Deck 13: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm.

(a) Fill in the missing values.

(b) What level of output should the firm produce? Explain.

(a) Fill in the missing values.

(b) What level of output should the firm produce? Explain.

Question

Question

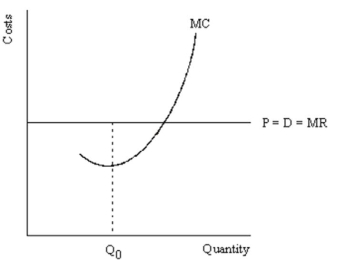

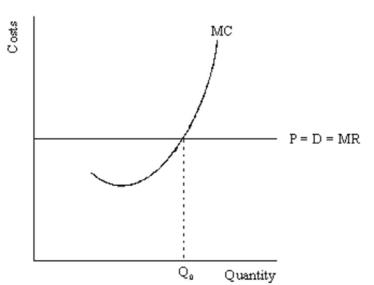

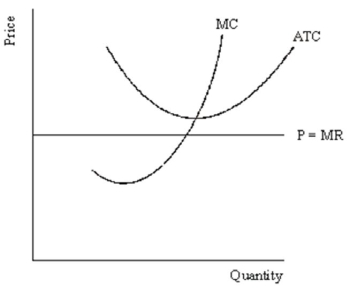

Using the following diagram, demonstrate graphically and explain verbally why Q0 is not a profit maximizing output level.

Question

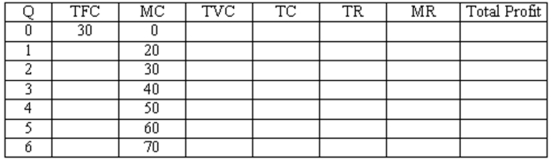

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm. The price of the product this firm produces is $50.  (a) Fill in the missing values.

(a) Fill in the missing values.

(b) What level of output should the firm produces? Why?

(c) What do you predict will happen to the number of firms in the industry? Why?

(d) What do you predict will happen to supply and the market price?

(e) At which price must the firm shut down?

(a) Fill in the missing values.(b) What level of output should the firm produces? Why?

(c) What do you predict will happen to the number of firms in the industry? Why?

(d) What do you predict will happen to supply and the market price?

(e) At which price must the firm shut down?

Question

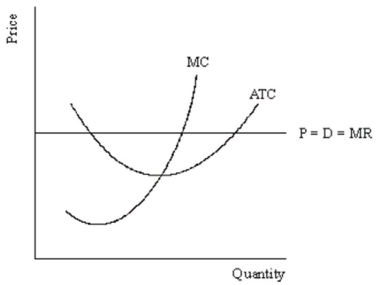

Using the following diagram, demonstrate that producing at the level of output associated with maximum per unit profit (minimum of the ATC curve) does not maximize total profit.

Question

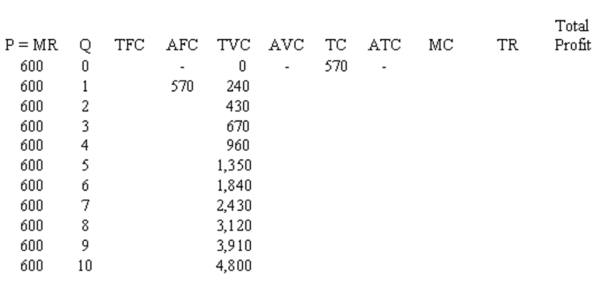

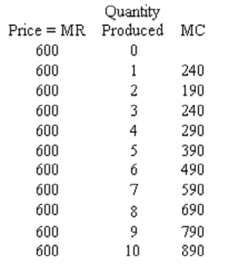

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm. What output level should the firm produce? Explain.  NOTE: Marginal values represent values between levels of output. For example, the marginal cost between 0 units and 1 unit is $240.

NOTE: Marginal values represent values between levels of output. For example, the marginal cost between 0 units and 1 unit is $240.

NOTE: Marginal values represent values between levels of output. For example, the marginal cost between 0 units and 1 unit is $240. Question

Consider the following diagram:  Would a perfectly competitive firm facing these conditions stay in business in the short run? Demonstrate your answer by comparing the loss if it stayed open to the loss if it closed.

Would a perfectly competitive firm facing these conditions stay in business in the short run? Demonstrate your answer by comparing the loss if it stayed open to the loss if it closed.

Would a perfectly competitive firm facing these conditions stay in business in the short run? Demonstrate your answer by comparing the loss if it stayed open to the loss if it closed. Question

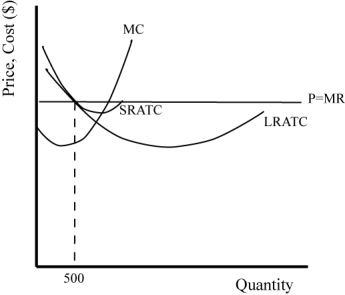

Study the graph below and answer the following questions.  (a) Is this firm making profit by producing 500 units in the short run? Why or why not?

(a) Is this firm making profit by producing 500 units in the short run? Why or why not?

(b) What will happen in the long run in this industry?

(c) Will the firm survive in this industry?

(a) Is this firm making profit by producing 500 units in the short run? Why or why not?(b) What will happen in the long run in this industry?

(c) Will the firm survive in this industry?

Question

Question

Question

Question

Question

Using the following diagram, demonstrate graphically and explain verbally why any movement away from output level Q0 would decrease the firm's profit.

Question

Question

Consider the following diagram of a representative competitive firm:  Is this a long-run equilibrium situation? If yes, explain why it is. If no, explain what will happen to transform it into a long-run equilibrium situation.

Is this a long-run equilibrium situation? If yes, explain why it is. If no, explain what will happen to transform it into a long-run equilibrium situation.

Is this a long-run equilibrium situation? If yes, explain why it is. If no, explain what will happen to transform it into a long-run equilibrium situation.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/35

Play

Full screen (f)

Deck 13: Perfect Competition

1

A perfectly competitive market is a market in which economic forces operate unimpeded. The six conditions necessary to have a perfectly competitive market are: (1.) Both buyers and sellers are price takers. (2.) The number of firms is large. (3.) There are no barriers to entry. (4.) Firms' products are identical. (5.) There is complete information. And (6.) selling firms are profit maximizing entrepreneurial firms. Discuss any three of these conditions.

(Any three of the following)

1. In a perfectly competitive industry both buyers and sellers are price takers. Price takers are firms or individuals who take the price determined by the market equilibrium as given. In a perfectly competitive market, market supply and demand determine the price; both firms and consumers take the price as given.

2. A large number of firms in this context means that there are so many firms that any one firm's output compared to market output is imperceptible, and what one firm does has no influence on what other firms do.

3. There are no barriers to entry. Barriers to entry may be social, political or economic impediments that prevent firms from entering a market. In a perfectly competitive industry, there could be no patents, and the minimum efficient scale should allow a large number of firms to produce at the lowest average cost.

4. Each firm's output is indistinguishable from any other firm's output. Corn sold on national grain markets would be an example. The price of all bushels would be the same. Pepsi and Coke are examples of products that are not identical. They may sell at different prices in the market and the market for colas and therefore cannot be regarded as perfectly competitive.

5. In a perfectly competitive market, firms and consumers know all there is to know about the market. This would include prices, products and available technology. Thus no firm or consumer would have a competitive edge over another.

6. For perfect competition to exist, firms must seek maximum profit and only profit, and the people who make the firm's decisions must receive profit and only profit.

1. In a perfectly competitive industry both buyers and sellers are price takers. Price takers are firms or individuals who take the price determined by the market equilibrium as given. In a perfectly competitive market, market supply and demand determine the price; both firms and consumers take the price as given.

2. A large number of firms in this context means that there are so many firms that any one firm's output compared to market output is imperceptible, and what one firm does has no influence on what other firms do.

3. There are no barriers to entry. Barriers to entry may be social, political or economic impediments that prevent firms from entering a market. In a perfectly competitive industry, there could be no patents, and the minimum efficient scale should allow a large number of firms to produce at the lowest average cost.

4. Each firm's output is indistinguishable from any other firm's output. Corn sold on national grain markets would be an example. The price of all bushels would be the same. Pepsi and Coke are examples of products that are not identical. They may sell at different prices in the market and the market for colas and therefore cannot be regarded as perfectly competitive.

5. In a perfectly competitive market, firms and consumers know all there is to know about the market. This would include prices, products and available technology. Thus no firm or consumer would have a competitive edge over another.

6. For perfect competition to exist, firms must seek maximum profit and only profit, and the people who make the firm's decisions must receive profit and only profit.

2

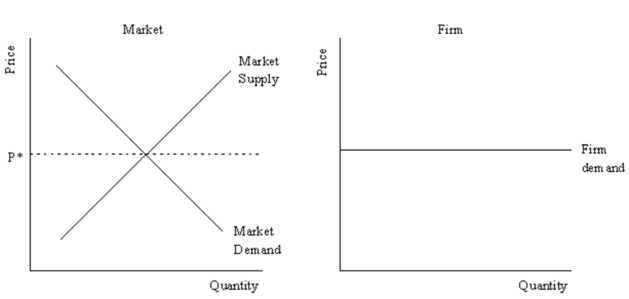

Demonstrate graphically and explain verbally how a demand curve facing a perfectly competitive firm relates to the market demand curve.

The demand curve facing a perfectly competitive firm is perfectly elastic at the price level that is determined by the equilibrium of the market demand and market supply curves. This can be illustrated as follows:

3

How does a market supply curve relate to a firm's supply curve?

A market supply curve is the horizontal summation of all the firms' marginal cost curves, taking into account any changes in input prices that might occur.

4

In determining the supply curve of a perfectly competitive firm, what cost information do you need? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

5

Retail stores generally set a fixed price and let people buy all they want at that price. Does that mean that the supply curve of those goods is perfectly elastic?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

6

How are normal profits related to economic profits?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

7

Firms know that when they enter a profitable industry, profits will eventually be eliminated by competition. Why would a firm want to enter such an industry?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

8

Explain, using an example if necessary to be clear, why the minimum point on the average variable cost curve is the shutdown point. In other words, why is a competitive firm's supply curve that portion of the marginal cost curve that lies above the minimum average variable cost?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

9

In determining the supply curve of a perfectly competitive firm, what cost information do you need? Why do you need that information? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

10

Explain how the long-run market supply curve for a perfectly competitive industry depends upon factor prices.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

11

Perfectly competitive firms are price takers. However, in the real world, it is rare that the customer goes into any business establishment and tells the seller what price he is willing to pay. Since buyers don't dictate price, where does price come from in perfectly competitive markets?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

12

Some firms, particularly but not exclusively Japanese firms, have historically considered their workers to be lifetime employees. Let's call these firms Type A firms. How would this management attitude affect Type A firms' production decisions during a period of slack demand and falling prices relative to other (Type

B) firms?

B) firms?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the necessary conditions for perfect competition are least likely to be satisfied in the real world? Explain your selections.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

14

Explain how the long-run market supply curve for a perfectly competitive industry depends upon factor prices. How would this apply to the milk producing industry?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

15

How does the Internet affect the competitive nature of markets?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

16

Why will perfectly competitive firms make zero profits in the long run? How are normal profits related to economic profits?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

17

How would an economist determine graphically the output and profit of a perfect competitor?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

18

Describe how a market supply curve relates to a firm's supply curve. How does the short-run market supply curve differ from the long run market supply curve?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

19

You are running a business in a perfectly competitive market. Your product sells for $5 and your marginal costs rise as output rises. What should you do in the two situations described below? What general rule do the above examples suggest about how a firm should determine the level of output to produce so as to maximize profit?

(a) The additional cost of producing another unit of output is $4. What should you do? What will this do to your total profit?

(b) The additional cost incurred from your last unit of output produced is $6. What should you do? What will this do to your total profit?

(c) What general rule do the above examples suggest about how a firm should determine the level of output to produce so as to maximize profit?

(a) The additional cost of producing another unit of output is $4. What should you do? What will this do to your total profit?

(b) The additional cost incurred from your last unit of output produced is $6. What should you do? What will this do to your total profit?

(c) What general rule do the above examples suggest about how a firm should determine the level of output to produce so as to maximize profit?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

20

Define a perfectly competitive market, and list the six conditions necessary for a market to be perfectly competitive.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

21

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm.

(a) Fill in the missing values.

(b) What level of output should the firm produce? Explain.

(a) Fill in the missing values.

(b) What level of output should the firm produce? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

22

Using a supply and demand and a typical firm diagram, illustrate the impact of a flood on the market for contractors once the flood has receded. NOTE: Assume the market was perfectly competitive and in a long-run equilibrium position before the flood. Also assume that construction is a constant-cost industry.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

23

Using the following diagram, demonstrate graphically and explain verbally why Q0 is not a profit maximizing output level.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

24

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm. The price of the product this firm produces is $50. (a) Fill in the missing values.

(b) What level of output should the firm produces? Why?

(c) What do you predict will happen to the number of firms in the industry? Why?

(d) What do you predict will happen to supply and the market price?

(e) At which price must the firm shut down?

(a) Fill in the missing values.(b) What level of output should the firm produces? Why?

(c) What do you predict will happen to the number of firms in the industry? Why?

(d) What do you predict will happen to supply and the market price?

(e) At which price must the firm shut down?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

25

Using the following diagram, demonstrate that producing at the level of output associated with maximum per unit profit (minimum of the ATC curve) does not maximize total profit.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

26

Consider the following table of numbers, which represents demand and cost conditions for a competitive firm. What output level should the firm produce? Explain. NOTE: Marginal values represent values between levels of output. For example, the marginal cost between 0 units and 1 unit is $240.

NOTE: Marginal values represent values between levels of output. For example, the marginal cost between 0 units and 1 unit is $240. Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

27

Consider the following diagram: Would a perfectly competitive firm facing these conditions stay in business in the short run? Demonstrate your answer by comparing the loss if it stayed open to the loss if it closed.

Would a perfectly competitive firm facing these conditions stay in business in the short run? Demonstrate your answer by comparing the loss if it stayed open to the loss if it closed. Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

28

Study the graph below and answer the following questions. (a) Is this firm making profit by producing 500 units in the short run? Why or why not?

(b) What will happen in the long run in this industry?

(c) Will the firm survive in this industry?

(a) Is this firm making profit by producing 500 units in the short run? Why or why not?(b) What will happen in the long run in this industry?

(c) Will the firm survive in this industry?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

29

Demonstrate graphically and explain verbally how a perfectly competitive firm's MC curve is its supply curve.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

30

Demonstrate graphically and explain verbally the case of a constant-cost industry in a perfectly competitive market. Draw both a firm and a market diagram. HINT: The long-run market supply curve in your diagram should be perfectly elastic (i.e., horizontal).

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

31

The American Widget Corporation (AWC) is a profit-maximizing and perfectly competitive firm that is currently experiencing a loss. However, the market price of widgets is expected to increase in the near future. The company's vice-president, Alan R. ("Big Tuna") Burns, has recommended against increasing output in response to a higher price for widgets. His argument is that the marginal cost of the additional units of output will increase, and these higher costs will worsen AWC's losses. Evaluate this argument using an appropriate picture.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

32

Demonstrate graphically and explain verbally where the level of output should be when a perfectly competitive firm is earning a positive economic profit. Be sure to label the profit maximizing level of output and shade in the area that represents profit.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

33

Using the following diagram, demonstrate graphically and explain verbally why any movement away from output level Q0 would decrease the firm's profit.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

34

Demonstrate graphically and explain verbally a perfectly competitive firms' long run equilibrium situation (be sure to show the long-run average total cost curve, short-run average total cost curve, marginal curve, and marginal revenue curve).

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

35

Consider the following diagram of a representative competitive firm: Is this a long-run equilibrium situation? If yes, explain why it is. If no, explain what will happen to transform it into a long-run equilibrium situation.

Is this a long-run equilibrium situation? If yes, explain why it is. If no, explain what will happen to transform it into a long-run equilibrium situation. Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 35 flashcards in this deck.