Deck 18: Accounting for Health Care Organizations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

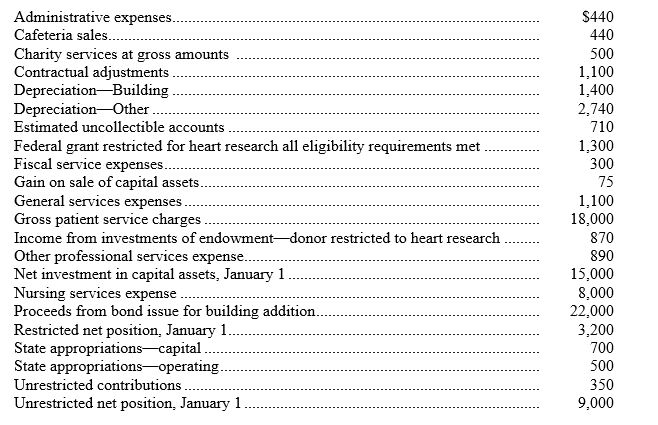

The following selected information is taken from the accounting records of the Jackson County Hospital for fiscal year 20X0. All accounts have a normal balance and are listed in alphabetical order. Also, all amounts are in thousands of dollars.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/35

Play

Full screen (f)

Deck 18: Accounting for Health Care Organizations

1

At their recent board of directors meeting, the County Hospital Board voted to designate $150,000 of current investments toward the renovation of the hospital planned for next year. This designation will be result in

A) A credit to cash.

B) A debit to unrestricted investments.

C) A debit to investments-designated for plant replacement.

D) A debit to construction in progress.

A) A credit to cash.

B) A debit to unrestricted investments.

C) A debit to investments-designated for plant replacement.

D) A debit to construction in progress.

C

2

The fair market value of a government hospital's investments that are restricted for future capital needs increased by $7,000. As of the end of the fiscal year,

A) Nonoperating gains will increase by $7,000.

B) General revenue will increase by $7,000.

C) This change in market value will not be reported unless the assets are sold.

D) Other financing sources will increase by $7,000.

A) Nonoperating gains will increase by $7,000.

B) General revenue will increase by $7,000.

C) This change in market value will not be reported unless the assets are sold.

D) Other financing sources will increase by $7,000.

A

3

Briefly answer the following questions on hospital reporting:

1. Identify the financial statements that must be presented for a government hospital.

2. How are the financial statements for a government hospital different from the financial statements for a not-for-profit hospital?

1. Identify the financial statements that must be presented for a government hospital.

2. How are the financial statements for a government hospital different from the financial statements for a not-for-profit hospital?

1. The required statements for a government hospital are:

-Statement of Net Position

-Statement of Revenues, Expenses, and Changes in Net Position

-Statement of Cash Flows

2. Although there are many similarities among the financial statements for a government hospital and a not-for-profit hospital, the key differences are:

-Net assets for not-for-profit hospitals are classified as unrestricted, temporarily restricted, and permanently restricted. Net position for government hospitals are classified as unrestricted, restricted, and net investment in capital assets.

-Not-for-profit hospitals report a statement of operations and a statement of changes in net assets. Government hospitals report a statement of revenues, expenses, and changes in net position.

-Not-for-profit hospitals report changes in all three categories of net assets. Government hospitals report only changes in total net position.

-Not-for-profit hospitals report assets released from restrictions. Government hospitals do not report assets released from restrictions.

-Not-for-profit hospitals follow FASB cash flow statement guidance three sections. Not-for-profit hospitals may prepare the statement using either the indirect method or the direct method. Government hospitals follow GASB cash flow statement guidance four sections. Government hospitals must prepare the statement using the direct method.

-Government hospitals defer revenue recognition on reimbursement grants until qualifying costs are incurred. Nongovernment, not-for-profit hospitals do not.

-Statement of Net Position

-Statement of Revenues, Expenses, and Changes in Net Position

-Statement of Cash Flows

2. Although there are many similarities among the financial statements for a government hospital and a not-for-profit hospital, the key differences are:

-Net assets for not-for-profit hospitals are classified as unrestricted, temporarily restricted, and permanently restricted. Net position for government hospitals are classified as unrestricted, restricted, and net investment in capital assets.

-Not-for-profit hospitals report a statement of operations and a statement of changes in net assets. Government hospitals report a statement of revenues, expenses, and changes in net position.

-Not-for-profit hospitals report changes in all three categories of net assets. Government hospitals report only changes in total net position.

-Not-for-profit hospitals report assets released from restrictions. Government hospitals do not report assets released from restrictions.

-Not-for-profit hospitals follow FASB cash flow statement guidance three sections. Not-for-profit hospitals may prepare the statement using either the indirect method or the direct method. Government hospitals follow GASB cash flow statement guidance four sections. Government hospitals must prepare the statement using the direct method.

-Government hospitals defer revenue recognition on reimbursement grants until qualifying costs are incurred. Nongovernment, not-for-profit hospitals do not.

4

For external financial reporting purposes, charity services are reported as

A) Expenses.

B) Revenues.

C) Deductions from revenues.

D) Nonoperating gains and losses.

A) Expenses.

B) Revenues.

C) Deductions from revenues.

D) Nonoperating gains and losses.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

5

A county hospital's patient charges for the year were $3,000,000. Of this amount, 25% is deemed to be uncollectible, 5% was considered to be charity services after the services were provided, and 10% will be reduced by contractual adjustments with third party providers. How much will be reported as expense in the external financial statements?

A) $0.

B) $300,000.

C) $750,000.

D) $1,200,000.

A) $0.

B) $300,000.

C) $750,000.

D) $1,200,000.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

6

If a government hospital gets unrestricted donations that are not a part of a hospital's major ongoing operations, those donations are classified on the statement of revenues, expenses, and changes in net position as

A) An operating revenue.

B) An operating gain.

C) An other financing source.

D) A nonoperating gain.

A) An operating revenue.

B) An operating gain.

C) An other financing source.

D) A nonoperating gain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements about services contributed to a government hospital is true?

A) Government hospitals may report contributed services as operating revenues.

B) Government hospitals are permitted, but not required, to recognize contributed services, regardless of the material value of the services.

C) Government hospitals are required to report contributed services at their fair market value.

D) Government hospitals are required to report contributed services as gains.

A) Government hospitals may report contributed services as operating revenues.

B) Government hospitals are permitted, but not required, to recognize contributed services, regardless of the material value of the services.

C) Government hospitals are required to report contributed services at their fair market value.

D) Government hospitals are required to report contributed services as gains.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

8

Restricted assets of a government hospital are used to account for resources

A) Restricted by donors or grantors.

B) Restricted by bond and other contracts.

C) Restricted by the hospital board of directors.

D) Restricted by management.

A) Restricted by donors or grantors.

B) Restricted by bond and other contracts.

C) Restricted by the hospital board of directors.

D) Restricted by management.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

9

Patient service revenues of a government hospital should be reported in the statement of revenues, expenses, and changes in net position

A) At the standard rates charged for the service regardless of bad debts, contractual adjustments, policy discounts, etc.

B) Net of bad debts, contractual adjustments, policy discounts, charity services.

C) Net of contractual adjustments, policy discounts, charity services, but not net of bad debts.

D) Net of bad debts, contractual adjustments, policy discounts, etc., but not net of charity services.

A) At the standard rates charged for the service regardless of bad debts, contractual adjustments, policy discounts, etc.

B) Net of bad debts, contractual adjustments, policy discounts, charity services.

C) Net of contractual adjustments, policy discounts, charity services, but not net of bad debts.

D) Net of bad debts, contractual adjustments, policy discounts, etc., but not net of charity services.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

10

Hospital equipment that originally cost $150,000 was sold for $60,000. The net book value of the equipment at the date of sale was $75,000. The hospital should report

A) An operating loss of $15,000.

B) A nonoperating loss of $15,000.

C) Expenses of $75,000.

D) Other financing sources of $60,000.

A) An operating loss of $15,000.

B) A nonoperating loss of $15,000.

C) Expenses of $75,000.

D) Other financing sources of $60,000.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

11

Welby County Hospital entered into a capital lease to purchase a new MRI machine. The capitalizable cost of the equipment was $400,000 and the hospital made a $40,000 down payment. The entry required when the asset was acquired was

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

12

The following selected information is taken from the accounting records of the Jackson County Hospital for fiscal year 20X0. All accounts have a normal balance and are listed in alphabetical order. Also, all amounts are in thousands of dollars.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

13

The measurement focus used by governmental hospitals is the

A) Cash measurement focus.

B) Current financial resources measurement focus.

C) Economic resources measurement focus.

D) Accrual measurement focus.

A) Cash measurement focus.

B) Current financial resources measurement focus.

C) Economic resources measurement focus.

D) Accrual measurement focus.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

14

County General Hospital estimates uncollectible accounts to be $112,000 and contractual adjustments to be $79,000. The entry needed to record these estimates would be

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

15

Hospital operating revenues include all of the following except

A) Investment income

B) Patient service revenue

C) Premium fees

D) Cafeteria sales

A) Investment income

B) Patient service revenue

C) Premium fees

D) Cafeteria sales

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

16

Premium fee revenues should be recognized as

A) Revenue in the period the premium was received.

B) Revenue in the period covered by the premium.

C) Deferred revenue until the services are actually provided.

D) Revenue only if services with standard charges equal to or greater than the premium for the period are provided in the period.

A) Revenue in the period the premium was received.

B) Revenue in the period covered by the premium.

C) Deferred revenue until the services are actually provided.

D) Revenue only if services with standard charges equal to or greater than the premium for the period are provided in the period.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

17

A government hospital would not report which category of net position:

A) Specific purpose net position.

B) Unrestricted net position.

C) Restricted net position.

D) Net investment in capital assets.

A) Specific purpose net position.

B) Unrestricted net position.

C) Restricted net position.

D) Net investment in capital assets.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

18

Listed below are selected transactions from the City of Watertown Hospital. All amounts are in thousands of dollars.

Transactions:

1. The hospital provided patient services during the year that had standard charges of $12,500. Contractual adjustments awarded to patients under contracts with insurance companies and under government programs totaled $2,000. Uncollectible accounts are expected to be approximately $800.

2. Nursing and other professional salaries paid during the year totaled $2,300.

3. Depreciation for the year was $500 for the building and $900 for equipment.

4. Medical supplies costing $2,600 were purchased during the year. The inventory of supplies increased from $200 at the beginning of the year to $300 at year end.

5. The hospital received a $4,000 to be used for the purchase of specialized diagnostic equipment.

6. The hospital received a $500 gift to be used for providing specialized coronary care services to patients.

7. The hospital purchased $2,000 of diagnostic equipment with the donation received for that purpose.

8. The hospital incurred $400 of operating expenses for the care of coronary patients consistent with the purposes of that donation.

9. The hospital issued $5,000 of 20-year, 8% bonds at par at mid-year to finance a new addition for the hospital.

10. The hospital estimates that malpractice claims against the hospital of $400 ultimately will result in liabilities of $100 that will have to be paid-but probably will not have to be paid during the next fiscal year.

Requirement: Prepare the journal entries required of a government hospital for these transactions.

Transactions:

1. The hospital provided patient services during the year that had standard charges of $12,500. Contractual adjustments awarded to patients under contracts with insurance companies and under government programs totaled $2,000. Uncollectible accounts are expected to be approximately $800.

2. Nursing and other professional salaries paid during the year totaled $2,300.

3. Depreciation for the year was $500 for the building and $900 for equipment.

4. Medical supplies costing $2,600 were purchased during the year. The inventory of supplies increased from $200 at the beginning of the year to $300 at year end.

5. The hospital received a $4,000 to be used for the purchase of specialized diagnostic equipment.

6. The hospital received a $500 gift to be used for providing specialized coronary care services to patients.

7. The hospital purchased $2,000 of diagnostic equipment with the donation received for that purpose.

8. The hospital incurred $400 of operating expenses for the care of coronary patients consistent with the purposes of that donation.

9. The hospital issued $5,000 of 20-year, 8% bonds at par at mid-year to finance a new addition for the hospital.

10. The hospital estimates that malpractice claims against the hospital of $400 ultimately will result in liabilities of $100 that will have to be paid-but probably will not have to be paid during the next fiscal year.

Requirement: Prepare the journal entries required of a government hospital for these transactions.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

19

Hospitals disclose the level of charity services provided by disclosing

A) The amount of revenues foregone in providing the services

B) The direct costs of providing charity services

C) Both the direct and indirect costs of providing charity services

D) The quantities and types of charity services provided

A) The amount of revenues foregone in providing the services

B) The direct costs of providing charity services

C) Both the direct and indirect costs of providing charity services

D) The quantities and types of charity services provided

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

20

County Medical Center received unrestricted contributions of $22,000. The hospital used the contributions to support general services. These contributions would be reported on the statement of cash flows as

A) Operating activities.

B) Noncapital financing activities.

C) Capital and related financing activities.

D) Investing activities.

A) Operating activities.

B) Noncapital financing activities.

C) Capital and related financing activities.

D) Investing activities.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following are reported by both government and nongovernment, not-for-profit hospitals?

A) Bad debt expense.

B) Restricted net position.

C) Investment income.

D) Unrestricted net position.

A) Bad debt expense.

B) Restricted net position.

C) Investment income.

D) Unrestricted net position.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

22

Nongovernment not-for-profit hospitals reported assets limited as to use for

A) Assets limited to a specific use by donors, by contracts, or by the hospital board.

B) Assets limited to a specific use by contracts or by the hospital board.

C) Assets limited to a specific use by contracts only.

D) Assets limited to a specific use by the hospital board only.

A) Assets limited to a specific use by donors, by contracts, or by the hospital board.

B) Assets limited to a specific use by contracts or by the hospital board.

C) Assets limited to a specific use by contracts only.

D) Assets limited to a specific use by the hospital board only.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

23

In the statement of revenues, expenses and changes in net position, expenses of government hospitals should be reported by

A) Natural classifications.

B) Department.

C) Function.

D) Either by natural classification or by function.

A) Natural classifications.

B) Department.

C) Function.

D) Either by natural classification or by function.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

24

Sources of generally accepted accounting principles for government hospitals include

A) AICPA Audit and Accounting Guide, Health Care Organizations.

B) FASAB standards.

C) FASB not-for-profit standards.

D) GAO Yellow Book.

A) AICPA Audit and Accounting Guide, Health Care Organizations.

B) FASAB standards.

C) FASB not-for-profit standards.

D) GAO Yellow Book.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

25

A nongovernment not-for-profit hospital presents all of the following financial statements, except

A) A balance sheet.

B) A statement of operations.

C) A statement of activities.

D) A statement of cash flows.

A) A balance sheet.

B) A statement of operations.

C) A statement of activities.

D) A statement of cash flows.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

26

A government hospital received a cash donation restricted for construction of a new wing to the hospital. How should the donation be reported be reported in the statement of cash flows?

A) Cash inflows from operating activities.

B) Cash inflows from noncapital financing activities.

C) Cash inflows from capital and related financing activities.

D) Cash inflows from investing activities.

A) Cash inflows from operating activities.

B) Cash inflows from noncapital financing activities.

C) Cash inflows from capital and related financing activities.

D) Cash inflows from investing activities.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

27

Which item is reported significantly differently by government hospitals than by nongovernment, not-for-profit hospitals?

A) Patient service revenues.

B) Net position.

C) Assets limited as to use.

D) Charity services.

A) Patient service revenues.

B) Net position.

C) Assets limited as to use.

D) Charity services.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following items are not reported in much the same manner by government hospitals and nongovernment not-for-profit hospitals?

A) Patient service revenues.

B) Donated professional services.

C) Premium fee revenues.

D) Cafeteria sales.

A) Patient service revenues.

B) Donated professional services.

C) Premium fee revenues.

D) Cafeteria sales.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following are reported for government hospitals but not for nongovernment, not-for-profit hospitals?

A) Capital leases.

B) Deferred inflows.

C) Net patient service revenues.

D) Premium fees.

A) Capital leases.

B) Deferred inflows.

C) Net patient service revenues.

D) Premium fees.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

30

Government hospitals and nongovernment not-for-profit hospitals report all of the following in the same manner except

A) Patient service revenues

B) Rent revenues

C) Provision for bad debts

D) Charity services

A) Patient service revenues

B) Rent revenues

C) Provision for bad debts

D) Charity services

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

31

A nongovernment not-for-profit hospital presents the following categories on its statement of cash flows, except

A) Cash flows from operating activities.

B) Cash flows from investing activities.

C) Cash flows from noncapital financing activities.

D) Cash flows from financing activities.

A) Cash flows from operating activities.

B) Cash flows from investing activities.

C) Cash flows from noncapital financing activities.

D) Cash flows from financing activities.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

32

A government hospital board of directors voted to set aside $3,000,000 of investments for future hospital expansion. In the hospital balance sheet, these resources should be reported.

A) Unrestricted net position.

B) Restricted net position.

C) Net investment in capital asset.

D) Permanently restricted net position.

A) Unrestricted net position.

B) Restricted net position.

C) Net investment in capital asset.

D) Permanently restricted net position.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

33

Dublin State Hospital would have earned $3,000,000 of patient service revenue under its established rate structure for the year. However, it does not expect to collect this amount due to charity allowances of $75,000, discounts to third-party payers of $200,000, and an estimated uncollectible amount of $50,000. For the year, how much should Dublin State Hospital report as patient service revenue?

A) $3,000,000.

B) $2,800,000.

C) $2,725,000.

D) $2,675,000.

A) $3,000,000.

B) $2,800,000.

C) $2,725,000.

D) $2,675,000.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following statements of a government hospital is not required?

A) Statement of cash flows.

B) Balance sheet.

C) Statement of revenues, expenses and changes in net position.

D) Statement of changes in fund balances.

A) Statement of cash flows.

B) Balance sheet.

C) Statement of revenues, expenses and changes in net position.

D) Statement of changes in fund balances.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

35

The standard charges for all services provided by a government hospital during the year were $5,000,000. The charges included charges for charity services valued at $100,000. They were reduced by contractual adjustments related to insurance contracts of $400,000. Uncollectible amounts related to these services are estimated at $150,000. The hospital must report net patient services revenues and expenses, respectively, of

A) $4,900,000 and $550,000

B) $4,500,000 and $150,000

C) $4,750,000 and $400,000

D) $4,350,000 and $0

A) $4,900,000 and $550,000

B) $4,500,000 and $150,000

C) $4,750,000 and $400,000

D) $4,350,000 and $0

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 35 flashcards in this deck.