Deck 14: Firms in Competitive Markets

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

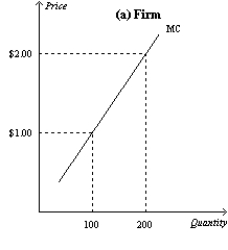

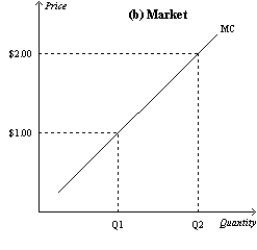

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $1.00?

A)300

B)6,000

C)30,000

D)60,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $1.00?

A)300

B)6,000

C)30,000

D)60,000

Question

Question

Question

Question

Question

Question

Question

Question

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 400 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)10,000

B)20,000

C)40,000

D)80,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 400 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)10,000

B)20,000

C)40,000

D)80,000

Question

Question

Question

Question

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)300

B)6,000

C)30,000

D)60,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)300

B)6,000

C)30,000

D)60,000

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/608

Play

Full screen (f)

Deck 14: Firms in Competitive Markets

1

Because there are many buyers and sellers in a perfectly competitive market, no one seller can influence the market price.

True

2

By comparing the marginal revenue and marginal cost from each unit produced, a firm in a competitive market can determine the profit-maximizing level of production.

True

3

When an individual firm in a competitive market decreases its production, it is likely that the market price will rise.

False

4

For a firm operating in a competitive market, both marginal revenue and average revenue exceed the market price.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

5

If a firm notices that its average revenue equals the current market price, that firm must be participating in a competitive market.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

6

Firms operating in perfectly competitive markets try to maximize profits.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

7

Firms in a competitive market are said to be price takers because there are many sellers in the market, and the goods offered by the firms are very similar if not identical.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

8

A profit-maximizing firm in a competitive market will decrease production when marginal cost exceeds average revenue.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

9

A firm is currently producing 100 units of output per day. The manager reports to the owner that producing the 100th unit costs the firm $5. The firm can sell the 100th unit for $4.75. The firm should continue to produce 100 units in order to maximize its profits (or minimize its losses).

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

10

For a firm operating in a perfectly competitive industry, marginal revenue and average revenue are equal.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

11

For a firm operating in a perfectly competitive industry, total revenue, marginal revenue, and average revenue are all equal.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

12

When an individual firm in a competitive market increases its production, it is likely that the market price will fall.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

13

Because there are many sellers in a competitive market, individual firms are unable to maximize profits.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

14

In a competitive market, firms are unable to differentiate their product from that of other producers.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

15

A firm's incentive to compare marginal revenue and marginal cost is an application of the principle that rational people think at the margin.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

16

In competitive markets, firms that raise their prices are typically rewarded with larger profits.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

17

The two characteristics of a competitive market are 1) many buyers and sellers in the market and 2) the goods offered by the various sellers are highly differentiated.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

18

A profit-maximizing firm in a competitive market will increase production when average revenue exceeds marginal cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

19

A firm is currently producing 100 units of output per day. The manager reports to the owner that producing the 100th unit costs the firm $5. The firm can sell the 100th unit for $5. The firm should continue to produce 100 units in order to maximize its profits (or minimize its losses).

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

20

Firms operating in perfectly competitive markets produce an output level where marginal revenue equals marginal cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

21

A firm is currently producing 100 units of output per day. The manager reports to the owner that producing the 100th unit costs the firm $5. The firm can sell the unit for $6. The firm should produce more than 100 units in order to maximize its profits (or minimize its losses).

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

22

A firm will shut down in the short run if revenue is not sufficient to cover its variable costs of production.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

23

A firm operating in a perfectly competitive industry will shut down in the short run but earn losses if the market price is less than that firm's average variable cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

24

The marginal firm in a competitive market will earn zero economic profit in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

25

Suppose a firm is considering producing zero units of output. We call this shutting down in the short run and exiting an industry in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

26

In the short run, if the market price is below the firm's average total cost of production, the firm will always shut down.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

27

When a profit-maximizing firm in a competitive market experiences rising prices, it will respond with an increase in production.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

28

A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if the market price is less than that firm's average total cost but greater than the firm's average variable cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

29

A miniature golf course is a good example of where fixed costs become relevant to the decision of when to open and when to close for the season.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

30

A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if the market price is less than that firm's average variable cost but greater than the firm's average fixed cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

31

In the short run, a firm should exit the industry if its marginal cost exceeds its marginal revenue.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

32

Suppose a firm is considering producing zero units of output. We call this exiting an industry in the short run and shutting down in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

33

A firm will shut down in the short run if revenue is not sufficient to cover all of its fixed costs of production.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

34

All firms maximize profits by producing an output level where marginal revenue equals marginal cost; for firms operating in perfectly competitive industries, maximizing profits also means producing an output level where price equals marginal cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

35

A popular resort restaurant will maximize profits if it chooses to stay open during the less-crowded "off season" when its total revenues exceed its fixed costs.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

36

A profit-maximizing firm in a competitive market will earn zero accounting profits in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

37

A popular resort restaurant will maximize profits if it chooses to stay open during the less-crowded "off season" when its total revenues exceed its variable costs.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

38

A firm operating in a competitive market will stay in business in the short run so long as the market price exceeds the firm's average total cost; otherwise, the firm will shut down.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

39

A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if the market price is less than that firm's average variable cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

40

The supply curve of a firm in a competitive market is the average variable cost curve above the minimum of marginal cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

41

A firm operating in a perfectly competitive market earns zero economic profit in the long run but remains in business because the firm's revenues cover the business owners' opportunity costs.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

42

In making a short-run profit-maximizing production decision, the firm must consider both fixed and variable cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

43

In the long run, when price is less than average total cost for all possible levels of production, a firm in a competitive market will choose to exit (or not enter) the market.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

44

In the long run, a competitive market with 1,000 identical firms will experience an equilibrium price equal to the minimum of each firm's average total cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

45

The stable, long-run equilibrium in a competitive market occurs when the market price equals the lowest point on a firm's average total cost curve.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

46

In the long run, when price is greater than average total cost, some firms in a competitive market will choose to enter the market.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

47

In the long run, a firm should exit the industry if its total costs exceed its total revenues.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

48

A firm operating in a perfectly competitive industry will continue to operate if it earns zero economic profits because it is likely to be earning positive accounting profits.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

49

A firm operating in a perfectly competitive market may earn positive, negative, or zero economic profit in the short run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

50

A dairy farmer must be able to calculate sunk costs in order to determine how much revenue the farm receives for the typical gallon of milk.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

51

In a long-run equilibrium where firms have identical costs, it is possible that some firms in a competitive market are making a positive economic profit.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

52

Because nothing can be done about sunk costs, they are irrelevant to decisions about business strategy.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

53

The long-run equilibrium in a competitive market characterized by firms with identical costs is generally characterized by firms operating at efficient scale.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

54

A competitive market will typically experience entry and exit until accounting profits are zero.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

55

A firm operating in a perfectly competitive industry will shut down in the short run if its economic profits fall to zero because it is likely to be earning negative accounting profits.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

56

The manager of a firm operating in a competitive market can ignore sunk costs when making business decisions.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

57

A firm operating in a perfectly competitive market may earn positive, negative, or zero economic profit in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

58

A competitive firm's profit will be increasing as long as marginal revenue is greater than marginal cost.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

59

When economic profits are zero in equilibrium, the firm's revenue must be sufficient to cover all opportunity costs.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

60

All competitive firms earn zero economic profit in both the short run and the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

61

If firms are competitive and profit maximizing, the price of a good equals the

A)marginal cost of production.

B)fixed cost of production.

C)total cost of production.

D)average total cost of production.

A)marginal cost of production.

B)fixed cost of production.

C)total cost of production.

D)average total cost of production.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

62

If a firm observes that the price of its product is above average variable cost, it would choose to continue to produce the good in the short run, even if that firm experiences economic losses.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

63

In competitive markets where firms are observed to be exiting the market, the firms that remain will obtain economic profits in the long run.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

64

A ski resort will choose to remain open in the summer whenever its fixed costs are low enough.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

65

Whenever firms in a perfectly competitive market produce the output level where marginal revenue equals marginal cost, we know that the firm is earning an economic profit.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

66

The production decisions of perfectly competitive firms follow one of the Ten Principles of Economics, which states that rational people

A)consider sunk costs.

B)equate prices to the average costs of production.

C)prefer to purchase products from smaller rather than larger firms.

D)think at the margin.

A)consider sunk costs.

B)equate prices to the average costs of production.

C)prefer to purchase products from smaller rather than larger firms.

D)think at the margin.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

67

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $1.00?

A)300

B)6,000

C)30,000

D)60,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $1.00?

A)300

B)6,000

C)30,000

D)60,000

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

68

In the long run, if we observe firms in a competitive market earning economic profits, we know that this market is in long-run equilibrium.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

69

Firms operating in a perfectly competitive market have an incentive to advertise their products since this will increase the demand for their products.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

70

Profit maximizing firms in competitive industries with free entry and exit face a price equal to the lowest possible

A)marginal cost of production.

B)fixed cost of production.

C)total cost of production.

D)average total cost of production.

A)marginal cost of production.

B)fixed cost of production.

C)total cost of production.

D)average total cost of production.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

71

All firms operating in a perfectly competitive market produce unique goods.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

72

A restaurant, which operates in a perfectly competitive market, is evaluating whether it should serve breakfast on a daily basis. It would choose to do this when its revenues cover its variable costs.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

73

The long-run supply curve in a competitive market is more elastic than the short-run supply curve.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

74

When a resource used in the production of a good sold in a competitive market is available in only limited quantities, the long-run supply curve is likely to be upward sloping.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

75

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 400 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)10,000

B)20,000

C)40,000

D)80,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 400 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)10,000

B)20,000

C)40,000

D)80,000

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

76

If some resources used in the production of a good are only available in limited quantities, then the long run market supply curve will be perfectly elastic.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

77

For firms operating in a perfectly competitive market, price must always be greater than marginal revenue.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

78

Firms in competitive markets can only earn economic profits in the long run, once the market is in equilibrium.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

79

Figure 14-9

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)300

B)6,000

C)30,000

D)60,000

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive market, and panel (b) depicts the linear market supply curve for a market with a fixed number of identical firms.

Refer to Figure 14-9. If there are 300 identical firms in this market, what level of output will be supplied to the market when price is $2.00?

A)300

B)6,000

C)30,000

D)60,000

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

80

The short-run supply curve in a competitive market must be more elastic than the long-run supply curve.

Unlock Deck

Unlock for access to all 608 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 608 flashcards in this deck.