Deck 3: Consolidated Statements: Subsequent to Acquisition

Full screen (f)

Question

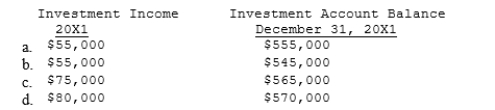

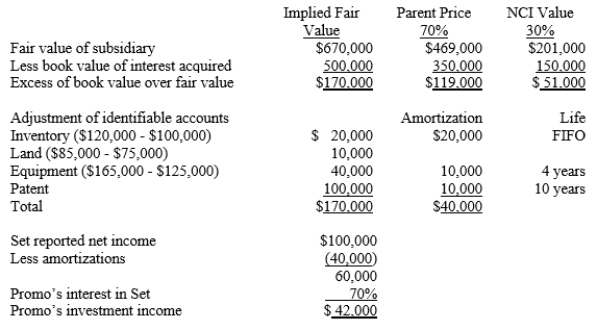

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows:  The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the sophisticated equity method?

A)$42,000

B)$49,000

C)$70,000

D)$100,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the sophisticated equity method?

A)$42,000

B)$49,000

C)$70,000

D)$100,000

Question

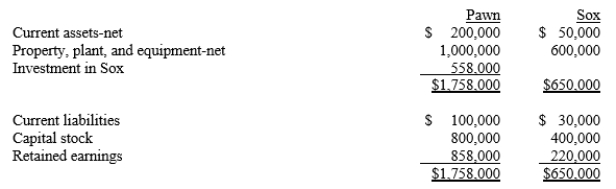

Balance sheet information for Pawn Company and its 90%-owned subsidiary, Sox Corporation, at December 31, 20X1, is summarized as follows:  Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

The consolidated balance sheet of Pawn and Sox at December 31, 20X1 will show

A)Investment in Sioux, $558,000.

B)Capital stock, $800,000.

C)Retained earnings, $1,078,000.

D)Noncontrolling interest, $65,000.

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.The consolidated balance sheet of Pawn and Sox at December 31, 20X1 will show

A)Investment in Sioux, $558,000.

B)Capital stock, $800,000.

C)Retained earnings, $1,078,000.

D)Noncontrolling interest, $65,000.

Question

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows:  The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What is consolidated net income if Promo recognizes income from Set using the sophisticated equity method?

A)$242,000

B)$249,000

C)$270,000

D)$300,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What is consolidated net income if Promo recognizes income from Set using the sophisticated equity method?

A)$242,000

B)$249,000

C)$270,000

D)$300,000

Question

Balance sheet information for Pawn Company and its 90%-owned subsidiary, Sox Corporation, at December 31, 20X1, is summarized as follows:  Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

Consolidated total assets of Pawn and Sox, at December 31, 20X1, will be ____.

A)$1,785,000

B)$1,850,000

C)$2,343,000

D)$2,408,000

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.Consolidated total assets of Pawn and Sox, at December 31, 20X1, will be ____.

A)$1,785,000

B)$1,850,000

C)$2,343,000

D)$2,408,000

Question

Question

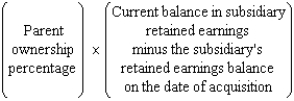

If in the consolidation process the investment in subsidiary account is increased or decreased by the amount determined by the following calculation:  the investment account is being converted from

the investment account is being converted from

A)cost to simple equity.

B)cost to sophisticated equity.

C)simple equity to sophisticated equity.

D)simple equity to cost.

the investment account is being converted fromA)cost to simple equity.

B)cost to sophisticated equity.

C)simple equity to sophisticated equity.

D)simple equity to cost.

Question

Question

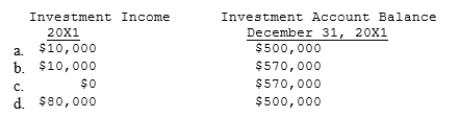

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows:  The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the simple equity method?

A)$33,000

B)$42,000

C)$70,000

D)$100,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the simple equity method?

A)$33,000

B)$42,000

C)$70,000

D)$100,000

Question

Question

Question

Question

Question

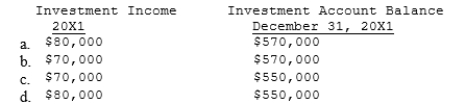

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows:  Using the sophisticated (full) equity method, which of the following amounts are correct?

Using the sophisticated (full) equity method, which of the following amounts are correct?

Using the sophisticated (full) equity method, which of the following amounts are correct? Question

Question

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows:  Using the cost method, which of the following amounts are correct?

Using the cost method, which of the following amounts are correct?

Using the cost method, which of the following amounts are correct? Question

Question

Question

Question

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows:  Using the simple equity method, which of the following amounts are correct?

Using the simple equity method, which of the following amounts are correct?

Using the simple equity method, which of the following amounts are correct? Question

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X2. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X2. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

Question

Question

Prossart Company owned 70% of the outstanding stock of Say Company. During the annual goodwill impairment test, the following information pertaining to Say was noted:  The amount of goodwill impairment loss that would be recorded on Prossart's books would be:

The amount of goodwill impairment loss that would be recorded on Prossart's books would be:

A)$200,000

B)$140,000

C)$100,000

D)$70,000

The amount of goodwill impairment loss that would be recorded on Prossart's books would be:A)$200,000

B)$140,000

C)$100,000

D)$70,000

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the sophisticated equity method.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the sophisticated equity method.

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 20X1 and December 31, 20X2 assuming that Parent records its investment in Subsidiary using

a. the cost method

b. the simple equity methodIf date alignment entries are not required, give rationale.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 20X1 and December 31, 20X2 assuming that Parent records its investment in Subsidiary using

a. the cost method

b. the simple equity methodIf date alignment entries are not required, give rationale.

Question

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Prepare a value analysis schedule

b. Prepare a determination and distribution of excess schedule

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Prepare a value analysis schedule

b. Prepare a determination and distribution of excess schedule

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the

a.cost method

b.simple equity method

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the

a.cost method

b.simple equity method

Question

Question

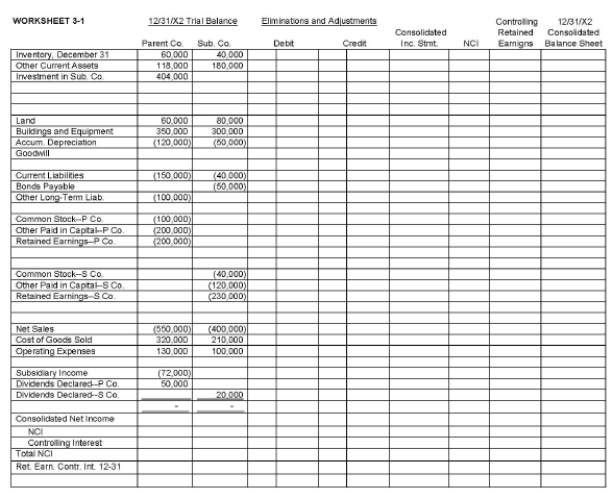

Refer to the information below and Worksheet 3-1.

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Complete the consolidating worksheet for December 31, 20X2.

b. Prepare supportive Income Distribution Schedules for Subsidiary and Parent.

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Complete the consolidating worksheet for December 31, 20X2.

b. Prepare supportive Income Distribution Schedules for Subsidiary and Parent.

Question

Question

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X1. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X1. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

Question

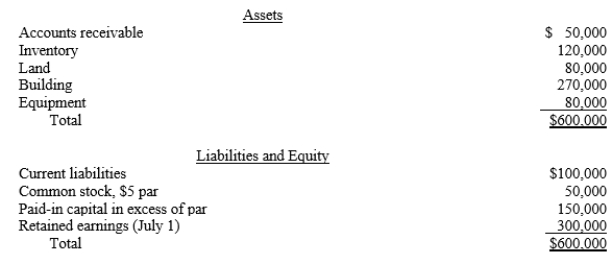

The Paris Company purchased an 80% interest in Seine, Inc. for $600,000 on July 1, 20X1, when Seine had the following balance sheet:

The inventory is understated by $20,000 and is sold in the third quarter of 20X1. The building has a fair value of $320,000 and a 10-year remaining life. The equipment has a fair value of $120,000 and a remaining life of 5 years. Any remaining excess is attributed to goodwill.

From July 1 through December 31, 20X1, Seine had net income of $100,000 and paid $10,000 in dividends.

Assume that Paris uses the cost method to record its investment in Seine.

Required:

a.Prepare a determination and distribution of excess schedule as of July 1, 20X1.

b.Prepare the eliminations and adjustments that would be made on the December 31, 20X1, consolidated worksheet to eliminate the investment in Seine. Distribute and amortize any excess.

The inventory is understated by $20,000 and is sold in the third quarter of 20X1. The building has a fair value of $320,000 and a 10-year remaining life. The equipment has a fair value of $120,000 and a remaining life of 5 years. Any remaining excess is attributed to goodwill.

From July 1 through December 31, 20X1, Seine had net income of $100,000 and paid $10,000 in dividends.

Assume that Paris uses the cost method to record its investment in Seine.

Required:

a.Prepare a determination and distribution of excess schedule as of July 1, 20X1.

b.Prepare the eliminations and adjustments that would be made on the December 31, 20X1, consolidated worksheet to eliminate the investment in Seine. Distribute and amortize any excess.

Question

The determination and distribution schedule for the consolidation of Petoskey (80% interest) and Sable reads in part:

Prepare the elimination entries to distribute and amortize the excess purchase cost on

a. 1/1/X1, the date of acquisition

b. 12/31/X1, the end of the first year following the acquisition

c. 12/31/X3, the end of the third year following the acquisition.

Prepare the elimination entries to distribute and amortize the excess purchase cost on

a. 1/1/X1, the date of acquisition

b. 12/31/X1, the end of the first year following the acquisition

c. 12/31/X3, the end of the third year following the acquisition.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/34

Play

Full screen (f)

Deck 3: Consolidated Statements: Subsequent to Acquisition

1

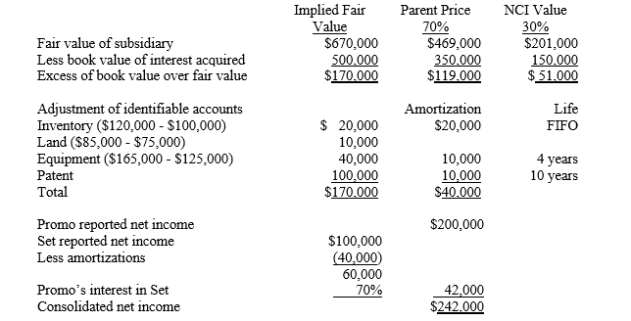

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows: The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the sophisticated equity method?

A)$42,000

B)$49,000

C)$70,000

D)$100,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the sophisticated equity method?

A)$42,000

B)$49,000

C)$70,000

D)$100,000

A

Determination and Distribution of Excess Schedule:

Determination and Distribution of Excess Schedule:

2

Balance sheet information for Pawn Company and its 90%-owned subsidiary, Sox Corporation, at December 31, 20X1, is summarized as follows: Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

The consolidated balance sheet of Pawn and Sox at December 31, 20X1 will show

A)Investment in Sioux, $558,000.

B)Capital stock, $800,000.

C)Retained earnings, $1,078,000.

D)Noncontrolling interest, $65,000.

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.The consolidated balance sheet of Pawn and Sox at December 31, 20X1 will show

A)Investment in Sioux, $558,000.

B)Capital stock, $800,000.

C)Retained earnings, $1,078,000.

D)Noncontrolling interest, $65,000.

B

The consolidated balance sheet will show capital stock of $800,000 as the consolidated financial statements will reflect the amount of the equity with outside shareholders, which is that of the parent and that attributable to the NCI. The NCI would be 10% of the net assets, or $62,000.

The Investment in Sox account will be eliminated in consolidation.

The consolidated balance sheet will show capital stock of $800,000 as the consolidated financial statements will reflect the amount of the equity with outside shareholders, which is that of the parent and that attributable to the NCI. The NCI would be 10% of the net assets, or $62,000.

The Investment in Sox account will be eliminated in consolidation.

3

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows: The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What is consolidated net income if Promo recognizes income from Set using the sophisticated equity method?

A)$242,000

B)$249,000

C)$270,000

D)$300,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What is consolidated net income if Promo recognizes income from Set using the sophisticated equity method?

A)$242,000

B)$249,000

C)$270,000

D)$300,000

A

Determination and Distribution of Excess Schedule:

Determination and Distribution of Excess Schedule:

4

Balance sheet information for Pawn Company and its 90%-owned subsidiary, Sox Corporation, at December 31, 20X1, is summarized as follows: Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.

Consolidated total assets of Pawn and Sox, at December 31, 20X1, will be ____.

A)$1,785,000

B)$1,850,000

C)$2,343,000

D)$2,408,000

Pawn acquired its interest in Sox for cash at book value several years ago when Sox's assets and liabilities were equal to their fair values.Consolidated total assets of Pawn and Sox, at December 31, 20X1, will be ____.

A)$1,785,000

B)$1,850,000

C)$2,343,000

D)$2,408,000

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

5

The method of accounting for subsidiaries where investment income is limited to dividends received is the

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

6

If in the consolidation process the investment in subsidiary account is increased or decreased by the amount determined by the following calculation: the investment account is being converted from

A)cost to simple equity.

B)cost to sophisticated equity.

C)simple equity to sophisticated equity.

D)simple equity to cost.

the investment account is being converted fromA)cost to simple equity.

B)cost to sophisticated equity.

C)simple equity to sophisticated equity.

D)simple equity to cost.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

7

In a mid-year purchase when the subsidiary's books are not closed until the end of the year, the consolidated net income contains the parent's share of the

A)subsidiary's income earned for the entire year.

B)subsidiary's income earned from the beginning of the year to the date of acquisition.

C)subsidiary's income earned from the date of acquisition to the end of the year.

D)dividends received from the subsidiary during the period of ownership.

A)subsidiary's income earned for the entire year.

B)subsidiary's income earned from the beginning of the year to the date of acquisition.

C)subsidiary's income earned from the date of acquisition to the end of the year.

D)dividends received from the subsidiary during the period of ownership.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

8

On January 1, 20X1, Promo, Inc. purchased 70% of Set Corporation for $469,000. On that date the book value of the net assets of Set totaled $500,000. Based on the appraisal done at the time of the purchase, all assets and liabilities had book values equal to their fair values except as follows: The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.

During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the simple equity method?

A)$33,000

B)$42,000

C)$70,000

D)$100,000

The remaining excess of cost over book value was allocated to a patent with a 10-year useful life.During 20X1 Promo reported net income of $200,000 and Set had net income of $100,000.

What income from subsidiary did Promo include in its net income if Promo uses the simple equity method?

A)$33,000

B)$42,000

C)$70,000

D)$100,000

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

9

In consolidated financial statements, it is expected that:

A)Dividends declared equals the sum of the total parent company's declared dividends and the total subsidiary's declared dividends.

B)Retained Earnings equals the sum of the controlling interest's separate retained earnings and the noncontrolling interest's separate retained earnings.

C)Common Stock equals the sum of the parent company's outstanding shares and the subsidiary's outstanding shares.

D)Consolidated Net Income equals the sum of the income distributed to the controlling interest and the income distributed to the noncontrolling interest.

A)Dividends declared equals the sum of the total parent company's declared dividends and the total subsidiary's declared dividends.

B)Retained Earnings equals the sum of the controlling interest's separate retained earnings and the noncontrolling interest's separate retained earnings.

C)Common Stock equals the sum of the parent company's outstanding shares and the subsidiary's outstanding shares.

D)Consolidated Net Income equals the sum of the income distributed to the controlling interest and the income distributed to the noncontrolling interest.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

10

The method of accounting for subsidiaries that is required for influential investments is the

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

11

On January 1, 20X1, Payne Corp. purchased 70% of Shayne Corp.'s $10 par common stock for $900,000. On this date, the carrying amount of Shayne's net assets was $1,000,000. The fair values of Shayne's identifiable assets and liabilities were the same as their carrying amounts except for plant assets (net), which were $200,000 in excess of the carrying amount. For the year ended December 31, 20X1, Shayne had net income of $150,000 and paid cash dividends totaling $90,000. Excess attributable to plant assets is amortized over 10 years.

In the December 31, 20X1, consolidated balance sheet, noncontrolling interest should be reported at ____.

A)$282,714

B)$300,500

C)$397,714

D)$345,500

In the December 31, 20X1, consolidated balance sheet, noncontrolling interest should be reported at ____.

A)$282,714

B)$300,500

C)$397,714

D)$345,500

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

12

The method of accounting for subsidiaries that better reflects the investment account on parent-only financial statements is the

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

A)cost method.

B)simple equity method.

C)investment method.

D)sophisticated equity method.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

13

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows: Using the sophisticated (full) equity method, which of the following amounts are correct?

Using the sophisticated (full) equity method, which of the following amounts are correct? Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements applying to the use of the equity method versus the cost method is true?

A)A parent company may incur a delay in closing its books while waiting for a subsidiary that it accounts for using the cost method to determine its income.

B)If no dividends were paid by the subsidiary, the investment account would have the same balance under both methods.

C)The method used has no impact on consolidated financial statements.

D)An advantage of the equity method is that no amortization of excess adjustments needs to be made on the consolidated worksheet.

A)A parent company may incur a delay in closing its books while waiting for a subsidiary that it accounts for using the cost method to determine its income.

B)If no dividends were paid by the subsidiary, the investment account would have the same balance under both methods.

C)The method used has no impact on consolidated financial statements.

D)An advantage of the equity method is that no amortization of excess adjustments needs to be made on the consolidated worksheet.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

15

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows: Using the cost method, which of the following amounts are correct?

Using the cost method, which of the following amounts are correct? Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

16

Alpha purchased an 80% interest in Beta on June 30, 20X1. Both Alpha's and Beta's reporting periods end December 31. Which of the following represents the controlling interest in consolidated net income for 20X1?

A)100% of Alpha's July 1-December 31 income plus 80% of Beta's July 1-December 31 income

B)100% of Alpha's July 1-December 31 income plus 100% of Beta's July 1-December 31 income

C)100% of Alpha's January 1-December 31 income plus 80% of Beta's July 1-December 31 income

D)100% of Alpha's January 1-December 31 income plus 80% of Beta's January 1-December 31 income

A)100% of Alpha's July 1-December 31 income plus 80% of Beta's July 1-December 31 income

B)100% of Alpha's July 1-December 31 income plus 100% of Beta's July 1-December 31 income

C)100% of Alpha's January 1-December 31 income plus 80% of Beta's July 1-December 31 income

D)100% of Alpha's January 1-December 31 income plus 80% of Beta's January 1-December 31 income

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

17

How is the portion of consolidated earnings to be assigned to noncontrolling interest in consolidated financial statements determined?

A)The net income of the parent is subtracted from the subsidiary's net income to determine the noncontrolling interest.

B)The subsidiary's net income is extended to the noncontrolling interest.

C)The amount of the subsidiary's earnings is multiplied by the noncontrolling's percentage ownership and is adjusted for the excess cost amortization applicable to the NCI.

D)The amount of consolidated earnings determined on the consolidated working papers is multiplied by the noncontrolling interest percentage at the balance-sheet date.

A)The net income of the parent is subtracted from the subsidiary's net income to determine the noncontrolling interest.

B)The subsidiary's net income is extended to the noncontrolling interest.

C)The amount of the subsidiary's earnings is multiplied by the noncontrolling's percentage ownership and is adjusted for the excess cost amortization applicable to the NCI.

D)The amount of consolidated earnings determined on the consolidated working papers is multiplied by the noncontrolling interest percentage at the balance-sheet date.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

18

What is the effect if an unconsolidated subsidiary is accounted for by the equity method but consolidated statements are being prepared for the parent company and other subsidiaries?

A)All of the unconsolidated subsidiary's accounts will be included individually in the consolidated statements.

B)The consolidated retained earnings will not reflect the earnings of the unconsolidated subsidiary.

C)The consolidated retained earnings will be the same as if the subsidiary had been included in the consolidation.

D)Dividend revenue from the unconsolidated subsidiary will be reflected in consolidated net income.

A)All of the unconsolidated subsidiary's accounts will be included individually in the consolidated statements.

B)The consolidated retained earnings will not reflect the earnings of the unconsolidated subsidiary.

C)The consolidated retained earnings will be the same as if the subsidiary had been included in the consolidation.

D)Dividend revenue from the unconsolidated subsidiary will be reflected in consolidated net income.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

19

Pete purchased 100% of the common stock of the Sanburn Company on January 1, 20X1, for $500,000. On that date, the stockholders' equity of Sanburn Company was $380,000. On the purchase date, inventory of Sanburn Company, which was sold during 20X1, was understated by $20,000. Any remaining excess of cost over book value is attributable to patent with a 20-year life. The reported income and dividends paid by Sanburn Company were as follows: Using the simple equity method, which of the following amounts are correct?

Using the simple equity method, which of the following amounts are correct? Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

20

On January 1, 20X1, Rabb Corp. purchased 80% of Sunny Corp.'s $10 par common stock for $975,000. On this date, the carrying amount of Sunny's net assets was $1,000,000. The fair values of Sunny's identifiable assets and liabilities were the same as their carrying amounts except for plant assets (net), which were $100,000 in excess of the carrying amount.

In the January 1, 20X1, consolidated balance sheet, goodwill should be reported at ____.

A)$0

B)$75,750

C)$95,000

D)$118,750

In the January 1, 20X1, consolidated balance sheet, goodwill should be reported at ____.

A)$0

B)$75,750

C)$95,000

D)$118,750

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

21

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X2. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X2. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

22

On January 1, 20X1, Piston, Inc. acquired Spur Corp. While recording the acquisition, Piston established a deferred tax liability. It is most likely that this account was created because

A)the transaction was a tax-free exchange to Piston.

B)Piston had not paid all of the income taxes due the government when acquiring Spur.

C)the transaction was a tax-free exchange to Spur.

D)Spur had not paid all of the income taxes due the government prior to the acquisition by Piston.

A)the transaction was a tax-free exchange to Piston.

B)Piston had not paid all of the income taxes due the government when acquiring Spur.

C)the transaction was a tax-free exchange to Spur.

D)Spur had not paid all of the income taxes due the government prior to the acquisition by Piston.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

23

Prossart Company owned 70% of the outstanding stock of Say Company. During the annual goodwill impairment test, the following information pertaining to Say was noted: The amount of goodwill impairment loss that would be recorded on Prossart's books would be:

A)$200,000

B)$140,000

C)$100,000

D)$70,000

The amount of goodwill impairment loss that would be recorded on Prossart's books would be:A)$200,000

B)$140,000

C)$100,000

D)$70,000

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

24

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the sophisticated equity method.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the sophisticated equity method.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

25

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 20X1 and December 31, 20X2 assuming that Parent records its investment in Subsidiary using

a. the cost method

b. the simple equity methodIf date alignment entries are not required, give rationale.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 20X1 and December 31, 20X2 assuming that Parent records its investment in Subsidiary using

a. the cost method

b. the simple equity methodIf date alignment entries are not required, give rationale.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

26

Under IASB for small and medium entities, goodwill:

A)is subject to impairment procedures.

B)is never adjusted.

C)is amortized over ten years.

D)is not recorded in an acquisition.

A)is subject to impairment procedures.

B)is never adjusted.

C)is amortized over ten years.

D)is not recorded in an acquisition.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

27

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Prepare a value analysis schedule

b. Prepare a determination and distribution of excess schedule

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Prepare a value analysis schedule

b. Prepare a determination and distribution of excess schedule

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

28

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the

a.cost method

b.simple equity method

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare Parent's 20X1 and 20X2 journal entries (after the purchase has been recorded) to record the transactions related to its investment in Subsidiary under the

a.cost method

b.simple equity method

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is not true regarding a subsidiary's tax loss carryovers in an acquisition?

A)The resulting deferred tax asset should be considered when determining the amount of goodwill.

B)The parent will always be able to use a portion of the tax loss carryovers in the current period.

C)A valuation allowance should be provided if it is probable the benefit will not be used.

D)the resulting deferred tax asset should be separated into current and noncurrent components.

A)The resulting deferred tax asset should be considered when determining the amount of goodwill.

B)The parent will always be able to use a portion of the tax loss carryovers in the current period.

C)A valuation allowance should be provided if it is probable the benefit will not be used.

D)the resulting deferred tax asset should be separated into current and noncurrent components.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

30

Refer to the information below and Worksheet 3-1.

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Complete the consolidating worksheet for December 31, 20X2.

b. Prepare supportive Income Distribution Schedules for Subsidiary and Parent.

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Complete the consolidating worksheet for December 31, 20X2.

b. Prepare supportive Income Distribution Schedules for Subsidiary and Parent.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

31

Discuss the merits of accounting for subsidiaries using the:

1) Simple equity method

2) Sophisticated equity method

3) Cost method.

1) Simple equity method

2) Sophisticated equity method

3) Cost method.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

32

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows:

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X1. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of 8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X1. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

33

The Paris Company purchased an 80% interest in Seine, Inc. for $600,000 on July 1, 20X1, when Seine had the following balance sheet:

The inventory is understated by $20,000 and is sold in the third quarter of 20X1. The building has a fair value of $320,000 and a 10-year remaining life. The equipment has a fair value of $120,000 and a remaining life of 5 years. Any remaining excess is attributed to goodwill.

From July 1 through December 31, 20X1, Seine had net income of $100,000 and paid $10,000 in dividends.

Assume that Paris uses the cost method to record its investment in Seine.

Required:

a.Prepare a determination and distribution of excess schedule as of July 1, 20X1.

b.Prepare the eliminations and adjustments that would be made on the December 31, 20X1, consolidated worksheet to eliminate the investment in Seine. Distribute and amortize any excess.

The inventory is understated by $20,000 and is sold in the third quarter of 20X1. The building has a fair value of $320,000 and a 10-year remaining life. The equipment has a fair value of $120,000 and a remaining life of 5 years. Any remaining excess is attributed to goodwill.

From July 1 through December 31, 20X1, Seine had net income of $100,000 and paid $10,000 in dividends.

Assume that Paris uses the cost method to record its investment in Seine.

Required:

a.Prepare a determination and distribution of excess schedule as of July 1, 20X1.

b.Prepare the eliminations and adjustments that would be made on the December 31, 20X1, consolidated worksheet to eliminate the investment in Seine. Distribute and amortize any excess.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

34

The determination and distribution schedule for the consolidation of Petoskey (80% interest) and Sable reads in part:

Prepare the elimination entries to distribute and amortize the excess purchase cost on

a. 1/1/X1, the date of acquisition

b. 12/31/X1, the end of the first year following the acquisition

c. 12/31/X3, the end of the third year following the acquisition.

Prepare the elimination entries to distribute and amortize the excess purchase cost on

a. 1/1/X1, the date of acquisition

b. 12/31/X1, the end of the first year following the acquisition

c. 12/31/X3, the end of the third year following the acquisition.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 34 flashcards in this deck.