvested wheat) without waiting for the assets to be sold.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

22

Sarkozy Enterprises, a subsidiary of Obama Company based in New York, reported the following information at the end of its first year of operations (all in French francs): assets--4,790,000; expenses--6,500,000; liabilities--2,950,000; capital stock--1,200;000, revenues--7,140,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $1,287 debit adjustment

B) $1,287 credit adjustment

C) $6,080 debit adjustment

D) $6,080 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $1,287 debit adjustment

B) $1,287 credit adjustment

C) $6,080 debit adjustment

D) $6,080 credit adjustment

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements is true regarding equity reserves?

A) Under U.S. GAAP, Other Comprehensive Income represents an equity reserve.

B) Under U.S. GAAP, the allowance for doubtful accounts is considered an equity reserve.

C) Under U.S. GAAP, appropriations of retained earnings are considered an equity reserve.

D) Under U.S. GAAP, equity reserves are not currently allowed.

A) Under U.S. GAAP, Other Comprehensive Income represents an equity reserve.

B) Under U.S. GAAP, the allowance for doubtful accounts is considered an equity reserve.

C) Under U.S. GAAP, appropriations of retained earnings are considered an equity reserve.

D) Under U.S. GAAP, equity reserves are not currently allowed.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

24

Fleming Company. converts its foreign subsidiary financial statements using the translation process. The company's subsidiary in Denmark reported the following for 2011: revenues and expenses of 80,000 and 54,000 kroner, respectively, earned or incurred evenly throughout the year, dividends of 32,000 kroner were paid during the year. The following exchange rates are available:

Translated net income for 2011 is

A) $70,200.

B) $78,000.

C) $(16,200).

D) $(8,400).

Translated net income for 2011 is

A) $70,200.

B) $78,000.

C) $(16,200).

D) $(8,400).

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

25

Under international accounting standards, cash paid for interest (associated with interest expense) can be shown on the statement of cash flows as an

A) operating activity only.

B) operating activity or a financing activity.

C) operating activity or an investing activity.

D) investing or financing activity.

A) operating activity only.

B) operating activity or a financing activity.

C) operating activity or an investing activity.

D) investing or financing activity.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

26

Under international accounting standards, the standard for accounting for construction contracts

A) allows only the completed-contract method.

B) expresses a preference for the completed-contract method only in some circumstances.

C) does not allow the completed-contract method.

D) does not allow the percentage-of-completion method.

A) allows only the completed-contract method.

B) expresses a preference for the completed-contract method only in some circumstances.

C) does not allow the completed-contract method.

D) does not allow the percentage-of-completion method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

27

Brown Enterprises, a subsidiary of Biden Company based in Delaware, reported the following information at the end of its first year of operations (all in British pounds): assets--483,000; expenses--360,000; liabilities--105,000; capital stock--90,000, revenues--648,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $34,020 debit adjustment

B) $34,020 credit adjustment

C) $11,520 debit adjustment

D) $11,520 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $34,020 debit adjustment

B) $34,020 credit adjustment

C) $11,520 debit adjustment

D) $11,520 credit adjustment

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

28

Under international accounting standards, cash received from dividends (associated with dividend revenue) can be shown on the statement of cash flows as

A) a financing activity only.

B) an operating or a financing activity.

C) a financing or an investing activity.

D) an investing activity only.

A) a financing activity only.

B) an operating or a financing activity.

C) a financing or an investing activity.

D) an investing activity only.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

29

Under international accounting standards, cash paid for income taxes (associated with income tax expense) can be shown on the statement of cash flows as an

A) operating activity only.

B) operating activity, or may be split between operating, investing, and financing activities depending on the nature of the transaction giving rise to the tax payment.

C) operating activity, or may be split between operating and investing activities depending on the transaction giving rise to the tax payment.

D) operating activity, or may be split between investing and financing activities depending on the transaction giving rise to the payment.

A) operating activity only.

B) operating activity, or may be split between operating, investing, and financing activities depending on the nature of the transaction giving rise to the tax payment.

C) operating activity, or may be split between operating and investing activities depending on the transaction giving rise to the tax payment.

D) operating activity, or may be split between investing and financing activities depending on the transaction giving rise to the payment.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

30

Churchill Enterprises, a subsidiary of Roosevelt Company based in New York, reported the following information at the end of its first year of operations (all in British pounds): assets--338,000; expenses--360,000; liabilities--101,000; capital stock--80;000, revenues--517,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $26,280 debit adjustment

B) $26,280 credit adjustment

C) $6,280 credit adjustment

D) $6,280 debit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $26,280 debit adjustment

B) $26,280 credit adjustment

C) $6,280 credit adjustment

D) $6,280 debit adjustment

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is true regarding the accounting for research and development costs under international accounting standards?

A) All research and development costs of any type are expensed.

B) All ordinary research and development costs are expensed, but development costs related to computer software are capitalized.

C) All ordinary research and development costs are expensed, but both research and development costs related to computer software are capitalized.

D) All development costs of any nature are capitalized.

A) All research and development costs of any type are expensed.

B) All ordinary research and development costs are expensed, but development costs related to computer software are capitalized.

C) All ordinary research and development costs are expensed, but both research and development costs related to computer software are capitalized.

D) All development costs of any nature are capitalized.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

32

Under international accounting standards regarding depreciation, an entity

A) may depreciate separately the components of a composite asset (e.g., land and building)

B) is not allowed to depreciate the components of a composite asset (e.g., land and building) separately.

C) must depreciate separately the components of a composite asset (e.g., land and building) separately.

D) must use fair value accounting for property, plant, and equipment, thus eliminating the need for depreciation.

A) may depreciate separately the components of a composite asset (e.g., land and building)

B) is not allowed to depreciate the components of a composite asset (e.g., land and building) separately.

C) must depreciate separately the components of a composite asset (e.g., land and building) separately.

D) must use fair value accounting for property, plant, and equipment, thus eliminating the need for depreciation.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is true regarding the accounting for property, plant, and equipment under international accounting standards?

A) Upward revaluations of property, plant, and equipment are not allowed.

B) The option is available for an entity to adjust upward the carrying value of property, plant, and equipment to fair value.

C) All entities must adjust upward the carrying value of property, plant, and equipment to fair value.

D) An entity has the option to adjust upward the carrying value of property, plant, and equipment to fair value, with gains and losses being shown in other comprehensive income.

A) Upward revaluations of property, plant, and equipment are not allowed.

B) The option is available for an entity to adjust upward the carrying value of property, plant, and equipment to fair value.

C) All entities must adjust upward the carrying value of property, plant, and equipment to fair value.

D) An entity has the option to adjust upward the carrying value of property, plant, and equipment to fair value, with gains and losses being shown in other comprehensive income.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

34

Under international accounting standards, cash paid for dividends can be shown on the statement of cash flows as

A) a financing activity only.

B) an investing activity only.

C) a financing or an operating activity.

D) should not be shown on the statement of cash flows but rather on the income statement.

A) a financing activity only.

B) an investing activity only.

C) a financing or an operating activity.

D) should not be shown on the statement of cash flows but rather on the income statement.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

35

Under international accounting standards, the derecognition of receivables requires that

A) economic ownership of the asset passes from the transferor to the transferee.

B) a binding legal agreement must exist between the transferor and the transferee.

C) the risks and rewards associated with the cash flows from the financial asset pass from the transferor to the transferee.

D) the receivable is determined to be fully collectible.

A) economic ownership of the asset passes from the transferor to the transferee.

B) a binding legal agreement must exist between the transferor and the transferee.

C) the risks and rewards associated with the cash flows from the financial asset pass from the transferor to the transferee.

D) the receivable is determined to be fully collectible.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

36

Under international accounting standards, cash received from interest (associated with interest revenue) can be shown on the statement of cash flows as an

A) operating activity only.

B) operating or financing activity.

C) operating or investing activity.

D) investing or financing activity.

A) operating activity only.

B) operating or financing activity.

C) operating or investing activity.

D) investing or financing activity.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is the current group within the International Accounting Standard Board organization that interprets existing standards or provides guidance in areas for which no accounting formal standard exists?

A) Standing Interpretations Committee

B) International Accounting Standards Committee

C) Emerging Issues Task Force

D) International Financial Reporting Interpretations Committee

A) Standing Interpretations Committee

B) International Accounting Standards Committee

C) Emerging Issues Task Force

D) International Financial Reporting Interpretations Committee

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is true regarding the application of lower-of-cost-or-market method under international accounting standards?

A) Inventory is recorded at the lower-of-cost-or-market value (defined as replacement cost of the inventory).

B) Inventory is recorded at the lower-of-cost-or-market value defined as net-realizable value.

C) Inventory is recorded at the lower-of-cost-or-market value defined as net-realizable value, minus the normal profit margin.

D) No lower-of-cost-or-market rule for inventory exists under international accounting standards.

A) Inventory is recorded at the lower-of-cost-or-market value (defined as replacement cost of the inventory).

B) Inventory is recorded at the lower-of-cost-or-market value defined as net-realizable value.

C) Inventory is recorded at the lower-of-cost-or-market value defined as net-realizable value, minus the normal profit margin.

D) No lower-of-cost-or-market rule for inventory exists under international accounting standards.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

39

Under international accounting standards, which of the following methods of inventory costing is not acceptable?

A) Weighted-average

B) Moving-average

C) FIFO

D) LIFO

A) Weighted-average

B) Moving-average

C) FIFO

D) LIFO

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

40

Rome Enterprises, a subsidiary of La Italia Company based in New York, reported the following information at the end of its first year of operations (all in euros): assets--1,320,000; expenses--340,000; liabilities--880,000; capital stock--80,000, revenues--400,000. Relevant exchange rates are as follows:

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $25,200 debit adjustment

B) $34,800 debit adjustment

C) $34,800 credit adjustment

D) $25,200 credit adjustment

As a result of the translation process, what amount is recorded on the financial statements as the translation adjustment?

A) $25,200 debit adjustment

B) $34,800 debit adjustment

C) $34,800 credit adjustment

D) $25,200 credit adjustment

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

41

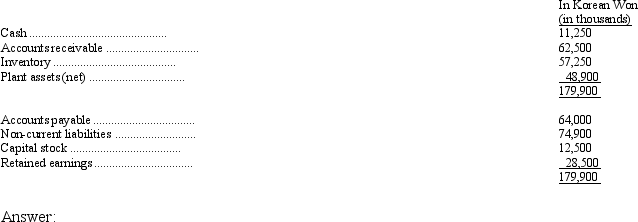

On July 15, 2011, United Manufacturing Inc., a New York based conglomerate, purchased, Sky Inc., a Korean-based company. Sky Inc.'s balance sheet on the date of purchase is as follows:

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

42

The measurement of deferred tax liabilities and assets under international accounting standards requires the use of

A) current-year tax rates; use of future-years' tax rates even though enacted is prohibited.

B) currently-enacted tax rates for future years..

C) currently-enacted tax rates for future years and future tax rates that have been announced by the government but have not yet been formally enacted into law

D) tax rates in effect when the temporary difference originated.

A) current-year tax rates; use of future-years' tax rates even though enacted is prohibited.

B) currently-enacted tax rates for future years..

C) currently-enacted tax rates for future years and future tax rates that have been announced by the government but have not yet been formally enacted into law

D) tax rates in effect when the temporary difference originated.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

43

Under international accounting standards, if a sale-leaseback results in an operating lease then

A) any profit on the original sale is deferred and recognized over the life of the subsequent lease.

B) assuming the original sale was clearly at fair value, any profit is recognized immediately even when the leaseback results in an operating lease.

C) any profit on the original sale is deferred and recognized over the life of the leased asset.

D) any profit on the original sale is not recognized in the financial statements.

A) any profit on the original sale is deferred and recognized over the life of the subsequent lease.

B) assuming the original sale was clearly at fair value, any profit is recognized immediately even when the leaseback results in an operating lease.

C) any profit on the original sale is deferred and recognized over the life of the leased asset.

D) any profit on the original sale is not recognized in the financial statements.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

44

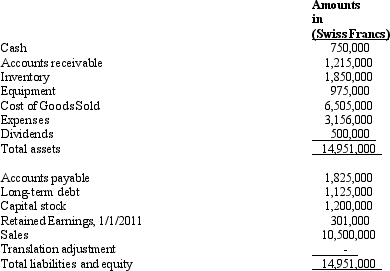

Sunset Technological, Inc., a U.S. multinational producer of computer hardware, has subsidiaries located throughout the world. Sunset Technology purchased Werner Technology Company, a Swiss producer of computer hardware components, on January 1, 2010. Werner's financial statements are prepared and submitted in Swiss francs to Sunset's headquarters. Werner's adjusted trial balance at December 31, 2011, is presented below:

Werner Technology Company

Adjusted Trial Balance

December 31, 2011

(in Swiss Francs)

Relevant exchange rates for 2011 and 2010 are as follows:

The statement of retained earnings for the year ended December 31, 2010, is as follows (in U.S. dollars):

Required:

Prepare a translated statement of income and retained earnings, and a translated statement of financial position in U.S. dollars for Werner Technology for 2011.

Werner Technology Company

Adjusted Trial Balance

December 31, 2011

(in Swiss Francs)

Relevant exchange rates for 2011 and 2010 are as follows:

The statement of retained earnings for the year ended December 31, 2010, is as follows (in U.S. dollars):

Required:

Prepare a translated statement of income and retained earnings, and a translated statement of financial position in U.S. dollars for Werner Technology for 2011.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

45

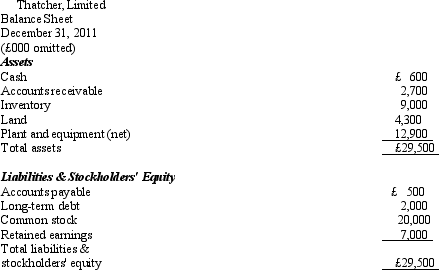

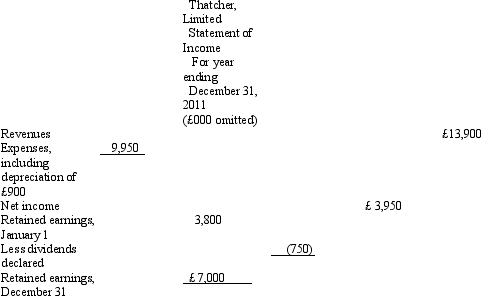

Reagan Corporation, a U.S. company, owns a 100% interest in its subsidiary, Thatcher Limited., located in the United Kingdom. Thatcher began operations on January 1, 2010. All revenues and expenses are received and paid in British pounds. The subsidiary maintains its accounting records in British pounds. In light of these facts, management of the U.S. parent has determined that the British pound is the functional currency of the subsidiary.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below in British pounds:

The following are relevant exchange rates for the year 2011:

£1 = $1.51 at the beginning of 2010, at which time the common stock

was issued.

£1 = $1.55 weighted average for 2011.

£1 = $1.58 at the date the dividends were declared and paid.

£1 = $1.53 at the end of 2011.

£1 = $1.56 at the beginning of 2011.

The balance of the cumulative translation account at January 1, 2011, was $1,157.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended for Thatcher, Limited.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below in British pounds:

The following are relevant exchange rates for the year 2011:

£1 = $1.51 at the beginning of 2010, at which time the common stock

was issued.

£1 = $1.55 weighted average for 2011.

£1 = $1.58 at the date the dividends were declared and paid.

£1 = $1.53 at the end of 2011.

£1 = $1.56 at the beginning of 2011.

The balance of the cumulative translation account at January 1, 2011, was $1,157.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended for Thatcher, Limited.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

46

Financial information for Toro Enterprises at the end of 2011 is as follows:

Relevant exchange rates are as follows:

In addition, the computed retained earnings balance from the prior year's translated financial statements is $2,405,000 at the end of 2011.

Prepare a translated trial balance for Toro Enterprises.

Relevant exchange rates are as follows:

In addition, the computed retained earnings balance from the prior year's translated financial statements is $2,405,000 at the end of 2011.

Prepare a translated trial balance for Toro Enterprises.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

47

The following financial information is for Olaf Company, a non-U.S. firm with shares listed on a U.S. stock exchange:

If Olaf Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $3,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of Olaf's reported stockholders' equity and net income to U.S. GAAP.

If Olaf Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $3,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of Olaf's reported stockholders' equity and net income to U.S. GAAP.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

48

The following financial information is for DC Company, a non-U.S. firm with shares listed on a U.S. stock exchange:

If DC Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $4,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of DC's reported stockholders' equity and net income to U.S. GAAP.

If DC Company were following U.S. GAAP, the minority interest would have been classified as a liability instead of as part of stockholders' equity. In addition, minority interest income of $4,000 for the year would have been excluded from the computation of net income. Under U.S. GAAP the investment securities would have been classified as trading securities and the interest on financing of self-constructed assets would have been capitalized rather than expensed.

Prepare reconciliations of DC's reported stockholders' equity and net income to U.S. GAAP.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

49

Mankato, Inc., purchased Kyoto Manufacturing Company, a Japanese company, on January 4, 2011. On the date of purchase, the exchange rate for 1 Japanese yen was U.S. $0.007. The balance sheet for Kyoto Manufacturing Co.,on the date of purchase is shown below:

Kyoto Manufacturing Co.

Balance Sheet

January 4, 2011

(in Japanese yen)

Required:

Prepare a translated balance sheet as of January 4, 2011.

Kyoto Manufacturing Co.

Balance Sheet

January 4, 2011

(in Japanese yen)

Required:

Prepare a translated balance sheet as of January 4, 2011.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

50

Under international accounting standards, the pension-related asset or liability is recognized on the balance sheet as the

A) net amount of the difference between the projected benefit obligation and plan assets and the deferred items (prior service cost, deferred pension gain/loss).

B) difference between the projected benefit obligation and plan assets.

C) difference between the accumulated benefit obligation and plan assets.

D) difference between the vested benefit obligation and plan assets.

A) net amount of the difference between the projected benefit obligation and plan assets and the deferred items (prior service cost, deferred pension gain/loss).

B) difference between the projected benefit obligation and plan assets.

C) difference between the accumulated benefit obligation and plan assets.

D) difference between the vested benefit obligation and plan assets.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

51

Under international accounting standards, deferred tax assets and liabilities are classified as

A) current and noncurrent.

B) only noncurrent.

C) only current.

D) neither current or noncurrent but are disclosed in a separate section of the balance sheet.

A) current and noncurrent.

B) only noncurrent.

C) only current.

D) neither current or noncurrent but are disclosed in a separate section of the balance sheet.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following is correct regarding the treatment of short-term obligations expected to be refinanced?

A) If an obligation has actually been refinanced or a firm refinancing agreement is in place by the date financial statements are issued, then reclassify the short-term obligation as long-term

B) Classify the short-term obligation as long-term if the obligation has been refinanced by the balance sheet date.

C) Classify the short-term obligation as long-term if the obligation has been refinanced by the date the financial statements are issued

D) There is no provision for reclassifying short-term obligations expected to refinanced as long-term obligations under international accounting standards.

A) If an obligation has actually been refinanced or a firm refinancing agreement is in place by the date financial statements are issued, then reclassify the short-term obligation as long-term

B) Classify the short-term obligation as long-term if the obligation has been refinanced by the balance sheet date.

C) Classify the short-term obligation as long-term if the obligation has been refinanced by the date the financial statements are issued

D) There is no provision for reclassifying short-term obligations expected to refinanced as long-term obligations under international accounting standards.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

53

The following financial information is available for Paul Company, a hypothetical non-U.S. firm with shares listed on a U.S. stock exchange:

If Paul were following U.S. GAAP, development costs would be expensed when incurred.

According to U.S. GAAP, the possible obligation for severance benefits would not be recognized until it had become probable.

Prepare a reconciliation of Paul's reported stockholders' equity and net income to the amounts of these items under U.S. GAAP.

If Paul were following U.S. GAAP, development costs would be expensed when incurred.

According to U.S. GAAP, the possible obligation for severance benefits would not be recognized until it had become probable.

Prepare a reconciliation of Paul's reported stockholders' equity and net income to the amounts of these items under U.S. GAAP.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

54

Under international accounting standards, remote contingent liabilities are

A) not disclosed.

B) not disclosed unless a guarantee arrangement (e. g., cosigning the loan of another party) exists.

C) disclosed if the amount of the contingent liability is reasonably estimable.

D) treated the same as reasonable possible contingencies.

A) not disclosed.

B) not disclosed unless a guarantee arrangement (e. g., cosigning the loan of another party) exists.

C) disclosed if the amount of the contingent liability is reasonably estimable.

D) treated the same as reasonable possible contingencies.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following statements is correct?

A) Capital stock of a foreign subsidiary is translated at the historical rate, that is, the rate prevailing on the date the subsidiary was acquired.

B) Dividends are translated at the average exchange rate for the year.

C) Retained earnings are translated at the average exchange rate for the year.

D) Assets and liabilities are translated at the historical rate prevailing when the subsidiary was acquired.

A) Capital stock of a foreign subsidiary is translated at the historical rate, that is, the rate prevailing on the date the subsidiary was acquired.

B) Dividends are translated at the average exchange rate for the year.

C) Retained earnings are translated at the average exchange rate for the year.

D) Assets and liabilities are translated at the historical rate prevailing when the subsidiary was acquired.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is correct regarding international accounting standards for the impairment of intangible assets?

A) Goodwill impairments may not be reversed.

B) Goodwill impairments may be reversed.

C) No impairment losses may be reversed.

D) A distinction is made between impairment procedures for intangibles with finite and indefinite lives.

A) Goodwill impairments may not be reversed.

B) Goodwill impairments may be reversed.

C) No impairment losses may be reversed.

D) A distinction is made between impairment procedures for intangibles with finite and indefinite lives.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

57

Northern Metalworks, Inc., purchased Canadian Metal Products, a Canadian company, on January 4, 2011. On the date of purchase, the exchange rate for 1 Canadian dollar was U.S. $0.79. Canadian Metal Products balance sheet on the date of purchase is shown below:

Required:

Prepare a translated balance sheet as of January 4, 2011.

Required:

Prepare a translated balance sheet as of January 4, 2011.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

58

Domingo Company, a U.S. company, owns a 100% interest in its subsidiary, Pavarotti, S.A., located in Italy. Pavarotti, S.A., began operations on January 1, 2011. The subsidiary's operations consist of leasing space in an office building. The building, which cost one million euros, was financed primarily by Italian banks. All revenues and expenses are received and paid in euros. The subsidiary also maintains its accounting records in euros. In light of these facts, management of the U.S. parent has determined that the euro is the functional currency of the subsidiary.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below, in euros:

The following are relevant exchange rates for the year 2011:

€1 = $1.50 at the beginning of 2011, at which time the common stock

was issued and the land and building were financed by the mortgage.

€1 = $1.55 weighted average for 2011.

€1 = $1.58 at the date the dividends were declared and paid and

the unearned rent was received.

€1 = $1.62 at the end of 2011.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended.

The subsidiary's balance sheet at December 31, 2011, and income statement for the year then ended, are presented below, in euros:

The following are relevant exchange rates for the year 2011:

€1 = $1.50 at the beginning of 2011, at which time the common stock

was issued and the land and building were financed by the mortgage.

€1 = $1.55 weighted average for 2011.

€1 = $1.58 at the date the dividends were declared and paid and

the unearned rent was received.

€1 = $1.62 at the end of 2011.

Required:

Prepare in U.S. dollars a balance sheet at December 31, 2011, and an income statement for the year then ended.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

59

The proper analysis of foreign operations by financial statement users requires that financial statements of the foreign operations be expressed in a common currency. For a U.S. company with a French subsidiary, this means converting the subsidiary's financial statements from francs to U.S. dollars.

One of the major issues in translating the financial statements of a foreign branch, division, or subsidiary is determining the functional currency of the foreign entity. The term "functional currency" has been defined by the Financial Accounting Standards Boards (FASB) as the currency of the primary economic environment in which the entity operates; normally, the currency of the environment in which the entity primarily generates and expends cash. Although the definition may seem relatively straightforward, the Financial Accounting Standards Board found it necessary to list various factors to guide management in determining the functional currency.

Required:

Identify the factors FASB identified that might be helpful in making the functional currency decision.

One of the major issues in translating the financial statements of a foreign branch, division, or subsidiary is determining the functional currency of the foreign entity. The term "functional currency" has been defined by the Financial Accounting Standards Boards (FASB) as the currency of the primary economic environment in which the entity operates; normally, the currency of the environment in which the entity primarily generates and expends cash. Although the definition may seem relatively straightforward, the Financial Accounting Standards Board found it necessary to list various factors to guide management in determining the functional currency.

Required:

Identify the factors FASB identified that might be helpful in making the functional currency decision.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following statements regarding international accounting standards for the impairment of tangible assets is correct?

A) Impairment losses cannot be subsequently reversed.

B) Impairment losses can be subsequently reversed to the extent of the amount of the initial impairment loss.

C) International accounting standards require a two-step test of impairment of a tangible asset.

D) Accounting for impairments is not necessary since entities are required under international accounting standards to adjust the values of property, plant, and equipment to fair value at the end of each reporting period for which reports are prepared.

A) Impairment losses cannot be subsequently reversed.

B) Impairment losses can be subsequently reversed to the extent of the amount of the initial impairment loss.

C) International accounting standards require a two-step test of impairment of a tangible asset.

D) Accounting for impairments is not necessary since entities are required under international accounting standards to adjust the values of property, plant, and equipment to fair value at the end of each reporting period for which reports are prepared.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 60 flashcards in this deck.