Deck 4: Budgeting, Budgetary Accounting, and Budgetary Reporting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

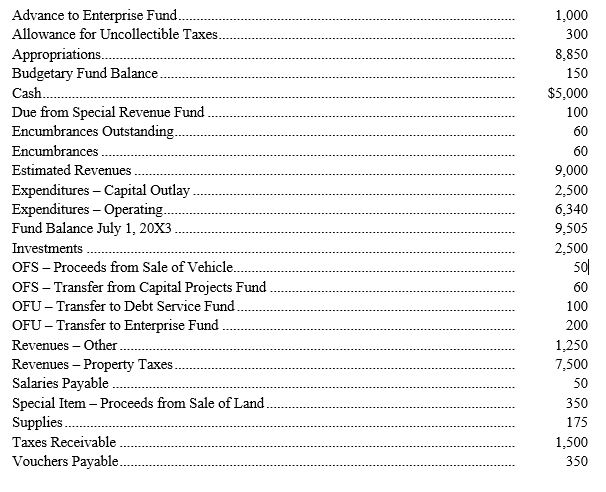

Listed below in alphabetical order are the general ledger and budgetary accounts for the City of Walland. All balances are year end, unless otherwise noted. All accounts have a normal balance. At the end of the year, the City Council passed an ordinance that all outstanding orders would be honored in the following fiscal year. Also, the Finance Officer set aside $40 for equipment replacement.

Requirements:

1. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 20X4.

2. Prepare the Balance Sheet for the year ended June 30, 20X4.

3. Prepare all necessary closing entries.

Requirements:

1. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 20X4.

2. Prepare the Balance Sheet for the year ended June 30, 20X4.

3. Prepare all necessary closing entries.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

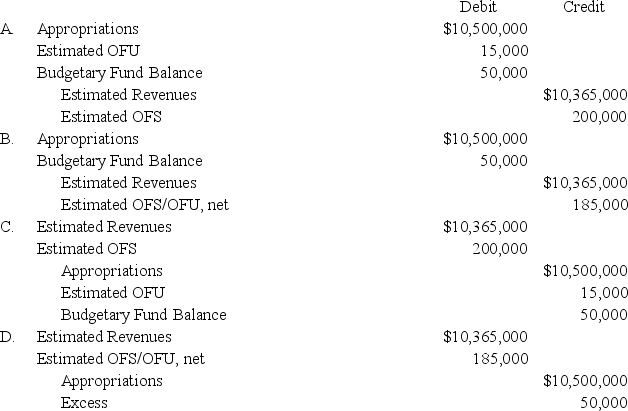

Which of the following budgetary entries would the township of Brussels make upon adoption of its General Fund budget for the year? Assume the following: Estimated Revenues $10,365,000

Appropriations 10,500,000

Estimated Other Financing Sources OFS 200,000

Estimated Other Financing Uses OFU 15,000

Appropriations 10,500,000

Estimated Other Financing Sources OFS 200,000

Estimated Other Financing Uses OFU 15,000

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/35

Play

Full screen (f)

Deck 4: Budgeting, Budgetary Accounting, and Budgetary Reporting

1

Under an encumbrance system, which account is debited when a purchase order is issued?

A) Expenditures.

B) Appropriations.

C) Encumbrances.

D) Encumbrances Outstanding.

A) Expenditures.

B) Appropriations.

C) Encumbrances.

D) Encumbrances Outstanding.

C

2

The purpose of encumbrance accounting is to

A) Manage a government's cash flows.

B) Avoid expenditures exceeding appropriations.

C) Replace expense accounting in governments.

D) Prevent government waste.

A) Manage a government's cash flows.

B) Avoid expenditures exceeding appropriations.

C) Replace expense accounting in governments.

D) Prevent government waste.

B

3

What general ledger account is not needed for an expenditures subsidiary ledger?

A) Appropriations.

B) Expenditures.

C) Encumbrances.

D) Encumbrances Outstanding.

A) Appropriations.

B) Expenditures.

C) Encumbrances.

D) Encumbrances Outstanding.

D

4

As part of a government's basic financial statements and required supplementary information, a budgetary comparison statement or schedule should be presented as

A) A basic financial statement.

B) In the other information section of the CAFR.

C) A note to the financial statements.

D) Budgetary reporting is optional for governments.

A) A basic financial statement.

B) In the other information section of the CAFR.

C) A note to the financial statements.

D) Budgetary reporting is optional for governments.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

5

The encumbrances method of budgetary reporting

A) Is never allowed by GAAP.

B) Never results in an outstanding encumbrance.

C) Is where outstanding encumbrances are considered to be expenditures.

D) Is always required by GAAP.

A) Is never allowed by GAAP.

B) Never results in an outstanding encumbrance.

C) Is where outstanding encumbrances are considered to be expenditures.

D) Is always required by GAAP.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

6

The most widely used approach to budgeting operating expenditures is

A) Zero-base.

B) Performance approach.

C) Object-of-expenditure.

D) Program and planning-programming-budgeting.

A) Zero-base.

B) Performance approach.

C) Object-of-expenditure.

D) Program and planning-programming-budgeting.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

7

A general budget is often a term used to describe a budget for all of the following except

A) A General Fund.

B) A Special Revenue Fund.

C) An Enterprise Fund.

D) A Debt Service Fund.

A) A General Fund.

B) A Special Revenue Fund.

C) An Enterprise Fund.

D) A Debt Service Fund.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

8

As part of a government's basic financial statements and required supplementary information, a budgetary comparison schedule is required for which funds?

A) All governmental funds.

B) All governmental funds with legally adopted annual budgets.

C) General Fund only.

D) General Fund and certain Special Revenue Funds with legally adopted annual budgets.

A) All governmental funds.

B) All governmental funds with legally adopted annual budgets.

C) General Fund only.

D) General Fund and certain Special Revenue Funds with legally adopted annual budgets.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

9

The "Unencumbered Balance" in an expenditure subsidiary ledger represents

A) Appropriation less expenditures.

B) Appropriation less encumbrances.

C) Appropriation less expenditures and encumbrances.

D) Estimated revenue less appropriation.

A) Appropriation less expenditures.

B) Appropriation less encumbrances.

C) Appropriation less expenditures and encumbrances.

D) Estimated revenue less appropriation.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

10

A city's General Fund general ledger includes accounts called Estimated Revenues, Appropriations, and Encumbrances. This indicates that the city

A) Formally integrates its budget into its accounts.

B) Uses a cash plus encumbrances basis of accounting.

C) Maintains its accounts on an accrual basis.

D) Erroneously reports encumbrances as expenditures.

A) Formally integrates its budget into its accounts.

B) Uses a cash plus encumbrances basis of accounting.

C) Maintains its accounts on an accrual basis.

D) Erroneously reports encumbrances as expenditures.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following does not represent a common approach to budgeting expenditures?

A) Zero-base budgeting.

B) Object-of-expenditure budget.

C) Program budgeting.

D) Marginal increase budgeting.

A) Zero-base budgeting.

B) Object-of-expenditure budget.

C) Program budgeting.

D) Marginal increase budgeting.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

12

During the year, Nathan Township amended their General Fund budget to reflect an increase in appropriations of $50,000 to be funded by an appropriation of existing fund balance. What would the necessary budgetary entry be to reflect this amendment?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

13

Managers may ration expenditure authority into either monthly or quarterly expenditure ceilings. This would be an example of

A) An allotment.

B) An allocation.

C) A ration.

D) An appropriation.

A) An allotment.

B) An allocation.

C) A ration.

D) An appropriation.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

14

Listed below in alphabetical order are the general ledger and budgetary accounts for the City of Walland. All balances are year end, unless otherwise noted. All accounts have a normal balance. At the end of the year, the City Council passed an ordinance that all outstanding orders would be honored in the following fiscal year. Also, the Finance Officer set aside $40 for equipment replacement.

Requirements:

1. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 20X4.

2. Prepare the Balance Sheet for the year ended June 30, 20X4.

3. Prepare all necessary closing entries.

Requirements:

1. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 20X4.

2. Prepare the Balance Sheet for the year ended June 30, 20X4.

3. Prepare all necessary closing entries.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

15

Common functional categories of expenditures in governmental funds include all of the following except

A) Public Safety.

B) Health and Sanitation.

C) Highways and Streets.

D) Utilities.

A) Public Safety.

B) Health and Sanitation.

C) Highways and Streets.

D) Utilities.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements regarding revenue subsidiary ledgers is false?

A) The number of revenue subsidiary ledgers necessary is at the discretion of management.

B) The number of revenue subsidiary ledgers used is limited by the number of broad revenue categories e.g., taxes, licenses and permits, intergovernmental that a governmental entity reports.

C) Entries to revenue subsidiary ledgers may be made at any time during a fiscal period.

D) Revenue subsidiary ledgers are never required.

A) The number of revenue subsidiary ledgers necessary is at the discretion of management.

B) The number of revenue subsidiary ledgers used is limited by the number of broad revenue categories e.g., taxes, licenses and permits, intergovernmental that a governmental entity reports.

C) Entries to revenue subsidiary ledgers may be made at any time during a fiscal period.

D) Revenue subsidiary ledgers are never required.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

17

SEQ CHAPTER \h \r 1Selected transactions of the City of Miser Station General Fund for the 20X1 fiscal year are presented on the following page. All amounts are in thousands of dollars.

General instructions:

a. Dates and formal explanations may be omitted, but number your entries appropriately.

b. All interest rates are annual percentage rates APRs.

c. Record your entries on the lined paper provided with your answer pages. Sufficient space has been provided to allow you to skip lines between entries.

d. When recording Revenues, classify them as Revenues-Property Taxes or Revenues-Other. When recording expenditures, classify them as Expenditures-Operating, Expenditures-Debt Service, or Expenditures-Capital Outlay. Additional detail for budgetary entries is not required.

e. Show all work for any amount required in an entry that is not given in the exam except when recording the amount necessary to balance the journal entry.

Requirements:

1. Prepare the general ledger journal entries for the transactions. If no entry is required, do not leave it blank. State "No Entry Required" and briefly explain why.

2. Indicate the effects of the transaction on the accounting equations for the General Fund and the General Capital Assets and General Long-Term Liabilities accounts. Do not leave a cell blank. If a transaction has no effect on a particular element, use "NE".

3. Maintain the subsidiary ledgers for Revenues - Property Taxes and Expenditures - Operating for all appropriate entries.

Transactions:

1. The City Council approved the following budget for the fiscal year:

Of these amounts, $8,000 is for operating expenditures and $10,000 is for property tax revenues.

2. The property tax levy was recorded, $10,000, of which 3% will probably prove uncollectible.

3. The city ordered $200 in supplies.

4. The City borrowed $500 from the Blount National Bank on a two-month, 6% note.

5. Cash receipts were see entry #2:

Property Taxes 8,500

License and Permits 150

Total Receipts 8,650

6. The City Council revised the budget see entry #1. Appropriations were reduced $3,000 and Estimated Revenues were reduced $2,000 Appropriations for Expenditures - Operating were reduced $1,000; property tax revenues were not affected.

7. Of the previous supplies order Entry #3, 75% of the order was received. The actual cost of the goods received was $135. The amount due the vendor will be paid at a later date.

8. City employees were paid, $25.

9. The city ordered a new police car. The estimated cost is $21.

10. The City repaid the short-term note see entry #4 when due.

11. Wrote off $100 of taxes receivable as uncollectible see entry #2.

12. Paid $12 to the Special Revenue Fund to repay it for General Fund employee salaries that were inadvertently recorded as expenditures of that fund.

13. The city received the police car see entry #9. The actual cost was $22. The vendor will be paid at a later date.

14. The city collected $50 for licenses.

15. The city paid $157 on account.

General instructions:

a. Dates and formal explanations may be omitted, but number your entries appropriately.

b. All interest rates are annual percentage rates APRs.

c. Record your entries on the lined paper provided with your answer pages. Sufficient space has been provided to allow you to skip lines between entries.

d. When recording Revenues, classify them as Revenues-Property Taxes or Revenues-Other. When recording expenditures, classify them as Expenditures-Operating, Expenditures-Debt Service, or Expenditures-Capital Outlay. Additional detail for budgetary entries is not required.

e. Show all work for any amount required in an entry that is not given in the exam except when recording the amount necessary to balance the journal entry.

Requirements:

1. Prepare the general ledger journal entries for the transactions. If no entry is required, do not leave it blank. State "No Entry Required" and briefly explain why.

2. Indicate the effects of the transaction on the accounting equations for the General Fund and the General Capital Assets and General Long-Term Liabilities accounts. Do not leave a cell blank. If a transaction has no effect on a particular element, use "NE".

3. Maintain the subsidiary ledgers for Revenues - Property Taxes and Expenditures - Operating for all appropriate entries.

Transactions:

1. The City Council approved the following budget for the fiscal year:

Of these amounts, $8,000 is for operating expenditures and $10,000 is for property tax revenues.

2. The property tax levy was recorded, $10,000, of which 3% will probably prove uncollectible.

3. The city ordered $200 in supplies.

4. The City borrowed $500 from the Blount National Bank on a two-month, 6% note.

5. Cash receipts were see entry #2:

Property Taxes 8,500

License and Permits 150

Total Receipts 8,650

6. The City Council revised the budget see entry #1. Appropriations were reduced $3,000 and Estimated Revenues were reduced $2,000 Appropriations for Expenditures - Operating were reduced $1,000; property tax revenues were not affected.

7. Of the previous supplies order Entry #3, 75% of the order was received. The actual cost of the goods received was $135. The amount due the vendor will be paid at a later date.

8. City employees were paid, $25.

9. The city ordered a new police car. The estimated cost is $21.

10. The City repaid the short-term note see entry #4 when due.

11. Wrote off $100 of taxes receivable as uncollectible see entry #2.

12. Paid $12 to the Special Revenue Fund to repay it for General Fund employee salaries that were inadvertently recorded as expenditures of that fund.

13. The city received the police car see entry #9. The actual cost was $22. The vendor will be paid at a later date.

14. The city collected $50 for licenses.

15. The city paid $157 on account.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the statements regarding the accounting for encumbrances is false?

A) The budgetary entry to record an encumbrance would be a debit to Encumbrances Outstanding and a credit to Encumbrances.

B) The budgetary entry to record an encumbrance would be a debit to Encumbrances and a credit to Encumbrances Outstanding.

C) If the actual cost of a purchase exceeds the amount of the original encumbrance, the original encumbrance is still reversed at the original amount.

D) The recording of an encumbrance is considered to be a budgetary entry.

A) The budgetary entry to record an encumbrance would be a debit to Encumbrances Outstanding and a credit to Encumbrances.

B) The budgetary entry to record an encumbrance would be a debit to Encumbrances and a credit to Encumbrances Outstanding.

C) If the actual cost of a purchase exceeds the amount of the original encumbrance, the original encumbrance is still reversed at the original amount.

D) The recording of an encumbrance is considered to be a budgetary entry.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

19

Legal authority to expend resources is adopted by a city council in the budgeting process. These legal authorizations are called

A) Appropriations.

B) Authorizations.

C) Encumbrances.

D) Expenditures.

A) Appropriations.

B) Authorizations.

C) Encumbrances.

D) Expenditures.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

20

A budgetary comparison schedule is required to include all of the following columns except

A) The original budget.

B) Actual on the GAAP basis.

C) Final revised budget.

D) Actual on the budgetary basis.

A) The original budget.

B) Actual on the GAAP basis.

C) Final revised budget.

D) Actual on the budgetary basis.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

21

The following information pertains to the Richardson County General Fund: Appropriations $10,000,000

Estimated Revenues 12,000,000

Expenditures 12,800,000

Revenues 9,200,000

Long-term note issue proceeds 1,000,000

Short-term note principal retirements 250,000

Operating transfers to other funds 75,000

The change in Richardson County's General Fund fund balance for the year is a

A) $2,600,000 decrease.

B) $2,675,000 decrease.

C) $2,925,000 decrease.

D) $3,600,000 decrease.

Estimated Revenues 12,000,000

Expenditures 12,800,000

Revenues 9,200,000

Long-term note issue proceeds 1,000,000

Short-term note principal retirements 250,000

Operating transfers to other funds 75,000

The change in Richardson County's General Fund fund balance for the year is a

A) $2,600,000 decrease.

B) $2,675,000 decrease.

C) $2,925,000 decrease.

D) $3,600,000 decrease.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following fund balance classifications is used for budgetary accounting but not for GAAP financial statement reporting?

A) Nonspendable Fund Balance.

B) Budgetary Fund Balance.

C) Committed Fund Balance.

D) Unassigned Fund Balance.

A) Nonspendable Fund Balance.

B) Budgetary Fund Balance.

C) Committed Fund Balance.

D) Unassigned Fund Balance.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

23

The Town of Red Herring issued $60,000 of purchase orders and recorded the encumbrance. Assume that when all orders were received, the actual cost was $59,000. What would be the net change in the unencumbered balance when the goods are received?

A) $60,000 increase.

B) $1,000 increase.

C) $1,000 decrease.

D) $59,000 decrease.

A) $60,000 increase.

B) $1,000 increase.

C) $1,000 decrease.

D) $59,000 decrease.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is not a common revenue source in a governmental fund budget?

A) Property taxes.

B) Other financing sources.

C) Charges for services.

D) Investment income or interest.

A) Property taxes.

B) Other financing sources.

C) Charges for services.

D) Investment income or interest.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

25

A city ordered uniforms with an expected cost of $6,000 for policemen. This amount is encumbered. The uniforms are received with an invoice of $5,900. The entries to record the receipt of the uniforms should include a credit to

A) Encumbrances of $6,000.

B) Encumbrances Outstanding of $6,000.

C) Encumbrances of $5,900.

D) Appropriations of $100.

A) Encumbrances of $6,000.

B) Encumbrances Outstanding of $6,000.

C) Encumbrances of $5,900.

D) Appropriations of $100.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

26

A governmental fund budgetary comparison statement or schedule should

A) Be prepared on the same basis the budget was enacted.

B) Always be prepared on a GAAP basis.

C) Always be prepared on a cash basis.

D) Be prepared only for the General Fund.

A) Be prepared on the same basis the budget was enacted.

B) Always be prepared on a GAAP basis.

C) Always be prepared on a cash basis.

D) Be prepared only for the General Fund.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following budgetary entries would the town of Geneva make upon adoption of its Special Revenue Fund Budget for the year? Assume the following: Estimated Revenues $6,400,000

Appropriations 6,080,000

Appropriations 6,080,000

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following budgetary entries would the township of Brussels make upon adoption of its General Fund budget for the year? Assume the following: Estimated Revenues $10,365,000

Appropriations 10,500,000

Estimated Other Financing Sources OFS 200,000

Estimated Other Financing Uses OFU 15,000

Appropriations 10,500,000

Estimated Other Financing Sources OFS 200,000

Estimated Other Financing Uses OFU 15,000

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

29

When preparing a budgetary comparison statement for a General Fund, which column is optional?

A) Final amended budget.

B) Original budget.

C) Variance comparing the final budget to the actual amounts on a budgetary basis.

D) Actual amounts on a budgetary basis.

A) Final amended budget.

B) Original budget.

C) Variance comparing the final budget to the actual amounts on a budgetary basis.

D) Actual amounts on a budgetary basis.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

30

A city ordered uniforms with an expected cost of $6,000 for policemen. This amount is encumbered. The uniforms are received with an invoice of $5,900. The entries to record the receipt of the uniforms should include a debit to

A) Encumbrances of $6,000.

B) Encumbrances Outstanding of $5,900.

C) Encumbrances Outstanding of $6,000.

D) Appropriations of $100.

A) Encumbrances of $6,000.

B) Encumbrances Outstanding of $5,900.

C) Encumbrances Outstanding of $6,000.

D) Appropriations of $100.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

31

A city ordered uniforms with an expected cost of $6,000 for policemen. The credit required to record this transaction is

A) Appropriations.

B) Encumbrances.

C) Vouchers payable.

D) Encumbrances Outstanding.

A) Appropriations.

B) Encumbrances.

C) Vouchers payable.

D) Encumbrances Outstanding.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

32

The Town of Red Herring issued $60,000 of purchase orders. Assume that when all orders were received, the actual cost was $59,000. How much would be recorded as expenditures when the goods are received?

A) $60,000.

B) $59,000.

C) $1,000.

D) $0.

A) $60,000.

B) $59,000.

C) $1,000.

D) $0.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

33

If a government uses a Budgetary Fund Balance account, the account balance

A) Will equal the difference between actual expenditures and appropriations at any point in time.

B) Will be the planned increase or decrease in fund balance at any point in time.

C) Will equal the difference between actual revenues and budgeted revenues at any point in time.

D) Will equal the difference between actual revenues and actual expenditures and encumbrances for the year.

A) Will equal the difference between actual expenditures and appropriations at any point in time.

B) Will be the planned increase or decrease in fund balance at any point in time.

C) Will equal the difference between actual revenues and budgeted revenues at any point in time.

D) Will equal the difference between actual revenues and actual expenditures and encumbrances for the year.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

34

The Town of Red Herring issued $60,000 of purchase orders. Assume that when all orders were received, the actual cost was $59,000. How much would be recorded as expenditures when the purchase orders were issued?

A) $60,000

B) $59,000

C) $1,000

D) $0

A) $60,000

B) $59,000

C) $1,000

D) $0

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

35

The following information pertains to the Scott County General Fund: Appropriations $15,000,000

Estimated Revenues 14,000,000

Expenditures 14,800,000

Revenues 14,200,000

The change in Scott County's General Fund fund balance for the year is a

A) $1,600,000 decrease.

B) $1,000,000 decrease.

C) $600,000 decrease.

D) $400,000 increase.

Estimated Revenues 14,000,000

Expenditures 14,800,000

Revenues 14,200,000

The change in Scott County's General Fund fund balance for the year is a

A) $1,600,000 decrease.

B) $1,000,000 decrease.

C) $600,000 decrease.

D) $400,000 increase.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 35 flashcards in this deck.