Deck 15: Tax Considerations in the Administration of Estates

Full screen (f)

Question

MATCHING

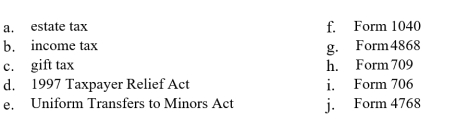

The United States Estate Tax Return

The United States Estate Tax Return

Question

MATCHING

Tax levied on wages,rents,pensions,annuities,royalties,alimony,and dividends

Tax levied on wages,rents,pensions,annuities,royalties,alimony,and dividends

Question

MATCHING

Tax levied on a donee who transfers property during life

Tax levied on a donee who transfers property during life

Question

Question

MATCHING

The United States Gift Tax Return

The United States Gift Tax Return

Question

Question

Question

Question

MATCHING

A law that replaced the unified credit with an applicable credit amount

A law that replaced the unified credit with an applicable credit amount

Question

MATCHING

The Application for Extension of Time to File a Return and/or Pay United States Estate Taxes

The Application for Extension of Time to File a Return and/or Pay United States Estate Taxes

Question

Question

MATCHING

The United States Individual Income Tax Return

The United States Individual Income Tax Return

Question

Question

Question

MATCHING

The Application for Automatic Extension of Time to File a United States Individual Income Tax Return

The Application for Automatic Extension of Time to File a United States Individual Income Tax Return

Question

MATCHING

Tax levied on an estate for the transfer of property upon death

Tax levied on an estate for the transfer of property upon death

Question

Question

MATCHING

A law that allows any kind of real or personal property to be transferred to a custodianship as a gift to a minor

A law that allows any kind of real or personal property to be transferred to a custodianship as a gift to a minor

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/30

Play

Full screen (f)

Deck 15: Tax Considerations in the Administration of Estates

1

MATCHING

The United States Estate Tax Return

The United States Estate Tax Return

I

2

MATCHING

Tax levied on wages,rents,pensions,annuities,royalties,alimony,and dividends

Tax levied on wages,rents,pensions,annuities,royalties,alimony,and dividends

B

3

MATCHING

Tax levied on a donee who transfers property during life

Tax levied on a donee who transfers property during life

C

4

Any state in which a decedent held property may impose estate tax on the decedent's estate.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

5

MATCHING

The United States Gift Tax Return

The United States Gift Tax Return

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

6

The personal representative is generally responsible for paying all taxes out of estate assets.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

7

Death tax payments are assessed against all income brackets,from the poor to the wealthy.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

8

Estate tax is a type of death tax.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

9

MATCHING

A law that replaced the unified credit with an applicable credit amount

A law that replaced the unified credit with an applicable credit amount

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

10

MATCHING

The Application for Extension of Time to File a Return and/or Pay United States Estate Taxes

The Application for Extension of Time to File a Return and/or Pay United States Estate Taxes

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

11

Every transferor is allowed a lifetime exemption from the generation-skipping transfer tax.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

12

MATCHING

The United States Individual Income Tax Return

The United States Individual Income Tax Return

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

13

Trust income is not subject to federal income tax.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

14

The federal unified gift and estate tax rate is a progressive and cumulative tax.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

15

MATCHING

The Application for Automatic Extension of Time to File a United States Individual Income Tax Return

The Application for Automatic Extension of Time to File a United States Individual Income Tax Return

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

16

MATCHING

Tax levied on an estate for the transfer of property upon death

Tax levied on an estate for the transfer of property upon death

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

17

All states have adopted the Uniform Transfers to Minors Act.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

18

MATCHING

A law that allows any kind of real or personal property to be transferred to a custodianship as a gift to a minor

A law that allows any kind of real or personal property to be transferred to a custodianship as a gift to a minor

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

19

The gross estate is the taxable estate.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

20

After a decedent's death,his or her estate is a new legal entity.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following states imposes an inheritance tax on successors?

A)Kentucky

B)Minnesota

C)South Carolina

D)Wyoming

A)Kentucky

B)Minnesota

C)South Carolina

D)Wyoming

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

22

Which does NOT generally have to be filed by April 15?

A)Federal Estate Tax Return

B)Federal Income Tax Return

C)Federal Gift Tax Return

D)Most state income tax returns

A)Federal Estate Tax Return

B)Federal Income Tax Return

C)Federal Gift Tax Return

D)Most state income tax returns

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

23

Which is an example of a Qualified Terminable Interest Property QTIP)property?

A)A trust with a life interest to the surviving spouse and remainder to the children

B)An automobile

C)A homestead

D)A life insurance policy with a one-time lump sum payment to the surviving spouse

A)A trust with a life interest to the surviving spouse and remainder to the children

B)An automobile

C)A homestead

D)A life insurance policy with a one-time lump sum payment to the surviving spouse

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

24

Which is NOT a reason that many people die without a valid will?

A)Inheritance tax

B)Estate tax

C)Gift tax

D)Income tax

A)Inheritance tax

B)Estate tax

C)Gift tax

D)Income tax

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

25

Which state has a state income tax?

A)New York

B)Nevada

C)Washington

D)Florida

A)New York

B)Nevada

C)Washington

D)Florida

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

26

Bob and Mary have a son,Steven,and a granddaughter,Kelly.If Bob made a transfer of interest in property to Kelly,who would be the skip person?

A)Kelly

B)Bob

C)Mary

D)Steven

A)Kelly

B)Bob

C)Mary

D)Steven

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

27

A testator's estate is entitled to the marital deduction if:

A)There is a surviving spouse and the decedent leaves all or a portion of the estate to him or her.

B)There is a surviving heir other than the spouse,and the decedent leaves all or a portion of the estate to the surviving heir.

C)There is no surviving spouse,but had there been,the decedent would have left all or a portion of the estate to him or her.

D)The marital deduction is not allowed because it has been repealed.

A)There is a surviving spouse and the decedent leaves all or a portion of the estate to him or her.

B)There is a surviving heir other than the spouse,and the decedent leaves all or a portion of the estate to the surviving heir.

C)There is no surviving spouse,but had there been,the decedent would have left all or a portion of the estate to him or her.

D)The marital deduction is not allowed because it has been repealed.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

28

Which does the personal representative NOT have to file?

A)Federal Sales Tax Return

B)State Estate Tax Return

C)Federal Individual Income Tax Return

D)State Individual Income Tax Return

A)Federal Sales Tax Return

B)State Estate Tax Return

C)Federal Individual Income Tax Return

D)State Individual Income Tax Return

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

29

Which CANNOT be subtracted from the gross estate to determine the taxable estate?

A)The lessening of the value of estate assets

B)Charitable deductions

C)Certain expenses,liens,and encumbrances

D)Marital deduction

A)The lessening of the value of estate assets

B)Charitable deductions

C)Certain expenses,liens,and encumbrances

D)Marital deduction

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

30

A joint federal tax return can be filed for the decedent ONLY if:

A)The surviving spouse agrees to file a joint return.

B)The surviving spouse remarried before the close of the year.

C)The surviving spouse lives in a different state.

D)The decedent was employed prior to his or her death.

A)The surviving spouse agrees to file a joint return.

B)The surviving spouse remarried before the close of the year.

C)The surviving spouse lives in a different state.

D)The decedent was employed prior to his or her death.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 30 flashcards in this deck.