Deck 14: Financial Reporting Deriving Governmentwide Financial Statements and Required Reconciliations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The one-worksheet conversion adjustment to reflect debt service payments of $85,000 $55,000 principal; $30,000 interest by a governmental fund would be

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/48

Play

Full screen (f)

Deck 14: Financial Reporting Deriving Governmentwide Financial Statements and Required Reconciliations

1

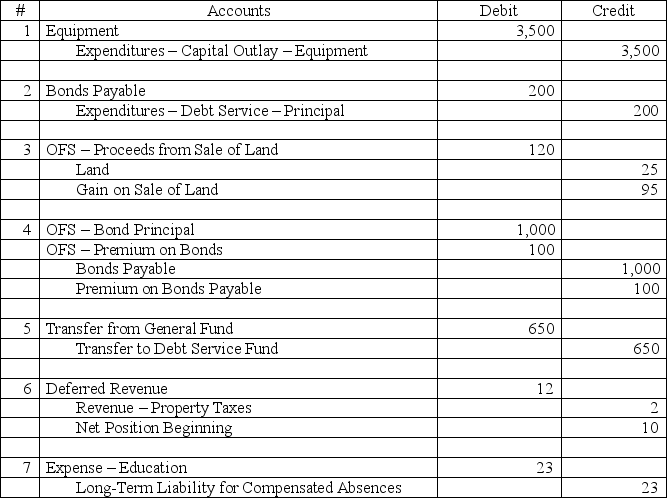

Selected governmental fund data from the City of Miller's Cove is presented below all amounts are in thousands of dollars:

Additional information:

1. Land sold had a book value of $25.

2. Deferred property taxes were $10 at the beginning of the year. Deferred property taxes at the end of the year were $12.

3. All of the compensated absence liabilities relate to the education function.

Requirement: Prepare the worksheet adjustments that would be needed to convert the following governmental fund data to governmental activities data for the government-wide statements.

Additional information:

1. Land sold had a book value of $25.

2. Deferred property taxes were $10 at the beginning of the year. Deferred property taxes at the end of the year were $12.

3. All of the compensated absence liabilities relate to the education function.

Requirement: Prepare the worksheet adjustments that would be needed to convert the following governmental fund data to governmental activities data for the government-wide statements.

2

Adjustments to Enterprise Funds to prepare the government-wide financial statements will mostly be limited to

A) Changes in measurement focus adjustments.

B) Changes in basis of accounting adjustments.

C) Internal Service Fund adjustments.

D) Changes in budgetary basis adjustments.

A) Changes in measurement focus adjustments.

B) Changes in basis of accounting adjustments.

C) Internal Service Fund adjustments.

D) Changes in budgetary basis adjustments.

C

3

The General Fund borrowed $100,000 from a Special Revenue Fund. Interest will be paid on the loan annually for five years and the principal repaid in full at the end of the fifth year. The governmental activities column should report

A) Both a loan payable and loan receivable for $100,000.

B) Other financing sources of $100,000.

C) Other financing uses of $100,000.

D) Nothing related to the loan arrangement.

A) Both a loan payable and loan receivable for $100,000.

B) Other financing sources of $100,000.

C) Other financing uses of $100,000.

D) Nothing related to the loan arrangement.

D

4

All of the following transactions could potentially be reconciling items between the governmental fund financial statements and government-wide governmental activities column except

A) The purchase of capital assets.

B) Accrual of compensated absences liability.

C) Issuance of long-term debt.

D) Borrowing from a local bank with a short-term loan.

A) The purchase of capital assets.

B) Accrual of compensated absences liability.

C) Issuance of long-term debt.

D) Borrowing from a local bank with a short-term loan.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

5

General capital assets with a net book value of $46,000 were transferred to an Enterprise Fund. The business-type activities column in the government-wide financial statements would report

A) A transfer in of $46,000.

B) A capital contribution of $46,000.

C) An other financing source of $46,000.

D) A revenue of $46,000.

A) A transfer in of $46,000.

B) A capital contribution of $46,000.

C) An other financing source of $46,000.

D) A revenue of $46,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

6

When converting the multiple governmental funds to the single entity represented by the governmental activities in the government-wide financial statements, which of the following adjustments will not be necessary?

A) Converting the cash account to reflect the different basis of accounting.

B) Adjusting for capital assets.

C) Adjusting for long-term liabilities.

D) Converting fund balance to net position.

A) Converting the cash account to reflect the different basis of accounting.

B) Adjusting for capital assets.

C) Adjusting for long-term liabilities.

D) Converting fund balance to net position.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

7

A city's Internal Service Fund provides services only to general government departments. During the year, the Internal Service Fund reports operating revenue of $100,000, operating expenses of $80,000 and interest income of $10,000. What adjustments are needed to the governmental funds operating statement information to reflect these transactions in the statement of activities in the government-wide statement?

A) Increase revenue by $110,000 and decrease expenses by $80,000.

B) Increase revenue by $10,000 and decrease expenses by $20,000.

C) Decrease expenses by $80,000 and increase revenue by $10,000.

D) Decrease expenses by $30,000 and decrease revenue by $20,000.

A) Increase revenue by $110,000 and decrease expenses by $80,000.

B) Increase revenue by $10,000 and decrease expenses by $20,000.

C) Decrease expenses by $80,000 and increase revenue by $10,000.

D) Decrease expenses by $30,000 and decrease revenue by $20,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following items would not require an adjustment to convert governmental fund information to governmental activities in the statement of net position?

A) Due to Debt Service Fund

B) Due to an Enterprise Fund

C) Due from a Special Revenue Fund

D) Due to Capital Projects Fund.

A) Due to Debt Service Fund

B) Due to an Enterprise Fund

C) Due from a Special Revenue Fund

D) Due to Capital Projects Fund.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following adjustments will not be necessary to covert the measurement focus and basis of accounting found in the governmental funds to the governmental activities reported in the government-wide financial statements?

A) Recording expenses with no corresponding expenditures.

B) Converting "when due" payables to accrual based payables.

C) Eliminating expenditures with no expense counterparts.

D) Adjusting the fair value of investments.

A) Recording expenses with no corresponding expenditures.

B) Converting "when due" payables to accrual based payables.

C) Eliminating expenditures with no expense counterparts.

D) Adjusting the fair value of investments.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

10

A city reports deferred tax revenue of $300,000 at the beginning of the year and $350,000 at the end of the year. What adjustment is needed to changes in fund balance to reconcile the governmental funds operating statement information to the changes in net position for governmental activities in the government-wide statement?

A) $300,000.

B) $50,000.

C) $50,000.

D) $350,000.

A) $300,000.

B) $50,000.

C) $50,000.

D) $350,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

11

A city's Internal Service Fund provides services only to general government departments. During the year, the Internal Service Fund reports operating revenue of $100,000 and operating expenses of $80,000. What adjustment is needed to the governmental funds operating statement information to reflect these transactions in the statement of activities in the government-wide statement?

A) Increase revenue by $100,000.

B) Decrease revenue by $20,000.

C) Decrease expenses by $20,000.

D) Increase expenses by $80,000.

A) Increase revenue by $100,000.

B) Decrease revenue by $20,000.

C) Decrease expenses by $20,000.

D) Increase expenses by $80,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

12

Information about the conversion of the Governmental Funds Balance Sheet to the Statement of Net Position for the City of Pleasant Hill is presented below all amounts are in thousands of dollars:

Requirement: Prepare the reconciliation of total fund balance to net position for governmental activities for the City of Pleasant Hill, given the following information.

Requirement: Prepare the reconciliation of total fund balance to net position for governmental activities for the City of Pleasant Hill, given the following information.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

13

A city has a long-term general government liability for compensated absences of $700,000 at the beginning of the year and $650,000 at the end of the year. What adjustment is needed to the fund balance to reconcile the governmental funds balance sheet information to net position for governmental activities in the government-wide statement?

A) $650,000.

B) $50,000.

C) $50,000.

D) $700,000.

A) $650,000.

B) $50,000.

C) $50,000.

D) $700,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following do most governmental entities not integrate into their general ledger accounts?

A) Governmental fund accounts.

B) Fiduciary fund accounts.

C) Government-wide information.

D) Proprietary fund accounts.

A) Governmental fund accounts.

B) Fiduciary fund accounts.

C) Government-wide information.

D) Proprietary fund accounts.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

15

A city has a long-term general government liability for compensated absences of $700,000 at the beginning of the year and $650,000 at the end of the year. What adjustment is needed to changes in fund balance to reconcile the governmental funds operating statement information to the changes in net position for governmental activities in the government-wide statement?

A) $50,000.

B) $50,000.

C) $650,000.

D) $700,000.

A) $50,000.

B) $50,000.

C) $650,000.

D) $700,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

16

A city reports deferred tax revenue of $300,000 at the beginning of the year and $350,000 at the end of the year. What adjustment is needed to fund balance to reconcile the governmental funds balance sheet information to net position for governmental activities in the government-wide statement?

A) $350,000.

B) $50,000.

C) $50,000.

D) $300,000.

A) $350,000.

B) $50,000.

C) $50,000.

D) $300,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

17

If an Internal Service Fund provides 60% of its services to the General Fund and 40% of its services to an Enterprise Fund, then governmental activities column in the government-wide financial statements will

A) Include 60% of the capital assets of the Internal Service Fund.

B) Reflect a reduction in expenses equal to 60% of the profit the Internal Service Fund reported for the year.

C) Include none of the capital assets of the Internal Service Fund.

D) Reflect a reduction in expenses equal to 100% of the profit the Internal Service Fund reported for the year.

A) Include 60% of the capital assets of the Internal Service Fund.

B) Reflect a reduction in expenses equal to 60% of the profit the Internal Service Fund reported for the year.

C) Include none of the capital assets of the Internal Service Fund.

D) Reflect a reduction in expenses equal to 100% of the profit the Internal Service Fund reported for the year.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

18

Information about the conversion of the Governmental Funds Change in Fund Balance to the Statement of Activities Change in Net Position for the City of Six Mile is presented below all amounts are in thousands of dollars:

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following financial accounting elements is not common to both the governmental funds and the governmental activities function in the government-wide financial statements?

A) Cash.

B) Short-term liabilities.

C) Deferred inflows.

D) Capital assets.

A) Cash.

B) Short-term liabilities.

C) Deferred inflows.

D) Capital assets.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

20

An incomplete operating statement conversion worksheet is provided below [in Excel file Ch14P-1] for the City of Walden Creek for FY 20X7.

Additional information:

1. Depreciation Expense for the year was:

Except for infrastructure, which is charged to the function that maintains it, depreciation is allocated as follows:

2. All capital outlay expenditures were capitalized except for $30,000 in asset purchases for the General Government that did not meet the capitalization threshold.

3. Deferred Revenues were $7,000 at the end of FY 20X6, $10,000 at the end of FY 20X7.

4. Interest Payable at the end of FY 20X6 was $4,000. At the end of FY 20X7 it was $3,000.

5. The vehicles that were sold had a net book value of $4,500.

6. Long-term compensated absences for the government increased $8,000 during the year. This increase was allocated to the functions at the same rate as depreciation.

Requirement: Complete the operating statement conversion worksheet.

Additional information:

1. Depreciation Expense for the year was:

Except for infrastructure, which is charged to the function that maintains it, depreciation is allocated as follows:

2. All capital outlay expenditures were capitalized except for $30,000 in asset purchases for the General Government that did not meet the capitalization threshold.

3. Deferred Revenues were $7,000 at the end of FY 20X6, $10,000 at the end of FY 20X7.

4. Interest Payable at the end of FY 20X6 was $4,000. At the end of FY 20X7 it was $3,000.

5. The vehicles that were sold had a net book value of $4,500.

6. Long-term compensated absences for the government increased $8,000 during the year. This increase was allocated to the functions at the same rate as depreciation.

Requirement: Complete the operating statement conversion worksheet.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

21

The General Fund paid $195,000 related to compensated absences during the year. If the beginning balance of long-term compensated absences payable for the governmental activities was $65,000 and the ending balance was $55,000, then the expenses related to compensated absences in the governmental activities column would be

A) $195,000.

B) $185,000.

C) $65,000.

D) $55,000.

A) $195,000.

B) $185,000.

C) $65,000.

D) $55,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following items would be subtracted from changes in fund balance in reconciling the governmental funds operating statement information to the changes in net position in the government-wide statement?

A) Depreciation.

B) Capital outlay expenditures.

C) Internal Service Fund increase in net position.

D) Repayment of bond principal.

A) Depreciation.

B) Capital outlay expenditures.

C) Internal Service Fund increase in net position.

D) Repayment of bond principal.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

23

Depreciation expense for the current year was $366,750 in the Water Enterprise Fund. Depreciation expense will be reported at the government-wide level as

A) Part of unallocated depreciation expense in governmental activities.

B) Part of unallocated depreciation expense in the business-type activities.

C) Part of the business-type activities expenses for the water activity.

D) Capital outlay expenses in business-type activities.

A) Part of unallocated depreciation expense in governmental activities.

B) Part of unallocated depreciation expense in the business-type activities.

C) Part of the business-type activities expenses for the water activity.

D) Capital outlay expenses in business-type activities.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

24

Depreciation expense on assets of the public safety function totaled $195,000 for the year. What is the effect on the operating statement conversion worksheet in the two-worksheet approach of this event?

A) There is no effect. The impact of depreciation is already reflected in the General Capital Assets accounts.

B) Public safety expenditures/expenses will be increased by $195,000.

C) Unallocated depreciation for the governmental activities will be increased by $195,000.

D) The depreciation will decrease the program revenues of the public safety function.

A) There is no effect. The impact of depreciation is already reflected in the General Capital Assets accounts.

B) Public safety expenditures/expenses will be increased by $195,000.

C) Unallocated depreciation for the governmental activities will be increased by $195,000.

D) The depreciation will decrease the program revenues of the public safety function.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

25

Business-type activities typically include

A) Only the enterprise funds.

B) Only the internal service funds.

C) All of the proprietary funds.

D) All of the proprietary and fiduciary funds.

A) Only the enterprise funds.

B) Only the internal service funds.

C) All of the proprietary funds.

D) All of the proprietary and fiduciary funds.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

26

In the two-worksheet approach, what type of adjustment will be necessary for interest expenditure/expense on the operating statement conversion worksheet?

A) No adjustment is necessary for interest expenditure/expense. The amount of interest expenditure on the governmental fund financial statements is the same amount that will be reported as interest expense in the government-wide statements.

B) Interest on long-term debt that has been incurred but not paid will need to be added to the interest expenditure reported on the governmental funds balance sheet.

C) Interest paid this year that is attributable to the previous year accrual for long-term debt will need to be deducted from interest expenditure reported on the governmental funds balance sheet.

D) An adjustment to the interest expenditure reported on the governmental funds operating statement will be necessary for the net change in accrued interest payable on long-term debt from the beginning of the year to the end of the year.

A) No adjustment is necessary for interest expenditure/expense. The amount of interest expenditure on the governmental fund financial statements is the same amount that will be reported as interest expense in the government-wide statements.

B) Interest on long-term debt that has been incurred but not paid will need to be added to the interest expenditure reported on the governmental funds balance sheet.

C) Interest paid this year that is attributable to the previous year accrual for long-term debt will need to be deducted from interest expenditure reported on the governmental funds balance sheet.

D) An adjustment to the interest expenditure reported on the governmental funds operating statement will be necessary for the net change in accrued interest payable on long-term debt from the beginning of the year to the end of the year.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

27

In the two-worksheet approach, each of the following worksheet adjustments would be made for the operating statement except

A) Adding depreciation expense.

B) Adding accumulated depreciation.

C) Converting interest expenditures to interest expenses.

D) Eliminating other financing sources or uses.

A) Adding depreciation expense.

B) Adding accumulated depreciation.

C) Converting interest expenditures to interest expenses.

D) Eliminating other financing sources or uses.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

28

The Capital Projects Fund issued general long-term debt at a premium. The balance sheet conversion worksheet of the two-worksheet approach would include

A) A deduction from an other financing source.

B) An addition to an other financing use.

C) An addition to an other financing source.

D) A deduction from an other financing use.

A) A deduction from an other financing source.

B) An addition to an other financing use.

C) An addition to an other financing source.

D) A deduction from an other financing use.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following items would be added to changes in fund balance in reconciling the governmental funds operating statement information to the changes in net position in the government-wide statement?

A) Depreciation.

B) Bond proceeds.

C) Book value of capital assets sold.

D) Repayment of bond principal.

A) Depreciation.

B) Bond proceeds.

C) Book value of capital assets sold.

D) Repayment of bond principal.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

30

In the two-worksheet approach, which of the following worksheet adjustments would not be made for the balance sheet?

A) Add capital assets.

B) Add accrued interest payable.

C) Add depreciation expenses.

D) Add bonds payable.

A) Add capital assets.

B) Add accrued interest payable.

C) Add depreciation expenses.

D) Add bonds payable.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following items would be added to changes in fund balance in reconciling the governmental funds operating statement information to the changes in net position in the government-wide statement?

A) Depreciation.

B) Capital outlay expenditures.

C) Book value of capital assets sold.

D) Bond proceeds.

A) Depreciation.

B) Capital outlay expenditures.

C) Book value of capital assets sold.

D) Bond proceeds.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

32

A county's Central Warehouse Internal Service Fund provides 65% of its services to governmental funds, 30% of its services to Enterprise Funds, and the remaining 5% to a local municipality. If there was a $10,000 loss in the Internal Service Fund during 20X9, the expenses in the governmental activities column would

A) Decrease by $10,000.

B) Increase by $7,000.

C) Increase by $10,000.

D) Decrease by $7,000.

A) Decrease by $10,000.

B) Increase by $7,000.

C) Increase by $10,000.

D) Decrease by $7,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

33

In the two-worksheet approach, what type of adjustment will be necessary for interest payable on the balance sheet conversion worksheet?

A) No adjustment is necessary for interest payable. This amount is the same in the fund statements and the government-wide statements.

B) Interest on long-term debt that has been incurred but not paid will need to be added to the interest payable reported on the governmental funds balance sheet.

C) Interest paid this year that is attributable to the previous year accrual for long-term debt will need to be deducted from interest payable reported on the governmental funds balance sheet.

D) The net change in accrued interest payable on long-term debt from the beginning of the year to the end of the year will be added to the amount of interest payable reported on the governmental funds balance sheet.

A) No adjustment is necessary for interest payable. This amount is the same in the fund statements and the government-wide statements.

B) Interest on long-term debt that has been incurred but not paid will need to be added to the interest payable reported on the governmental funds balance sheet.

C) Interest paid this year that is attributable to the previous year accrual for long-term debt will need to be deducted from interest payable reported on the governmental funds balance sheet.

D) The net change in accrued interest payable on long-term debt from the beginning of the year to the end of the year will be added to the amount of interest payable reported on the governmental funds balance sheet.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

34

The required reconciliation of the governmental fund balance sheet to the governmental activities statement of net position does not include adjustments related to

A) Capital assets.

B) Interfund charges for services.

C) Deferred revenue.

D) Long-term liabilities.

A) Capital assets.

B) Interfund charges for services.

C) Deferred revenue.

D) Long-term liabilities.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

35

The required reconciliation of the governmental fund financial statement information to the governmental activities information in the corresponding government-wide financial statements

A) Must be presented at the bottom of the fund financial statements and at the bottom of the government-wide financial statements.

B) Must be presented only at the bottom of the government-wide financial statements.

C) May be presented either at the bottom of the fund financial statements or in separate schedules.

D) Must be presented in separate schedules, not on the face of the financial statements.

A) Must be presented at the bottom of the fund financial statements and at the bottom of the government-wide financial statements.

B) Must be presented only at the bottom of the government-wide financial statements.

C) May be presented either at the bottom of the fund financial statements or in separate schedules.

D) Must be presented in separate schedules, not on the face of the financial statements.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following items is NOT included in reconciling the governmental funds operating statement information to the changes in net position in the government-wide statement?

A) Depreciation.

B) Amortization of bond premiums.

C) Expenditures for retirement of general long-term debt principal.

D) Increase in salaries payable.

A) Depreciation.

B) Amortization of bond premiums.

C) Expenditures for retirement of general long-term debt principal.

D) Increase in salaries payable.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following items would be subtracted from changes in fund balance in reconciling the governmental funds operating statement information to the changes in net position in the government-wide statement?

A) Depreciation.

B) Bond issue costs.

C) Salary expenditures.

D) Debt principal payments.

A) Depreciation.

B) Bond issue costs.

C) Salary expenditures.

D) Debt principal payments.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

38

Internal Service Funds, classified as a proprietary fund type, are reported in the government-wide statements as

A) Governmental activities.

B) Business-type activities.

C) Either governmental activities or business-type activities depending upon the primary user of the activity.

D) Like Fiduciary Funds, Internal Service Funds are not reported in the government-wide statements.

A) Governmental activities.

B) Business-type activities.

C) Either governmental activities or business-type activities depending upon the primary user of the activity.

D) Like Fiduciary Funds, Internal Service Funds are not reported in the government-wide statements.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

39

If a county sells a capital asset with a net book value of $35,000 for $27,000, how will this transaction be recorded on the operating statement conversion worksheet of the two-worksheet conversion approach?

A) A deduction from an other financing source for $8,000.

B) An addition to an other financing use for $35,000.

C) An addition to an other financing use for $8,000.

D) A deduction from an other financing source for $35,000.

A) A deduction from an other financing source for $8,000.

B) An addition to an other financing use for $35,000.

C) An addition to an other financing use for $8,000.

D) A deduction from an other financing source for $35,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

40

Net investment in capital assets would not include

A) Accounts payable, even if it was capital related.

B) Notes payable that is capital related.

C) Inventory.

D) Accumulated depreciation.

A) Accounts payable, even if it was capital related.

B) Notes payable that is capital related.

C) Inventory.

D) Accumulated depreciation.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

41

The Capital Projects Fund issued general long-term debt at a premium. The one-worksheet conversion adjustment would include a

A) Debit to cash.

B) Credit to bonds payable.

C) Debit to unamortized premium on bonds.

D) Credit to other financing sources.

A) Debit to cash.

B) Credit to bonds payable.

C) Debit to unamortized premium on bonds.

D) Credit to other financing sources.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

42

Taxes were levied in the General Fund during 20X8. $157,700 of the taxes were still uncollectible as of the end of the fiscal year. The one-worksheet conversion adjustment necessary as the government-wide statements are being prepared would include a DEBIT to

A) Deferred revenues.

B) Allowance for doubtful accounts.

C) Taxes receivable.

D) Other financing sources.

A) Deferred revenues.

B) Allowance for doubtful accounts.

C) Taxes receivable.

D) Other financing sources.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

43

A government had capital outlay expenditures of $226,000 during the year for the public safety function accounted for in the General Fund. It was determined that $195,000 of the capital outlay should be reported as capital assets in the government-wide financial statements. What would the one-worksheet conversion adjustment be to record the capital assets as a governmental activity?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

44

A government had capital outlay expenditures of $226,000 during the year for the public safety function accounted for in the General Fund. It was determined that only $195,000 of the expenditures met the capitalization threshold of the government. How would this transaction appear on the operating statement conversion worksheet in the two-worksheet conversion approach?

A) The only effect would be to reduce capital outlay expenditures by $226,000.

B) Capital outlay expenditures would be reduced by $226,000, and public safety expenditures/expenses would be increased by $31,000.

C) Capital outlay expenditures would be reduced by $195,000, and public safety expenditures/expenses would be increased by $31,000.

D) The only effect would be to reduce capital outlay expenditures by $195,000.

A) The only effect would be to reduce capital outlay expenditures by $226,000.

B) Capital outlay expenditures would be reduced by $226,000, and public safety expenditures/expenses would be increased by $31,000.

C) Capital outlay expenditures would be reduced by $195,000, and public safety expenditures/expenses would be increased by $31,000.

D) The only effect would be to reduce capital outlay expenditures by $195,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

45

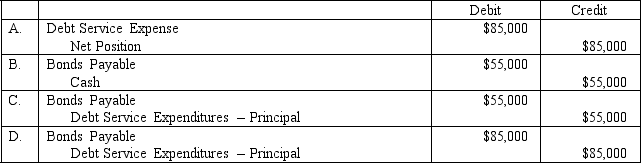

The one-worksheet conversion adjustment to reflect debt service payments of $85,000 $55,000 principal; $30,000 interest by a governmental fund would be

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

46

The Cable Enterprise Fund purchased $300,000 of capital equipment during the year. The one-worksheet conversion adjustment necessary for the preparation of the government-wide financial statements would be

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

47

If a county receives $27,000, for the sale of a dump truck with a historical cost of $60,000, and accumulated depreciation of $25,000, the one-worksheet conversion adjustment would be

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

48

Depreciation expense on assets of the public safety function totaled $195,000 for the year. The one-worksheet conversion adjustment necessary to record the depreciation expense as part of governmental activities would be

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 48 flashcards in this deck.