Deck 11: Internal Service Funds

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

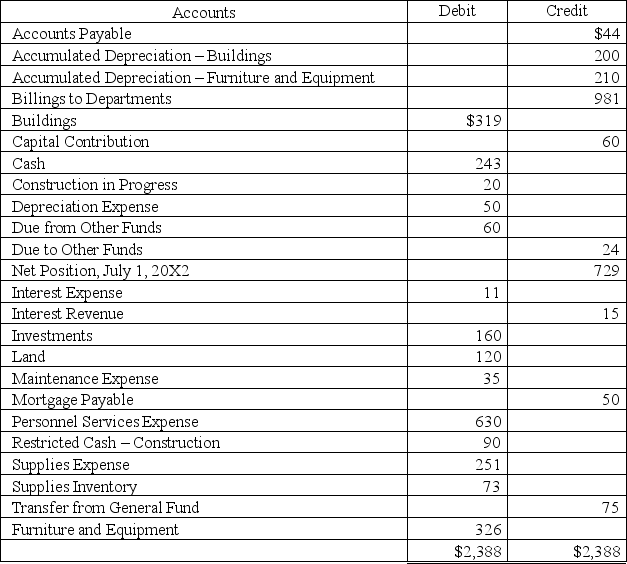

The accounts listed below are taken from an Internal Service Fund adjusted trial balance (all amounts are in thousands):

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended June 30, 20X3, for the City of Bell Buckle.

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended June 30, 20X3, for the City of Bell Buckle.

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended June 30, 20X3, for the City of Bell Buckle. Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 11: Internal Service Funds

1

Inventory in an Internal Service Fund would most likely be reflected in which of the following net position classifications?

A) Nonspendable net position.

B) Net investment in capital assets.

C) Restricted net position.

D) Unrestricted net position.

A) Nonspendable net position.

B) Net investment in capital assets.

C) Restricted net position.

D) Unrestricted net position.

D

2

The General Fund contributes $40,000 to an Internal Service Fund to subsidize its operations. The contribution is not considered to be an interfund loan. The Internal Service Fund will report this contribution as a

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

A

3

Caraway County has a Self-Insurance Internal Service Fund. If the fund purchases $100,000 of investments during the month, the

A) Fund's total assets will increase by $100,000.

B) Fund's total assets will decrease by $100,000.

C) Fund's total assets will remain the same.

D) Fund's expenditures will increase by $100,000.

A) Fund's total assets will increase by $100,000.

B) Fund's total assets will decrease by $100,000.

C) Fund's total assets will remain the same.

D) Fund's expenditures will increase by $100,000.

C

4

A municipality's Central Garage Internal Service Fund had total billings for $8,000 for the month. Of the 40 vehicles serviced, 20 were police vehicles, 10 were water department vehicles, and 10 were wastewater department vehicles. What would the journal entry be to account for this transaction?

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

The Central Warehouse Internal Service Fund purchased $15,000 of inventory on account, which was unpaid as of the month end. Which of the following statements regarding the accounting for the transaction is false?

A) Expenses in the Internal Service Fund will increase.

B) Capital assets recorded in the Internal Service Fund remain unchanged.

C) The transaction will increase total assets.

D) The transaction will increase total liabilities.

A) Expenses in the Internal Service Fund will increase.

B) Capital assets recorded in the Internal Service Fund remain unchanged.

C) The transaction will increase total assets.

D) The transaction will increase total liabilities.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

A Motor Pool Internal Service Fund purchased ten new vehicles for their fleet inventory. The fund entered into a capital lease. The capitalizable cost totaled $300,000 and there was a $50,000 down payment. The entry to record the transaction in the Internal Service Fund would be

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

The General Fund paid $4,000 to the Internal Service Fund for services rendered. Which of the following statements accurately reflects the reporting effects of the transaction?

A) The Internal Service Fund will report revenues of $4,000.

B) The Internal Service Fund will report capital contributions of $4,000.

C) The Internal Service will report a transfer in of $4,000.

D) The Internal Service Fund will record a direct adjustment to unrestricted net position.

A) The Internal Service Fund will report revenues of $4,000.

B) The Internal Service Fund will report capital contributions of $4,000.

C) The Internal Service will report a transfer in of $4,000.

D) The Internal Service Fund will record a direct adjustment to unrestricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

Interest revenue earned by an Internal Service Fund will be reported on the statement of revenues, expenses, and changes in net position as

A) Operating revenue.

B) Nonoperating revenue.

C) An other financing source.

D) A capital contribution.

A) Operating revenue.

B) Nonoperating revenue.

C) An other financing source.

D) A capital contribution.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

The use of an Internal Service Fund is mandated by generally accepted accounting principles for which of the following activities?

A) Risk financing activities.

B) Government motor pool.

C) Centralized warehouse.

D) GAAP does not require the use of an Internal Service Fund.

A) Risk financing activities.

B) Government motor pool.

C) Centralized warehouse.

D) GAAP does not require the use of an Internal Service Fund.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

The Tullahoma School District's Print Shop Internal Service Fund received $25,000 from a state grant to help subsidize the purchase of new printing equipment. The Internal Service Fund will report this contribution as a

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

A government plans to create an Internal Service Fund to account for its new central warehouse. The General Fund loans the Internal Service Fund $100,000, which is going to pay back the loan interest-free in five years. The entry in the Internal Service Fund to record this transaction would be

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

The accounts listed below are taken from an Internal Service Fund adjusted trial balance (all amounts are in thousands):

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended June 30, 20X3, for the City of Bell Buckle.

Requirements: Prepare Statement of Fund Net Position and Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended June 30, 20X3, for the City of Bell Buckle. Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

Listed below are selected transactions for the Maury County Internal Service Fund.

1. Purchased a building on January 2, 20X2, by paying $100,000 down and borrowing $350,000 on a 6%, 10-year mortgage. Assume semi-annual mortgage payments are due each June 30 and December 31, beginning this year. The building will be depreciated over 20 years with no salvage value using the straight-line method.

2. Purchased supplies on account, $58,000. The fund uses the perpetual inventory method when accounting for supplies.

3. Paid employee salaries, $120,000. Accrued salaries at year end were $13,000. Accrued salaries at the beginning of the year were $9,000.

4. Billed General Fund departments $400,000 for services provided to those departments. Billings to the Enterprise Fund totaled $30,000. 90% of these billings were collected by year end. The remaining 10% is not expected to be collected from the other funds until the second quarter of the next fiscal year.

5. The first semi-annual mortgage payment of $23,500 was made.

6. Paid $50,000 on account.

7. Supplies on hand at year end have a cost of $4,000. The beginning of the year inventory was $6,000.

8. The second semi-annual mortgage payment of $23,500 was made.

9. Record depreciation on the building for the year.

1. Prepare the journal entries required in the Internal Service Fund. If no entry is required, state "No entry required" and explain why.

2. Indicate the effects of each transaction on the accounting equation of the Internal Service Fund accounts. If an element of the equation is not affected or if the net effect is zero, put "NE" in the appropriate box. Do not leave any boxes blank.

1. Purchased a building on January 2, 20X2, by paying $100,000 down and borrowing $350,000 on a 6%, 10-year mortgage. Assume semi-annual mortgage payments are due each June 30 and December 31, beginning this year. The building will be depreciated over 20 years with no salvage value using the straight-line method.

2. Purchased supplies on account, $58,000. The fund uses the perpetual inventory method when accounting for supplies.

3. Paid employee salaries, $120,000. Accrued salaries at year end were $13,000. Accrued salaries at the beginning of the year were $9,000.

4. Billed General Fund departments $400,000 for services provided to those departments. Billings to the Enterprise Fund totaled $30,000. 90% of these billings were collected by year end. The remaining 10% is not expected to be collected from the other funds until the second quarter of the next fiscal year.

5. The first semi-annual mortgage payment of $23,500 was made.

6. Paid $50,000 on account.

7. Supplies on hand at year end have a cost of $4,000. The beginning of the year inventory was $6,000.

8. The second semi-annual mortgage payment of $23,500 was made.

9. Record depreciation on the building for the year.

1. Prepare the journal entries required in the Internal Service Fund. If no entry is required, state "No entry required" and explain why.

2. Indicate the effects of each transaction on the accounting equation of the Internal Service Fund accounts. If an element of the equation is not affected or if the net effect is zero, put "NE" in the appropriate box. Do not leave any boxes blank.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following would most likely be accounted for in an Internal Service Fund?

A) A government's water and sewer department if it provides water and sewer services to government departments as well as to residents and businesses in the community.

B) A government's central printing shop that provides a very minimal amount of services to a few outside customers.

C) The Payroll and Benefits Department of the government.

D) A consolidated supplies facility where most of the customers are other governments.

A) A government's water and sewer department if it provides water and sewer services to government departments as well as to residents and businesses in the community.

B) A government's central printing shop that provides a very minimal amount of services to a few outside customers.

C) The Payroll and Benefits Department of the government.

D) A consolidated supplies facility where most of the customers are other governments.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

Nathan Township's General Fund transfers three vehicles to the Internal Service Fund. The vehicles, which have a useful life of five years, are transferred at the end of their fourth year. The original cost for all three vehicles totaled $75,000. The entry in the Internal Service Fund would be

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

The Tullahoma School District's Print Shop Internal Service Fund received $25,000 from a state grant to help subsidize its printing operations. The Internal Service Fund will report this contribution as a

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

An Internal Service Fund had investments with an original cost of $100,000. As of the end of the fiscal year, the fair market value on these investments was $85,000. The Internal Service Fund would

A) Report expenses of $15,000.

B) Report a reduction of revenue of $15,000.

C) Not adjust the value of the investments reported on the balance sheet.

D) Report a loss on investments of $15,000.

A) Report expenses of $15,000.

B) Report a reduction of revenue of $15,000.

C) Not adjust the value of the investments reported on the balance sheet.

D) Report a loss on investments of $15,000.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

The General Fund contributes $40,000 to an Internal Service Fund to subsidize the purchase of a capital asset. The contribution is not considered to be an interfund loan. The Internal Service Fund will report this contribution as a

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

A) Transfer in.

B) Capital contribution.

C) Nonoperating revenue.

D) Direct equity adjustment to restricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

An Internal Service Fund is considered to be

A) A governmental fund.

B) A proprietary fund.

C) A fiduciary fund.

D) Either a governmental fund or a proprietary fund, depending on the nature of the activity accounted for within the fund.

A) A governmental fund.

B) A proprietary fund.

C) A fiduciary fund.

D) Either a governmental fund or a proprietary fund, depending on the nature of the activity accounted for within the fund.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

Five sections for reporting items in an Internal Service Fund Statement of Cash Flows prepared using the direct method (excluding the reconciliation of operating income to cash flows from operations) are:

A. Operating Activities

B. Noncapital Financing Activities

C. Capital and Related Financing Activities

D. Investing Activities

E. Noncash Financing and Investing Activities

Using these five sections, indicate in which section each of the following Internal Service Fund transactions should be reported. If a transaction should not be reported on the Statement of Cash Flows, indicate it using the letter "X".

1. Purchase of an Internal Service Fund capital asset for cash.

2. Providing services to other funds on a cash basis.

3. Issuing refunding bonds to refinance bonds issued 10 years ago to provide financing for capital asset acquisitions.

4. Sale of Internal Service Fund capital assets for cash.

5. Transfer from a Special Revenue Fund for the specific purpose of financing an Internal Service Fund capital asset purchase.

6. Payment of office workers' salaries.

7. Amortization of the Deferred Interest Expense Adjustment created when the capital asset debt was refunded.

8. Transfer to a Capital Projects Fund to provide financing for a general government capital asset construction project.

9. Purchases of investments with cash received from issuing bonds to finance construction of Internal Service Fund capital assets.

10. Transfer to the General Fund for the purpose of financing specific operating costs of a department accounted for in that fund.

11. Issuing bonds to provide operating cash for the Internal Service Fund.

12. Signing a capital lease for equipment to be used by activities accounted for in the Internal Service Fund.

13. Interest received during the year earned on investments.

14. Transfer the proceeds from the sale of an Internal Service Fund capital asset to the General Fund.

15. Depreciation on Internal Service Fund capital assets.

16. Proceeds of bonds issued to finance construction of Internal Service Fund capital assets.

17. Interest paid on bonds issued to finance construction of an Internal Service Fund capital asset.

18. Principal retirement payments on bonds issued to finance construction of Internal Service Fund capital assets

19. Unrealized gain on investments held at year end.

20. Receipt of a capital grant for an ongoing Internal Service Fund capital asset construction project.

A. Operating Activities

B. Noncapital Financing Activities

C. Capital and Related Financing Activities

D. Investing Activities

E. Noncash Financing and Investing Activities

Using these five sections, indicate in which section each of the following Internal Service Fund transactions should be reported. If a transaction should not be reported on the Statement of Cash Flows, indicate it using the letter "X".

1. Purchase of an Internal Service Fund capital asset for cash.

2. Providing services to other funds on a cash basis.

3. Issuing refunding bonds to refinance bonds issued 10 years ago to provide financing for capital asset acquisitions.

4. Sale of Internal Service Fund capital assets for cash.

5. Transfer from a Special Revenue Fund for the specific purpose of financing an Internal Service Fund capital asset purchase.

6. Payment of office workers' salaries.

7. Amortization of the Deferred Interest Expense Adjustment created when the capital asset debt was refunded.

8. Transfer to a Capital Projects Fund to provide financing for a general government capital asset construction project.

9. Purchases of investments with cash received from issuing bonds to finance construction of Internal Service Fund capital assets.

10. Transfer to the General Fund for the purpose of financing specific operating costs of a department accounted for in that fund.

11. Issuing bonds to provide operating cash for the Internal Service Fund.

12. Signing a capital lease for equipment to be used by activities accounted for in the Internal Service Fund.

13. Interest received during the year earned on investments.

14. Transfer the proceeds from the sale of an Internal Service Fund capital asset to the General Fund.

15. Depreciation on Internal Service Fund capital assets.

16. Proceeds of bonds issued to finance construction of Internal Service Fund capital assets.

17. Interest paid on bonds issued to finance construction of an Internal Service Fund capital asset.

18. Principal retirement payments on bonds issued to finance construction of Internal Service Fund capital assets

19. Unrealized gain on investments held at year end.

20. Receipt of a capital grant for an ongoing Internal Service Fund capital asset construction project.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

The General Fund transfers cash to provide working capital for a new Internal Service Fund. The Internal Service Fund would report this transaction in the operating statement as

A) Revenues.

B) Other financing sources.

C) Nonoperating revenues.

D) Transfer in.

A) Revenues.

B) Other financing sources.

C) Nonoperating revenues.

D) Transfer in.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

The General Fund transfers cash to provide working capital for a new Internal Service Fund. The Internal Service Fund would report this transaction in the statement of cash flows as

A) Cash flows from operating activities.

B) Cash flows from noncapital financing activities.

C) Cash flows from capital and related financing activities.

D) Cash flows from investing activities.

A) Cash flows from operating activities.

B) Cash flows from noncapital financing activities.

C) Cash flows from capital and related financing activities.

D) Cash flows from investing activities.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

If a government has more than one Internal Service Fund, they are reported in the basic financial statements

A) In separate columns for each fund.

B) In separate columns for each major Internal Service Fund.

C) As a single column by fund type.

D) Not included in the basic financial statements.

A) In separate columns for each fund.

B) In separate columns for each major Internal Service Fund.

C) As a single column by fund type.

D) Not included in the basic financial statements.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

If a Self-Insurance Internal Service Fund pays claims of $5,000 during the month, the fund will report

A) Expenses of $5,000.

B) Transfers out of $5,000.

C) Nonoperating expenses of $5,000.

D) A decrease in prepaid assets of $5,000.

A) Expenses of $5,000.

B) Transfers out of $5,000.

C) Nonoperating expenses of $5,000.

D) A decrease in prepaid assets of $5,000.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

An Internal Service Fund would report which of the following items on its balance sheet

A) Restricted fund balance.

B) Unrestricted net position.

C) Assigned fund balance.

D) Capital contributions.

A) Restricted fund balance.

B) Unrestricted net position.

C) Assigned fund balance.

D) Capital contributions.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

According to GAAP, Only City's Transportation Services Internal Service Fund must present which financial statements?

I. A Statement of Net Position

II. A Statement of Revenues, Expenditures, and Changes in Fund Net Position

III. A Statement of Revenues, Expenses, and Changes in Fund Net Position

IV. A Statement of Cash Flows

A) I and II only.

B) I and III only.

C) I, II, and IV only.

D) I, III, and IV only.

I. A Statement of Net Position

II. A Statement of Revenues, Expenditures, and Changes in Fund Net Position

III. A Statement of Revenues, Expenses, and Changes in Fund Net Position

IV. A Statement of Cash Flows

A) I and II only.

B) I and III only.

C) I, II, and IV only.

D) I, III, and IV only.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

Which measurement focus and basis of accounting should an Internal Service Fund use?

A) Economic resources Modified accrual

B) Current financial resources Modified accrual

C) Economic resources Accrual

D) Current financial resources Accrual

A) Economic resources Modified accrual

B) Current financial resources Modified accrual

C) Economic resources Accrual

D) Current financial resources Accrual

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

Internal Service Funds may report each of the following net position classifications except

A) Net investment in capital assets.

B) Restricted net position.

C) Nonspendable net position.

D) Unrestricted net position.

A) Net investment in capital assets.

B) Restricted net position.

C) Nonspendable net position.

D) Unrestricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

A self-insurance Internal Service Fund may include which of the following in its charges to other funds?

A) A reasonable provision for profit over a period of time.

B) Charges based on actuarial or other acceptable estimates of costs.

C) A reasonable provision for expected future catastrophic losses.

D) An amount equal to current year costs.

A) A reasonable provision for profit over a period of time.

B) Charges based on actuarial or other acceptable estimates of costs.

C) A reasonable provision for expected future catastrophic losses.

D) An amount equal to current year costs.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

The required statements for an Internal Service Fund include a Statement of

A) Activities.

B) Revenues, Expenditures, and Changes in Fund Balance.

C) Revenues, Expenditures, and Changes in Fund Net Position.

D) Revenues, Expenses, and Changes in Fund Net Position.

A) Activities.

B) Revenues, Expenditures, and Changes in Fund Balance.

C) Revenues, Expenditures, and Changes in Fund Net Position.

D) Revenues, Expenses, and Changes in Fund Net Position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

Governments that centralize their risk financing activities should not account for this activity in which type of fund?

A) General Fund.

B) Internal Service Fund.

C) Special Revenue Fund.

D) Permanent Fund.

A) General Fund.

B) Internal Service Fund.

C) Special Revenue Fund.

D) Permanent Fund.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements accurately describes why the statement of revenues, expenses and changes in net position for an Internal Service Fund differs slightly from one for an Enterprise Fund?

A) Internal Service Funds do not report operating revenue.

B) Internal Service Funds report other financing sources and uses.

C) Internal Service Funds do not report depreciation expense.

D) The statement of revenues, expenses and changes in net position is formatted the same for Enterprise Funds and Internal Service Funds.

A) Internal Service Funds do not report operating revenue.

B) Internal Service Funds report other financing sources and uses.

C) Internal Service Funds do not report depreciation expense.

D) The statement of revenues, expenses and changes in net position is formatted the same for Enterprise Funds and Internal Service Funds.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following accounts would potentially appear on both an Internal Service Fund statement of net position and a General Fund balance sheet?

A) Inventory.

B) Capital assets.

C) Bonds payable.

D) Restricted net position.

A) Inventory.

B) Capital assets.

C) Bonds payable.

D) Restricted net position.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

Assume that an Internal Service Fund purchases land on which to construct a new warehousing facility. The fund paid cash for 30% of the purchase price and financed the reminder with a loan from a local lending institution. The Internal Service Fund will

A) Increase Net Investment in Capital Assets.

B) Report capital outlay expenditures.

C) Depreciate the cost of the land over its useful life.

D) Record the land in the General Capital Assets accounts.

A) Increase Net Investment in Capital Assets.

B) Report capital outlay expenditures.

C) Depreciate the cost of the land over its useful life.

D) Record the land in the General Capital Assets accounts.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

Transfers from an Internal Service fund to another fund are reported in the Internal Service Fund's Statement of Cash Flows as

A) Cash flows from operating activities.

B) Cash flows from noncapital financing activities.

C) Cash flows from capital and related financing activities.

D) Cash flows from investing activities.

A) Cash flows from operating activities.

B) Cash flows from noncapital financing activities.

C) Cash flows from capital and related financing activities.

D) Cash flows from investing activities.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

An Internal Service Fund billed other departments $1,200,000 for services provided during the year. Expenses of $700,000 for salaries, $250,000 for supplies and materials used, $100,000 for depreciation, and $100,000 for interest expenses were incurred. The fund received a $42,000 transfer from the General Fund during the year. The Internal Service Fund should report operating income for the year of

A) $50,000.

B) $92,000.

C) $150,000.

D) $192,000.

A) $50,000.

B) $92,000.

C) $150,000.

D) $192,000.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

In an Internal Service Fund, the expectation is that

A) Each year's revenues should equal each year's expenses because the revenues are simply an allocation of that year's expenses.

B) Each year's revenues should equal each year's expenditures because the revenues are simply an allocation of that year's expenditures.

C) Accumulated revenues over time should approximately equal the accumulated expenses over time.

D) Expenses will exceed revenues because depreciation expense is reported in an Internal Service Fund.

A) Each year's revenues should equal each year's expenses because the revenues are simply an allocation of that year's expenses.

B) Each year's revenues should equal each year's expenditures because the revenues are simply an allocation of that year's expenditures.

C) Accumulated revenues over time should approximately equal the accumulated expenses over time.

D) Expenses will exceed revenues because depreciation expense is reported in an Internal Service Fund.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

A self-insurance activity that is accounted for in an Internal Service Fund pays $365,000 in claims during the year. Because the Internal Service Fund is a proprietary fund, the claims will be reported on the statement of revenues, expenses, and change in net position as

A) An operating expense.

B) A nonoperating expense.

C) A contra-revenue to premiums charged.

D) An other financing use.

A) An operating expense.

B) A nonoperating expense.

C) A contra-revenue to premiums charged.

D) An other financing use.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

40

Match between columns

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.