Deck 1: Business Combinations: New Rules for a Long-Standing Business Practice

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Cozzi Company is being purchased and has the following balance sheet as of the purchase date:  The price paid for Cozzi's net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The amount of goodwill to be recorded in the purchase is:

The price paid for Cozzi's net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The amount of goodwill to be recorded in the purchase is:

A)$0

B)$150,000

C)$170,000

D)$190,000

The price paid for Cozzi's net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The amount of goodwill to be recorded in the purchase is:A)$0

B)$150,000

C)$170,000

D)$190,000

Question

Question

Question

Question

Question

Publics Company acquired the net assets of Citizen Company during 20X5. The purchase price was $800,000. On the date of the transaction, Citizen had no long-term investments in marketable equity securities and $400,000 in liabilities, of which the fair value approximated book value. The fair value of Citizen assets on the acquisition date was as follows:  How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?

How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?

A)Retained earnings should be reduced by $200,000.

B)A $600,000 gain on acquisition of business should be recognized.

C)A $200,000 gain on acquisition of business should be recognized.

D)A deferred credit of $200,000 should be set up and subsequently amortized to future net income over a period not to exceed 40 years.

How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?A)Retained earnings should be reduced by $200,000.

B)A $600,000 gain on acquisition of business should be recognized.

C)A $200,000 gain on acquisition of business should be recognized.

D)A deferred credit of $200,000 should be set up and subsequently amortized to future net income over a period not to exceed 40 years.

Question

Question

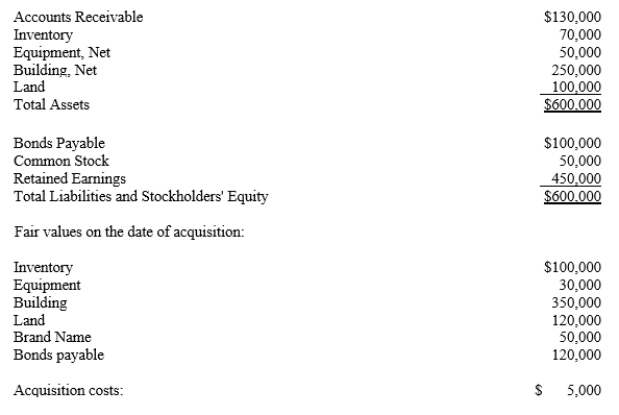

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet:  What is the amount recorded by ACME for the Building?

What is the amount recorded by ACME for the Building?

A)$110,000

B)$20,000

C)$80,000

D)$100,000

What is the amount recorded by ACME for the Building?A)$110,000

B)$20,000

C)$80,000

D)$100,000

Question

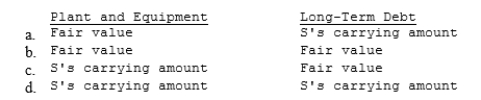

Company B acquired the net assets of Company S in exchange for cash. The acquisition price exceeds the fair value of the net assets acquired. How should Company B determine the amounts to be reported for the plant and equipment, and for long-term debt of the acquired Company S?

Question

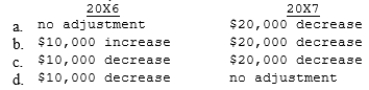

In performing the impairment test for goodwill, the company had the following 20X6 and 20X7 information available.  Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the 20X6 and 20X7 adjustment to goodwill, if any?

Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the 20X6 and 20X7 adjustment to goodwill, if any?

Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the 20X6 and 20X7 adjustment to goodwill, if any? Question

Balter Inc. acquired Jersey Company on January 1, 20X5. When the purchase occurred Jersey Company had the following information related to fixed assets:  The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were:

The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were:

What is the 20X5 depreciation expense Balter will record related to purchasing Jersey Company?

A)$8,000

B)$15,000

C)$28,000

D)$30,000

The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were: What is the 20X5 depreciation expense Balter will record related to purchasing Jersey Company?

A)$8,000

B)$15,000

C)$28,000

D)$30,000

Question

On January 1, 20X1, Honey Bee Corporation purchased the net assets of Green Hornet Company for $1,500,000. On this date, a condensed balance sheet for Green Hornet showed:

Required:

Record the entry on Honey Bee's books for the acquisition of Green Hornet's net assets.

Required:

Record the entry on Honey Bee's books for the acquisition of Green Hornet's net assets.

Question

Question

Vibe Company purchased the net assets of Atlantic Company in a business combination accounted for as a purchase. As a result, goodwill was recorded. For tax purposes, this combination was considered to be a tax-free merger. Included in the assets is a building with an appraised value of $210,000 on the date of the business combination. This asset had a net book value of $70,000. The building had an adjusted tax basis to Atlantic (and to Vibe as a result of the merger) of $120,000. Assuming a 40% income tax rate, at what amount should Vibe record this building on its books after the purchase?

Question

Question

Question

Diamond acquired Heart's net assets. At the time of the acquisition Heart's Balance sheet was as follows:

Required:

Record the entry for the purchase of the net assets of Heart by Diamond at the following cash prices:

a.$700,000

b.$300,000

Required:

Record the entry for the purchase of the net assets of Heart by Diamond at the following cash prices:

a.$700,000

b.$300,000

Question

Question

On January 1, 20X5, Brown Inc. acquired Larson Company's net assets in exchange for Brown's common stock with a par value of $100,000 and a fair value of $800,000. Brown also paid $10,000 in direct acquisition costs and $15,000 in stock issuance costs.

On this date, Larson's condensed account balances showed the following:

Required:

Record Brown's purchase of Larson Company's net assets.

On this date, Larson's condensed account balances showed the following:

Required:

Record Brown's purchase of Larson Company's net assets.

Question

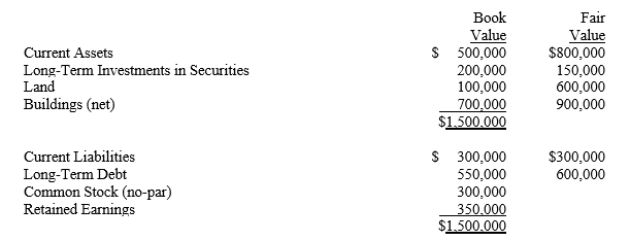

On January 1, 20X5, Zebb and Nottle Companies had condensed balance sheets as shown below:

Required:

Record the acquisition of Nottle's net assets, the issuance of the stock and/or payment of cash, and payment of the related costs. Assume that Zebb issued 30,000 shares of new common stock with a fair value of $25 per share and paid $500,000 cash for all of the net assets of Nottle. Acquisition costs of $50,000 and stock issuance costs of $20,000 were paid in cash. Current assets had a fair value of $650,000, plant and equipment had a fair value of $900,000, and long-term debt had a fair value of $330,000.

Required:

Record the acquisition of Nottle's net assets, the issuance of the stock and/or payment of cash, and payment of the related costs. Assume that Zebb issued 30,000 shares of new common stock with a fair value of $25 per share and paid $500,000 cash for all of the net assets of Nottle. Acquisition costs of $50,000 and stock issuance costs of $20,000 were paid in cash. Current assets had a fair value of $650,000, plant and equipment had a fair value of $900,000, and long-term debt had a fair value of $330,000.

Question

Question

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet:  What is the amount of goodwill or gain related to the acquisition?

What is the amount of goodwill or gain related to the acquisition?

A)Goodwill of $70,000

B)Goodwill of $30,000

C)A gain of $30,000

D)A gain of $70,000

What is the amount of goodwill or gain related to the acquisition?A)Goodwill of $70,000

B)Goodwill of $30,000

C)A gain of $30,000

D)A gain of $70,000

Question

Question

While performing a goodwill impairment test, the company had the following information:  Based upon this information the proper conclusion is:

Based upon this information the proper conclusion is:

A)The company should recognize a goodwill impairment loss of $20,000.

B)Goodwill is not impaired.

C)The company should recognize a goodwill impairment loss of $40,000.

D)The company should recognize a goodwill impairment loss of $60,000.

Based upon this information the proper conclusion is:A)The company should recognize a goodwill impairment loss of $20,000.

B)Goodwill is not impaired.

C)The company should recognize a goodwill impairment loss of $40,000.

D)The company should recognize a goodwill impairment loss of $60,000.

Question

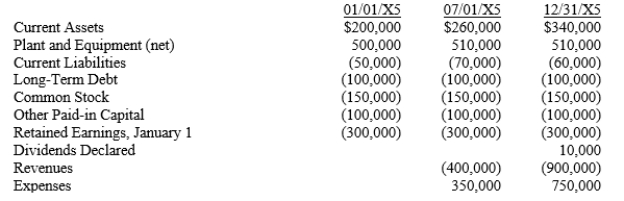

On January 1, July 1, and December 31, 20X5, a condensed trial balance for Nelson Company showed the following debits and (credits):

Assume that, on July 1, 20X5, Systems Corporation purchased the net assets of Nelson Company for $750,000 in cash. On this date, the fair values for certain net assets were:

Current Assets

$280,000

Plant and Equipment (remaining life of 10 years)600,000

Nelson Company's books were NOT closed on June 30, 20X5.

For all of 20X5, Systems' revenues and expenses were $1,500,000 and $1,200,000, respectively.

Required:

(1)Record the entry on Systems' books for the July 1, 20X5 purchase of Nelson.

Assume that, on July 1, 20X5, Systems Corporation purchased the net assets of Nelson Company for $750,000 in cash. On this date, the fair values for certain net assets were:

Current Assets

$280,000

Plant and Equipment (remaining life of 10 years)600,000

Nelson Company's books were NOT closed on June 30, 20X5.

For all of 20X5, Systems' revenues and expenses were $1,500,000 and $1,200,000, respectively.

Required:

(1)Record the entry on Systems' books for the July 1, 20X5 purchase of Nelson.

Question

Question

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet:  What is the amount of gain or loss on disposal of business should Comb Corp. recognize?

What is the amount of gain or loss on disposal of business should Comb Corp. recognize?

A)Gain of $60,000

B)Gain of $60,000

C)Loss of $30,000

D)Loss of $60,000

What is the amount of gain or loss on disposal of business should Comb Corp. recognize?A)Gain of $60,000

B)Gain of $60,000

C)Loss of $30,000

D)Loss of $60,000

Question

Question

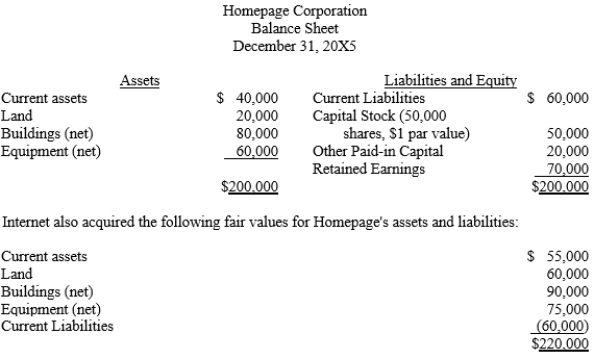

Internet Corporation is considering the acquisition of Homepage Corporation and has obtained the following audited condensed balance sheet:

Internet and Homepage agree on a price of $280,000 for Homepage's net assets. Prepare the necessary journal entry to record the purchase given the following scenarios:

a.Internet pays cash for Homepage Corporation and incurs $5,000 of acquisition costs.

b.Internet issues its $5 par value stock as consideration. The fair value of the stock at the acquisition date is $50 per share. Additionally, Internet incurs $5,000 of security issuance costs.

Internet and Homepage agree on a price of $280,000 for Homepage's net assets. Prepare the necessary journal entry to record the purchase given the following scenarios:

a.Internet pays cash for Homepage Corporation and incurs $5,000 of acquisition costs.

b.Internet issues its $5 par value stock as consideration. The fair value of the stock at the acquisition date is $50 per share. Additionally, Internet incurs $5,000 of security issuance costs.

Question

Question

Poplar Corp. acquires the net assets of Sapling Company, which has the following balance sheet:

If Poplar paid $300,000 what journal entries would be recorded by both Poplar Corp. and Sapling Company?

If Poplar paid $300,000 what journal entries would be recorded by both Poplar Corp. and Sapling Company?

Question

The Chan Corporation purchased the net assets (existing liabilities were assumed) of the Don Company for $900,000 cash. The balance sheet for the Don Company on the date of acquisition showed the following:

Required:

The equipment has a fair value of $300,000, and the plant assets have a fair value of $500,000. Assume that the Chan Corporation has an effective tax rate of 40%. Prepare the entry to record the purchase of the Don Company for each of the following separate cases with specific added information:

a.The sale is a nontaxable exchange to the seller that limits the buyer to depreciation and amortization on only book value for tax purposes.

b.The bonds have a current fair value of $190,000. The transaction is a taxable exchange.

c.There are $100,000 of prior-year losses that can be used to claim a tax refund. The transaction is a taxable exchange.

d.There are $150,000 of past losses that can be carried forward to future years to offset taxes that will be due. The transaction is a taxable exchange.

Required:

The equipment has a fair value of $300,000, and the plant assets have a fair value of $500,000. Assume that the Chan Corporation has an effective tax rate of 40%. Prepare the entry to record the purchase of the Don Company for each of the following separate cases with specific added information:

a.The sale is a nontaxable exchange to the seller that limits the buyer to depreciation and amortization on only book value for tax purposes.

b.The bonds have a current fair value of $190,000. The transaction is a taxable exchange.

c.There are $100,000 of prior-year losses that can be used to claim a tax refund. The transaction is a taxable exchange.

d.There are $150,000 of past losses that can be carried forward to future years to offset taxes that will be due. The transaction is a taxable exchange.

Question

Question

The Blue Reef Company purchased the net assets of the Pink Coral Company on January 1, 20X1, and made the following entry to record the purchase:

Required:

Make the required entry on January 1, 20X3, assuming that additional shares would be issued on that date to compensate for any fall in the value of Blue Reef common stock below $16 per share. The settlement would be to cure the deficiency by issuing added shares based on their fair value on January 1, 20X3. The fair price of the shares on January 1, 20X3 was $10.

Required:

Make the required entry on January 1, 20X3, assuming that additional shares would be issued on that date to compensate for any fall in the value of Blue Reef common stock below $16 per share. The settlement would be to cure the deficiency by issuing added shares based on their fair value on January 1, 20X3. The fair price of the shares on January 1, 20X3 was $10.

Question

On January 1, 20X3 the fair values of Pink Coral's net assets were as follows:

On January 1, 20X3, Blue Reef Company purchased the net assets of the Pink Coral Company by issuing 100,000 shares of its $1 par value stock when the fair value of the stock was $6.20. It was further agreed that Blue Reef would pay an additional amount on January 1, 20X5, if the average income during the 2-year period of 20X3-20X4 exceeded $80,000 per year. The expected value of this consideration was calculated as $184,000; the measurement period is one year. Blue Reef paid $15,000 in professional fees to negotiate the purchase and construct the acquisition agreement and $10,000 in stock issuance costs.

Required: Prepare Blue Reef's entries:

a) on January 1, 20X3 to record the acquisition

b) on August 1, 20X3 to revise the contingent consideration to $170,000

c) on January 1, 20X5 to settle the contingent consideration clause of the agreement for $175,000

On January 1, 20X3, Blue Reef Company purchased the net assets of the Pink Coral Company by issuing 100,000 shares of its $1 par value stock when the fair value of the stock was $6.20. It was further agreed that Blue Reef would pay an additional amount on January 1, 20X5, if the average income during the 2-year period of 20X3-20X4 exceeded $80,000 per year. The expected value of this consideration was calculated as $184,000; the measurement period is one year. Blue Reef paid $15,000 in professional fees to negotiate the purchase and construct the acquisition agreement and $10,000 in stock issuance costs.

Required: Prepare Blue Reef's entries:

a) on January 1, 20X3 to record the acquisition

b) on August 1, 20X3 to revise the contingent consideration to $170,000

c) on January 1, 20X5 to settle the contingent consideration clause of the agreement for $175,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/46

Play

Full screen (f)

Deck 1: Business Combinations: New Rules for a Long-Standing Business Practice

1

Some advantages of obtaining control by acquiring a controlling interest in stock include all but:

A)Negotiations are made directly with the acquiree's management.

B)The legal liability of each corporation is limited to its own assets.

C)The cost may be lower since only a controlling interest in the assets, not the total assets, is acquired.

D)Tax advantages may result from preservation of the legal entities.

A)Negotiations are made directly with the acquiree's management.

B)The legal liability of each corporation is limited to its own assets.

C)The cost may be lower since only a controlling interest in the assets, not the total assets, is acquired.

D)Tax advantages may result from preservation of the legal entities.

A

If a company was acquiring a controlling interest in stock, the negotiations would be with the target company's stockholders.

If a company was acquiring a controlling interest in stock, the negotiations would be with the target company's stockholders.

2

Which of the following costs of a business combination can be deducted from the value assigned to paid-in capital in excess of par?

A)Direct and indirect acquisition costs.

B)Direct acquisition costs.

C)Direct acquisition costs and stock issue costs if stock is issued as consideration.

D)Stock issue costs if stock is issued as consideration.

A)Direct and indirect acquisition costs.

B)Direct acquisition costs.

C)Direct acquisition costs and stock issue costs if stock is issued as consideration.

D)Stock issue costs if stock is issued as consideration.

D

Stock issue costs can be deducted from the value assigned to paid-in capital in excess of par when stock is issued as consideration. All other direct and indirect acquisition costs are expensed.

Stock issue costs can be deducted from the value assigned to paid-in capital in excess of par when stock is issued as consideration. All other direct and indirect acquisition costs are expensed.

3

One large Midwestern bank's acquisition of another midwestern bank would be an example of a:

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

D

A horizontal merger occurs when two companies offering similar products or services that are likely competitors in the same marketplace merge.

A horizontal merger occurs when two companies offering similar products or services that are likely competitors in the same marketplace merge.

4

Goodwill results when:

A)a controlling interest is acquired.

B)the price of the acquisition exceeds the sum of the fair values of the net identifiable assets acquired.

C)the fair value of net assets acquired exceeds the acquisition price.

D)the price of the acquisition exceeds the book value of an acquired company.

A)a controlling interest is acquired.

B)the price of the acquisition exceeds the sum of the fair values of the net identifiable assets acquired.

C)the fair value of net assets acquired exceeds the acquisition price.

D)the price of the acquisition exceeds the book value of an acquired company.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

5

A tax advantage of business combination can occur when the existing owner of a company sells out and receives:

A)cash to defer the taxable gain as a "tax-free reorganization."

B)stock to defer the taxable gain as a "tax-free reorganization."

C)cash to create a taxable gain.

D)stock to create a taxable gain.

A)cash to defer the taxable gain as a "tax-free reorganization."

B)stock to defer the taxable gain as a "tax-free reorganization."

C)cash to create a taxable gain.

D)stock to create a taxable gain.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

6

A controlling interest in a company implies that the parent company

A)owns all of the subsidiary's stock.

B)has acquired a majority of the subsidiary's common stock.

C)has paid cash for a majority of the subsidiary's stock.

D)has transferred common stock for a majority of the subsidiary's outstanding bonds and debentures.

A)owns all of the subsidiary's stock.

B)has acquired a majority of the subsidiary's common stock.

C)has paid cash for a majority of the subsidiary's stock.

D)has transferred common stock for a majority of the subsidiary's outstanding bonds and debentures.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

7

When determining the fair values of assets acquired in an acquisition, the highest level of measurement per GAAP is

A)adjusted market value based on prices of similar assets.

B)unadjusted market values in an actively traded market.

C)based on discounted cash flows.

D)the entity's best estimate of an exit or sale value.

A)adjusted market value based on prices of similar assets.

B)unadjusted market values in an actively traded market.

C)based on discounted cash flows.

D)the entity's best estimate of an exit or sale value.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

8

A contingent liability of an acquiree

A)refers to future consideration due that is part of the acquisition agreement.

B)is recorded when it is probable that future events will confirm its existence.

C)may be recorded beyond the measurement period under certain circumstances.

D)should be recorded even if the amount cannot be reasonably estimated.

A)refers to future consideration due that is part of the acquisition agreement.

B)is recorded when it is probable that future events will confirm its existence.

C)may be recorded beyond the measurement period under certain circumstances.

D)should be recorded even if the amount cannot be reasonably estimated.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

9

A(n) ________________ occurs when the management of the target company purchases a controlling interest in that company and the company incurs a significant amount of debt as a result.

A)greenmail

B)statutory merger

C)poison pill

D)leveraged buyout

A)greenmail

B)statutory merger

C)poison pill

D)leveraged buyout

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

10

ABC Co. is acquiring XYZ Inc. XYZ has the following intangible assets:

Patent on a product that is deemed to have no useful life $10,000.

Customer list with an observable fair value of $50,000.

A 5-year operating lease with favorable terms having a discounted present value of $8,000.

Identifiable research and development costs of $100,000.

ABC will record how much for acquired Intangible Assets from the purchase of XYZ Inc?

A)$168,000

B)$58,000

C)$158,000

D)$150,000

Patent on a product that is deemed to have no useful life $10,000.

Customer list with an observable fair value of $50,000.

A 5-year operating lease with favorable terms having a discounted present value of $8,000.

Identifiable research and development costs of $100,000.

ABC will record how much for acquired Intangible Assets from the purchase of XYZ Inc?

A)$168,000

B)$58,000

C)$158,000

D)$150,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

11

A large nation-wide bank's acquisition of a major investment advisory firm would be an example of a:

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

12

Cozzi Company is being purchased and has the following balance sheet as of the purchase date: The price paid for Cozzi's net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The amount of goodwill to be recorded in the purchase is:

A)$0

B)$150,000

C)$170,000

D)$190,000

The price paid for Cozzi's net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The amount of goodwill to be recorded in the purchase is:A)$0

B)$150,000

C)$170,000

D)$190,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

13

Acquisition costs such as the fees of accountants and lawyers that were necessary to negotiate and consummate the purchase are

A)recorded as a deferred asset and amortized over a period not to exceed 15 years

B)expensed if immaterial but capitalized and amortized if over 2% of the acquisition price

C)expensed in the period of the purchase

D)included as part of the price paid for the company purchased

A)recorded as a deferred asset and amortized over a period not to exceed 15 years

B)expensed if immaterial but capitalized and amortized if over 2% of the acquisition price

C)expensed in the period of the purchase

D)included as part of the price paid for the company purchased

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

14

An economic advantage of a business combination includes

A)Utilizing duplicative assets.

B)Creating separate management teams.

C)Shared fixed costs.

D)Horizontally combining levels within the marketing chain.

A)Utilizing duplicative assets.

B)Creating separate management teams.

C)Shared fixed costs.

D)Horizontally combining levels within the marketing chain.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following would not be considered an identifiable intangible asset?

A)Assembled workforce

B)Customer lists

C)Production backlog

D)Internet domain name

A)Assembled workforce

B)Customer lists

C)Production backlog

D)Internet domain name

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

16

Crystal Co. purchased all of the common stock of Sill Corp. on January 1 of the current year. Five years prior to the acquisition, Sill Corp. had issued 30-year bonds bearing an interest rate of 8%. At the time of the acquisition, the prevailing interest rate for similar bonds was 5%. These bonds should be included in the consolidated balance sheet at

A)face value.

B)at a value higher than Sill's recorded value due to the change in interest rates.

C)at a value lower than Sill's recorded value due to the change in interest rates.

D)at Sill's recorded value.

A)face value.

B)at a value higher than Sill's recorded value due to the change in interest rates.

C)at a value lower than Sill's recorded value due to the change in interest rates.

D)at Sill's recorded value.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

17

Publics Company acquired the net assets of Citizen Company during 20X5. The purchase price was $800,000. On the date of the transaction, Citizen had no long-term investments in marketable equity securities and $400,000 in liabilities, of which the fair value approximated book value. The fair value of Citizen assets on the acquisition date was as follows: How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?

A)Retained earnings should be reduced by $200,000.

B)A $600,000 gain on acquisition of business should be recognized.

C)A $200,000 gain on acquisition of business should be recognized.

D)A deferred credit of $200,000 should be set up and subsequently amortized to future net income over a period not to exceed 40 years.

How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?A)Retained earnings should be reduced by $200,000.

B)A $600,000 gain on acquisition of business should be recognized.

C)A $200,000 gain on acquisition of business should be recognized.

D)A deferred credit of $200,000 should be set up and subsequently amortized to future net income over a period not to exceed 40 years.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

18

A building materials company's acquisition of a television station would be an example of a:

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

A)market extension merger.

B)conglomerate merger.

C)product extension merger.

D)horizontal merger.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

19

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet: What is the amount recorded by ACME for the Building?

A)$110,000

B)$20,000

C)$80,000

D)$100,000

What is the amount recorded by ACME for the Building?A)$110,000

B)$20,000

C)$80,000

D)$100,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

20

Company B acquired the net assets of Company S in exchange for cash. The acquisition price exceeds the fair value of the net assets acquired. How should Company B determine the amounts to be reported for the plant and equipment, and for long-term debt of the acquired Company S?

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

21

In performing the impairment test for goodwill, the company had the following 20X6 and 20X7 information available. Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the 20X6 and 20X7 adjustment to goodwill, if any?

Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the 20X6 and 20X7 adjustment to goodwill, if any? Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

22

Balter Inc. acquired Jersey Company on January 1, 20X5. When the purchase occurred Jersey Company had the following information related to fixed assets: The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were:

What is the 20X5 depreciation expense Balter will record related to purchasing Jersey Company?

A)$8,000

B)$15,000

C)$28,000

D)$30,000

The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were: What is the 20X5 depreciation expense Balter will record related to purchasing Jersey Company?

A)$8,000

B)$15,000

C)$28,000

D)$30,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

23

On January 1, 20X1, Honey Bee Corporation purchased the net assets of Green Hornet Company for $1,500,000. On this date, a condensed balance sheet for Green Hornet showed:

Required:

Record the entry on Honey Bee's books for the acquisition of Green Hornet's net assets.

Required:

Record the entry on Honey Bee's books for the acquisition of Green Hornet's net assets.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

24

When an acquisition of another company occurs, FASB requires disclosing all of the following except:

A)amounts recorded for each major class of assets and liabilities.

B)information concerning contingent consideration including a description of the arrangements and the range of outcomes.

C)results of operations for the current period if both companies had remained separate.

D)A qualitative description of factors that make up the goodwill recognized.

A)amounts recorded for each major class of assets and liabilities.

B)information concerning contingent consideration including a description of the arrangements and the range of outcomes.

C)results of operations for the current period if both companies had remained separate.

D)A qualitative description of factors that make up the goodwill recognized.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

25

Vibe Company purchased the net assets of Atlantic Company in a business combination accounted for as a purchase. As a result, goodwill was recorded. For tax purposes, this combination was considered to be a tax-free merger. Included in the assets is a building with an appraised value of $210,000 on the date of the business combination. This asset had a net book value of $70,000. The building had an adjusted tax basis to Atlantic (and to Vibe as a result of the merger) of $120,000. Assuming a 40% income tax rate, at what amount should Vibe record this building on its books after the purchase?

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

26

Orbit Inc. purchased Planet Co. on January 1, 20X3. At that time an existing patent having a 5-year estimated life was assigned a provisional value of $10,000 and goodwill was assigned a value of $100,000. By the end of fiscal year 20X3, better information was available that indicated the fair value of the patent was $20,000. How should intangible assets be reported at the beginning of fiscal year 20X4?

A)Goodwill $100,000 Patent $10,000

B)Goodwill $90,000 Patent $16,000

C)Goodwill $84,000 Patent $16,000

D)Goodwill $90,000 Patent $20,000

A)Goodwill $100,000 Patent $10,000

B)Goodwill $90,000 Patent $16,000

C)Goodwill $84,000 Patent $16,000

D)Goodwill $90,000 Patent $20,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

27

Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded assets and liabilities was $1,500,000 and $250,000, respectively. Jackson also had in-process research and development projects valued at $150,000 and its pension plan's projected benefit obligation exceeded the plan assets by $50,000. What was the amount of the goodwill related to the acquisition?

A)$750,000

B)$50,000

C)$250,000

D)$650,000

A)$750,000

B)$50,000

C)$250,000

D)$650,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

28

Diamond acquired Heart's net assets. At the time of the acquisition Heart's Balance sheet was as follows:

Required:

Record the entry for the purchase of the net assets of Heart by Diamond at the following cash prices:

a.$700,000

b.$300,000

Required:

Record the entry for the purchase of the net assets of Heart by Diamond at the following cash prices:

a.$700,000

b.$300,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

29

Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded assets and liabilities was $1,500,000 and $250,000, respectively. If Jackson meets specified sales targets, Jones is required to pay an additional $200,000 in cash per the acquisition agreement. Jones estimates the probability of this to be 50%. The direct costs related to the acquisition were $50,000. What was the amount of the goodwill related to the acquisition?

A)$900,000

B)$950,000

C)$850,000

D)$750,000

A)$900,000

B)$950,000

C)$850,000

D)$750,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

30

On January 1, 20X5, Brown Inc. acquired Larson Company's net assets in exchange for Brown's common stock with a par value of $100,000 and a fair value of $800,000. Brown also paid $10,000 in direct acquisition costs and $15,000 in stock issuance costs.

On this date, Larson's condensed account balances showed the following:

Required:

Record Brown's purchase of Larson Company's net assets.

On this date, Larson's condensed account balances showed the following:

Required:

Record Brown's purchase of Larson Company's net assets.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

31

On January 1, 20X5, Zebb and Nottle Companies had condensed balance sheets as shown below:

Required:

Record the acquisition of Nottle's net assets, the issuance of the stock and/or payment of cash, and payment of the related costs. Assume that Zebb issued 30,000 shares of new common stock with a fair value of $25 per share and paid $500,000 cash for all of the net assets of Nottle. Acquisition costs of $50,000 and stock issuance costs of $20,000 were paid in cash. Current assets had a fair value of $650,000, plant and equipment had a fair value of $900,000, and long-term debt had a fair value of $330,000.

Required:

Record the acquisition of Nottle's net assets, the issuance of the stock and/or payment of cash, and payment of the related costs. Assume that Zebb issued 30,000 shares of new common stock with a fair value of $25 per share and paid $500,000 cash for all of the net assets of Nottle. Acquisition costs of $50,000 and stock issuance costs of $20,000 were paid in cash. Current assets had a fair value of $650,000, plant and equipment had a fair value of $900,000, and long-term debt had a fair value of $330,000.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

32

Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded assets and liabilities was $1,500,000 and $250,000, respectively. Jackson also had unrecorded copyrights valued at $150,000 and its direct costs related to the acquisition were $50,000. What was the amount of the goodwill related to the acquisition?

A)$600,000

B)$650,000

C)$550,000

D)$700,000

A)$600,000

B)$650,000

C)$550,000

D)$700,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

33

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet: What is the amount of goodwill or gain related to the acquisition?

A)Goodwill of $70,000

B)Goodwill of $30,000

C)A gain of $30,000

D)A gain of $70,000

What is the amount of goodwill or gain related to the acquisition?A)Goodwill of $70,000

B)Goodwill of $30,000

C)A gain of $30,000

D)A gain of $70,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

34

Polk issues common stock to acquire all the assets of the Sam Company on January 1, 20X5. There is a contingent share agreement, which states that if the income of the Sam Division exceeds a certain level during 20X5 and 20X6, additional shares will be issued on January 1, 20X7. The impact of issuing the additional shares is to

A)increase the price assigned to fixed assets.

B)have no effect on asset values, but to reassign the amounts assigned to equity accounts.

C)reduce retained earnings.

D)record additional goodwill.

A)increase the price assigned to fixed assets.

B)have no effect on asset values, but to reassign the amounts assigned to equity accounts.

C)reduce retained earnings.

D)record additional goodwill.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

35

While performing a goodwill impairment test, the company had the following information: Based upon this information the proper conclusion is:

A)The company should recognize a goodwill impairment loss of $20,000.

B)Goodwill is not impaired.

C)The company should recognize a goodwill impairment loss of $40,000.

D)The company should recognize a goodwill impairment loss of $60,000.

Based upon this information the proper conclusion is:A)The company should recognize a goodwill impairment loss of $20,000.

B)Goodwill is not impaired.

C)The company should recognize a goodwill impairment loss of $40,000.

D)The company should recognize a goodwill impairment loss of $60,000.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, July 1, and December 31, 20X5, a condensed trial balance for Nelson Company showed the following debits and (credits):

Assume that, on July 1, 20X5, Systems Corporation purchased the net assets of Nelson Company for $750,000 in cash. On this date, the fair values for certain net assets were:

Current Assets

$280,000

Plant and Equipment (remaining life of 10 years)600,000

Nelson Company's books were NOT closed on June 30, 20X5.

For all of 20X5, Systems' revenues and expenses were $1,500,000 and $1,200,000, respectively.

Required:

(1)Record the entry on Systems' books for the July 1, 20X5 purchase of Nelson.

Assume that, on July 1, 20X5, Systems Corporation purchased the net assets of Nelson Company for $750,000 in cash. On this date, the fair values for certain net assets were:

Current Assets

$280,000

Plant and Equipment (remaining life of 10 years)600,000

Nelson Company's books were NOT closed on June 30, 20X5.

For all of 20X5, Systems' revenues and expenses were $1,500,000 and $1,200,000, respectively.

Required:

(1)Record the entry on Systems' books for the July 1, 20X5 purchase of Nelson.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following income factors should not be considered in expected future income when estimating the value of goodwill?

A)sales for the period

B)income tax expense

C)extraordinary items

D)cost of goods sold

A)sales for the period

B)income tax expense

C)extraordinary items

D)cost of goods sold

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

38

ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following information was available related to Comb's balance sheet: What is the amount of gain or loss on disposal of business should Comb Corp. recognize?

A)Gain of $60,000

B)Gain of $60,000

C)Loss of $30,000

D)Loss of $60,000

What is the amount of gain or loss on disposal of business should Comb Corp. recognize?A)Gain of $60,000

B)Gain of $60,000

C)Loss of $30,000

D)Loss of $60,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

39

Orbit Inc. purchased Planet Co. on January 1, 20X3. At that time an existing patent having a 5-year life was not recorded as a separately identified intangible asset. At the end of fiscal year 20X4, it is determined the patent is valued at $20,000, and goodwill has a book value of $100,000. How should intangible assets be reported at the beginning of fiscal year 20X5?

A)Goodwill $100,000 Patent $0

B)Goodwill $100,000 Patent $20,000

C)Goodwill $80,000 Patent $20,000

D)Goodwill $80,000 Patent $16,000

A)Goodwill $100,000 Patent $0

B)Goodwill $100,000 Patent $20,000

C)Goodwill $80,000 Patent $20,000

D)Goodwill $80,000 Patent $16,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

40

Internet Corporation is considering the acquisition of Homepage Corporation and has obtained the following audited condensed balance sheet:

Internet and Homepage agree on a price of $280,000 for Homepage's net assets. Prepare the necessary journal entry to record the purchase given the following scenarios:

a.Internet pays cash for Homepage Corporation and incurs $5,000 of acquisition costs.

b.Internet issues its $5 par value stock as consideration. The fair value of the stock at the acquisition date is $50 per share. Additionally, Internet incurs $5,000 of security issuance costs.

Internet and Homepage agree on a price of $280,000 for Homepage's net assets. Prepare the necessary journal entry to record the purchase given the following scenarios:

a.Internet pays cash for Homepage Corporation and incurs $5,000 of acquisition costs.

b.Internet issues its $5 par value stock as consideration. The fair value of the stock at the acquisition date is $50 per share. Additionally, Internet incurs $5,000 of security issuance costs.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

41

Goodwill is an intangible asset. There are a variety of recommendations about how intangible assets should be included in the financial statements. Discuss the recommendations for proper disclosure of goodwill. Include a comparison with disclosure of other intangible assets.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

42

Poplar Corp. acquires the net assets of Sapling Company, which has the following balance sheet:

If Poplar paid $300,000 what journal entries would be recorded by both Poplar Corp. and Sapling Company?

If Poplar paid $300,000 what journal entries would be recorded by both Poplar Corp. and Sapling Company?

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

43

The Chan Corporation purchased the net assets (existing liabilities were assumed) of the Don Company for $900,000 cash. The balance sheet for the Don Company on the date of acquisition showed the following:

Required:

The equipment has a fair value of $300,000, and the plant assets have a fair value of $500,000. Assume that the Chan Corporation has an effective tax rate of 40%. Prepare the entry to record the purchase of the Don Company for each of the following separate cases with specific added information:

a.The sale is a nontaxable exchange to the seller that limits the buyer to depreciation and amortization on only book value for tax purposes.

b.The bonds have a current fair value of $190,000. The transaction is a taxable exchange.

c.There are $100,000 of prior-year losses that can be used to claim a tax refund. The transaction is a taxable exchange.

d.There are $150,000 of past losses that can be carried forward to future years to offset taxes that will be due. The transaction is a taxable exchange.

Required:

The equipment has a fair value of $300,000, and the plant assets have a fair value of $500,000. Assume that the Chan Corporation has an effective tax rate of 40%. Prepare the entry to record the purchase of the Don Company for each of the following separate cases with specific added information:

a.The sale is a nontaxable exchange to the seller that limits the buyer to depreciation and amortization on only book value for tax purposes.

b.The bonds have a current fair value of $190,000. The transaction is a taxable exchange.

c.There are $100,000 of prior-year losses that can be used to claim a tax refund. The transaction is a taxable exchange.

d.There are $150,000 of past losses that can be carried forward to future years to offset taxes that will be due. The transaction is a taxable exchange.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

44

While acquisitions are often friendly, there are numerous occasions when a party does not want to be acquired. Discuss possible defensive strategies that firms can implement to fend off a hostile takeover attempt.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

45

The Blue Reef Company purchased the net assets of the Pink Coral Company on January 1, 20X1, and made the following entry to record the purchase:

Required:

Make the required entry on January 1, 20X3, assuming that additional shares would be issued on that date to compensate for any fall in the value of Blue Reef common stock below $16 per share. The settlement would be to cure the deficiency by issuing added shares based on their fair value on January 1, 20X3. The fair price of the shares on January 1, 20X3 was $10.

Required:

Make the required entry on January 1, 20X3, assuming that additional shares would be issued on that date to compensate for any fall in the value of Blue Reef common stock below $16 per share. The settlement would be to cure the deficiency by issuing added shares based on their fair value on January 1, 20X3. The fair price of the shares on January 1, 20X3 was $10.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 20X3 the fair values of Pink Coral's net assets were as follows:

On January 1, 20X3, Blue Reef Company purchased the net assets of the Pink Coral Company by issuing 100,000 shares of its $1 par value stock when the fair value of the stock was $6.20. It was further agreed that Blue Reef would pay an additional amount on January 1, 20X5, if the average income during the 2-year period of 20X3-20X4 exceeded $80,000 per year. The expected value of this consideration was calculated as $184,000; the measurement period is one year. Blue Reef paid $15,000 in professional fees to negotiate the purchase and construct the acquisition agreement and $10,000 in stock issuance costs.

Required: Prepare Blue Reef's entries:

a) on January 1, 20X3 to record the acquisition

b) on August 1, 20X3 to revise the contingent consideration to $170,000

c) on January 1, 20X5 to settle the contingent consideration clause of the agreement for $175,000

On January 1, 20X3, Blue Reef Company purchased the net assets of the Pink Coral Company by issuing 100,000 shares of its $1 par value stock when the fair value of the stock was $6.20. It was further agreed that Blue Reef would pay an additional amount on January 1, 20X5, if the average income during the 2-year period of 20X3-20X4 exceeded $80,000 per year. The expected value of this consideration was calculated as $184,000; the measurement period is one year. Blue Reef paid $15,000 in professional fees to negotiate the purchase and construct the acquisition agreement and $10,000 in stock issuance costs.

Required: Prepare Blue Reef's entries:

a) on January 1, 20X3 to record the acquisition

b) on August 1, 20X3 to revise the contingent consideration to $170,000

c) on January 1, 20X5 to settle the contingent consideration clause of the agreement for $175,000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 46 flashcards in this deck.