Deck 7: Job Costing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

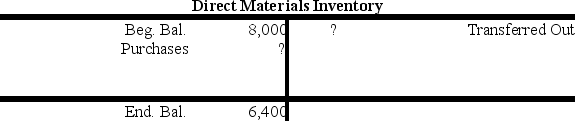

Question

Question

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the value of the ending Work-in-Process inventory balance?

A) $0.

B) $4,200.

C) $7,500.

D) $8,000.

-

What is the value of the ending Work-in-Process inventory balance?

A) $0.

B) $4,200.

C) $7,500.

D) $8,000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the amount of the materials purchased?

A) $14,400.

B) $16,400.

C) $18,000.

D) $19,600.

-

What is the amount of the materials purchased?

A) $14,400.

B) $16,400.

C) $18,000.

D) $19,600.

Question

Question

Question

Question

Question

Question

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the value of the beginning Finished Goods Inventory?

A) $0.

B) $4,200.

C) $13,300.

D) $21,700.

-

What is the value of the beginning Finished Goods Inventory?

A) $0.

B) $4,200.

C) $13,300.

D) $21,700.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

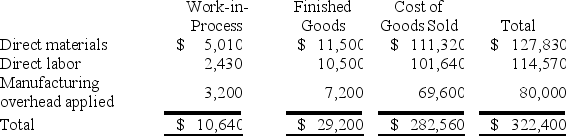

Carson Inc. has provided the following data for the month of May. There were no beginning inventories; consequently, the direct materials, direct labor, and manufacturing overhead applied listed below are all for the current month.

Manufacturing overhead for the month was underapplied by $10,000.

The company allocates any underapplied or overapplied overhead among work-in-process, finished goods, and cost of goods sold at the end of the month on the basis of the overhead applied during the month in those accounts.

The journal entry to record the allocation of any underapplied or overapplied overhead for May would include a:

A) credit to Finished Goods Inventory of $900.

B) debit to Finished Goods Inventory of $29,200.

C) credit to Finished Goods Inventory of $29,200.

D) debit to Finished Goods Inventory of $900.

Manufacturing overhead for the month was underapplied by $10,000.

The company allocates any underapplied or overapplied overhead among work-in-process, finished goods, and cost of goods sold at the end of the month on the basis of the overhead applied during the month in those accounts.

The journal entry to record the allocation of any underapplied or overapplied overhead for May would include a:

A) credit to Finished Goods Inventory of $900.

B) debit to Finished Goods Inventory of $29,200.

C) credit to Finished Goods Inventory of $29,200.

D) debit to Finished Goods Inventory of $900.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/159

Play

Full screen (f)

Deck 7: Job Costing

1

It is unethical to intentionally charge costs to the wrong job.

True

2

The predetermined overhead rate is computed by dividing the estimated manufacturing overhead costs by the estimated activity of the allocation base.

True

3

Most major projects require budget and completion stage revisions at certain intervals due to their inherent uncertainty.

True

4

Normal costing uses the actual allocation base activity to apply manufacturing overhead costs to jobs during the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

5

Job shops have three types of inventory accounts: Direct Materials, Work-in-Process, and Finished Goods.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

6

Service organizations generally use the same job costing procedures as manufacturers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

7

At the end of the accounting period, manufacturing overhead costs are applied to uncompleted jobs using the same predetermined overhead rate that is used to apply manufacturing overhead costs to completed jobs.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

8

Actual costing does not use a predetermined overhead rate to apply manufacturing overhead costs to jobs completed during the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

9

Overapplied overhead occurs when the actual overhead costs incurred during a period are greater than the overhead costs applied during the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

10

A job is a product or service that can be easily and conveniently distinguished from other products/services.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

11

The journal entry to record actual manufacturing overhead for indirect labor debits Manufacturing Overhead Control and credits Work-in-Process inventory.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

12

Underapplied overhead occurs when the actual overhead costs incurred during a period are greater than the overhead costs applied during the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

13

The journal entry to apply manufacturing overhead costs to completed jobs credits either Applied Manufacturing Overhead or Manufacturing Overhead Control.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

14

Job cost sheets are used in accounting systems as a subsidiary ledger for the Work-in-Process account.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

15

Accounting for direct materials and direct labor is easier than accounting for manufacturing overhead costs.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

16

Service organizations, by their nature, cannot have a balance in Work-in-Process Inventory.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

17

The cost in the ending Finished Goods inventory account consists of the direct materials, direct labor, and manufacturing overhead of all jobs still in process at the end of the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

18

The periodic allocation of manufacturing overhead costs to job cost sheets is based on an event, not a transaction.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

19

Indirect materials and indirect labor are two examples of manufacturing overhead costs.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

20

The journal entry to record actual manufacturing overhead for indirect materials debits Manufacturing Overhead Control and credits Accounts Payable.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following companies would most likely use job costing?

A) Paper manufacturer.

B) Paint producer.

C) Breakfast cereal maker.

D) Advertising agency.

A) Paper manufacturer.

B) Paint producer.

C) Breakfast cereal maker.

D) Advertising agency.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

22

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the value of the ending Work-in-Process inventory balance?

A) $0.

B) $4,200.

C) $7,500.

D) $8,000.

-

What is the value of the ending Work-in-Process inventory balance?

A) $0.

B) $4,200.

C) $7,500.

D) $8,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

23

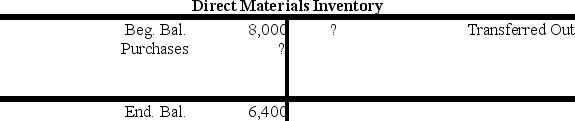

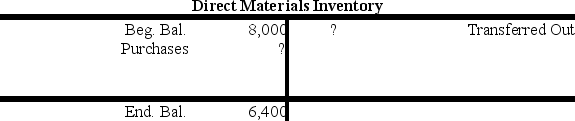

Compute the Work-in-Process transferred to the finished goods warehouse on April 30 using the following information:

A) $650.

B) $675.

C) $700.

D) $750.

A) $650.

B) $675.

C) $700.

D) $750.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

24

The journal entry to record the requisition of direct materials for new jobs started during the period is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

25

The following events took place at a manufacturing company for the current year:

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

-

What is the value of the ending Work-in-Process Inventory?

A) $13,261.50.

B) $14,259.00.

C) $88,410.00.

D) $95,060.50.

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

-

What is the value of the ending Work-in-Process Inventory?

A) $13,261.50.

B) $14,259.00.

C) $88,410.00.

D) $95,060.50.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following documents would be used as the basis for posting to the direct labor section of the job cost sheet?

A) Purchase requisition.

B) Purchase order.

C) Receiving report.

D) Time card.

A) Purchase requisition.

B) Purchase order.

C) Receiving report.

D) Time card.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is used as the basis for posting to the direct materials section of the job cost sheet?

A) Purchase requisition.

B) Materials requisition.

C) Receiving report.

D) Purchase order.

A) Purchase requisition.

B) Materials requisition.

C) Receiving report.

D) Purchase order.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

28

The following events took place at a manufacturing company for the current year:

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

-

What is the company's Cost of Goods Sold?

A) $164,190.00.

B) $139,561.50.

C) $252,600.00.

D) $214,710.50.

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

-

What is the company's Cost of Goods Sold?

A) $164,190.00.

B) $139,561.50.

C) $252,600.00.

D) $214,710.50.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

29

The following events took place at a manufacturing company for the current year:

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

What is the value of the ending Finished Goods Inventory?

A) $13,261.50.

B) $24,628.50.

C) $26,481.00.

D) $164,190.00.

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

What is the value of the ending Finished Goods Inventory?

A) $13,261.50.

B) $24,628.50.

C) $26,481.00.

D) $164,190.00.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following accounts is used to accumulate the actual manufacturing overhead costs incurred during a period?

A) Applied Manufacturing Overhead.

B) Work-in-Process Inventory.

C) Manufacturing Overhead Control.

D) Cost of Goods Sold.

A) Applied Manufacturing Overhead.

B) Work-in-Process Inventory.

C) Manufacturing Overhead Control.

D) Cost of Goods Sold.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

31

Stock Co. uses a job costing system. The following debits (credits) appeared in Stock's work-in-process account for the month of April:

Stock applies overhead to production at a predetermined rate of 80% of direct labor cost. Job No. 5, the only job still in process on April 30 has been charged with direct labor of $2,000. What was the amount of direct materials charged to Job No. 5? (CPA adapted)

A) $3,000.

B) $5,200.

C) $8,800.

D) $24,000.

Stock applies overhead to production at a predetermined rate of 80% of direct labor cost. Job No. 5, the only job still in process on April 30 has been charged with direct labor of $2,000. What was the amount of direct materials charged to Job No. 5? (CPA adapted)

A) $3,000.

B) $5,200.

C) $8,800.

D) $24,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

32

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the amount of the materials purchased?

A) $14,400.

B) $16,400.

C) $18,000.

D) $19,600.

-

What is the amount of the materials purchased?

A) $14,400.

B) $16,400.

C) $18,000.

D) $19,600.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

33

For which of the following businesses would a job costing system be appropriate?

A) Auto repair shop.

B) Crude oil refinery.

C) Drug manufacturer.

D) Root beer producer.

A) Auto repair shop.

B) Crude oil refinery.

C) Drug manufacturer.

D) Root beer producer.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is not a characteristic of job costing?

A) Each job is distinguishable from other jobs.

B) Identical units are produced on an ongoing basis.

C) Job cost data are used for setting prices and bids.

D) It is possible to compare actual costs with estimated costs.

A) Each job is distinguishable from other jobs.

B) Identical units are produced on an ongoing basis.

C) Job cost data are used for setting prices and bids.

D) It is possible to compare actual costs with estimated costs.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

35

The journal entry to record the completion of a job in a job costing system is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

36

The journal entry to record the actual manufacturing overhead costs for indirect materials is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

37

The journal entry to record the issuance of direct materials represented by the following materials requisitions for the month includes:

A) a debit to Materials Inventory, $15,945.

B) a debit to Materials Inventory, $16,670.

C) a debit to Work-in-Process Inventory, $15,945.

D) a credit to Work-in-Process Inventory, $15,945.

A) a debit to Materials Inventory, $15,945.

B) a debit to Materials Inventory, $16,670.

C) a debit to Work-in-Process Inventory, $15,945.

D) a credit to Work-in-Process Inventory, $15,945.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

38

The financial records for the Harrison Manufacturing Company have been destroyed in a fire. The following information has been obtained from a separate set of books maintained by the cost accountant. The cost accountant now asks for your assistance in computing the missing amounts.

-

What is the value of the beginning Finished Goods Inventory?

A) $0.

B) $4,200.

C) $13,300.

D) $21,700.

-

What is the value of the beginning Finished Goods Inventory?

A) $0.

B) $4,200.

C) $13,300.

D) $21,700.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

39

The following events took place at a manufacturing company for the current year:

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

What is the journal entry to record the direct labor costs for the period?

A) Option A

B) Option B

C) Option C

D) Option D

(1) Purchased $95,000 in direct materials.

(2) Incurred labor costs as follows: (a) direct, $56,000 and (b) indirect, $13,600.

(3) Other manufacturing overhead was $107,000, excluding indirect labor.

(4) Transferred 80% of the materials to the manufacturing assembly line.

(5) Completed 65% of the Work-in-Process during the year.

(6) Sold 85% of the completed goods.

(7) There were no beginning inventories.

What is the journal entry to record the direct labor costs for the period?

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following statements is(are) true regarding product costing?

(A) A job is a cost object that can be easily and conveniently distinguished from other cost objects.

(B) Job cost sheets are used in accounting systems as a subsidiary ledger for the Work-in-Process account.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

(A) A job is a cost object that can be easily and conveniently distinguished from other cost objects.

(B) Job cost sheets are used in accounting systems as a subsidiary ledger for the Work-in-Process account.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

41

Delgato Corporation, a manufacturing company, has provided data concerning its operations for September. The beginning balance in the raw materials account was $37,000 and the ending balance was $29,000. Raw materials purchases during the month totaled $57,000. Manufacturing overhead cost incurred during the month was $102,000, of which $2,000 consisted of raw materials classified as indirect materials. The direct materials cost for November was:

A) $63,000.

B) $57,000.

C) $65,000.

D) $49,000.

A) $63,000.

B) $57,000.

C) $65,000.

D) $49,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

42

In a job costing system, direct material cost is ordinarily debited to:

A) Manufacturing Overhead.

B) Cost of Goods Sold.

C) Finished Goods Inventory.

D) Work-in-Process Inventory.

A) Manufacturing Overhead.

B) Cost of Goods Sold.

C) Finished Goods Inventory.

D) Work-in-Process Inventory.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

43

The Falcon Company does not maintain backup documents for its computer files. In June, some of the current data were lost, and you have been asked to help reconstruct the data. The following beginning balances on June 1 are known:

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the ending balance in the Work-in-Process Inventory on June 30?

A) $4,800.

B) $5,300.

C) $9,300.

D) $9,800.

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the ending balance in the Work-in-Process Inventory on June 30?

A) $4,800.

B) $5,300.

C) $9,300.

D) $9,800.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

44

Fogel Flight Company uses a job costing system. The direct materials for Job #045391 were purchased in September and put into production in October. The job was not completed by the end of October. At the end of October, in what account would the direct materials cost assigned to Job #045391 be located?

A) Raw Materials Inventory.

B) Work-in-Process Inventory.

C) Finished Goods Inventory.

D) Cost of Goods Manufactured.

A) Raw Materials Inventory.

B) Work-in-Process Inventory.

C) Finished Goods Inventory.

D) Cost of Goods Manufactured.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

45

What document is used to determine the actual amount of direct labor to record on a job cost sheet?

A) Time ticket.

B) Payroll register.

C) Production order.

D) Wages payable account.

A) Time ticket.

B) Payroll register.

C) Production order.

D) Wages payable account.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

46

The balance in the Work-in-Process Inventory account equals:

A) the balance in the Finished Goods Inventory account.

B) the balance in the Cost of Goods Sold account.

C) the balances on the job cost sheets of uncompleted jobs.

D) the balance in the Manufacturing Overhead account.

A) the balance in the Finished Goods Inventory account.

B) the balance in the Cost of Goods Sold account.

C) the balances on the job cost sheets of uncompleted jobs.

D) the balance in the Manufacturing Overhead account.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

47

Grayson Inc. has provided the following data for the month of October. The balance in the Finished Goods Inventory account at the beginning of the month was $49,000 and at the end of the month was $45,000. The cost of goods manufactured for the month was $226,000. The actual manufacturing overhead cost incurred was $74,000 and the manufacturing overhead cost applied to Work-in-Process was $70,000. The adjusted cost of goods sold that would appear on the income statement for October is:

A) $226,000.

B) $230,000.

C) $222,000.

D) $234,000.

A) $226,000.

B) $230,000.

C) $222,000.

D) $234,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

48

Under Lamar Company's job costing system, manufacturing overhead is applied to Work-in-Process Inventory using a predetermined overhead rate. During June, Lamar's transactions included the following:

Lamar Company had no beginning or ending inventories. What was the cost of goods manufactured for June? (CMA adapted)

A) $302,000.

B) $310,000.

C) $322,000.

D) $330,000.

Lamar Company had no beginning or ending inventories. What was the cost of goods manufactured for June? (CMA adapted)

A) $302,000.

B) $310,000.

C) $322,000.

D) $330,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

49

The following selected data were taken from the books of the Owens O-Rings Company. The company uses job costing to account for manufacturing costs. The data relate to April operations.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

If Job 406 was sold on account for $41,500, how much gross profit would be recognized for the job?

A) $3,800.

B) $5,900.

C) $18,500.

D) $35,600.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

If Job 406 was sold on account for $41,500, how much gross profit would be recognized for the job?

A) $3,800.

B) $5,900.

C) $18,500.

D) $35,600.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

50

The following selected data were taken from the books of the Owens O-Rings Company. The company uses job costing to account for manufacturing costs. The data relate to April operations.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

The end of the month Work-in-Process Inventory balance would be:

A) $18,200.

B) $24,850.

C) $64,100.

D) $88,950.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

The end of the month Work-in-Process Inventory balance would be:

A) $18,200.

B) $24,850.

C) $64,100.

D) $88,950.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

51

The following selected data were taken from the books of the Owens O-Rings Company. The company uses job costing to account for manufacturing costs. The data relate to April operations.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

The balance in the factory overhead account would represent the fact that overhead was:

A) $1,050 underapplied.

B) $3,150 underapplied.

C) $1,250 overapplied.

D) $4,350 overapplied.

(1) Materials and supplies were requisitioned from the stores clerk as follows:

Job 405, material X, $7,000.

Job 406, material X, $3,000; material Y, $6,000.

Job 407, material X, $7,000; material Y, $3,200.

For general factory use: materials A, B, and C, $2,300.

(2) Time tickets for the month were chargeable as follows:

(3) Other information:

Factory paychecks for $36,700 were issued during the month.

Various factory overhead charges of $19,400 were incurred on account.

Depreciation of factory equipment for the month was $5,400.

Factory overhead was applied to jobs at the rate of $3.50 per direct labor hour.

Job orders completed during the month: Job 405 and Job 406.

Selling and administrative costs were $2,100.

Factory overhead is closed out only at the end of the year.

-

The balance in the factory overhead account would represent the fact that overhead was:

A) $1,050 underapplied.

B) $3,150 underapplied.

C) $1,250 overapplied.

D) $4,350 overapplied.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

52

The Falcon Company does not maintain backup documents for its computer files. In June, some of the current data were lost, and you have been asked to help reconstruct the data. The following beginning balances on June 1 are known:

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the amount of direct materials purchased during June?

A) $38,000.

B) $40,000.

C) $42,000.

D) $43,000.

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the amount of direct materials purchased during June?

A) $38,000.

B) $40,000.

C) $42,000.

D) $43,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

53

The Falcon Company does not maintain backup documents for its computer files. In June, some of the current data were lost, and you have been asked to help reconstruct the data. The following beginning balances on June 1 are known:

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the Cost of Goods Manufactured for June?

A) $89,000.

B) $84,000.

C) $94,000.

D) $99,000.

Reviewing old documents and interviewing selected employees have generated the following additional information:

The production superintendent's job cost sheets indicated that materials of $2,600 were included in the June 30 Work-in-Process Inventory. Also, 300 direct labor-hours had been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An analysis of canceled checks indicated payments of $40,000 were made to suppliers during June.

Payroll records indicate that 5,200 direct labor-hours were recorded for June. It was verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled $84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor-hours for the year and an estimated $180,000 in manufacturing overhead costs.

-

What is the Cost of Goods Manufactured for June?

A) $89,000.

B) $84,000.

C) $94,000.

D) $99,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

54

The following are Margin Co.'s production costs for December:

What amount of costs should be traced to specific products in the production process? (CPA adapted)

A) $194,000.

B) $190,000.

C) $100,000.

D) $90,000.

What amount of costs should be traced to specific products in the production process? (CPA adapted)

A) $194,000.

B) $190,000.

C) $100,000.

D) $90,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

55

Carson Inc. has provided the following data for the month of May. There were no beginning inventories; consequently, the direct materials, direct labor, and manufacturing overhead applied listed below are all for the current month.

Manufacturing overhead for the month was underapplied by $10,000.

The company allocates any underapplied or overapplied overhead among work-in-process, finished goods, and cost of goods sold at the end of the month on the basis of the overhead applied during the month in those accounts.

The journal entry to record the allocation of any underapplied or overapplied overhead for May would include a:

A) credit to Finished Goods Inventory of $900.

B) debit to Finished Goods Inventory of $29,200.

C) credit to Finished Goods Inventory of $29,200.

D) debit to Finished Goods Inventory of $900.

Manufacturing overhead for the month was underapplied by $10,000.

The company allocates any underapplied or overapplied overhead among work-in-process, finished goods, and cost of goods sold at the end of the month on the basis of the overhead applied during the month in those accounts.

The journal entry to record the allocation of any underapplied or overapplied overhead for May would include a:

A) credit to Finished Goods Inventory of $900.

B) debit to Finished Goods Inventory of $29,200.

C) credit to Finished Goods Inventory of $29,200.

D) debit to Finished Goods Inventory of $900.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

56

Pigot Corporation uses job costing and has two production departments, M and A. Budgeted manufacturing costs for the year are as follows:

The actual direct materials and direct labor costs charged to Job. No. 432 during the year were as follows:

Pigot applies manufacturing overhead to production orders on the basis of direct labor cost using departmental rates predetermined at the beginning of the year based on the annual budget. The total cost associated with Job. No. 432 for the year should be:

A) $50,000.

B) $55,000.

C) $65,000.

D) $75,000.

The actual direct materials and direct labor costs charged to Job. No. 432 during the year were as follows:

Pigot applies manufacturing overhead to production orders on the basis of direct labor cost using departmental rates predetermined at the beginning of the year based on the annual budget. The total cost associated with Job. No. 432 for the year should be:

A) $50,000.

B) $55,000.

C) $65,000.

D) $75,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

57

What are the transfers from the Finished Goods Inventory called?

A) Cost of Goods Manufactured.

B) Cost of Goods Available.

C) Cost of Goods Completed.

D) Cost of Goods Sold.

A) Cost of Goods Manufactured.

B) Cost of Goods Available.

C) Cost of Goods Completed.

D) Cost of Goods Sold.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

58

Under Eagle Co.'s job costing system, manufacturing overhead is applied to Work-in-Process using a predetermined annual overhead rate. During February, Eagle's transactions included the following:

Eagle had neither beginning nor ending inventory in Work-in-Process Inventory. What was the cost of jobs completed in February? (CPA adapted)

A) $302,000.

B) $310,000.

C) $322,000.

D) $330,000.

Eagle had neither beginning nor ending inventory in Work-in-Process Inventory. What was the cost of jobs completed in February? (CPA adapted)

A) $302,000.

B) $310,000.

C) $322,000.

D) $330,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following accounts is debited when direct labor is recorded?

A) Work-in-Process Inventory.

B) Salaries and wages expense

C) Salaries and wages payable.

D) Manufacturing overhead.

A) Work-in-Process Inventory.

B) Salaries and wages expense

C) Salaries and wages payable.

D) Manufacturing overhead.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

60

Demur Inc., a manufacturing company, has provided the following data for the month of April. The balance in the Work-in-Process Inventory account was $10,000 at the beginning of the month and $22,000 at the end of the month. During the month, the company incurred direct materials cost of $63,000 and direct labor cost of $39,000. The actual manufacturing overhead cost incurred was $40,000. The manufacturing overhead cost applied to Work-in-Process was $43,000. The cost of goods manufactured for April was:

A) $133,000.

B) $142,000.

C) $145,000.

D) $130,000.

A) $133,000.

B) $142,000.

C) $145,000.

D) $130,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

61

It is possible that the total cost of a job started in April and completed in May will not include:

A) direct materials added in April.

B) direct labor added in May.

C) applied overhead in April.

D) direct materials purchased in May.

A) direct materials added in April.

B) direct labor added in May.

C) applied overhead in April.

D) direct materials purchased in May.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

62

In a job costing system, the dollar amount in the journal entry that transfers the costs of jobs from Work-in-Process Inventory to Finished Goods Inventory is the sum of the costs charged to all jobs:

A) sold during the period.

B) completed during the period.

C) in process during the period.

D) started in process during the period.

A) sold during the period.

B) completed during the period.

C) in process during the period.

D) started in process during the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

63

Manufacturing overhead applied on the basis of direct labor-hours was $120,000, while actual manufacturing overhead incurred was $124,000 for the month of April. Which of the following is always true given the statement above?

A) Overhead was overapplied by $4,000.

B) Overhead was underapplied by $4,000.

C) Actual direct labor-hours exceeded budgeted direct labor-hours.

D) Actual direct labor-hours were less than budgeted direct labor-hours.

A) Overhead was overapplied by $4,000.

B) Overhead was underapplied by $4,000.

C) Actual direct labor-hours exceeded budgeted direct labor-hours.

D) Actual direct labor-hours were less than budgeted direct labor-hours.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following events or transactions will not result in manufacturing overhead being applied to production?

A) Completion of a job in the current period that was started in a prior period.

B) Completion of a job in the current period that was started in the current period.

C) Preparing financial statements when work is in process at the end of the period.

D) Preparing financial statements when there is no work-in-process at the end of the period.

A) Completion of a job in the current period that was started in a prior period.

B) Completion of a job in the current period that was started in the current period.

C) Preparing financial statements when work is in process at the end of the period.

D) Preparing financial statements when there is no work-in-process at the end of the period.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

65

In a traditional job costing system, the use of indirect labor in the production department increases: (CPA adapted)

A) Stores Control.

B) Work-in-Process Control.

C) Manufacturing Overhead Control.

D) Manufacturing Overhead Applied.

A) Stores Control.

B) Work-in-Process Control.

C) Manufacturing Overhead Control.

D) Manufacturing Overhead Applied.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following actions do not cause an impropriety in job costing?

A) Misstating the stage of completion.

B) Choosing to use normal costing rather than actual costing.

C) Charging costs to the wrong job.

D) Choosing an allocation method based on the results rather than choosing the method based on resource usage.

A) Misstating the stage of completion.

B) Choosing to use normal costing rather than actual costing.

C) Charging costs to the wrong job.

D) Choosing an allocation method based on the results rather than choosing the method based on resource usage.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

67

The journal entry to record the completion of a job in a job costing system is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following approaches allocates overhead by multiplying a predetermined overhead rate × actual activity?

A) Actual costing.

B) Normal costing.

C) Regression costing.

D) Standard costing.

A) Actual costing.

B) Normal costing.

C) Regression costing.

D) Standard costing.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

69

If a company multiplies its predetermined overhead rate by the actual activity level of its allocation base, it is using:

A) standard costing.

B) normal costing.

C) actual costing.

D) budget costing.

A) standard costing.

B) normal costing.

C) actual costing.

D) budget costing.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

70

The journal entry to write-off an insignificant overapplied overhead balance at the end of an accounting period for a service firm is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

71

Before prorating the manufacturing overhead costs at the end of 2020, the Cost of Goods Sold and Finished Goods Inventory accounts had applied overhead costs of $57,500 and $20,000 in them, respectively. There was no Work-in-Process at the beginning or end of 2020. During the year, manufacturing overhead costs of $74,000 were actually incurred. The balance in the Applied Manufacturing Overhead was $77,500 at the end of 2020.

- If the under or overapplied overhead is prorated between Cost of Goods Sold and the inventory accounts, how much will be allocated to the Finished Goods Inventory? (rounded to the nearest whole dollar)

A) $903.

B) $1,217.

C) $1,283.

D) $2,597.

- If the under or overapplied overhead is prorated between Cost of Goods Sold and the inventory accounts, how much will be allocated to the Finished Goods Inventory? (rounded to the nearest whole dollar)

A) $903.

B) $1,217.

C) $1,283.

D) $2,597.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

72

Underapplied overhead occurs when the balance in the Manufacturing Overhead Control account is:

A) greater than the balance in the Applied Manufacturing Overhead account.

B) equal to the balance in the Applied Manufacturing Overhead account.

C) less than the balance in the Applied Manufacturing Overhead account.

D) less than the balance in the Finished Goods Inventory account.

A) greater than the balance in the Applied Manufacturing Overhead account.

B) equal to the balance in the Applied Manufacturing Overhead account.

C) less than the balance in the Applied Manufacturing Overhead account.

D) less than the balance in the Finished Goods Inventory account.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

73

Before prorating the manufacturing overhead costs at the end of 2020, the Cost of Goods Sold and Finished Goods Inventory accounts had applied overhead costs of $57,500 and $20,000 in them, respectively. There was no Work-in-Process at the beginning or end of 2020. During the year, manufacturing overhead costs of $74,000 were actually incurred. The balance in the Applied Manufacturing Overhead was $77,500 at the end of 2020.

- If the under- or overapplied overhead is prorated between Cost of Goods Sold and the inventory accounts, what will be the Cost of Goods Sold balance after the proration? (rounded to the nearest whole dollar)

A) $58,403.

B) $56,597.

C) $60,197.

D) $54,903.

- If the under- or overapplied overhead is prorated between Cost of Goods Sold and the inventory accounts, what will be the Cost of Goods Sold balance after the proration? (rounded to the nearest whole dollar)

A) $58,403.

B) $56,597.

C) $60,197.

D) $54,903.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

74

The journal entry to write-off a significant underapplied overhead balance at the end of an accounting period is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

75

If a company multiplies its actual overhead rate by the actual activity level of its allocation base, it is using:

A) standard costing.

B) normal costing.

C) actual costing.

D) budget costing.

A) standard costing.

B) normal costing.

C) actual costing.

D) budget costing.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

76

The journal entry to write-off an insignificant underapplied overhead balance at the end of an accounting period is:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

77

The actual manufacturing overhead incurred at Liberty Industries during May was $59,000, while the manufacturing overhead applied to Work-in-Process was $74,000. The company's Cost of Goods Sold was $289,000 prior to closing out its Manufacturing Overhead account. The company closes out its Manufacturing Overhead account to Cost of Goods Sold. Which of the following statements is true?

A) Manufacturing overhead was overapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $274,000.

B) Manufacturing overhead was underapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $274,000.

C) Manufacturing overhead was overapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $304,000.

D) Manufacturing overhead was underapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $304,000.

A) Manufacturing overhead was overapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $274,000.

B) Manufacturing overhead was underapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $274,000.

C) Manufacturing overhead was overapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $304,000.

D) Manufacturing overhead was underapplied by $15,000; Cost of Goods Sold after closing out the Manufacturing Overhead account is $304,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements is(are) true regarding the application of manufacturing overhead?

(A) Manufacturing overhead is only recorded on the job cost sheets when financial statements are prepared or a job is completed.

(B) Overapplied overhead occurs when the actual overhead costs incurred during a period are greater than the overhead costs applied during the period.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

(A) Manufacturing overhead is only recorded on the job cost sheets when financial statements are prepared or a job is completed.

(B) Overapplied overhead occurs when the actual overhead costs incurred during a period are greater than the overhead costs applied during the period.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

79

Travis Company's records show that overhead was overapplied by $10,000 last year. This overapplied overhead was closed out to the Cost of Goods Sold account at the end of the year. In trying to determine why overhead was overapplied by such a large amount, the company has discovered that $6,000 of depreciation on factory equipment was charged to administrative expense in error. Given the above information, which of the following statements is true?

A) Manufacturing overhead was actually overapplied by $16,000 for the year.

B) The company's net income is understated by $6,000 for the year.

C) Under the circumstances posed above, the error in recording depreciation would have no effect on operating income for the year.

D) The $6,000 in depreciation should have been charged to Work-in-Process rather than to administrative expense.

A) Manufacturing overhead was actually overapplied by $16,000 for the year.

B) The company's net income is understated by $6,000 for the year.

C) Under the circumstances posed above, the error in recording depreciation would have no effect on operating income for the year.

D) The $6,000 in depreciation should have been charged to Work-in-Process rather than to administrative expense.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

80

The predetermined overhead rate for manufacturing overhead for 2020 is $4.00 per direct labor hour. Employees are expected to earn $5.00 per hour and the company is planning on paying its employees $100,000 during the year. However, only 75% of the employees are classified as "direct labor." What was the estimated manufacturing overhead for 2020?

A) $60,000.

B) $75,000.

C) $80,000.

D) $93,750.

A) $60,000.

B) $75,000.

C) $80,000.

D) $93,750.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 159 flashcards in this deck.