Deck 9: Competitive Markets

Full screen (f)

Question

Question

Question

Question

Question

Question

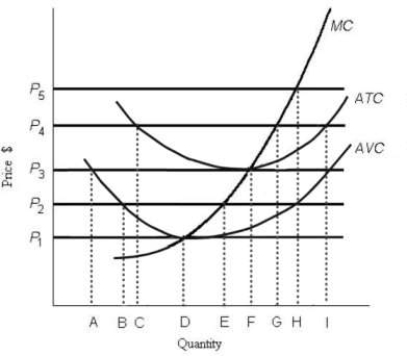

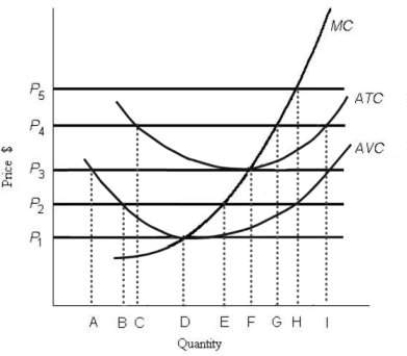

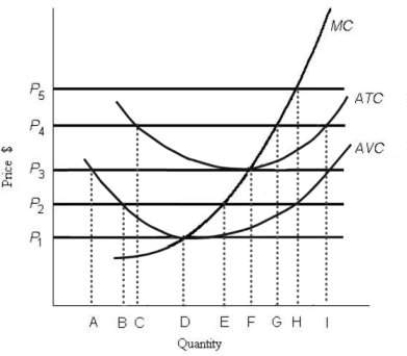

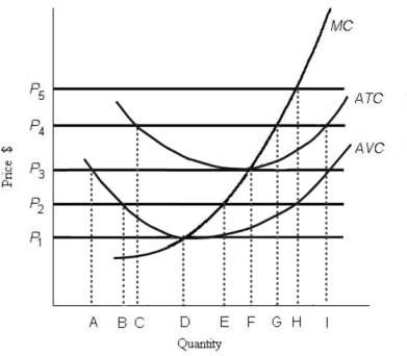

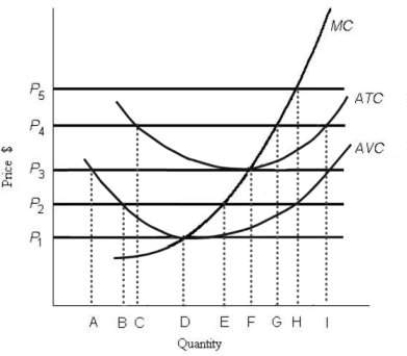

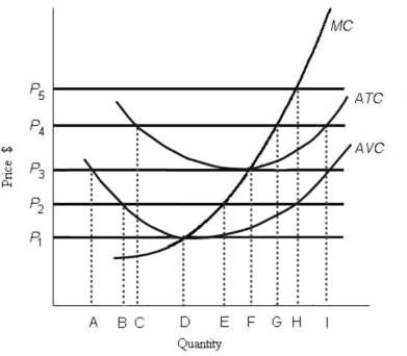

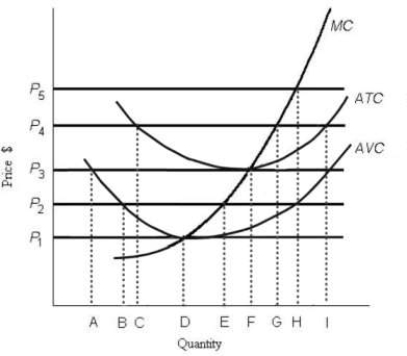

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P2, the profit- maximizing firm in the short run should

A) produce output B.

B) produce output C.

C) produce output D.

D) produce output E.

E) shut down, as it is incurring losses.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P2, the profit- maximizing firm in the short run should

A) produce output B.

B) produce output C.

C) produce output D.

D) produce output E.

E) shut down, as it is incurring losses.

Question

Question

Question

Question

Question

Question

Question

Question

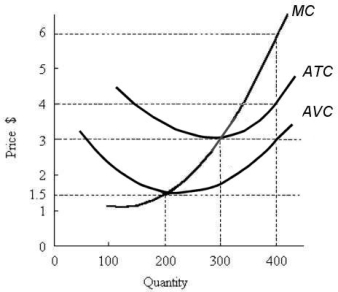

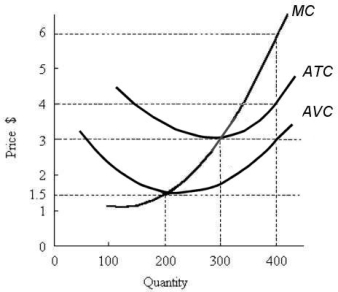

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 2

FIGURE 9- 2

Refer to Figure 9- 2. If the current market price is $6, the profit- maximizing output for this firm is

A) 100 units.

B) 200 units.

C) 300 units.

D) 400 units.

E) 500 units.

FIGURE 9- 2Refer to Figure 9- 2. If the current market price is $6, the profit- maximizing output for this firm is

A) 100 units.

B) 200 units.

C) 300 units.

D) 400 units.

E) 500 units.

Question

Question

Question

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The price at which the firm earns zero economic profits is

A) P3.

B) P2.

C) P5.

D) P1.

E) P4.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The price at which the firm earns zero economic profits is

A) P3.

B) P2.

C) P5.

D) P1.

E) P4.

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The firm's short- run supply curve starts at output and rises along the marginal cost (MC) curve.

A) D

B) E

C) F

D) G

E) H

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The firm's short- run supply curve starts at output and rises along the marginal cost (MC) curve.

A) D

B) E

C) F

D) G

E) H

Question

Question

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P3, the profit- maximizing firm in the short run should

A) produce output A.

B) produce output F or shut down, as it doesn't matter which.

C) produce output D.

D) shut down because more profits could be earned in another industry.

E) produce output F.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P3, the profit- maximizing firm in the short run should

A) produce output A.

B) produce output F or shut down, as it doesn't matter which.

C) produce output D.

D) shut down because more profits could be earned in another industry.

E) produce output F.

Question

Question

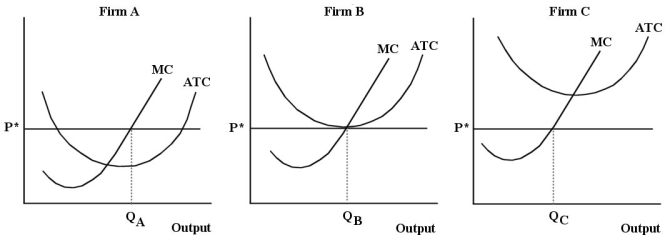

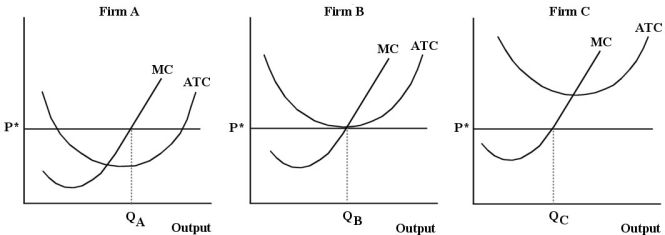

The diagram below shows the short- run cost curves for 3 perfectly competitive firms in the same industry.  FIGURE 9- 6

FIGURE 9- 6

Refer to Figure 9- 6. If Firms A, B and C are in the same industry, is this industry in long- run equilibrium?

A) Yes, because P = MC = MR for each of the 3 firms.

B) Yes, because each of the 3 firms is operating at its minimum efficient scale.

C) No, because if the industry were in equilibrium, all 3 firms would be earning zero economic profits.

D) No, because Firm A is not producing at a profit- maximizing level of output.

E) Yes, because all 3 firms are producing at their minimum average total cost.

FIGURE 9- 6Refer to Figure 9- 6. If Firms A, B and C are in the same industry, is this industry in long- run equilibrium?

A) Yes, because P = MC = MR for each of the 3 firms.

B) Yes, because each of the 3 firms is operating at its minimum efficient scale.

C) No, because if the industry were in equilibrium, all 3 firms would be earning zero economic profits.

D) No, because Firm A is not producing at a profit- maximizing level of output.

E) Yes, because all 3 firms are producing at their minimum average total cost.

Question

Question

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The short- run shut down price for the firm is

A) P2.

B) P5.

C) P1.

D) P4.

E) P3.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The short- run shut down price for the firm is

A) P2.

B) P5.

C) P1.

D) P4.

E) P3.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 2

FIGURE 9- 2

Refer to Figure 9- 2. If the market price is $1, the firm will produce _ _ units of output in the short run.

A) 0

B) 100

C) 200

D) 300

E) 400

FIGURE 9- 2Refer to Figure 9- 2. If the market price is $1, the firm will produce _ _ units of output in the short run.

A) 0

B) 100

C) 200

D) 300

E) 400

Question

Question

The diagram below shows the short- run cost curves for 3 perfectly competitive firms in the same industry.  FIGURE 9- 6

FIGURE 9- 6

Refer to Figure 9- 6. Which of the following statements about Firms A, B and C is true?

A) Firm A is earning profits, Firm B is breaking even, and Firm C is suffering losses.

B) Firms A, B and C are earning profits.

C) Firm A is breaking even, Firm B is suffering losses, and Firm C is earning profits.

D) Firm A is suffering losses, Firm B is breaking even, and Firm C is earning profits.

E) Firms A, B and C are breaking even.

FIGURE 9- 6Refer to Figure 9- 6. Which of the following statements about Firms A, B and C is true?

A) Firm A is earning profits, Firm B is breaking even, and Firm C is suffering losses.

B) Firms A, B and C are earning profits.

C) Firm A is breaking even, Firm B is suffering losses, and Firm C is earning profits.

D) Firm A is suffering losses, Firm B is breaking even, and Firm C is earning profits.

E) Firms A, B and C are breaking even.

Question

Question

Question

Question

Question

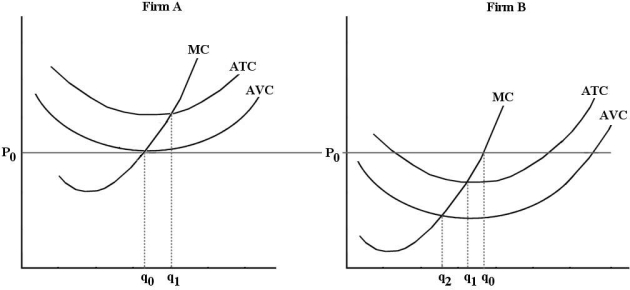

Consider the following cost curves for two perfectly competitive firms, A and B.  FIGURE 9- 4

FIGURE 9- 4

Refer to Figure 9- 4. Firms A and B are in the same industry. Choose the statement that best describes the situation facing the two firms.

A) Firm A and Firm B are both suffering economic losses and will soon exit the industry.

B) Firm A is making losses but remains producing as long as price falls no further; Firm B is producing at lower cost and is earning economic profits.

C) Firm A and Firm B are both earning positive economic profits; new firms will likely enter the industry.

D) Firm A is suffering losses and will be shut down immediately; Firm B will be shut down if the price falls any further.

FIGURE 9- 4Refer to Figure 9- 4. Firms A and B are in the same industry. Choose the statement that best describes the situation facing the two firms.

A) Firm A and Firm B are both suffering economic losses and will soon exit the industry.

B) Firm A is making losses but remains producing as long as price falls no further; Firm B is producing at lower cost and is earning economic profits.

C) Firm A and Firm B are both earning positive economic profits; new firms will likely enter the industry.

D) Firm A is suffering losses and will be shut down immediately; Firm B will be shut down if the price falls any further.

Question

Question

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. This perfectly competitive firm would incur economic losses at prices below

A) P1.

B) P2.

C) P3.

D) P4.

E) P5.

FIGURE 9- 1Refer to Figure 9- 1. This perfectly competitive firm would incur economic losses at prices below

A) P1.

B) P2.

C) P3.

D) P4.

E) P5.

Question

Question

Question

Consider the following cost curves for Firm X, a perfectly competitive firm.  FIGURE 9- 3

FIGURE 9- 3

Refer to Figure 9- 3. In this industry, which one of the following is FALSE?

A) If the scale of Firm X at output Q2 and price P2 is large enough that Firm X has an appreciable share of the market, Firm X will no longer be a price taker.

B) If the price were to fall below P2, firms would leave the industry.

C) At output Q2 and price P2, Firm X is maximizing its long- run profits.

D) If the price were to rise above P2, new firms would enter the industry.

E) Only one firm can reach the size of output Q2.

FIGURE 9- 3Refer to Figure 9- 3. In this industry, which one of the following is FALSE?

A) If the scale of Firm X at output Q2 and price P2 is large enough that Firm X has an appreciable share of the market, Firm X will no longer be a price taker.

B) If the price were to fall below P2, firms would leave the industry.

C) At output Q2 and price P2, Firm X is maximizing its long- run profits.

D) If the price were to rise above P2, new firms would enter the industry.

E) Only one firm can reach the size of output Q2.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

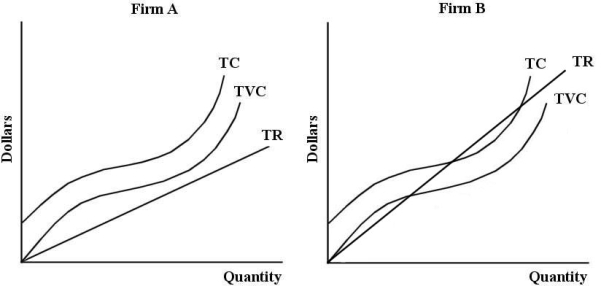

Consider the total cost and revenue curves shown below, for two perfectly competitive firms, Firm A and Firm B.  FIGURE 9- 5

FIGURE 9- 5

Refer to Figure 9- 5. Given its total cost and revenue curves, Firm B should

A) shut down temporarily.

B) maximize its profits by producing that level of output such that the slope of the TVC curve is equal to the slope of the TR curve.

C) produce the level of output where the TC curve intersects the TR curve.

D) maximize its profits by producing that level of output such that the slope of the TC curve is equal to the slope of the TR curve.

E) exit the industry.

FIGURE 9- 5Refer to Figure 9- 5. Given its total cost and revenue curves, Firm B should

A) shut down temporarily.

B) maximize its profits by producing that level of output such that the slope of the TVC curve is equal to the slope of the TR curve.

C) produce the level of output where the TC curve intersects the TR curve.

D) maximize its profits by producing that level of output such that the slope of the TC curve is equal to the slope of the TR curve.

E) exit the industry.

Question

Question

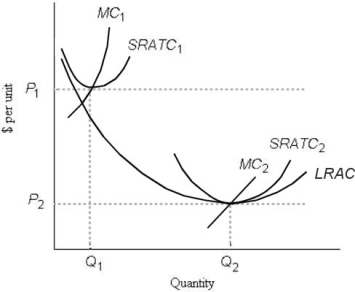

Consider the following cost curves for Firm X, a perfectly competitive firm.  FIGURE 9- 3

FIGURE 9- 3

Refer to Figure 9- 3. If Firm X has a capital stock that generates SRATC1, then in the long run Firm X will have to

A) maintain its output level at Q1, because it is maximizing its short- run profits.

B) set its output at Q1 with an expanded plant size.

C) set its output at Q1 with the existing plant size.

D) expand its output to Q2 with the existing plant size.

E) either expand its plant size or exit from the industry.

FIGURE 9- 3Refer to Figure 9- 3. If Firm X has a capital stock that generates SRATC1, then in the long run Firm X will have to

A) maintain its output level at Q1, because it is maximizing its short- run profits.

B) set its output at Q1 with an expanded plant size.

C) set its output at Q1 with the existing plant size.

D) expand its output to Q2 with the existing plant size.

E) either expand its plant size or exit from the industry.

Question

Consider the following short- run cost curves for a perfectly competitive firm.  FIGURE 9- 1

FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P4, the profit- maximizing firm in the short run should produce output

A) C.

B) F.

C) G.

D) H.

E) I.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P4, the profit- maximizing firm in the short run should produce output

A) C.

B) F.

C) G.

D) H.

E) I.

Question

Question

Consider the total cost and revenue curves shown below, for two perfectly competitive firms, Firm A and Firm B.  FIGURE 9- 5

FIGURE 9- 5

Refer to Figure 9- 5. If both Firms A and B are producing a level of output such that the slope of the TC curve is equal to the slope of the TR curve,

A) then both firms are earning positive economic profits because the distance between TR and TC is the greatest.

B) then both firms are suffering losses because the distance between TR and TC is the smallest.

C) then MC = MR and the firm is maximizing profit (or minimizing losses).

D) then MC = MR but the firm may not be maximizing its profits.

E) then the ATC is at a minimum and the firm is maximizing profits.

FIGURE 9- 5Refer to Figure 9- 5. If both Firms A and B are producing a level of output such that the slope of the TC curve is equal to the slope of the TR curve,

A) then both firms are earning positive economic profits because the distance between TR and TC is the greatest.

B) then both firms are suffering losses because the distance between TR and TC is the smallest.

C) then MC = MR and the firm is maximizing profit (or minimizing losses).

D) then MC = MR but the firm may not be maximizing its profits.

E) then the ATC is at a minimum and the firm is maximizing profits.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/125

Play

Full screen (f)

Deck 9: Competitive Markets

1

In long- run equilibrium, a perfectly competitive firm has

A) P = MC = minimum short- run ATC = minimum long- run AC.

B) a highly differentiated product.

C) successfully established barriers to entry.

D) large economic profits.

E) a strong profit incentive to expand capacity.

A) P = MC = minimum short- run ATC = minimum long- run AC.

B) a highly differentiated product.

C) successfully established barriers to entry.

D) large economic profits.

E) a strong profit incentive to expand capacity.

A

2

Assume the following total cost schedule for a perfectly competitive firm.

-Refer to Table 9- 2. If the market price were $71, the competitive firm wishing to maximize its profits would

A) not produce because P < minimum of ATC.

B) not produce because P < TFC.

C) produce 6 units of output.

D) produce 2 units of output.

E) produce 5 units of output.

-Refer to Table 9- 2. If the market price were $71, the competitive firm wishing to maximize its profits would

A) not produce because P < minimum of ATC.

B) not produce because P < TFC.

C) produce 6 units of output.

D) produce 2 units of output.

E) produce 5 units of output.

produce 5 units of output.

3

Which of the following statements is one of the assumptions of the theory of perfect competition?

A) Firms produce a wide variety of versions of the product.

B) Firms are price setters.

C) Consumers know the prices charged by each firm.

D) A firm's entry to the market is regulated by the federal Competition Bureau.

E) Firms compete with each other by varying their price.

A) Firms produce a wide variety of versions of the product.

B) Firms are price setters.

C) Consumers know the prices charged by each firm.

D) A firm's entry to the market is regulated by the federal Competition Bureau.

E) Firms compete with each other by varying their price.

C

4

In order to decide the appropriate output to produce, the manager of a perfectly competitive firm needs to know

A) the prevailing market price for the firm's output.

B) what other firms in the industry are producing.

C) the industry or market demand.

D) the industry or market supply.

E) its competitors' market strategies.

A) the prevailing market price for the firm's output.

B) what other firms in the industry are producing.

C) the industry or market demand.

D) the industry or market supply.

E) its competitors' market strategies.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

5

A firm in a perfectly competitive industry

A) will maximize its profit by producing where P = ATC.

B) will not produce at all if P < the minimum of AVC.

C) can improve its competitive position and sell more output by advertising its product.

D) will not produce at all if P < ATC.

E) will maximize its profit by producing where P = AVC.

A) will maximize its profit by producing where P = ATC.

B) will not produce at all if P < the minimum of AVC.

C) can improve its competitive position and sell more output by advertising its product.

D) will not produce at all if P < ATC.

E) will maximize its profit by producing where P = AVC.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

6

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P2, the profit- maximizing firm in the short run should

A) produce output B.

B) produce output C.

C) produce output D.

D) produce output E.

E) shut down, as it is incurring losses.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P2, the profit- maximizing firm in the short run should

A) produce output B.

B) produce output C.

C) produce output D.

D) produce output E.

E) shut down, as it is incurring losses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

7

A firm in a perfectly competitive market

A) is aware of its competitors' costs.

B) is dependant upon the behaviour of its competitors.

C) competes actively with other sellers in the industry.

D) has no power to influence the market price.

E) is limited in the amount of product it can sell without affecting the price.

A) is aware of its competitors' costs.

B) is dependant upon the behaviour of its competitors.

C) competes actively with other sellers in the industry.

D) has no power to influence the market price.

E) is limited in the amount of product it can sell without affecting the price.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

8

Consider the price and quantity data below for a perfectly competitive firm producing mousetraps.

-Refer to Table 9- 1. Suppose this firm is producing 1250 mousetraps and its average total cost is $4 per unit. The firm will be

A) suffering losses of $5000.

B) earning profits of $1250.

C) earning profits of $5000.

D) suffering losses of $1250.

E) breaking even.

-Refer to Table 9- 1. Suppose this firm is producing 1250 mousetraps and its average total cost is $4 per unit. The firm will be

A) suffering losses of $5000.

B) earning profits of $1250.

C) earning profits of $5000.

D) suffering losses of $1250.

E) breaking even.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

9

Suppose a perfectly competitive industry is in long- run equilibrium. A new one- time cost- saving technology is then developed and new plants are built. Eventually, a new long- run equilibrium will be established where

A) new plants employ the new technology, but existing plants continue to produce as long as they cover their fixed costs.

B) all plants use the new technology, and market output will be higher.

C) high- cost and low- cost firms exist side by side and market output will be higher.

D) all plants continue to operate until they are physically worn out as long as price is greater than the the firm's average variable cost.

E) the industry supply curve has shifted to the left and price and output are both higher.

A) new plants employ the new technology, but existing plants continue to produce as long as they cover their fixed costs.

B) all plants use the new technology, and market output will be higher.

C) high- cost and low- cost firms exist side by side and market output will be higher.

D) all plants continue to operate until they are physically worn out as long as price is greater than the the firm's average variable cost.

E) the industry supply curve has shifted to the left and price and output are both higher.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

10

Any firm's average revenue is defined as

A) the total amount received by the seller from the sale of a product.

B) the change in total revenue resulting from the sale of an additional unit of the product.

C) price times quantity of the product sold.

D) the change in price resulting from the sale of an additional unit of the product.

E) total revenue divided by the number of units sold.

A) the total amount received by the seller from the sale of a product.

B) the change in total revenue resulting from the sale of an additional unit of the product.

C) price times quantity of the product sold.

D) the change in price resulting from the sale of an additional unit of the product.

E) total revenue divided by the number of units sold.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

11

Suppose a paper mill in Quebec is shut down by its owner, even though the plant and equipment are in excellent shape and the paper is of top quality. What could explain this?

A) The price the firm is receiving for the paper is less than its average variable cost.

B) The owner is minimizing its production costs.

C) The price the firm is receiving is less than the average total cost.

D) The price the firm is receiving for the paper is greater than its marginal cost.

E) The paper mill must not have been operating at its profit- maximizing level of output.

A) The price the firm is receiving for the paper is less than its average variable cost.

B) The owner is minimizing its production costs.

C) The price the firm is receiving is less than the average total cost.

D) The price the firm is receiving for the paper is greater than its marginal cost.

E) The paper mill must not have been operating at its profit- maximizing level of output.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

12

Consider the following total cost schedule for a perfectly competitive firm producing ball- point pens. TABLE 9- 3

-Refer to Table 9- 3. As this firm increases output from 40 units to 50 units per period, its marginal cost rises to

A) $0.10

B) $0.17

C) $0.375

D) $0.40

E) $0.50

-Refer to Table 9- 3. As this firm increases output from 40 units to 50 units per period, its marginal cost rises to

A) $0.10

B) $0.17

C) $0.375

D) $0.40

E) $0.50

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

13

When economists say that a perfectly competitive firm is a "quantity adjuster", they mean that

A) it can vary its output by an infinite amount.

B) changing the output level does not affect the costs of production.

C) its marginal- cost curve coincides with its own demand curve.

D) it is a price taker.

E) it is not concerned with cost factors.

A) it can vary its output by an infinite amount.

B) changing the output level does not affect the costs of production.

C) its marginal- cost curve coincides with its own demand curve.

D) it is a price taker.

E) it is not concerned with cost factors.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

14

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 2

Refer to Figure 9- 2. If the current market price is $6, the profit- maximizing output for this firm is

A) 100 units.

B) 200 units.

C) 300 units.

D) 400 units.

E) 500 units.

FIGURE 9- 2Refer to Figure 9- 2. If the current market price is $6, the profit- maximizing output for this firm is

A) 100 units.

B) 200 units.

C) 300 units.

D) 400 units.

E) 500 units.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

15

Average revenue (AR) for an individual firm in a perfectly competitive market equals

A) Oq/Op.

B) (p × q)/q.

C) Op × Oq.

D) p × q.

E) O(p × q)/Oq.

A) Oq/Op.

B) (p × q)/q.

C) Op × Oq.

D) p × q.

E) O(p × q)/Oq.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

16

Consider the price and quantity data below for a perfectly competitive firm producing mousetraps.

-Refer to Table 9- 1. Suppose this firm is producing 1500 mousetraps and its average total cost is

$5.10 per unit. The firm will be

A) suffering losses of $7650.

B) suffering losses of $150.

C) breaking even.

D) earning profits of $150.

E) earning profits of $7650.

-Refer to Table 9- 1. Suppose this firm is producing 1500 mousetraps and its average total cost is

$5.10 per unit. The firm will be

A) suffering losses of $7650.

B) suffering losses of $150.

C) breaking even.

D) earning profits of $150.

E) earning profits of $7650.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

17

Suppose that in a perfectly competitive industry, the market price of the product is $12. Firm A is producing the output level at which average total cost equals marginal cost, both of which are $10. To maximize its profits, Firm A should

A) increase its advertising.

B) change the price of the product.

C) reduce its output.

D) leave its output unchanged.

E) expand its output.

A) increase its advertising.

B) change the price of the product.

C) reduce its output.

D) leave its output unchanged.

E) expand its output.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

18

In the short run, the profit- maximizing behaviour for a price- taking firm requires it to operate where

A) P = MC, given that P is greater than or equal to AVC.

B) P = TR = TC.

C) P > MR > MC.

D) P = MC, given that P is greater than or equal to ATC.

E) AVC = AR.

A) P = MC, given that P is greater than or equal to AVC.

B) P = TR = TC.

C) P > MR > MC.

D) P = MC, given that P is greater than or equal to ATC.

E) AVC = AR.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

19

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The price at which the firm earns zero economic profits is

A) P3.

B) P2.

C) P5.

D) P1.

E) P4.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The price at which the firm earns zero economic profits is

A) P3.

B) P2.

C) P5.

D) P1.

E) P4.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

20

In a perfectly competitive market, smaller- than- efficient sized firms can exist in

A) both the short run and the long run, but they must reduce plant size to remain competitive.

B) both the short and long run.

C) the long run, and they will make positive economic profits.

D) the short run.

E) the long run.

A) both the short run and the long run, but they must reduce plant size to remain competitive.

B) both the short and long run.

C) the long run, and they will make positive economic profits.

D) the short run.

E) the long run.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

21

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The firm's short- run supply curve starts at output and rises along the marginal cost (MC) curve.

A) D

B) E

C) F

D) G

E) H

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The firm's short- run supply curve starts at output and rises along the marginal cost (MC) curve.

A) D

B) E

C) F

D) G

E) H

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

22

Consider the price and quantity data below for a perfectly competitive firm producing mousetraps.

-Refer to Table 9- 1. If this firm is producing 1250 mousetraps, its total revenue is , its average revenue is and its marginal revenue is .

A) $5; $5; $5

B) $6250; $250; $5

C) $6250; $5; $5

D) $5000; $5; $250

E) $1750; $250; $5

-Refer to Table 9- 1. If this firm is producing 1250 mousetraps, its total revenue is , its average revenue is and its marginal revenue is .

A) $5; $5; $5

B) $6250; $250; $5

C) $6250; $5; $5

D) $5000; $5; $250

E) $1750; $250; $5

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

23

Given the usual assumptions about perfect competition, a perfectly competitive firm

A) can affect the market conditions in a significant way.

B) can set the price it charges.

C) competes actively with other sellers in the industry.

D) can sell as much of its product as it wishes at the market price.

E) is aware of its competitors' costs.

A) can affect the market conditions in a significant way.

B) can set the price it charges.

C) competes actively with other sellers in the industry.

D) can sell as much of its product as it wishes at the market price.

E) is aware of its competitors' costs.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

24

The market demand curve for a perfectly competitive industry is typically

A) upward sloping.

B) identical to the competitive firm's demand curve.

C) infinitely elastic.

D) a rectangular hyperbola.

E) downward sloping.

A) upward sloping.

B) identical to the competitive firm's demand curve.

C) infinitely elastic.

D) a rectangular hyperbola.

E) downward sloping.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

25

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P3, the profit- maximizing firm in the short run should

A) produce output A.

B) produce output F or shut down, as it doesn't matter which.

C) produce output D.

D) shut down because more profits could be earned in another industry.

E) produce output F.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P3, the profit- maximizing firm in the short run should

A) produce output A.

B) produce output F or shut down, as it doesn't matter which.

C) produce output D.

D) shut down because more profits could be earned in another industry.

E) produce output F.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

26

For a perfectly competitive firm in long- run profit- maximizing equilibrium,

A) marginal revenue is greater than marginal cost.

B) price is greater than marginal cost.

C) economic profits are greater than zero.

D) average fixed costs are at the maximum.

E) price equals minimum short- run and long- run average total cost.

A) marginal revenue is greater than marginal cost.

B) price is greater than marginal cost.

C) economic profits are greater than zero.

D) average fixed costs are at the maximum.

E) price equals minimum short- run and long- run average total cost.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

27

The diagram below shows the short- run cost curves for 3 perfectly competitive firms in the same industry. FIGURE 9- 6

Refer to Figure 9- 6. If Firms A, B and C are in the same industry, is this industry in long- run equilibrium?

A) Yes, because P = MC = MR for each of the 3 firms.

B) Yes, because each of the 3 firms is operating at its minimum efficient scale.

C) No, because if the industry were in equilibrium, all 3 firms would be earning zero economic profits.

D) No, because Firm A is not producing at a profit- maximizing level of output.

E) Yes, because all 3 firms are producing at their minimum average total cost.

FIGURE 9- 6Refer to Figure 9- 6. If Firms A, B and C are in the same industry, is this industry in long- run equilibrium?

A) Yes, because P = MC = MR for each of the 3 firms.

B) Yes, because each of the 3 firms is operating at its minimum efficient scale.

C) No, because if the industry were in equilibrium, all 3 firms would be earning zero economic profits.

D) No, because Firm A is not producing at a profit- maximizing level of output.

E) Yes, because all 3 firms are producing at their minimum average total cost.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

28

The short- run supply curve for a perfectly competitive firm is

A) its entire marginal- cost curve.

B) its marginal- cost curve above the average- variable- cost curve.

C) the industry supply curve.

D) its average- revenue curve.

E) its rising portion of the average- variable- cost curve.

A) its entire marginal- cost curve.

B) its marginal- cost curve above the average- variable- cost curve.

C) the industry supply curve.

D) its average- revenue curve.

E) its rising portion of the average- variable- cost curve.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

29

If firms in a competitive industry are earning positive economic profits, in the long run we expect

A) the individual firms will lower their price to discourage new firms from entering the industry.

B) the government would intervene and force the firms to lower prices.

C) the demand curve for the product will shift to the left, so that the price of the product will fall.

D) the supply curve for the product will shift to the right as new firms enter the industry, causing industry output to increase and price to fall.

E) there would be no change in the industry as long as P = MC for the individual firms.

A) the individual firms will lower their price to discourage new firms from entering the industry.

B) the government would intervene and force the firms to lower prices.

C) the demand curve for the product will shift to the left, so that the price of the product will fall.

D) the supply curve for the product will shift to the right as new firms enter the industry, causing industry output to increase and price to fall.

E) there would be no change in the industry as long as P = MC for the individual firms.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

30

When a firm is referred to as a "price taker",

A) the firm can alter its rate of production and sales without affecting the market price of the product.

B) the firm initially takes price as given and tries to influence it through advertising.

C) the demand curve that the firm faces is perfectly inelastic.

D) the firm can alter the market price as it changes its rate of production.

E) the firm will be willing to sell an infinite quantity at the market price.

A) the firm can alter its rate of production and sales without affecting the market price of the product.

B) the firm initially takes price as given and tries to influence it through advertising.

C) the demand curve that the firm faces is perfectly inelastic.

D) the firm can alter the market price as it changes its rate of production.

E) the firm will be willing to sell an infinite quantity at the market price.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

31

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The short- run shut down price for the firm is

A) P2.

B) P5.

C) P1.

D) P4.

E) P3.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. The short- run shut down price for the firm is

A) P2.

B) P5.

C) P1.

D) P4.

E) P3.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

32

A perfectly competitive firm is currently producing an output level where price is $10.00, average variable cost is $6.00, average total cost is $10.00, and marginal cost is $8.00. In order to maximize profits, this firm should

A) decrease its output.

B) increase the market price.

C) shut down.

D) increase its output.

E) not change its output -- this firm is at its profit- maximizing position.

A) decrease its output.

B) increase the market price.

C) shut down.

D) increase its output.

E) not change its output -- this firm is at its profit- maximizing position.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

33

In the short run, a profit- maximizing firm will expand output

A) until total revenue equals total cost.

B) as long as marginal revenue is greater than marginal cost.

C) until marginal revenue equals average variable cost.

D) as long as marginal cost is greater than marginal revenue.

E) until marginal cost begins to rise.

A) until total revenue equals total cost.

B) as long as marginal revenue is greater than marginal cost.

C) until marginal revenue equals average variable cost.

D) as long as marginal cost is greater than marginal revenue.

E) until marginal cost begins to rise.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

34

Suppose a perfectly competitive firm is producing a level of output for which price equals average total cost, and average total cost is less than marginal cost. In order to maximize its profits, the firm should

A) shut down.

B) not change its output.

C) reduce its output.

D) increase the market price.

E) expand its output.

A) shut down.

B) not change its output.

C) reduce its output.

D) increase the market price.

E) expand its output.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

35

The supply curve for a perfectly competitive industry is the horizontal summation of the individual firms'

A) MC curves above AVC.

B) MC curves above ATC.

C) short- run average cost curves.

D) MC curves above AFC.

E) AVC curves above MC.

A) MC curves above AVC.

B) MC curves above ATC.

C) short- run average cost curves.

D) MC curves above AFC.

E) AVC curves above MC.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

36

Comparing the short- run and long- run profit- maximizing positions of a perfectly competitive firm, which statement is true?

A) The firm may have unexploited economies of scale in both the short run and the long run.

B) Price will equal marginal cost in the short run, but not necessarily in the long run.

C) Price should equal average cost in the long run, but not necessarily in the short run.

D) The firm will produce at minimum average cost in both the short and long run.

E) Economic profit may exist in the short run and in the long run.

A) The firm may have unexploited economies of scale in both the short run and the long run.

B) Price will equal marginal cost in the short run, but not necessarily in the long run.

C) Price should equal average cost in the long run, but not necessarily in the short run.

D) The firm will produce at minimum average cost in both the short and long run.

E) Economic profit may exist in the short run and in the long run.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

37

Assume the following total cost schedule for a perfectly competitive firm.

-Refer to Table 9- 2. At what price would a profit- maximizing firm earn zero economic profits?

A) $40.

B) $70.

C) $145.

D) $220.

E) $430.

-Refer to Table 9- 2. At what price would a profit- maximizing firm earn zero economic profits?

A) $40.

B) $70.

C) $145.

D) $220.

E) $430.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

38

In the long run it is not possible for a perfectly competitive firm to

A) alter its plant size.

B) set the product price.

C) adjust its output.

D) replace its antiquated equipment.

E) adopt new technology.

A) alter its plant size.

B) set the product price.

C) adjust its output.

D) replace its antiquated equipment.

E) adopt new technology.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following producers operate in a market structure closely approximated by perfect competition?

A) A Safeway grocery store

B) A Saskatchewan wheat farmer

C) The Bank of Montreal

D) A restaurant in your neighbourhood

E) Air Canada

A) A Safeway grocery store

B) A Saskatchewan wheat farmer

C) The Bank of Montreal

D) A restaurant in your neighbourhood

E) Air Canada

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

40

The price elasticity of demand faced by an individual wheat farmer would come closest to which following value?

A) 0.00007.

B) 0.7.

C) 1.0.

D) 71.0.

E) 71 000.

A) 0.00007.

B) 0.7.

C) 1.0.

D) 71.0.

E) 71 000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

41

If a perfectly competitive firm in the short run is producing where P = ATC = MC, this firm is

A) on the downward- sloping portion of its demand curve.

B) at its profit- maximizing output level.

C) earning economic profits.

D) incurring losses.

E) obliged to shut down.

A) on the downward- sloping portion of its demand curve.

B) at its profit- maximizing output level.

C) earning economic profits.

D) incurring losses.

E) obliged to shut down.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

42

Consider the following total cost schedule for a perfectly competitive firm producing ball- point pens.

-Refer to Table 9- 3. Suppose the prevailing market price for this firm's product is $0.40 and the firm produces its profit- maximizing level of output. At this price

A) the firm is suffering economic losses and this firm will exit the industry.

B) the firm should decrease output.

C) the firm is earning positive economic profits.

D) the firm is earning zero economic profits.

E) the firm should increase output.

-Refer to Table 9- 3. Suppose the prevailing market price for this firm's product is $0.40 and the firm produces its profit- maximizing level of output. At this price

A) the firm is suffering economic losses and this firm will exit the industry.

B) the firm should decrease output.

C) the firm is earning positive economic profits.

D) the firm is earning zero economic profits.

E) the firm should increase output.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

43

Which following statement does NOT apply to a perfectly competitive market?

A) Consumers prefer certain brands over others.

B) Consumers can shop for the lowest available price.

C) All firms in the industry are price takers.

D) There is freedom of entry and exit of firms in the industry.

E) All firms have realized the possible economies of scale.

A) Consumers prefer certain brands over others.

B) Consumers can shop for the lowest available price.

C) All firms in the industry are price takers.

D) There is freedom of entry and exit of firms in the industry.

E) All firms have realized the possible economies of scale.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

44

In economics, perfect competition refers to a market structure where

A) firms co- operate with each other.

B) firms can set the price of their product.

C) all firms are earning profits.

D) each firm has zero market power.

E) firms behave strategically.

A) firms co- operate with each other.

B) firms can set the price of their product.

C) all firms are earning profits.

D) each firm has zero market power.

E) firms behave strategically.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following terms would best describe the price elasticity of demand facing a perfectly competitive firm?

A) perfectly inelastic

B) inelastic

C) elastic

D) perfectly elastic

E) unit

A) perfectly inelastic

B) inelastic

C) elastic

D) perfectly elastic

E) unit

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

46

The conditions for a perfectly competitive market include which one of the following?

A) Firms can control prices.

B) New entrants cannot threaten the position of existing firms.

C) Firms must employ the newest technologies as soon as they are developed.

D) Firms behave as price takers.

E) Profits are zero in the short run.

A) Firms can control prices.

B) New entrants cannot threaten the position of existing firms.

C) Firms must employ the newest technologies as soon as they are developed.

D) Firms behave as price takers.

E) Profits are zero in the short run.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

47

Suppose your trucking firm in a perfectly competitive industry is making zero economic profits in the short run. The federal government imposes a new safety regulation that affects all firms, thus shifting the marginal cost curve upward. As a result your firm's profit maximizing short- run output will

A) increase as price rises in the long run.

B) decrease because the new MC curve will intersect the horizontal demand curve at a lower rate of output.

C) remain the same because you will pass on the extra costs to the consumers.

D) increase as firms will leave the industry at the higher costs, thus driving up the market price.

E) remain the same since the new regulation does not affect ATC.

A) increase as price rises in the long run.

B) decrease because the new MC curve will intersect the horizontal demand curve at a lower rate of output.

C) remain the same because you will pass on the extra costs to the consumers.

D) increase as firms will leave the industry at the higher costs, thus driving up the market price.

E) remain the same since the new regulation does not affect ATC.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

48

When economists say that a firm is a price taker they mean that

A) the demand curve that the firm faces is perfectly inelastic.

B) the firm can alter the market price as it changes its rate of production.

C) the firm initially takes price as given and tries to influence it through advertising.

D) at the price prevailing in the market, the firm will be willing to sell an infinite quantity.

E) the firm can alter its rate of production and sales without affecting the market price of the product.

A) the demand curve that the firm faces is perfectly inelastic.

B) the firm can alter the market price as it changes its rate of production.

C) the firm initially takes price as given and tries to influence it through advertising.

D) at the price prevailing in the market, the firm will be willing to sell an infinite quantity.

E) the firm can alter its rate of production and sales without affecting the market price of the product.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

49

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 2

Refer to Figure 9- 2. If the market price is $1, the firm will produce _ _ units of output in the short run.

A) 0

B) 100

C) 200

D) 300

E) 400

FIGURE 9- 2Refer to Figure 9- 2. If the market price is $1, the firm will produce _ _ units of output in the short run.

A) 0

B) 100

C) 200

D) 300

E) 400

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

50

If a perfectly competitive firm produces at an output level where marginal cost equals marginal revenue, then

A) the difference between TR and TC is zero.

B) the firm should shut down.

C) the firm is maximizing its revenue.

D) there is no reason to reduce or expand output, as long as AVC is greater than or equal to price.

E) the last unit produced adds the same amount to costs as it does to revenue.

A) the difference between TR and TC is zero.

B) the firm should shut down.

C) the firm is maximizing its revenue.

D) there is no reason to reduce or expand output, as long as AVC is greater than or equal to price.

E) the last unit produced adds the same amount to costs as it does to revenue.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

51

The diagram below shows the short- run cost curves for 3 perfectly competitive firms in the same industry. FIGURE 9- 6

Refer to Figure 9- 6. Which of the following statements about Firms A, B and C is true?

A) Firm A is earning profits, Firm B is breaking even, and Firm C is suffering losses.

B) Firms A, B and C are earning profits.

C) Firm A is breaking even, Firm B is suffering losses, and Firm C is earning profits.

D) Firm A is suffering losses, Firm B is breaking even, and Firm C is earning profits.

E) Firms A, B and C are breaking even.

FIGURE 9- 6Refer to Figure 9- 6. Which of the following statements about Firms A, B and C is true?

A) Firm A is earning profits, Firm B is breaking even, and Firm C is suffering losses.

B) Firms A, B and C are earning profits.

C) Firm A is breaking even, Firm B is suffering losses, and Firm C is earning profits.

D) Firm A is suffering losses, Firm B is breaking even, and Firm C is earning profits.

E) Firms A, B and C are breaking even.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

52

If the demand curve faced by a firm is downward sloping, we can reasonably believe that the

A) firm can influence the price of the product it sells.

B) firm will have no effect on the price of the product it sells.

C) firm's contributions to total output of the product is insignificant.

D) firm has no control over the price of the product it sells but can vary the output.

E) firm must lower prices if it hopes to increase its profits.

A) firm can influence the price of the product it sells.

B) firm will have no effect on the price of the product it sells.

C) firm's contributions to total output of the product is insignificant.

D) firm has no control over the price of the product it sells but can vary the output.

E) firm must lower prices if it hopes to increase its profits.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

53

Assume the following total cost schedule for a perfectly competitive firm.

-Refer to Table 9- 2. The profit- maximizing firm would shut down in the short run if the market price of its output dropped below

A) $35.

B) $40.

C) $70.

D) $90.

E) $100.

-Refer to Table 9- 2. The profit- maximizing firm would shut down in the short run if the market price of its output dropped below

A) $35.

B) $40.

C) $70.

D) $90.

E) $100.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

54

Assume the following total cost schedule for a perfectly competitive firm.

-Refer to Table 9- 2. If the firm is producing at an output level of 2 units, the ATC is _ and the AVC is _ .

A) $85; $35

B) $100; $70

C) $70; $35

D) $50; $50

E) $140; $40

-Refer to Table 9- 2. If the firm is producing at an output level of 2 units, the ATC is _ and the AVC is _ .

A) $85; $35

B) $100; $70

C) $70; $35

D) $50; $50

E) $140; $40

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following conditions is true of a perfectly competitive industry when it is in long- run equilibrium?

A) Accounting profits for all firms are zero.

B) Firms are exiting the industry.

C) Price equals minimum short- run average total cost for all firms.

D) Firms are entering the industry.

E) Firms are experiencing increasing returns to scale.

A) Accounting profits for all firms are zero.

B) Firms are exiting the industry.

C) Price equals minimum short- run average total cost for all firms.

D) Firms are entering the industry.

E) Firms are experiencing increasing returns to scale.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

56

Consider the following cost curves for two perfectly competitive firms, A and B. FIGURE 9- 4

Refer to Figure 9- 4. Firms A and B are in the same industry. Choose the statement that best describes the situation facing the two firms.

A) Firm A and Firm B are both suffering economic losses and will soon exit the industry.

B) Firm A is making losses but remains producing as long as price falls no further; Firm B is producing at lower cost and is earning economic profits.

C) Firm A and Firm B are both earning positive economic profits; new firms will likely enter the industry.

D) Firm A is suffering losses and will be shut down immediately; Firm B will be shut down if the price falls any further.

FIGURE 9- 4Refer to Figure 9- 4. Firms A and B are in the same industry. Choose the statement that best describes the situation facing the two firms.

A) Firm A and Firm B are both suffering economic losses and will soon exit the industry.

B) Firm A is making losses but remains producing as long as price falls no further; Firm B is producing at lower cost and is earning economic profits.

C) Firm A and Firm B are both earning positive economic profits; new firms will likely enter the industry.

D) Firm A is suffering losses and will be shut down immediately; Firm B will be shut down if the price falls any further.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

57

For any firm operating in any market structure, marginal revenue is defined as

A) price times quantity of the product sold.

B) the total amount received by the seller from the sale of a product.

C) total revenue divided by the number of units sold.

D) the change in price resulting from the sale of an additional unit of the product.

E) the change in total revenue resulting from the sale of an additional unit of the product.

A) price times quantity of the product sold.

B) the total amount received by the seller from the sale of a product.

C) total revenue divided by the number of units sold.

D) the change in price resulting from the sale of an additional unit of the product.

E) the change in total revenue resulting from the sale of an additional unit of the product.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

58

Why will a perfectly competitive firm not sell its product below the prevailing market price?

A) It faces inelastic demand.

B) It can sell all it wishes at the market price.

C) This would lead to a price war among sellers.

D) The sellers in the market have agreed to not sell below a specified price.

E) Its costs would increase dramatically.

A) It faces inelastic demand.

B) It can sell all it wishes at the market price.

C) This would lead to a price war among sellers.

D) The sellers in the market have agreed to not sell below a specified price.

E) Its costs would increase dramatically.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

59

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. This perfectly competitive firm would incur economic losses at prices below

A) P1.

B) P2.

C) P3.

D) P4.

E) P5.

FIGURE 9- 1Refer to Figure 9- 1. This perfectly competitive firm would incur economic losses at prices below

A) P1.

B) P2.

C) P3.

D) P4.

E) P5.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

60

For a given market price, a competitive firm's average- revenue curve

A) increases to the right and then declines when MC = MR.

B) is the same as the firm's demand curve.

C) is a positively sloped straight line, starting from the origin.

D) is a straight line that coincides with the market demand curve.

E) is the same as the firm's TR curve.

A) increases to the right and then declines when MC = MR.

B) is the same as the firm's demand curve.

C) is a positively sloped straight line, starting from the origin.

D) is a straight line that coincides with the market demand curve.

E) is the same as the firm's TR curve.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

61

A perfectly competitive firm's demand curve

A) has unit elasticity.

B) is a horizontal line where P = AR = MR.

C) is identical to the market demand curve.

D) is downward sloping.

E) yields constant total revenues.

A) has unit elasticity.

B) is a horizontal line where P = AR = MR.

C) is identical to the market demand curve.

D) is downward sloping.

E) yields constant total revenues.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

62

Consider the following cost curves for Firm X, a perfectly competitive firm. FIGURE 9- 3

Refer to Figure 9- 3. In this industry, which one of the following is FALSE?

A) If the scale of Firm X at output Q2 and price P2 is large enough that Firm X has an appreciable share of the market, Firm X will no longer be a price taker.

B) If the price were to fall below P2, firms would leave the industry.

C) At output Q2 and price P2, Firm X is maximizing its long- run profits.

D) If the price were to rise above P2, new firms would enter the industry.

E) Only one firm can reach the size of output Q2.

FIGURE 9- 3Refer to Figure 9- 3. In this industry, which one of the following is FALSE?

A) If the scale of Firm X at output Q2 and price P2 is large enough that Firm X has an appreciable share of the market, Firm X will no longer be a price taker.

B) If the price were to fall below P2, firms would leave the industry.

C) At output Q2 and price P2, Firm X is maximizing its long- run profits.

D) If the price were to rise above P2, new firms would enter the industry.

E) Only one firm can reach the size of output Q2.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

63

Consider a perfectly competitive firm in the following position: output = 4000 units, market price =

$1, fixed costs = $2000, variable costs = $1000, and marginal cost = $1.10. To maximize profits the firm should

A) reduce its output.

B) increase the market price.

C) not change its output.

D) expand its output.

E) shut down.

$1, fixed costs = $2000, variable costs = $1000, and marginal cost = $1.10. To maximize profits the firm should

A) reduce its output.

B) increase the market price.

C) not change its output.

D) expand its output.

E) shut down.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

64

The demand curve facing a perfectly competitive firm depends on

A) the marginal cost of the firm.

B) market demand alone.

C) market demand and the firm's supply curve.

D) market supply alone.

E) market demand and the market supply curve.

A) the marginal cost of the firm.

B) market demand alone.

C) market demand and the firm's supply curve.

D) market supply alone.

E) market demand and the market supply curve.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

65

Consider the following total cost schedule for a perfectly competitive firm producing ball- point pens.

-Refer to Table 9- 3. If this firm were producing at an output level of 30 units, the AFC would be

And the AVC would be .

A) $0.10; $0.30

B) $0.17; $0.20

C) $0.20; $0.17

D) $5; $6

E) $6; $5

-Refer to Table 9- 3. If this firm were producing at an output level of 30 units, the AFC would be

And the AVC would be .

A) $0.10; $0.30

B) $0.17; $0.20

C) $0.20; $0.17

D) $5; $6

E) $6; $5

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

66

A perfectly competitive firm facing a price of $4.00 is currently producing an output level where average variable cost is $2.00, average total cost is $4.00, and marginal cost is $3.00. In order to maximize profits, this firm should

A) decrease output.

B) increase the market price.

C) not change output. This firm is at its profit- maximizing position.

D) shut down.

E) increase output.

A) decrease output.

B) increase the market price.

C) not change output. This firm is at its profit- maximizing position.

D) shut down.

E) increase output.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

67

If a perfectly competitive firm is faced with average revenue below average variable cost it will shut down so as to reduce its

A) losses to the amount of its marginal costs.

B) costs to below its revenue.

C) losses to the amount of its variable costs.

D) costs to zero.

E) losses to the amount of its fixed costs.

A) losses to the amount of its marginal costs.

B) costs to below its revenue.

C) losses to the amount of its variable costs.

D) costs to zero.

E) losses to the amount of its fixed costs.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

68

The perfectly elastic demand curve faced by a competitive firm means that

A) the product's price will be unaffected by any realistic change in the firm's level of output.

B) the firm could increase total revenue by increasing the price.

C) it could actually sell an infinite amount of output at the going price.

D) as the firm expands output its marginal revenue will fall.

E) total revenue is constant regardless of quantity produced.

A) the product's price will be unaffected by any realistic change in the firm's level of output.

B) the firm could increase total revenue by increasing the price.

C) it could actually sell an infinite amount of output at the going price.

D) as the firm expands output its marginal revenue will fall.

E) total revenue is constant regardless of quantity produced.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

69

For a given market price, a competitive firm's marginal- revenue curve

A) is a straight line that coincides with the market demand curve.

B) increases to the right and then declines when MC = MR.

C) is the same as the firm's TR curve.

D) is a positively sloped straight line, starting from the origin.

E) is the same as the firm's demand curve.

A) is a straight line that coincides with the market demand curve.

B) increases to the right and then declines when MC = MR.

C) is the same as the firm's TR curve.

D) is a positively sloped straight line, starting from the origin.

E) is the same as the firm's demand curve.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following statements about a perfectly competitive industry in long- run equilibrium is true?

A) Individual firms will have no incentive for technological improvement.

B) Each firm is producing at the minimum point on its LRAC curve.

C) Losses are tolerable because of high fixed costs.

D) In order to stay in the industry each firm is making an economic profit.

E) Firms must exhibit economies of scale.

A) Individual firms will have no incentive for technological improvement.

B) Each firm is producing at the minimum point on its LRAC curve.

C) Losses are tolerable because of high fixed costs.

D) In order to stay in the industry each firm is making an economic profit.

E) Firms must exhibit economies of scale.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

71

Suppose that in a perfectly competitive industry, the market price of the product is $27. A firm is producing the output level at which average total cost equals marginal cost, both of which are $25. Average variable cost is $23. To maximize profits in the short run, the firm should

A) leave its output unchanged.

B) increase its output.

C) shut down.

D) reduce its output.

E) change the price of the product.

A) leave its output unchanged.

B) increase its output.

C) shut down.

D) reduce its output.

E) change the price of the product.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

72

Consider the following total cost schedule for a perfectly competitive firm producing ball- point pens.

-Refer to Table 9- 3. Suppose the prevailing market price for this firm's product is $0.40. The profit- maximizing level of output for this firm is between

A) 10 and 20 units.

B) 0 and 10 units.

C) 20 and 30 units.

D) 30 and 40 units.

E) 40 and 50 units.

-Refer to Table 9- 3. Suppose the prevailing market price for this firm's product is $0.40. The profit- maximizing level of output for this firm is between

A) 10 and 20 units.

B) 0 and 10 units.

C) 20 and 30 units.

D) 30 and 40 units.

E) 40 and 50 units.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

73

Suppose a typical competitive firm has the following data in the short run: price = $10; output =

100 units; ATC = $8; AVC = $7. What will likely happen?

A) In the long run the industry will expand because of economic profits.

B) The typical firm would shut down, until the remaining firms have a higher price.

C) The size of the industry will remain the same in the long run.

D) In the long run the industry will contract because firms are suffering losses.

E) There is not enough information to formulate an answer.

100 units; ATC = $8; AVC = $7. What will likely happen?

A) In the long run the industry will expand because of economic profits.

B) The typical firm would shut down, until the remaining firms have a higher price.

C) The size of the industry will remain the same in the long run.

D) In the long run the industry will contract because firms are suffering losses.

E) There is not enough information to formulate an answer.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

74

Consider the total cost and revenue curves shown below, for two perfectly competitive firms, Firm A and Firm B. FIGURE 9- 5

Refer to Figure 9- 5. Given its total cost and revenue curves, Firm B should

A) shut down temporarily.

B) maximize its profits by producing that level of output such that the slope of the TVC curve is equal to the slope of the TR curve.

C) produce the level of output where the TC curve intersects the TR curve.

D) maximize its profits by producing that level of output such that the slope of the TC curve is equal to the slope of the TR curve.

E) exit the industry.

FIGURE 9- 5Refer to Figure 9- 5. Given its total cost and revenue curves, Firm B should

A) shut down temporarily.

B) maximize its profits by producing that level of output such that the slope of the TVC curve is equal to the slope of the TR curve.

C) produce the level of output where the TC curve intersects the TR curve.

D) maximize its profits by producing that level of output such that the slope of the TC curve is equal to the slope of the TR curve.

E) exit the industry.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

75

Suppose that in a perfectly competitive industry, the market price of the product is $6. A firm is producing the output level at which average total cost equals marginal cost, both of which are $8. Average variable cost is $4. To maximize its profits in the short run, the firm should

A) leave its output unchanged.

B) -- there is insufficient information to know.

C) reduce its output.

D) expand its output.

E) shut down.

A) leave its output unchanged.

B) -- there is insufficient information to know.

C) reduce its output.

D) expand its output.

E) shut down.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

76

Consider the following cost curves for Firm X, a perfectly competitive firm. FIGURE 9- 3

Refer to Figure 9- 3. If Firm X has a capital stock that generates SRATC1, then in the long run Firm X will have to

A) maintain its output level at Q1, because it is maximizing its short- run profits.

B) set its output at Q1 with an expanded plant size.

C) set its output at Q1 with the existing plant size.

D) expand its output to Q2 with the existing plant size.

E) either expand its plant size or exit from the industry.

FIGURE 9- 3Refer to Figure 9- 3. If Firm X has a capital stock that generates SRATC1, then in the long run Firm X will have to

A) maintain its output level at Q1, because it is maximizing its short- run profits.

B) set its output at Q1 with an expanded plant size.

C) set its output at Q1 with the existing plant size.

D) expand its output to Q2 with the existing plant size.

E) either expand its plant size or exit from the industry.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

77

Consider the following short- run cost curves for a perfectly competitive firm. FIGURE 9- 1

Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P4, the profit- maximizing firm in the short run should produce output

A) C.

B) F.

C) G.

D) H.

E) I.

FIGURE 9- 1Refer to Figure 9- 1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P4, the profit- maximizing firm in the short run should produce output

A) C.

B) F.

C) G.

D) H.

E) I.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

78

Consider the textile industry, which we assume to be a competitive industry, and which experiences continuous cost- reducing technological change. Which of the following statements best describes this industry?

A) High- cost textile mills will co- exist with low- cost mills as long as the revenue for the high- cost mills is covering their variable costs.

B) The price of the product is determined by the minimum ATC of the lowest- cost plants.

C) All textile mills in the industry will be earning zero economic profits or losses.

D) Both A and B

E) Both B and C

A) High- cost textile mills will co- exist with low- cost mills as long as the revenue for the high- cost mills is covering their variable costs.

B) The price of the product is determined by the minimum ATC of the lowest- cost plants.

C) All textile mills in the industry will be earning zero economic profits or losses.

D) Both A and B

E) Both B and C

Unlock Deck