Deck 8: Budgetary Control and Variance Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

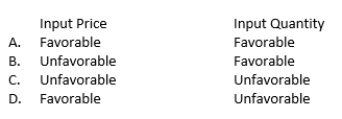

Thurston Company's budget allows for one pound of material to be used for each unit produced.The budget indicates that the material costs $2.50 per pound.Actual units produced totaled 8,000.The company used a total of 8,200 pounds of material at an actual cost of $2.40 per pound.There were no beginning or ending inventories of raw materials.The input price and input quantity variances, respectively, would be:

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/54

Play

Full screen (f)

Deck 8: Budgetary Control and Variance Analysis

1

Cost variance analysis in a single-product company differs significantly from a multi-product company.

False

2

Total Profit Variance = Actual Profit - Master Budget Profit.

True

3

A variance is the difference between a budgeted amount and a forecasted amount.

False

4

Small variances probably indicate random factors at work while large variances could signal a permanent change in the operating environment.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

5

Any profit difference between the master and flexible budgets is due solely to the difference between budgeted and actual sales.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

6

If sales volume exceeds expectations, actual profit will always be higher than budgeted profit.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

7

The primary limitations of variance analysis pertain to relevance and feedback.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

8

The lack of timeliness and specificity in financial variances force organizations to use primarily non-financial controls to ensure that they are meeting organizational objectives.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

9

In general, financial controls are more useful for evaluating managers at higher levels in an organizational hierarchy, while non financial controls are more useful in monitoring and evaluating employees at lower levels.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

10

A good plan is the foundation for effective control.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

11

Cheaper ingredients lead to a favorable price variance, but also may lead to unfavorable quantity variances.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

12

The input quantity variance is also referred to as the input efficiency variance because it captures the efficiency of input resource use.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

13

If a materials input price is higher than budgeted, the result is an unfavorable materials efficiency variance.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

14

Many firms use process control charts and statistical control methods to help employees track performance on a real-time basis.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

15

A budget reconciliation is a report that uses variances to reconcile the difference between master budget profit and actual profit.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

16

Variance analysis may be performed to isolate the profit impact of individual input and output factors.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

17

Variance analysis is a technique used for determining the profit effect due to differences between the actual and budgeted size of the market for a product.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

18

For most organizations, a budget is the benchmark for evaluating actual performance.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

19

Sales Volume Variance = (Actual Sales Quantity - Budgeted Sales Quantity) x Actual Unit Contribution Margin

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

20

In a process control chart, observations outside the control limits are likely due to random fluctuations.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is not a component of the total profit variance?

A)Sales volume variance.

B)Flexible budget variance.

C)Sales price variance.

D)Market size and share variance.

E)All of the above are components of the total profit variance.

A)Sales volume variance.

B)Flexible budget variance.

C)Sales price variance.

D)Market size and share variance.

E)All of the above are components of the total profit variance.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

22

The Farmington Company has a flexible budget based on direct labor hours.At the 100,000 hours level, the budget shows the following variable overhead costs: Indirect materials $ 16,000

Indirect labor $ 44,000 At an activity level of 120,000 hours, total variable costs will be:

A)$19,200

B)$60,000

C)$52,800

D)$72,000

Indirect labor $ 44,000 At an activity level of 120,000 hours, total variable costs will be:

A)$19,200

B)$60,000

C)$52,800

D)$72,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

23

Jackie's Jewelry Company reported the following budgeted and actual results based on sales of 100 units of product: The company's total input quantity variance is:

A)$50 favorable.

B)$160 unfavorable.

C)$150 favorable.

D)$50 unfavorable.

A)$50 favorable.

B)$160 unfavorable.

C)$150 favorable.

D)$50 unfavorable.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

24

If the labor efficiency variance is $1,000unfavorable, then:

A)Budgeted labor rate exceeded actual labor rate.

B)Actual labor rate exceeded budgeted labor rate.

C)Budgeted labor input exceeded actual labor input.

D)Actual labor input exceeded budgeted labor input.

E)None of the above.

A)Budgeted labor rate exceeded actual labor rate.

B)Actual labor rate exceeded budgeted labor rate.

C)Budgeted labor input exceeded actual labor input.

D)Actual labor input exceeded budgeted labor input.

E)None of the above.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

25

The formula for the sales volume variance is:

A)(Actual Sales Quantity - Budgeted Sales Quantity) x Actual Unit Contribution Margin

B)(Budgeted Sales Quantity - Actual Sales Quantity) x Total Profit Variance

C)Flexible Budget Profit - Master Budget Profit.

D)(Budgeted Sales Quantity - Actual Sales Quantity) ÷ Total Profit Variance

E)(Actual Sales Quantity - Budgeted Sales Quantity) ÷ Actual Unit Contribution Margin

A)(Actual Sales Quantity - Budgeted Sales Quantity) x Actual Unit Contribution Margin

B)(Budgeted Sales Quantity - Actual Sales Quantity) x Total Profit Variance

C)Flexible Budget Profit - Master Budget Profit.

D)(Budgeted Sales Quantity - Actual Sales Quantity) ÷ Total Profit Variance

E)(Actual Sales Quantity - Budgeted Sales Quantity) ÷ Actual Unit Contribution Margin

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

26

PVC Pro produces PVC pipe in 12 foot lengths.The following information was provided concerning its labor and materials

How much is the materials price variance?

A)$1,530 F

B)$465 F

C)$1,050 F

D)$1,065 F

How much is the materials price variance?

A)$1,530 F

B)$465 F

C)$1,050 F

D)$1,065 F

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

27

The formula for calculating an input price variance is:

A)(Actual volume less budgeted volume) x actual price.

B)(Budgeted volume less actual volume) x budgeted price.

C)(Budgeted price less actual price) x actual volume.

D)(Actual price less budgeted price) x budgeted volume,

A)(Actual volume less budgeted volume) x actual price.

B)(Budgeted volume less actual volume) x budgeted price.

C)(Budgeted price less actual price) x actual volume.

D)(Actual price less budgeted price) x budgeted volume,

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

28

A favorable materials price variance will occur when:

A)Actual costs of materials were less than budgeted

B)More material was used than was budgeted

C)Actual cost of materials were greater than budgeted

D)Less material was used than was budgeted

A)Actual costs of materials were less than budgeted

B)More material was used than was budgeted

C)Actual cost of materials were greater than budgeted

D)Less material was used than was budgeted

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

29

The two major components of the total profit variance are:

A)Sales volume variance and flexible budget variance.

B)Price variance and quantity variance.

C)Sales volume variance and sales mix variance.

D)Flexible budget variance and quantity variance.

E)None of the above.

A)Sales volume variance and flexible budget variance.

B)Price variance and quantity variance.

C)Sales volume variance and sales mix variance.

D)Flexible budget variance and quantity variance.

E)None of the above.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

30

The starting point for preparing a monthly budget is:

A)Projecting sales.

B)Projecting production.

C)Projecting cash inflows.

D)Projecting cash outflows.

E)Projecting material needs.

A)Projecting sales.

B)Projecting production.

C)Projecting cash inflows.

D)Projecting cash outflows.

E)Projecting material needs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

31

The purpose of creating a flexible budget is to:

A)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual sales.

B)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual variable costs.

C)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual fixed costs.

D)Determine which department is responsible for the overall budget variance.

A)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual sales.

B)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual variable costs.

C)Determine how much of the difference between actual and budgeted profits was due strictly to the difference between budgeted and actual fixed costs.

D)Determine which department is responsible for the overall budget variance.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

32

Sales commissions for the Grant Company are budgeted based on a percent of sales.The sales department budgeted sales of $150,000 for total commissions of $4,500.If actual sales totaled $170,000 the flexible budget will show total commissions of:

A)$24,500

B)$5,100

C)$4,500

D)$15,500

A)$24,500

B)$5,100

C)$4,500

D)$15,500

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

33

The following material budgets have been developed for the Criders Company. If the company purchased 16,000 units, the actual price per pound of material purchased must have been:

A)$6.70

B)$5.00

C)$6.30

D)$5.80

A)$6.70

B)$5.00

C)$6.30

D)$5.80

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

34

Variance analysis is an important tool because:

A)It helps management determine where bottlenecks in the production process occurred

B)It helps management determine better pricing strategies

C)It helps management determine why actual profits varied from budgeted profits

D)It helps management determine which department operated most efficiently.

A)It helps management determine where bottlenecks in the production process occurred

B)It helps management determine better pricing strategies

C)It helps management determine why actual profits varied from budgeted profits

D)It helps management determine which department operated most efficiently.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is not true?

A)If actual sales are greater than budgeted sales, the result is a favorable variance.

B)If actual cost is greater than budgeted cost, the result is an unfavorable variance.

C)If budgeted sales are greater than actual sales, the result is an unfavorable variance.

D)If budgeted cost is greater than actual cost, the result is an unfavorable variance.

E)If actual cost is less than budgeted cost, the result is a favorable variance.

A)If actual sales are greater than budgeted sales, the result is a favorable variance.

B)If actual cost is greater than budgeted cost, the result is an unfavorable variance.

C)If budgeted sales are greater than actual sales, the result is an unfavorable variance.

D)If budgeted cost is greater than actual cost, the result is an unfavorable variance.

E)If actual cost is less than budgeted cost, the result is a favorable variance.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

36

For what purpose is a flexible budget used?

A)To provide various possible outcomes for management to consider.

B)To adjust input prices so that future variances are eliminated.

C)To insure that profit does not drop below a predetermined level.

D)To identify the sources of variances.

A)To provide various possible outcomes for management to consider.

B)To adjust input prices so that future variances are eliminated.

C)To insure that profit does not drop below a predetermined level.

D)To identify the sources of variances.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

37

The controller for Navia, Inc.created a budget prior to the current period.At the end of the period, the controller compared the budget with the actual results.For what purpose is the controller using budgets?

A)Coordination

B)Control

C)Variances

D)Planning

A)Coordination

B)Control

C)Variances

D)Planning

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following items would differ in amount when comparing the master and flexible budgets for a freight company in which actual sales resulted in $2,500,000 based on 8,000 shipments during a period that 7,800 shipments were budgeted?

A)Total sales revenue.

B)Equipment costs.

C)Rent.

D)All of the above will differ.

A)Total sales revenue.

B)Equipment costs.

C)Rent.

D)All of the above will differ.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

39

Given the following data, calculate total profit variance.

A)$2,000 Favorable.

B)$2,000 Unfavorable.

C)$10,000 Unfavorable.

D)$10,000 Favorable.

E)$5,000 Favorable.

A)$2,000 Favorable.

B)$2,000 Unfavorable.

C)$10,000 Unfavorable.

D)$10,000 Favorable.

E)$5,000 Favorable.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following would not result in a variance from budget:

A)A machine breaks down.

B)Budgets are set in a manner making them difficult to achieve.

C)A supplier raises prices.

D)The Chief Executive Officer takes a week of vacation.

A)A machine breaks down.

B)Budgets are set in a manner making them difficult to achieve.

C)A supplier raises prices.

D)The Chief Executive Officer takes a week of vacation.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

41

In comparison to financial measures, nonfinancial measures tend to be?

A)Less timely, less specific.

B)More timely, less specific.

C)Less timely, more specific.

D)More timely, more specific.

A)Less timely, less specific.

B)More timely, less specific.

C)Less timely, more specific.

D)More timely, more specific.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

42

Given the following data, what is the sales mix variance for Rizzo Company?

A)200 Favorable.

B)200 Unfavorable.

C)29,900 Favorable.

D)29,900 Unfavorable.

E)300 Unfavorable.

A)200 Favorable.

B)200 Unfavorable.

C)29,900 Favorable.

D)29,900 Unfavorable.

E)300 Unfavorable.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following trends in variances may not indicate an inherent problem?

A)Marketing personnel overstating costs to give themselves additional leeway in operations.

B)Repeatedly having unfavorable labor efficiency variances.

C)An unexpected increase in demand.

D)A developing problem in the manufacturing process.

E)Finding mostly favorable variances over time.

A)Marketing personnel overstating costs to give themselves additional leeway in operations.

B)Repeatedly having unfavorable labor efficiency variances.

C)An unexpected increase in demand.

D)A developing problem in the manufacturing process.

E)Finding mostly favorable variances over time.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following is a method firms used to help track employee performance on a real-time basis?

A)Budget reconciliation report.

B)Process control charts.

C)Labor efficiency variance.

D)Spending variance.

E)None of the above.

A)Budget reconciliation report.

B)Process control charts.

C)Labor efficiency variance.

D)Spending variance.

E)None of the above.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

45

A company may experience a favorable labor rate variance but an unfavorable labor efficiency variance when:

A)Sales lagged behind the budgeted amounts of the sales department.

B)There were breakdowns in machinery.

C)The product mix changed during the period.

D)The company experienced a high amount of turnover in its workforce.

A)Sales lagged behind the budgeted amounts of the sales department.

B)There were breakdowns in machinery.

C)The product mix changed during the period.

D)The company experienced a high amount of turnover in its workforce.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

46

The Parsons Company has budgeted to capture 25% of the market in which they operate which currently contains 1,000 stores.The budgeted contribution margin per unit sold is $4.50.If they were actually able to capture only 20% of the market, but their actual contribution margin was $5.00 per unit, their market share variance was:

A)$250 favorable

B)$225 unfavorable

C)$250 unfavorable

D)$225 favorable

A)$250 favorable

B)$225 unfavorable

C)$250 unfavorable

D)$225 favorable

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following would lead to a variance resulting from a permanent change in a firm's operating environment?

A)An abnormally high incidence of employees calling in sick during a period.

B)A new competitor entering the market.

C)Upper-level management failing to consult lower level workers and instituting extremely tight budgetary controls.

D)A critical machine unexpectedly breaking down for a number of days.

A)An abnormally high incidence of employees calling in sick during a period.

B)A new competitor entering the market.

C)Upper-level management failing to consult lower level workers and instituting extremely tight budgetary controls.

D)A critical machine unexpectedly breaking down for a number of days.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

48

A spending variance results when there is a difference between actual and budgeted:

A)Fixed costs

B)Variable costs

C)Sales Revenue

D)Unit sales

A)Fixed costs

B)Variable costs

C)Sales Revenue

D)Unit sales

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following is not a general rule to follow in a variance investigation?

A)Adjust budgeted amounts to agree with actual amounts.

B)Investigate all significant variances, whether favorable or unfavorable.

C)Examine trends.

D)Consider the total picture.

E)All of the above are general rules to follow.

A)Adjust budgeted amounts to agree with actual amounts.

B)Investigate all significant variances, whether favorable or unfavorable.

C)Examine trends.

D)Consider the total picture.

E)All of the above are general rules to follow.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

50

A sales mix variance:

A)If unfavorable, indicates that a greater percentage of products with higher contribution margins are being sold than were budgeted.

B)Indicates which products are having a negative impact on profits.

C)Reports the effect on profits due to a change in the sales mix from the master budget.

D)Reports the effect on profits due to an overall change in sales quantity.

A)If unfavorable, indicates that a greater percentage of products with higher contribution margins are being sold than were budgeted.

B)Indicates which products are having a negative impact on profits.

C)Reports the effect on profits due to a change in the sales mix from the master budget.

D)Reports the effect on profits due to an overall change in sales quantity.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

51

Firms use non-financial measures to:

A)Identify problems with their processes.

B)Help align goals.

C)Provide on-going feedback to employees.

D)Evaluate employees.

E)All of the above.

A)Identify problems with their processes.

B)Help align goals.

C)Provide on-going feedback to employees.

D)Evaluate employees.

E)All of the above.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

52

Cico Buckets had budgeted unit sales of 41,600 buckets.Actual sales during May totaled 42,000 buckets at $4.25 per bucket.Its budgeted sales price was $4.00 per bucket.The master budget contribution margin totaled $62,400 and the budgeted variable cost per unit was $2.50.How much is Haslo's sales volume variance?

A)$600 F

B)$100 F

C)$1,600 F

D)$1,700 F

A)$600 F

B)$100 F

C)$1,600 F

D)$1,700 F

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

53

Thurston Company's budget allows for one pound of material to be used for each unit produced.The budget indicates that the material costs $2.50 per pound.Actual units produced totaled 8,000.The company used a total of 8,200 pounds of material at an actual cost of $2.40 per pound.There were no beginning or ending inventories of raw materials.The input price and input quantity variances, respectively, would be:

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

54

The primary limitations of variance analysis pertain to

A)Controllability and budgeting.

B)Timeliness and specificity.

C)Timeliness and controllability.

D)Controllability and specificity.

E)Budgeting and controllability.

A)Controllability and budgeting.

B)Timeliness and specificity.

C)Timeliness and controllability.

D)Controllability and specificity.

E)Budgeting and controllability.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 54 flashcards in this deck.