Deck 5: Production and Cost Analysis in the Short Run

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

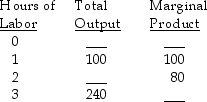

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the marginal product of the third hour of labor?

A) 60

B) 80

C) 100

D) 240

Refer to Scenario 1. What is the marginal product of the third hour of labor?

A) 60

B) 80

C) 100

D) 240

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. The production function illustrated in the table:

A) incurs diminishing marginal returns beyond the first unit of labor.

B) incurs diminishing marginal returns beyond the second unit of labor.

C) incurs diminishing marginal returns beyond the third unit of labor.

D) does not incur diminishing marginal returns because marginal product is positive for each unit of labor employed.

Refer to Scenario 1. The production function illustrated in the table:

A) incurs diminishing marginal returns beyond the first unit of labor.

B) incurs diminishing marginal returns beyond the second unit of labor.

C) incurs diminishing marginal returns beyond the third unit of labor.

D) does not incur diminishing marginal returns because marginal product is positive for each unit of labor employed.

Question

Question

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the total output when 2 hours of labor are employed?

A) 80

B) 100

C) 180

D) 200

Refer to Scenario 1. What is the total output when 2 hours of labor are employed?

A) 80

B) 100

C) 180

D) 200

Question

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the average product of the first three hours of labor?

A) 60

B) 80

C) 100

D) 240

Refer to Scenario 1. What is the average product of the first three hours of labor?

A) 60

B) 80

C) 100

D) 240

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Refer to Scenario 2. Diminishing marginal returns starts to occur between units:

A) 2 and 3.

B) 3 and 4.

C) 4 and 5.

D) 5 and 6.

Question

Question

Question

Refer to Scenario 3. The marginal cost of producing the sixth unit of output is:

A) $33.33 approximate).

B) $55.

C) $200.

D) $250.

Question

Question

Question

Refer to Scenario 2. The marginal cost of the sixth unit of output is:

A) $1.33.

B) $7.50.

C) $8.00.

D) $45.00.

Question

Question

Question

Question

Refer to Scenario 3. Diminishing marginal returns are incurred when output is increased from:

A) 1 to 2 units of output.

B) 2 to 3 units of output.

C) 3 to 4 units of output.

D) 4 to 5 units of output.

Question

Refer to Scenario 3. The average variable cost of producing three units of output is:

A) $15.

B) $25.

C) $41.67 approximate).

D) $75.

Question

Question

Question

Question

Refer to Scenario 3. The average total cost of 5 units of output is

A) $8.

B) $10.

C) $29.

D) $39.

Question

Question

Refer to Scenario 2. The average fixed cost of 2 units of output is:

A) $8.00.

B) $8.50.

C) $12.00.

D) $20.50.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/101

Play

Full screen (f)

Deck 5: Production and Cost Analysis in the Short Run

1

The term "fixed input" refers to:

A) inputs to production that do not vary with respect to quality.

B) inputs to production that do not vary in price.

C) inputs to production that yield a constant or "fixed" marginal product.

D) inputs to production, the quantity of which cannot be varied in the short run.

A) inputs to production that do not vary with respect to quality.

B) inputs to production that do not vary in price.

C) inputs to production that yield a constant or "fixed" marginal product.

D) inputs to production, the quantity of which cannot be varied in the short run.

D

2

Assume a factory that currently employs 25 workers and owns a factory with 10,000 square feet of floor space is considering doubling the size of its factory. Economists would classify this as:

A) a short-run decision.

B) a long-run decision.

C) neither a short-run nor a long-run decision.

D) both a short-run and a long-run decision.

A) a short-run decision.

B) a long-run decision.

C) neither a short-run nor a long-run decision.

D) both a short-run and a long-run decision.

B

3

The marginal product of a variable input is calculated as:

A) the change in total product divided by the change in output.

B) total product divided by the change in the variable input.

C) the change in total product divided by the change in the variable input.

D) total product divided by the total quantity of the variable input.

A) the change in total product divided by the change in output.

B) total product divided by the change in the variable input.

C) the change in total product divided by the change in the variable input.

D) total product divided by the total quantity of the variable input.

C

4

The average product of a variable input is calculated as:

A) total product divided by total output.

B) the change in total product divided by the change in the variable input.

C) total product divided by the change in the variable input.

D) total product divided by the total quantity of the variable input.

A) total product divided by total output.

B) the change in total product divided by the change in the variable input.

C) total product divided by the change in the variable input.

D) total product divided by the total quantity of the variable input.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

5

In the context of a production function, the remote order takers in the fast food industry would be classified as:

A) a fixed input.

B) a marginal input.

C) a variable input.

D) an inframarginal input.

A) a fixed input.

B) a marginal input.

C) a variable input.

D) an inframarginal input.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following would be classified as a short-run decision?

A) A firm's decision to decrease in the amount of electricity used in day -to-day operations by encouraging employees to adopt conservation strategies, e.g., shut off lights when leaving a room.

B) A restaurant's decision to increase the number of patrons it can accommodate by adding on a new dining room.

C) A trucking firm's decision to move to a smaller facility.

D) A university's decision to add a new residence hall.

A) A firm's decision to decrease in the amount of electricity used in day -to-day operations by encouraging employees to adopt conservation strategies, e.g., shut off lights when leaving a room.

B) A restaurant's decision to increase the number of patrons it can accommodate by adding on a new dining room.

C) A trucking firm's decision to move to a smaller facility.

D) A university's decision to add a new residence hall.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

7

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the marginal product of the third hour of labor?

A) 60

B) 80

C) 100

D) 240

Refer to Scenario 1. What is the marginal product of the third hour of labor?

A) 60

B) 80

C) 100

D) 240

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

8

Consider the production function for bottled water. All of the following would be considered variable inputs except:

A) the plastic bottles.

B) the water the bottles are filled with.

C) the machine used to fill each bottle.

D) the electricity used to power the machine used to fill the bottles.

A) the plastic bottles.

B) the water the bottles are filled with.

C) the machine used to fill each bottle.

D) the electricity used to power the machine used to fill the bottles.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

9

Assume a factory that currently employs 25 workers is considering adding another 5 workers to its payroll. Economists would classify this as:

A) a short-run decision.

B) a long-run decision.

C) neither a short-run nor a long-run decision.

D) both a short-run and a long-run decision.

A) a short-run decision.

B) a long-run decision.

C) neither a short-run nor a long-run decision.

D) both a short-run and a long-run decision.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

10

The amount of output a firm can produce with a given quantity of fixed and variable inputs is called:

A) total product.

B) average variable product.

C) marginal product.

D) total fixed product.

A) total product.

B) average variable product.

C) marginal product.

D) total fixed product.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

11

In the mathematical formulation of the short-run production function:

A) the quantity of output is usually assumed to be fixed.

B) the quantity of capital employed is usually assumed to be fixed.

C) the quantity of both labor and capital employed are usually assumed to be fixed.

D) the quantity of both labor and capital must be allowed to vary so that output can vary in the short run.

A) the quantity of output is usually assumed to be fixed.

B) the quantity of capital employed is usually assumed to be fixed.

C) the quantity of both labor and capital employed are usually assumed to be fixed.

D) the quantity of both labor and capital must be allowed to vary so that output can vary in the short run.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

12

A firm's production function is the relationship between:

A) the inputs employed by the firm and the resulting costs of production.

B) the factors of production and the resulting outputs of the production process.

C) the demand for a firm's output and the quantity it is able to produce with available resources.

D) the firm's production costs and the amount of revenue it receives from the sale of its output.

A) the inputs employed by the firm and the resulting costs of production.

B) the factors of production and the resulting outputs of the production process.

C) the demand for a firm's output and the quantity it is able to produce with available resources.

D) the firm's production costs and the amount of revenue it receives from the sale of its output.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

13

The amount of output produced with an additional unit of variable input is referred to as:

A) total product.

B) average variable product.

C) marginal product.

D) average fixed product.

A) total product.

B) average variable product.

C) marginal product.

D) average fixed product.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

14

Assume that after the fifth worker, each additional worker a firm hires is less productive than the previous worker. Based on this information, we can conclude that beyond the fifth worker, the average product of labor will:

A) increase.

B) stay the same.

C) decrease.

D) cannot be determined without additional information.

A) increase.

B) stay the same.

C) decrease.

D) cannot be determined without additional information.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

15

The main difference between the short run and the long run is that:

A) in the short run all inputs are fixed, while in the long run all inputs are variable.

B) in the short run the firm varies all of its inputs to find the least-cost combination of inputs.

C) in the short run, at least one of the firm's input levels is fixed.

D) in the long run, the firm is making a constrained decision about how to use existing plant and equipment efficiently.

A) in the short run all inputs are fixed, while in the long run all inputs are variable.

B) in the short run the firm varies all of its inputs to find the least-cost combination of inputs.

C) in the short run, at least one of the firm's input levels is fixed.

D) in the long run, the firm is making a constrained decision about how to use existing plant and equipment efficiently.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

16

The text lists all of the following as outcomes of McDonald's experimental adoption of remote order taking except:

A) a decrease in accuracy in filling orders.

B) increased speed at the drive through window.

C) an increase in the costs associated with the drive-through portion of McDonald's business.

D) employee dissatisfaction with constant monitoring and the stress of the process.

A) a decrease in accuracy in filling orders.

B) increased speed at the drive through window.

C) an increase in the costs associated with the drive-through portion of McDonald's business.

D) employee dissatisfaction with constant monitoring and the stress of the process.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

17

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. The production function illustrated in the table:

A) incurs diminishing marginal returns beyond the first unit of labor.

B) incurs diminishing marginal returns beyond the second unit of labor.

C) incurs diminishing marginal returns beyond the third unit of labor.

D) does not incur diminishing marginal returns because marginal product is positive for each unit of labor employed.

Refer to Scenario 1. The production function illustrated in the table:

A) incurs diminishing marginal returns beyond the first unit of labor.

B) incurs diminishing marginal returns beyond the second unit of labor.

C) incurs diminishing marginal returns beyond the third unit of labor.

D) does not incur diminishing marginal returns because marginal product is positive for each unit of labor employed.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following inputs is most likely to be "fixed" in the short run?

A) Labor.

B) Capital.

C) Energy.

D) Raw Material.

A) Labor.

B) Capital.

C) Energy.

D) Raw Material.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

19

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the total output when 2 hours of labor are employed?

A) 80

B) 100

C) 180

D) 200

Refer to Scenario 1. What is the total output when 2 hours of labor are employed?

A) 80

B) 100

C) 180

D) 200

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

20

Scenario 1: The following is a hypothetical short-run production function:

Refer to Scenario 1. What is the average product of the first three hours of labor?

A) 60

B) 80

C) 100

D) 240

Refer to Scenario 1. What is the average product of the first three hours of labor?

A) 60

B) 80

C) 100

D) 240

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following statements is false?

A) Economic costs include the opportunity costs of the resources owned by the firm.

B) Accounting costs typically include only explicit costs.

C) Economic profit will always be less than accounting profit if resources owned and used by the firm have any opportunity costs.

D) Accounting profit is equal to total revenue minus implicit costs.

A) Economic costs include the opportunity costs of the resources owned by the firm.

B) Accounting costs typically include only explicit costs.

C) Economic profit will always be less than accounting profit if resources owned and used by the firm have any opportunity costs.

D) Accounting profit is equal to total revenue minus implicit costs.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is the best example of "depreciation"?

A) An individual worker becoming tired at the end of an eight-hour work day.

B) The notion that individuals obtain less utility from paying taxes than giving to charities.

C) A truck used by a pizzeria to make deliveries is worth less at the end of one year.

D) A rise in prices depreciating the value of consumers' real incomes.

A) An individual worker becoming tired at the end of an eight-hour work day.

B) The notion that individuals obtain less utility from paying taxes than giving to charities.

C) A truck used by a pizzeria to make deliveries is worth less at the end of one year.

D) A rise in prices depreciating the value of consumers' real incomes.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

23

Economic profit is equal to the difference between:

A) total revenue and the full opportunity cost of all the resources used in production.

B) total revenue and implicit costs.

C) accounting profit and explicit costs.

D) implicit and explicit costs.

A) total revenue and the full opportunity cost of all the resources used in production.

B) total revenue and implicit costs.

C) accounting profit and explicit costs.

D) implicit and explicit costs.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

24

All else constant, an increase in productivity has the effect of causing:

A) the marginal product of labor to increase and no effect on the average product of labor.

B) the average product of labor to increase and no effect on the marginal product of labor.

C) the marginal product of labor to increase and the average product of labor to decrease.

D) both the marginal and average product of labor to increase.

A) the marginal product of labor to increase and no effect on the average product of labor.

B) the average product of labor to increase and no effect on the marginal product of labor.

C) the marginal product of labor to increase and the average product of labor to decrease.

D) both the marginal and average product of labor to increase.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

25

Marginal product equals 0 when:

A) average product equals zero.

B) total product equals average product.

C) average product reached its minimum value.

D) total product reaches its maximum value.

A) average product equals zero.

B) total product equals average product.

C) average product reached its minimum value.

D) total product reaches its maximum value.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is true of the typical relationship between marginal product MP) and average product AP)?

A) If MP is greater than AP, then AP is falling.

B) The AP curve intersects the MP curve at minimum MP.

C) The MP curve intersects the AP curve at maximum AP.

D) If MP is less than AP, then AP is increasing.

A) If MP is greater than AP, then AP is falling.

B) The AP curve intersects the MP curve at minimum MP.

C) The MP curve intersects the AP curve at maximum AP.

D) If MP is less than AP, then AP is increasing.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

27

All else constant, as the amount of a firm's implicit costs increases, the difference between economic profit and accounting profit will:

A) increase.

B) stay the same.

C) decrease.

D) cannot be determined without more information.

A) increase.

B) stay the same.

C) decrease.

D) cannot be determined without more information.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

28

Fred is considering opening a ski shop in Colorado. Assume Fred will incur the following costs: building rent = $100,000/year, inventory = $250,000/year, energy = $50,000/year, and labor one clerk) = $10,000/year. In addition, Fred's current income as a computer programmer is $40,000 per year. Assuming Fred would earn $460,000 in revenues, he could expect to earn:

A) an accounting profit of $10,000 per year.

B) an accounting profit of $60,000 per year.

C) an economic profit of $10,000 per year.

D) an economic profit of $50,000 per year.

A) an accounting profit of $10,000 per year.

B) an accounting profit of $60,000 per year.

C) an economic profit of $10,000 per year.

D) an economic profit of $50,000 per year.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is not a determinant of a firm's cost functions?

A) The production function.

B) The price of labor.

C) The productivity of the firm's capital stock.

D) The price of the firm's output.

A) The production function.

B) The price of labor.

C) The productivity of the firm's capital stock.

D) The price of the firm's output.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following statements is correct?

A) Workers employed by General Motors are approximately twice as productive as their Japanese counterparts.

B) Between 1979 and 1998, Chrysler and Ford eliminated the productivity gap between all of their production facilities and their Japanese counterparts.

C) The increase in productivity Japanese manufacturers experienced in the early 1980s was the result primarily of long-run changes in management focusing on inventory systems and plant layout.

D) Auto workers in the United States are less productive than their Japanese counterparts primarily due to the higher wages U.S. workers receive.

A) Workers employed by General Motors are approximately twice as productive as their Japanese counterparts.

B) Between 1979 and 1998, Chrysler and Ford eliminated the productivity gap between all of their production facilities and their Japanese counterparts.

C) The increase in productivity Japanese manufacturers experienced in the early 1980s was the result primarily of long-run changes in management focusing on inventory systems and plant layout.

D) Auto workers in the United States are less productive than their Japanese counterparts primarily due to the higher wages U.S. workers receive.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

31

Suppose a sole proprietorship is earning total revenues of $100,000 and is incurring explicit costs of $75,000. If the owner could work for another company for $30,000 a year, we would conclude that:

A) the firm is incurring an economic loss.

B) implicit costs are $25,000.

C) the total economic costs are $100,000.

D) the individual is earning an economic profit of $25,000.

A) the firm is incurring an economic loss.

B) implicit costs are $25,000.

C) the total economic costs are $100,000.

D) the individual is earning an economic profit of $25,000.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

32

The "law of diminishing marginal returns" applies to:

A) the short run, but not the long run.

B) the long run, but not the short run.

C) both the short run and the long run.

D) neither the short run nor the long run.

A) the short run, but not the long run.

B) the long run, but not the short run.

C) both the short run and the long run.

D) neither the short run nor the long run.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

33

From the manager's perspective:

A) it is important to treat implicit costs as explicit in order to make sound strategic decisions.

B) implicit costs are simply a theoretical construct and should be ignored in the decision-making process.

C) only explicit costs matter because accounting profit is based on explicit costs.

D) there is no difference between implicit and explicit costs. As such, treating implicit costs as explicit would result in double counting and an overstatement of total costs.

A) it is important to treat implicit costs as explicit in order to make sound strategic decisions.

B) implicit costs are simply a theoretical construct and should be ignored in the decision-making process.

C) only explicit costs matter because accounting profit is based on explicit costs.

D) there is no difference between implicit and explicit costs. As such, treating implicit costs as explicit would result in double counting and an overstatement of total costs.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

34

Data on productivity gains in the 1990s in the United States strongly suggest that a significant share of those gains was attributable to:

A) improvements in education and training.

B) improvements in information technology.

C) substantial reductions in labor costs.

D) increased demand for goods and services.

A) improvements in education and training.

B) improvements in information technology.

C) substantial reductions in labor costs.

D) increased demand for goods and services.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

35

The amount of money a firm pays to lease a building it uses for office space is called:

A) the full opportunity cost of production.

B) an explicit cost.

C) a real cost of production.

D) an implicit cost.

A) the full opportunity cost of production.

B) an explicit cost.

C) a real cost of production.

D) an implicit cost.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

36

The payment of wages by a firm is an example of:

A) an explicit cost of production.

B) an implicit cost of production.

C) an irreversible cost of production.

D) a long-run cost of production.

A) an explicit cost of production.

B) an implicit cost of production.

C) an irreversible cost of production.

D) a long-run cost of production.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

37

Diminishing marginal returns occur when:

A) units of a variable input are added to a fixed input and total product falls.

B) units of a variable input are added to a fixed input and marginal product falls.

C) the size of the plant is increased in the long run.

D) the quantity of the fixed input is increased and returns to the variable input fall.

A) units of a variable input are added to a fixed input and total product falls.

B) units of a variable input are added to a fixed input and marginal product falls.

C) the size of the plant is increased in the long run.

D) the quantity of the fixed input is increased and returns to the variable input fall.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is an example of an "implicit cost"?

A) Interest that could have been earned on retained earnings used by the firm to finance expansion.

B) The payment of rent by the firm for the building in which it is housed.

C) The interest payment made by the firm for funds borrowed from a bank.

D) The payment of wages by the firm.

A) Interest that could have been earned on retained earnings used by the firm to finance expansion.

B) The payment of rent by the firm for the building in which it is housed.

C) The interest payment made by the firm for funds borrowed from a bank.

D) The payment of wages by the firm.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following statements regarding historical costs is correct?

A) Historical costs represent what the firm paid for an input when it was purchased, adjusted for inflation.

B) Historical costs vary depending on the method of depreciation a firm uses.

C) Historical costs are a good indicator of the current opportunity cost of a piece of capital.

D) Using historical costs can cause true economic profit to be under or over stated.

A) Historical costs represent what the firm paid for an input when it was purchased, adjusted for inflation.

B) Historical costs vary depending on the method of depreciation a firm uses.

C) Historical costs are a good indicator of the current opportunity cost of a piece of capital.

D) Using historical costs can cause true economic profit to be under or over stated.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

40

An implicit cost is defined as:

A) the opportunity cost of using a resource that is not explicitly paid out by the firm.

B) the difference between an input's explicit cost and its actual cost.

C) the amount by which economic profit exceeds accounting profit.

D) the amount by which the money spent on an input to production exceeds its opportunity cost.

A) the opportunity cost of using a resource that is not explicitly paid out by the firm.

B) the difference between an input's explicit cost and its actual cost.

C) the amount by which economic profit exceeds accounting profit.

D) the amount by which the money spent on an input to production exceeds its opportunity cost.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

41

If a firm experiences constant returns to the variable input in the short run,

A) marginal cost will be greater than average variable cost, but the two will become more equal as output increases.

B) marginal cost will be less than average variable cost, but the two will become more equal as output increases.

C) marginal cost will be greater than average variable cost, and the difference between the two will become larger as output increases.

D) marginal cost and average variable cost will be equal over the range of output in question.

A) marginal cost will be greater than average variable cost, but the two will become more equal as output increases.

B) marginal cost will be less than average variable cost, but the two will become more equal as output increases.

C) marginal cost will be greater than average variable cost, and the difference between the two will become larger as output increases.

D) marginal cost and average variable cost will be equal over the range of output in question.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

42

Refer to Scenario 2. Diminishing marginal returns starts to occur between units:

A) 2 and 3.

B) 3 and 4.

C) 4 and 5.

D) 5 and 6.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

43

Assume there is an improvement in technology that increases the marginal product of each unit of labor. This would have the effect of:

A) reducing the average total cost, average variable cost, and marginal cost of production.

B) increasing the average total cost, average variable cost, and marginal cost of production.

C) reducing the average variable cost and marginal cost of production, but average total cost would be unchanged.

D) reducing the average total cost and average variable cost of production, but marginal cost would be unchanged.

A) reducing the average total cost, average variable cost, and marginal cost of production.

B) increasing the average total cost, average variable cost, and marginal cost of production.

C) reducing the average variable cost and marginal cost of production, but average total cost would be unchanged.

D) reducing the average total cost and average variable cost of production, but marginal cost would be unchanged.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

44

Marginal cost is defined as:

A) the change in total cost due to a one unit change in output.

B) total cost divided by output.

C) the change in output due to a one unit change in an input.

D) total product divided by the quantity of input.

A) the change in total cost due to a one unit change in output.

B) total cost divided by output.

C) the change in output due to a one unit change in an input.

D) total product divided by the quantity of input.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

45

Refer to Scenario 3. The marginal cost of producing the sixth unit of output is:

A) $33.33 approximate).

B) $55.

C) $200.

D) $250.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

46

Assume a firm is currently producing 100 units of output, total fixed costs are $10,000, and average variable costs are $8. Based on this information we can conclude, with certainty, that the firm's:

A) marginal costs are $8.

B) total variable costs are $8000.

C) average fixed costs are $2.

D) total costs are $10,800.

A) marginal costs are $8.

B) total variable costs are $8000.

C) average fixed costs are $2.

D) total costs are $10,800.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

47

Production functions A and B result in the same average total costs of production. However, production function A is twice as capital intensive as production function B. In this case, all else constant:

A) marginal costs will be higher in A than they are in B.

B) marginal costs will be higher in B than they will in A.

C) because total costs are equal, marginal costs will be equal for the two production functions as well.

D) there is no way to say anything about the relative marginal costs of production in the two production functions without additional information.

A) marginal costs will be higher in A than they are in B.

B) marginal costs will be higher in B than they will in A.

C) because total costs are equal, marginal costs will be equal for the two production functions as well.

D) there is no way to say anything about the relative marginal costs of production in the two production functions without additional information.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

48

Refer to Scenario 2. The marginal cost of the sixth unit of output is:

A) $1.33.

B) $7.50.

C) $8.00.

D) $45.00.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following statements concerning the relationships among the firm's total cost functions is false?

A) TC = TFC + TVC

B) TVC = TFC - TC

C) TFC = TC - TVC

D) TC = TFC when output = 0.

A) TC = TFC + TVC

B) TVC = TFC - TC

C) TFC = TC - TVC

D) TC = TFC when output = 0.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following statements is correct?

A) In the short run, if a firm chooses to produce no output i.e., shut down) its total costs of production will equal its total fixed costs.

B) If a firm decides to shut down, its short-run total costs will equal 0.

C) As a firm increases output in the short run, the change in total costs is equal to the change in total variable costs.

D) A firm minimizes its total costs of production when average variable cost is minimized.

A) In the short run, if a firm chooses to produce no output i.e., shut down) its total costs of production will equal its total fixed costs.

B) If a firm decides to shut down, its short-run total costs will equal 0.

C) As a firm increases output in the short run, the change in total costs is equal to the change in total variable costs.

D) A firm minimizes its total costs of production when average variable cost is minimized.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

51

If a firm experiences constant returns to the variable input in the short run,

A) marginal product will be greater than average variable product, but the two will become more equal as output increases.

B) marginal product will be less than average variable product, but the two will become more equal as output increases.

C) marginal product will be greater than average variable product, and the difference between the two will become larger as output increases.

D) marginal product and average variable product will be equal over the range of output in question.

A) marginal product will be greater than average variable product, but the two will become more equal as output increases.

B) marginal product will be less than average variable product, but the two will become more equal as output increases.

C) marginal product will be greater than average variable product, and the difference between the two will become larger as output increases.

D) marginal product and average variable product will be equal over the range of output in question.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

52

Refer to Scenario 3. Diminishing marginal returns are incurred when output is increased from:

A) 1 to 2 units of output.

B) 2 to 3 units of output.

C) 3 to 4 units of output.

D) 4 to 5 units of output.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

53

Refer to Scenario 3. The average variable cost of producing three units of output is:

A) $15.

B) $25.

C) $41.67 approximate).

D) $75.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

54

Marginal cost is defined as the change in cost when output changes by one unit. In the short run, marginal cost can also be measured by the change in cost when output changes by one unit.

A) total; fixed

B) variable; fixed

C) fixed; variable

D) total; variable

A) total; fixed

B) variable; fixed

C) fixed; variable

D) total; variable

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

55

So long as a firm is enjoying increasing marginal returns, a one unit increase in output will cause marginal costs to and total costs to .

A) increase; increase

B) decrease; increase

C) increase; decrease

D) decrease; decrease

A) increase; increase

B) decrease; increase

C) increase; decrease

D) decrease; decrease

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is true of the relationship among the average cost functions?

A) ATC = AFC - AVC

B) AVC = AFC + ATC

C) AFC = ATC + AVC

D) AFC = ATC - AVC

A) ATC = AFC - AVC

B) AVC = AFC + ATC

C) AFC = ATC + AVC

D) AFC = ATC - AVC

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

57

Refer to Scenario 3. The average total cost of 5 units of output is

A) $8.

B) $10.

C) $29.

D) $39.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following is true of the relationship between the marginal cost function and the average total cost and average variable cost functions?

A) If MC is greater than ATC and AVC, then ATC and AVC will increase.

B) The ATC and AVC curves intersect the MC curve at minimum MC.

C) The MC curve, ATC curve, and AVC curve all intersect at the same point.

D) At each level of output, MC is equal to difference between AVC and ATC.

A) If MC is greater than ATC and AVC, then ATC and AVC will increase.

B) The ATC and AVC curves intersect the MC curve at minimum MC.

C) The MC curve, ATC curve, and AVC curve all intersect at the same point.

D) At each level of output, MC is equal to difference between AVC and ATC.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

59

Refer to Scenario 2. The average fixed cost of 2 units of output is:

A) $8.00.

B) $8.50.

C) $12.00.

D) $20.50.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

60

For a particular production function, over the range of output where marginal product rises as units of the variable input are added to the fixed input, marginal cost will be:

A) increasing.

B) constant.

C) decreasing.

D) cannot be determined without additional information.

A) increasing.

B) constant.

C) decreasing.

D) cannot be determined without additional information.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

61

The law of diminishing returns is a result of the fact that more and more units of a variable input are being added to a fixed input. Because of the limitations imposed by the fixed input, at some point the productivity of additional units of the variable input must decline.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

62

A firm's production function is the relationship between the factors of production and the resulting outputs of the production process.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

63

One of the interesting findings of a survey of firm managers by Blinder et al. is that:

A) the vast majority of firms pay considerable attention to marginal costs in making decisions about how much output to produce.

B) the majority of respondents suggested that fixed costs are a relatively unimportant consideration when making output decisions.

C) approximately 75 percent of respondents indicated that their marginal costs of production are rising over the relevant range of output.

D) a significant percentage of respondents to the survey did not appear to understand the concept of marginal cost.

A) the vast majority of firms pay considerable attention to marginal costs in making decisions about how much output to produce.

B) the majority of respondents suggested that fixed costs are a relatively unimportant consideration when making output decisions.

C) approximately 75 percent of respondents indicated that their marginal costs of production are rising over the relevant range of output.

D) a significant percentage of respondents to the survey did not appear to understand the concept of marginal cost.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

64

For a particular farmer and a single growing season, the amount of seed that is planted would be considered a variable input.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

65

Much of the empirical evidence on the behavior of costs for real-world firms suggests that:

A) average costs functions are U-shaped as suggested by economic theory.

B) for most firms, marginal costs are declining in the range in which the firms operate.

C) for many firms, marginal and average variable costs are constant over wide ranges of output.

D) there is no relationship between the marginal and average variable costs of production.

A) average costs functions are U-shaped as suggested by economic theory.

B) for most firms, marginal costs are declining in the range in which the firms operate.

C) for many firms, marginal and average variable costs are constant over wide ranges of output.

D) there is no relationship between the marginal and average variable costs of production.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

66

A firm's decision to expand the size of its production facility would be considered a short-run decision so long as the expansion can be completed in less than a year.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

67

By definition, in the typical firm's short-run production function all inputs are fixed in amount.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

68

When a firm is considering whether to buy a new piece of equipment with retained earnings, the amount of interest that could be earned on that money is an explicit cost and should be treated as such.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

69

If, for a particular short-run production, we observe that marginal product is decreasing we can conclude that average product is decreasing as well.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

70

The marginal product of a variable input is calculated by dividing total product by the change in the variable input.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

71

The "long run" is defined as a period of time long enough for the quantities of all of the inputs to production to vary.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

72

According to the text, much of the increase in productivity that has occurred more recently in the fast food industry was the result of improvements in capital and technology.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

73

All else constant, an improvement in technology would cause a firm's total, average and marginal product functions to increase graphically, shift up).

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

74

At the point where a firm incurs diminishing marginal returns, total product will begin to decline.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

75

The full opportunity costs of production are calculated as the sum of both explicit and implicit costs.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

76

The term "variable input" is used to refer to inputs that vary in terms of quality and, therefore, productivity.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

77

For a typical short-run production function, so long as marginal product is increasing, average product will be increasing as well.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

78

The typical short-run production function is incapable of distinguishing among the different types of labor that might be hired by the firm.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

79

Because it is a machine, a personal computer should be treated as a fixed input in the typical firm's short-run production function.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

80

Once a firm incurs diminishing marginal returns, total product will begin to decline as more of the variable input is employed.

Unlock Deck

Unlock for access to all 101 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 101 flashcards in this deck.