Deck 7: Materiality and Risk

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

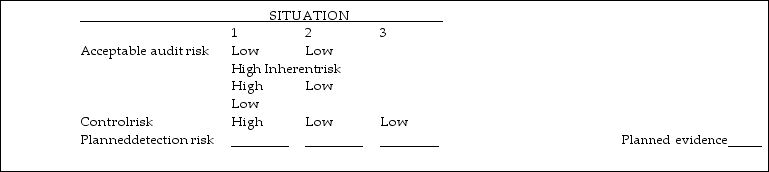

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk or acceptable audit risk. It is more common to assess these risks as high, medium or low. For each of the four situations below, fill in the blanks for planned detection risk and the amount of evidence you would plan to gather ('planned evidence') using the terms high, medium or low.

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/106

Play

Full screen (f)

Deck 7: Materiality and Risk

1

Which one of the following statements is NOT correct?

A) Either an understatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.

B) A misclassification in the balance sheet will have no effect on operating income.

C) Either an overstatement of an asset account or an understatement of a liability account would have the same effect on the income statement.

D) Either an overstatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.

A) Either an understatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.

B) A misclassification in the balance sheet will have no effect on operating income.

C) Either an overstatement of an asset account or an understatement of a liability account would have the same effect on the income statement.

D) Either an overstatement of an asset account or an overstatement of a liability account would have the same effect on the income statement.

D

2

When allocating materiality, most practitioners choose to allocate to:

A) both balance sheet and income statement accounts because there could be errors on either one.

B) the income statement accounts because they are more important.

C) all of the financial statements because there could be errors on other statements besides the income statement and balance sheet.

D) the balance sheet accounts because there are fewer.

A) both balance sheet and income statement accounts because there could be errors on either one.

B) the income statement accounts because they are more important.

C) all of the financial statements because there could be errors on other statements besides the income statement and balance sheet.

D) the balance sheet accounts because there are fewer.

D

3

If acceptable audit risk is low and inherent and control risks are high, the amount of evidence required is:

A) low.

B) high.

C) medium.

D) indeterminate.

A) low.

B) high.

C) medium.

D) indeterminate.

B

4

Many account balances require estimates and/or a great deal of management judgement. One area that does NOT require such judgement would be:

A) liability for warranty payments.

B) obsolete inventory.

C) interest expense.

D) allowance for uncollectible accounts.

A) liability for warranty payments.

B) obsolete inventory.

C) interest expense.

D) allowance for uncollectible accounts.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

5

Which one of the following might NOT be a signal of a lack of integrity in management?

A) Frequent turnover of key financial personnel

B) Frequent disagreements with previous auditors

C) Frequent turnover of key internal audit personnel

D) Prior criminal conviction of an assembly line foreman

A) Frequent turnover of key financial personnel

B) Frequent disagreements with previous auditors

C) Frequent turnover of key internal audit personnel

D) Prior criminal conviction of an assembly line foreman

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is NOT a good indicator of the degree to which statements are relied on by external users?

A) Distribution of ownership among the public

B) Client's size, as measured by total assets or total revenue

C) Nature and amount of liabilities

D) Amount of net income or loss after taxes

A) Distribution of ownership among the public

B) Client's size, as measured by total assets or total revenue

C) Nature and amount of liabilities

D) Amount of net income or loss after taxes

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

7

Materiality is affected by quantitative and factors.

A) relevant

B) audit risk

C) qualitative

D) absolute

A) relevant

B) audit risk

C) qualitative

D) absolute

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is NOT correct?

A) Materiality is a relative rather than an absolute concept.

B) Given equal dollar amounts, fraud is usually considered more important than errors.

C) Normally, the most important base used as the criterion for deciding materiality is total assets.

D) Qualitative factors as well as quantitative factors affect materiality.

A) Materiality is a relative rather than an absolute concept.

B) Given equal dollar amounts, fraud is usually considered more important than errors.

C) Normally, the most important base used as the criterion for deciding materiality is total assets.

D) Qualitative factors as well as quantitative factors affect materiality.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

9

The audit risk model is used primarily:

A) to evaluate the evidence that has been gathered.

B) while doing tests of controls.

C) for planning purposes in determining how much evidence to accumulate.

D) to determine the type of opinion to express.

A) to evaluate the evidence that has been gathered.

B) while doing tests of controls.

C) for planning purposes in determining how much evidence to accumulate.

D) to determine the type of opinion to express.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

10

A major limitation in the application of the audit risk model is:

A) the difficulty in understanding the effect on other factors in the model when one factor is changed.

B) the difficulty in defining the terms of the model.

C) the difficulty in measuring the components of the model.

D) the failure of the Auditing and Assurance Standards Board to accept it and incorporate it into the standards.

A) the difficulty in understanding the effect on other factors in the model when one factor is changed.

B) the difficulty in defining the terms of the model.

C) the difficulty in measuring the components of the model.

D) the failure of the Auditing and Assurance Standards Board to accept it and incorporate it into the standards.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

11

Most auditors would use a higher inherent risk for inventory when:

A) inventory turnover slowed during the year

B) obsolete inventory has been identified

C) there is a large number of errors in the previous year

D) both A and C

A) inventory turnover slowed during the year

B) obsolete inventory has been identified

C) there is a large number of errors in the previous year

D) both A and C

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

12

Regardless of how the allocation of the preliminary judgement about materiality was done, when the audit is complete the auditor must be confident that the combined errors in all accounts are:

A) less than the preliminary judgement.

B) less than or equal to the preliminary judgement.

C) equal to the preliminary judgement.

D) more than the preliminary judgement.

A) less than the preliminary judgement.

B) less than or equal to the preliminary judgement.

C) equal to the preliminary judgement.

D) more than the preliminary judgement.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

13

Likely misstatements arise from:

A) the auditor's estimate of misstatements.

B) projections of misstatements based on the auditor's tests.

C) projections of misstatements based on the auditor's preliminary assessment of materiality.

D) differences between management's and the auditor's judgement about estimates of account balances.

A) the auditor's estimate of misstatements.

B) projections of misstatements based on the auditor's tests.

C) projections of misstatements based on the auditor's preliminary assessment of materiality.

D) differences between management's and the auditor's judgement about estimates of account balances.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

14

Auditors are concerned about under- auditing as:

A) control risk may be assessed inappropriately.

B) insufficient evidence may have been allocated to the audit.

C) it exposes the audit firm to loss of professional reputation.

D) an audit may be assessed incorrectly.

A) control risk may be assessed inappropriately.

B) insufficient evidence may have been allocated to the audit.

C) it exposes the audit firm to loss of professional reputation.

D) an audit may be assessed incorrectly.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

15

When setting a preliminary judgement about materiality at the planning stage, auditors may have to subsequently change this preliminary assessment. The new assessment is called:

A) allocated materiality.

B) planned materiality.

C) revised assessment of materiality.

D) segment materiality.

A) allocated materiality.

B) planned materiality.

C) revised assessment of materiality.

D) segment materiality.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

16

Acceptable audit risk is ordinarily set by the auditor during planning and:

A) varies by each major cycle and by each account.

B) holds constant for each major cycle but varies by account.

C) holds constant for each major cycle and account.

D) varies by each major cycle but is constant by account.

A) varies by each major cycle and by each account.

B) holds constant for each major cycle but varies by account.

C) holds constant for each major cycle and account.

D) varies by each major cycle but is constant by account.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

17

When discussing planned detection risk (PDR) and the audit risk model, which of the following statements is NOT true?

A) PDR determines the amount of evidence the auditor plans to accumulate, inversely with the size of planned detection risk.

B) When PDR is changed from low to medium, the required accumulation of evidence would be increased.

C) PDR is a measure of the risk that the auditor will not detect a misstatement in an assertion that could be material.

D) PDR is dependent on the other three factors in the model; i.e., it will change only if another changes.

A) PDR determines the amount of evidence the auditor plans to accumulate, inversely with the size of planned detection risk.

B) When PDR is changed from low to medium, the required accumulation of evidence would be increased.

C) PDR is a measure of the risk that the auditor will not detect a misstatement in an assertion that could be material.

D) PDR is dependent on the other three factors in the model; i.e., it will change only if another changes.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

18

If planned detection risk is reduced, the amount of evidence the auditor accumulates will:

A) increase.

B) decrease.

C) be indeterminate.

D) remain unchanged.

A) increase.

B) decrease.

C) be indeterminate.

D) remain unchanged.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is NOT a difficulty auditors face when allocating materiality?

A) Audit costs

B) Reliability of audit evidence

C) Expectations of misstatements in accounts

D) Understatements and/or overstatements

A) Audit costs

B) Reliability of audit evidence

C) Expectations of misstatements in accounts

D) Understatements and/or overstatements

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

20

The Auditor's Responsibility paragraph in the auditor's report includes two important phrases that are directly related to materiality and risk. These two phrases are: 1. 'Relevant ethical requirements relating to audit engagements.'

2) 'Plan and perform the audit.'

3) 'Free from material misstatement.'

4) 'Reasonable assurance.'

A) 1 and 2

B) 3 and 4

C) 2 and 3

D) 1 and 4

2) 'Plan and perform the audit.'

3) 'Free from material misstatement.'

4) 'Reasonable assurance.'

A) 1 and 2

B) 3 and 4

C) 2 and 3

D) 1 and 4

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

21

Which one of the following statements regarding inherent risk is correct?

A) The inherent risk assigned in the audit risk model is dependent upon the strengths in client's internal control system.

B) The inherent risk assigned in the audit risk model is unaffected by the auditor's experience with client's organisation.

C) Most auditors set a high inherent risk in the first year of an audit and reduce it in subsequent years as they gain experience, even when there is inherent risk.

D) Most auditors set a low inherent risk in the first year of an audit and increase it if experience shows that it was incorrect.

A) The inherent risk assigned in the audit risk model is dependent upon the strengths in client's internal control system.

B) The inherent risk assigned in the audit risk model is unaffected by the auditor's experience with client's organisation.

C) Most auditors set a high inherent risk in the first year of an audit and reduce it in subsequent years as they gain experience, even when there is inherent risk.

D) Most auditors set a low inherent risk in the first year of an audit and increase it if experience shows that it was incorrect.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

22

Bases are needed for evaluating materiality. What base would you use for the Balance Sheet?

A) Total assets

B) Current liabilities

C) Current assets

D) Operating profit before income tax

A) Total assets

B) Current liabilities

C) Current assets

D) Operating profit before income tax

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

23

ASA 320 indicates that materiality should be considered:

A) when determining the nature, timing and extent of audit procedures.

B) when evaluating the effect of uncorrected misstatements, if any, on the financial report and in forming the opinion in the auditor's report.

C) at all stages of audit planning.

D) both A and B above

A) when determining the nature, timing and extent of audit procedures.

B) when evaluating the effect of uncorrected misstatements, if any, on the financial report and in forming the opinion in the auditor's report.

C) at all stages of audit planning.

D) both A and B above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

24

Bases are needed for evaluating materiality. If you used operating profit before income tax, what minimum percentage would you use for planning materiality?

A) 1%

B) 5%

C) 10%

D) None of the above

A) 1%

B) 5%

C) 10%

D) None of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

25

Materiality is a rather than an absolute concept.

A) qualitative

B) relative

C) relevant

D) quantitative

A) qualitative

B) relative

C) relevant

D) quantitative

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

26

The preliminary judgement about materiality is the amount by which the auditor believes the statements could be misstated and still not affect the economic decisions of users.

A) median average

B) minimum

C) mean average

D) maximum

A) median average

B) minimum

C) mean average

D) maximum

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

27

When management has an adequate level of integrity for the auditor to accept the engagement but cannot be regarded as completely honest in all dealings, auditors normally:

A) increase acceptable audit risk and reduce inherent risk.

B) reduce acceptable audit risk and increase inherent risk.

C) reduce inherent risk and control risk.

D) increase inherent risk and control risk.

A) increase acceptable audit risk and reduce inherent risk.

B) reduce acceptable audit risk and increase inherent risk.

C) reduce inherent risk and control risk.

D) increase inherent risk and control risk.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

28

An auditor may compensate for a weakness or deficiency in the internal control by increasing the:

A) extent of tests of controls.

B) preliminary judgement about audit risk.

C) extent of substantive tests.

D) level of detection risk.

A) extent of tests of controls.

B) preliminary judgement about audit risk.

C) extent of substantive tests.

D) level of detection risk.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

29

The estimate for sampling error results because the auditor has sampled only a portion of the population. Sampling error represents the:

A) maximum misstatements in the audited accounts.

B) maximum misstatements in accounts not audited.

C) minimum misstatements in accounts not audited.

D) minimum misstatements in the audited accounts.

A) maximum misstatements in the audited accounts.

B) maximum misstatements in accounts not audited.

C) minimum misstatements in accounts not audited.

D) minimum misstatements in the audited accounts.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

30

Tolerable misstatement as set by the auditor:

A) increases inherent risk and control risk.

B) increases control risk only.

C) increases inherent risk only.

D) does not affect inherent or control risks.

A) increases inherent risk and control risk.

B) increases control risk only.

C) increases inherent risk only.

D) does not affect inherent or control risks.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

31

Which one of the following discoveries by the auditor would NOT raise the red flag of increased inherent risk?

A) Review of the results of the previous year's audit shows there were significant misstatements in accounts payable.

B) This is the fourth consecutive year that the firm has audited this client.

C) The client is an electronics manufacturer that is holding extensive inventory.

D) Client is a parent company with a subsidiary.

A) Review of the results of the previous year's audit shows there were significant misstatements in accounts payable.

B) This is the fourth consecutive year that the firm has audited this client.

C) The client is an electronics manufacturer that is holding extensive inventory.

D) Client is a parent company with a subsidiary.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

32

In an audit area that has a low acceptable risk, it would be prudent to:

A) review the completed working papers more thoroughly.

B) increase the amount of audit evidence gathered.

C) assign more experienced staff to that area.

D) do all of the above.

A) review the completed working papers more thoroughly.

B) increase the amount of audit evidence gathered.

C) assign more experienced staff to that area.

D) do all of the above.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

33

When there is a high degree of engagement risk, auditors can factor this into the audit risk model by:

A) increasing the assessment of inherent risk.

B) reducing the planned detection risk.

C) reducing the acceptable audit risk.

D) all of the above

A) increasing the assessment of inherent risk.

B) reducing the planned detection risk.

C) reducing the acceptable audit risk.

D) all of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

34

AASB 1031 suggests guidelines.

A) relevant

B) quantitative

C) qualitative

D) relative

A) relevant

B) quantitative

C) qualitative

D) relative

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

35

Which one of the following factors is NOT a good indicator of potential financial failure?

A) Client relies heavily on debt financing, especially by financing permanent assets with short- term loans.

B) Client's retained earnings were reduced by half as a result of a large dividend payout.

C) Client is constantly short of cash and working capital.

D) Client has had increasing net losses for several years.

A) Client relies heavily on debt financing, especially by financing permanent assets with short- term loans.

B) Client's retained earnings were reduced by half as a result of a large dividend payout.

C) Client is constantly short of cash and working capital.

D) Client has had increasing net losses for several years.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

36

An aim of allocating a preliminary judgement about materiality to Balance Sheet accounts is to:

A) increase audit quality.

B) determine the level of audit to accumulate.

C) minimise audit costs and maintain audit quality.

D) reduce audit risk.

A) increase audit quality.

B) determine the level of audit to accumulate.

C) minimise audit costs and maintain audit quality.

D) reduce audit risk.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

37

Auditors begin their assessments of inherent risk during the planning phase. Which of the following would NOT be a topic of the planning phase that would also help to assess inherent risk?

A) Obtaining client's agreement on the engagement letter

B) Identifying related parties

C) Obtaining knowledge about the client's business and industry

D) Touring the client's plant and offices

A) Obtaining client's agreement on the engagement letter

B) Identifying related parties

C) Obtaining knowledge about the client's business and industry

D) Touring the client's plant and offices

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

38

Materiality and risk are concepts in planning the audit and designing an audit approach.

A) typical

B) optional

C) fundamental

D) reasonable

A) typical

B) optional

C) fundamental

D) reasonable

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

39

The amount of evidence required will be lower where:

A) IR and CR are both low and planned DR is high.

B) IR and CR are both high and planned DR is low.

C) IR and CR are both low and DR is low.

D) IR and CR are both medium and planned DR is medium.

A) IR and CR are both low and planned DR is high.

B) IR and CR are both high and planned DR is low.

C) IR and CR are both low and DR is low.

D) IR and CR are both medium and planned DR is medium.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

40

The audit risk model is:

A) useful in evaluating results but of limited use in planning.

B) useful when performing the tests of balances, but of little value in either the planning or evaluation stages.

C) a planning, testing and evaluation model.

D) useful in planning but of limited use in evaluating results.

A) useful in evaluating results but of limited use in planning.

B) useful when performing the tests of balances, but of little value in either the planning or evaluation stages.

C) a planning, testing and evaluation model.

D) useful in planning but of limited use in evaluating results.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

41

When auditors allocate the preliminary judgement about materiality to account balances, the materiality allocated to any given account balance is referred to as:

A) the error range.

B) tolerable materiality.

C) tolerable misstatement.

D) the materiality range.

A) the error range.

B) tolerable materiality.

C) tolerable misstatement.

D) the materiality range.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

42

Auditors respond to risk by:

A) changing the extent of testing and type of audit procedures.

B) modifying the assessment of materiality.

C) increasing the amount of evidence collected.

D) all of the above

A) changing the extent of testing and type of audit procedures.

B) modifying the assessment of materiality.

C) increasing the amount of evidence collected.

D) all of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

43

Direct projection from the sample to the population:

A) takes into account errors in accounts not audited.

B) is only necessary when the sample error is material.

C) ignores sampling error.

D) none of the above

A) takes into account errors in accounts not audited.

B) is only necessary when the sample error is material.

C) ignores sampling error.

D) none of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

44

If an auditor were to calculate an estimate of the errors by direct projection from the sample to the population, and found $15,000 of net overstatement errors in a sample of $100 000 out of a total population of $500 000, the estimate of errors in the population would be:

A) $7,500.

B) $750,000.

C) $75,000.

D) $750.

A) $7,500.

B) $750,000.

C) $75,000.

D) $750.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

45

Which one of the following is an example of the concept of inherent risk?

A) Humans make more errors than computers; therefore, a manual accounting system is riskier than a computerised system.

B) Audits with larger sample sizes are less risky than those with smaller sample sizes.

C) Loans receivable for a finance company are less likely to be collectible than those of a bank.

D) Accounting systems with vouchers have many more controls built in, so the risk that there will be errors on the financial statements is reduced.

A) Humans make more errors than computers; therefore, a manual accounting system is riskier than a computerised system.

B) Audits with larger sample sizes are less risky than those with smaller sample sizes.

C) Loans receivable for a finance company are less likely to be collectible than those of a bank.

D) Accounting systems with vouchers have many more controls built in, so the risk that there will be errors on the financial statements is reduced.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

46

In situations in which the auditor believes the chance of financial failure or loss is high, and there is a corresponding increase in engagement risk for the auditor, acceptable audit risk should:

A) be calculated using a computerised statistical package.

B) be reduced.

C) be increased.

D) remain the same.

A) be calculated using a computerised statistical package.

B) be reduced.

C) be increased.

D) remain the same.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

47

If it is probable that the economic decisions of users would have been influenced by the omission or misstatement of information, then that information is:

A) relevant.

B) significant.

C) insignificant.

D) material.

A) relevant.

B) significant.

C) insignificant.

D) material.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

48

Where auditors have knowledge of specific intended users and uses, their judgement of what they consider material:

A) is based on the last audit.

B) may be affected.

C) remains unchanged.

D) none of the above

A) is based on the last audit.

B) may be affected.

C) remains unchanged.

D) none of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

49

A careful reading of the standards reveals that applying materiality in practice is:

A) based on experience.

B) fairly simple.

C) straightforward.

D) none of the above

A) based on experience.

B) fairly simple.

C) straightforward.

D) none of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

50

Why might an auditor revise the preliminary assessment of materiality?

A) Because of qualitative events

B) Because the auditor determined preliminary assessment of materiality before year- end

C) Because client circumstances may have changed

D) All of the above

A) Because of qualitative events

B) Because the auditor determined preliminary assessment of materiality before year- end

C) Because client circumstances may have changed

D) All of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

51

Which one of the following statements is true? Misstatements found in the previous year's audit:

A) have a high likelihood of occurring again in the current year's audit.

B) and occurring again in the current year's audit would be an indication of management fraud.

C) and occurring again in the current year's audit would be an indication of employee fraud.

D) have little likelihood of occurring again in the current year's audit.

A) have a high likelihood of occurring again in the current year's audit.

B) and occurring again in the current year's audit would be an indication of management fraud.

C) and occurring again in the current year's audit would be an indication of employee fraud.

D) have little likelihood of occurring again in the current year's audit.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

52

When discussing control risk (CR) and the audit risk model, which one of the following statements is NOT true?

A) The relationship between control risk and detection risk is inverse.

B) CR is a measure of the auditor's assessment of the likelihood that errors will not be prevented or detected by the client's internal control.

C) The relationship between control risk and evidence is direct.

D) If the auditor concludes that internal control is completely ineffective to prevent or detect errors, he or she would assign a 0% to CR.

A) The relationship between control risk and detection risk is inverse.

B) CR is a measure of the auditor's assessment of the likelihood that errors will not be prevented or detected by the client's internal control.

C) The relationship between control risk and evidence is direct.

D) If the auditor concludes that internal control is completely ineffective to prevent or detect errors, he or she would assign a 0% to CR.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

53

When discussing acceptable audit risk (AAR) and the audit risk model, which one of the following statements is true?

A) AAR is objectively determined by the auditor.

B) The terms audit assurance, overall assurance or level of assurance are synonyms for AAR.

C) When the auditor decides on a lower acceptable audit risk, it means the auditor wants to be more certain that the financial statements are not materially misstated.

D) AAR is the risk that the auditor is willing to take that the financial statements are fairly stated after the audit is completed and an unqualified opinion has been reached.

A) AAR is objectively determined by the auditor.

B) The terms audit assurance, overall assurance or level of assurance are synonyms for AAR.

C) When the auditor decides on a lower acceptable audit risk, it means the auditor wants to be more certain that the financial statements are not materially misstated.

D) AAR is the risk that the auditor is willing to take that the financial statements are fairly stated after the audit is completed and an unqualified opinion has been reached.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

54

The five steps in applying materiality are listed below in random order. 1. Estimate the combined misstatement.

2) Estimate the total misstatement in the segment.

3) Set preliminary judgement of materiality.

4) Allocate preliminary judgement of materiality to segments.

5) Compare combined estimate with preliminary judgement about materiality. The correct sequence from start to finish would be:

A) 1 2 5 4 3.

B) 3 4 2 1 5.

C) 4 3 1 5 2.

D) 5 1 3 2 4.

2) Estimate the total misstatement in the segment.

3) Set preliminary judgement of materiality.

4) Allocate preliminary judgement of materiality to segments.

5) Compare combined estimate with preliminary judgement about materiality. The correct sequence from start to finish would be:

A) 1 2 5 4 3.

B) 3 4 2 1 5.

C) 4 3 1 5 2.

D) 5 1 3 2 4.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

55

Bases are needed for evaluating materiality. If you used current liabilities or current assets, what minimum percentage would you use for planning materiality?

A) 10%

B) 5%

C) 1%

D) None of the above

A) 10%

B) 5%

C) 1%

D) None of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is NOT a consideration when the auditor is attempting to assess the inherent risk?

A) Existence of related parties

B) Nature of client's business

C) Frequency and intensity of top management's review of the accounting transactions and records

D) Results of previous audits

A) Existence of related parties

B) Nature of client's business

C) Frequency and intensity of top management's review of the accounting transactions and records

D) Results of previous audits

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

57

Because control risk and inherent risk vary from cycle to cycle, account to account or objective to objective:

A) detection risk and required audit evidence will also vary.

B) detection risk will vary, but audit evidence will remain constant.

C) detection risk will remain constant, but audit evidence will vary.

D) acceptable audit risk must remain a constant.

A) detection risk and required audit evidence will also vary.

B) detection risk will vary, but audit evidence will remain constant.

C) detection risk will remain constant, but audit evidence will vary.

D) acceptable audit risk must remain a constant.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

58

Allocating the preliminary judgement about materiality to segments of the financial statements is necessary because:

A) evidence is accumulated for the financial statements as a whole so the materiality doesn't apply to them.

B) it is required by the Code of Professional Conduct.

C) it is required by the Corporations Act.

D) evidence is accumulated by segments rather than for the financial statements as a whole.

A) evidence is accumulated for the financial statements as a whole so the materiality doesn't apply to them.

B) it is required by the Code of Professional Conduct.

C) it is required by the Corporations Act.

D) evidence is accumulated by segments rather than for the financial statements as a whole.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following statements about preliminary assessment of materiality is FALSE?

A) It is a matter of auditor judgement.

B) It is a professional opinion, and it may not change during the engagement.

C) It is the maximum amount by which the auditor believes the statements could be misstated and still not affect the decisions of reasonable users.

D) Auditors decide on the combined amount of misstatements in the financial statements that they would consider material early in the audit, when they are developing the overall strategy for the audit.

A) It is a matter of auditor judgement.

B) It is a professional opinion, and it may not change during the engagement.

C) It is the maximum amount by which the auditor believes the statements could be misstated and still not affect the decisions of reasonable users.

D) Auditors decide on the combined amount of misstatements in the financial statements that they would consider material early in the audit, when they are developing the overall strategy for the audit.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

60

Risk is:

A) a measure of uncertainty.

B) measured by tolerable error.

C) to be avoided in the audit.

D) all of the above

A) a measure of uncertainty.

B) measured by tolerable error.

C) to be avoided in the audit.

D) all of the above

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

61

The auditor's preliminary judgement about materiality is the maximum amount by which the auditor believes the financial statements could be misstated and still not affect the economic decisions of users.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

62

Using your knowledge of the relationships among acceptable audit risk, inherent risk, control risk, planned detection risk, tolerable error and planned evidence, state the effect on planned evidence (increase or decrease) of changing each of the following factors, while the other factors remain unchanged.

1. An increase in acceptable audit risk. __________

2. An increase in inherent risk. __________

3. A decrease in control risk. __________

4. An increased in planned detection risk. __________

5. An increase in tolerable misstatement. __________

1. An increase in acceptable audit risk. __________

2. An increase in inherent risk. __________

3. A decrease in control risk. __________

4. An increased in planned detection risk. __________

5. An increase in tolerable misstatement. __________

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

63

The auditor assesses control risk and inherent risk. On a typical engagement, the auditor would be LEAST likely to assess these for:

A) the overall audit.

B) each audit objective.

C) each cycle.

D) each account.

A) the overall audit.

B) each audit objective.

C) each cycle.

D) each account.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

64

Discuss how auditors use the audit risk model when planning an audit.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

65

Inherent risk is reduced where the likelihood of misstatement is low. This would be true for accounts receivable if:

A) most balances in accounts receivable were from overseas customers.

B) most balances in accounts receivable were from related parties.

C) most balances in accounts receivable were overdue.

D) most balances in accounts receivable were current.

A) most balances in accounts receivable were from overseas customers.

B) most balances in accounts receivable were from related parties.

C) most balances in accounts receivable were overdue.

D) most balances in accounts receivable were current.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

66

Acceptable audit risk and planned detection risk are inversely related; i.e., as acceptable audit risk increases, planned detection risk should decrease, ceteris paribus.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

67

Audit assurance is the complement of planned detection risk, i.e., one minus planned detection risk.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

68

A materiality level of $1000 would require more audit evidence than would a materiality level of

$100 000.

$100 000.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

69

Match six of the terms (a- i) with the definitions provided below (1- 6):

a. business risk

b. preliminary judgement about materiality

c. inherent risk

d. planned detection risk

e. audit assurance

f. acceptable audit risk

g. tolerable error

h. control risk

i. materiality

1. A measure of the risk that the auditor will not detect a misstatement that exists in an assertion that could be material.

2. The risk that the auditor or audit firm will suffer harm because of a client relationship even though the audit report rendered for the client was correct.

3. A measure of the auditor's assessment of the likelihood that misstatements exceeding a tolerable amount in a segment will not be prevented or detected by the client's internal controls.

4. A measure of how much risk the auditor is willing to take that the financial statements may be materially misstated after the audit is completed and an unqualified audit opinion has been issued.

5. The materiality allocated to any given account balance.

6. The maximum amount by which the auditor believes that the statements could be misstated and still not affect the economic decisions of users.

a. business risk

b. preliminary judgement about materiality

c. inherent risk

d. planned detection risk

e. audit assurance

f. acceptable audit risk

g. tolerable error

h. control risk

i. materiality

1. A measure of the risk that the auditor will not detect a misstatement that exists in an assertion that could be material.

2. The risk that the auditor or audit firm will suffer harm because of a client relationship even though the audit report rendered for the client was correct.

3. A measure of the auditor's assessment of the likelihood that misstatements exceeding a tolerable amount in a segment will not be prevented or detected by the client's internal controls.

4. A measure of how much risk the auditor is willing to take that the financial statements may be materially misstated after the audit is completed and an unqualified audit opinion has been issued.

5. The materiality allocated to any given account balance.

6. The maximum amount by which the auditor believes that the statements could be misstated and still not affect the economic decisions of users.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

70

Identify each of the three major issues or 'difficulties' an auditor must consider when allocating materiality to accounts, and describe how each issue affects the allocation decision.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

71

Identify the three strategies that auditors can use during the audit to respond to risk.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

72

Explain why it is necessary to allocate the preliminary judgement about materiality to individual accounts (segments) in the financial statements. Also explain why allocating to balance sheet accounts is more common than allocating to income statement accounts.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

73

Preliminary assessment of materiality is the combined amount of misstatements in the financial statements that auditors would consider material early in the audit.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

74

Inherent risk and planned detection risk are inversely related; i.e., as inherent risk increases, planned detection risk should decrease, ceteris paribus.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

75

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk or acceptable audit risk. It is more common to assess these risks as high, medium or low. For each of the four situations below, fill in the blanks for planned detection risk and the amount of evidence you would plan to gather ('planned evidence') using the terms high, medium or low.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

76

The definition of materiality in the auditing standards is consistent with that contained in accounting

standards.

standards.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

77

An acceptable audit risk assessment of low indicates a risky client requiring more extensive evidence, assignment of more experienced personnel and/or a more extensive review of working papers.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

78

The primary purpose of allocating the preliminary judgement about materiality to financial statement accounts is to help the auditor decide the appropriate evidence to accumulate for each account.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

79

Risk in auditing means that the auditor accepts some level of uncertainty in performing the audit function. An effective auditor will:

A) set the risk level between 5% and 10%.

B) recognise that risks exist and deal with those risks in an appropriate manner.

C) perform the audit procedures first and quantitatively set the risk level before forming an opinion and writing the report.

D) take any means available to reduce the risk to the lowest possible level.

A) set the risk level between 5% and 10%.

B) recognise that risks exist and deal with those risks in an appropriate manner.

C) perform the audit procedures first and quantitatively set the risk level before forming an opinion and writing the report.

D) take any means available to reduce the risk to the lowest possible level.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

80

Control risk and the amount of substantive evidence required are directly related; i.e., as control risk increases, the amount of substantive evidence the auditor plans to accumulate should increase.

Unlock Deck

Unlock for access to all 106 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 106 flashcards in this deck.