Deck 17: Fraud Awareness Auditing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

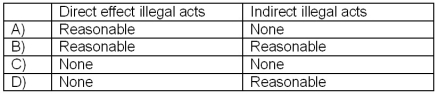

Jones CA is auditing the financial statements of XYZ Retailing, Inc.What assurance does

Jones provide XYZ that illegal acts that are material to financial statements will be detected?

A)A

B)B

C)C

D)D

Jones provide XYZ that illegal acts that are material to financial statements will be detected?

A)A

B)B

C)C

D)D

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/45

Play

Full screen (f)

Deck 17: Fraud Awareness Auditing

1

Over 90 percent of frauds are discovered by external or internal auditors.

False

2

Fraud examiners refer to people engaged specifically in the work of fraud investigation.

True

3

External auditors have the same responsibility for finding illegal acts as they do for finding material errors and irregularities.

False

4

CAS 240 (5135) requires auditors to ignore the traditional assumption of management's honesty.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

5

An economic motive for fraud is the need for money.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

6

Financial statement fraud is considered when someone knowingly makes material misrepresentations of fact with the intent of making someone believe the falsehood and suffer a loss as a result of acting upon that falsehood.Which of the following would be considered fraud?

A)Increasing the returns allowance as a result of unusually high sales near year end.

B)Transferring non-performing assets at historical values to a non-consolidated subsidiary.

C)Employee theft from petty cash.

D)Purchasing several months' supply of office supplies in order to qualify for a large volume discount.

A)Increasing the returns allowance as a result of unusually high sales near year end.

B)Transferring non-performing assets at historical values to a non-consolidated subsidiary.

C)Employee theft from petty cash.

D)Purchasing several months' supply of office supplies in order to qualify for a large volume discount.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

7

All errors and irregularities, including trivial ones, should be reported to the audit committee.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

8

Designing tight control systems is likely the best long term solution to preventing fraud.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

9

Unlike other auditors, fraud examiners think of materiality as a cumulative amount.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

10

Fraudulent financial reporting is an intentional act that results in materially misleading financial statements.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

11

Irregularities are unintentional misstatements or omissions in financial statements.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

12

The term "irregularities" generally refers to

A)Unintentional errors.

B)Illegal acts.

C)Intentional misstatements in financial statements.

D)Violations of GAAS.

A)Unintentional errors.

B)Illegal acts.

C)Intentional misstatements in financial statements.

D)Violations of GAAS.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is not a characteristic of fraud?

A)Intent to deceive.

B)Misrepresentation or intentional omission of significant information.

C)Taking unfair or dishonest advantage of others for personal gain.

D)Negligence on the part of executive management.

A)Intent to deceive.

B)Misrepresentation or intentional omission of significant information.

C)Taking unfair or dishonest advantage of others for personal gain.

D)Negligence on the part of executive management.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

14

Management fraud is an intentional act that injures investors or creditors.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

15

Most frauds are committed by people with low level responsibilities in an organization.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

16

When a financial auditor suspects financial reporting fraud, they should discuss their suspicions with the client to see if there is an alternative explanation.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

17

Misstating financial information in one period to prevent a loan being called for violating debt to equity covenants is okay as long as the violation is reversed in the next period.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

18

External auditors must design an audit to provide reasonable assurance of detecting material errors and irregularities.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

19

External auditors are required to report illegal acts to the appropriate governmental agency within 30 days of finding them.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

20

Lack of integrity is the most important factor affecting the risk of management fraud.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is normally considered an accounting estimate?

A)Credit sales.

B)Amortization of capital assets.

C)Repairs and maintenance expense.

D)Audit fees.

A)Credit sales.

B)Amortization of capital assets.

C)Repairs and maintenance expense.

D)Audit fees.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

22

An auditor who discovers that client employees have committed an illegal act with material consequences on the financial statements is most likely to seek legal advice and consider withdrawing from the engagement if

A)The illegal act is a violation of generally accepted accounting principles.

B)The client does not take appropriate action after being informed about the illegal act.

C)The illegal act was committed during a prior year that was not audited.

D)The auditor has already assessed control risk at the maximum level.

A)The illegal act is a violation of generally accepted accounting principles.

B)The client does not take appropriate action after being informed about the illegal act.

C)The illegal act was committed during a prior year that was not audited.

D)The auditor has already assessed control risk at the maximum level.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

23

A good reason for involving fraud auditors in the planning of a regular audit of financial statements is:

A)When there are many fraud risk factors.

B)When the audit committee authorizes further investigation.

C)It makes the client aware of how seriously the auditor takes its fraud detection responsibility.

D)It improves the documentation standards of the financial statement audit.

A)When there are many fraud risk factors.

B)When the audit committee authorizes further investigation.

C)It makes the client aware of how seriously the auditor takes its fraud detection responsibility.

D)It improves the documentation standards of the financial statement audit.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

24

What is the most important factor affecting the risk of management fraud?

A)Lack of integrity.

B)Lack of internal controls

C)Lack of board of director involvement in organization.

D)Lack of audited financial statements.

A)Lack of integrity.

B)Lack of internal controls

C)Lack of board of director involvement in organization.

D)Lack of audited financial statements.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

25

Horizontal analysis can be used in fraud detection by:

A)Checking the trend in earnings from year to year of persons suspected of fraud.

B)Looking for significant changes in financial statement amounts and ratios across several fiscal periods.

C)Looking for odd relations of one account to a base such as sales.

D)Looking for the change in net worth of a suspect from the beginning to the end of a period.

A)Checking the trend in earnings from year to year of persons suspected of fraud.

B)Looking for significant changes in financial statement amounts and ratios across several fiscal periods.

C)Looking for odd relations of one account to a base such as sales.

D)Looking for the change in net worth of a suspect from the beginning to the end of a period.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements about illegal acts committed by clients is correct?

A)An auditor has no responsibility to detect illegal acts that have an indirect effect on the financial statements.

B)An audit in accordance with generally accepted auditing standards normally includes audit procedures specifically designed to detect illegal acts that have an indirect but material effect on the financial statements.

C)An auditor considers illegal acts from the perspective of the reliability of management's representations rather than their relation to audit objectives derived from financial statement assertions.

D)An auditor's responsibility to detect illegal acts that have a direct and material effect on the financial statements is the same as that for errors and irregularities.

A)An auditor has no responsibility to detect illegal acts that have an indirect effect on the financial statements.

B)An audit in accordance with generally accepted auditing standards normally includes audit procedures specifically designed to detect illegal acts that have an indirect but material effect on the financial statements.

C)An auditor considers illegal acts from the perspective of the reliability of management's representations rather than their relation to audit objectives derived from financial statement assertions.

D)An auditor's responsibility to detect illegal acts that have a direct and material effect on the financial statements is the same as that for errors and irregularities.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

27

Certain conditions are often present when a manager prepares deliberately misstated financial statements.Which of the following is not such a condition?

A)Unfavourable industry conditions.

B)Lack of working capital.

C)Low debt.

D)Slow customer collections.

A)Unfavourable industry conditions.

B)Lack of working capital.

C)Low debt.

D)Slow customer collections.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

28

Statistics on fraud show that:

A)Senior executives commit the highest number of frauds and the senior executives cause the highest losses due to fraud.

B)Employees below the level of senior executives commit the highest number of frauds and cause the highest losses due to fraud.

C)Senior executives commit the highest number of frauds and employees below the level of the senior executives cause the highest losses due to fraud.

D)Employees below the level of senior executives commit the highest number of frauds but the senior executives commit the highest value frauds.

A)Senior executives commit the highest number of frauds and the senior executives cause the highest losses due to fraud.

B)Employees below the level of senior executives commit the highest number of frauds and cause the highest losses due to fraud.

C)Senior executives commit the highest number of frauds and employees below the level of the senior executives cause the highest losses due to fraud.

D)Employees below the level of senior executives commit the highest number of frauds but the senior executives commit the highest value frauds.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

29

In the audit of financial statements, which of the following procedures would the auditor call an "extended procedure"?

A)Measure the time lag between the date that cash receipts are recorded in the accounting records and the date that the deposit is credited to the bank account.

B)Observe the client's physical inventory count and take test counts of stock in the warehouse.

C)Send positive confirmations on accounts receivable balances.

D)Interview the staff in the accounting department and document the controls over the recording of sales transactions.

A)Measure the time lag between the date that cash receipts are recorded in the accounting records and the date that the deposit is credited to the bank account.

B)Observe the client's physical inventory count and take test counts of stock in the warehouse.

C)Send positive confirmations on accounts receivable balances.

D)Interview the staff in the accounting department and document the controls over the recording of sales transactions.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

30

Fraud is a difficult crime to stop entirely because:

A)People are basically untrustworthy.

B)Management needs freedom to conduct its businesses as it sees fit.

C)People see beating controls as a game.

D)The rewards greatly exceed the probable penalties.

A)People are basically untrustworthy.

B)Management needs freedom to conduct its businesses as it sees fit.

C)People see beating controls as a game.

D)The rewards greatly exceed the probable penalties.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

31

The first digit in a social insurance number

A)Has no meaning.

B)Is related to the date of birth of the recipient.

C)Indicates the province or region where the number was issued.

D)Is sequentially numbered based on when the card was issued.

A)Has no meaning.

B)Is related to the date of birth of the recipient.

C)Indicates the province or region where the number was issued.

D)Is sequentially numbered based on when the card was issued.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following auditors is least interested in materiality?

A)External auditors.

B)Internal auditors.

C)OAG auditors.

D)Fraud examiners.

A)External auditors.

B)Internal auditors.

C)OAG auditors.

D)Fraud examiners.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

33

External auditors are responsible

A)For authenticating documents.

B)To report immaterial irregularities to a level of management at least one level above the level where the irregularities occurred.

C)For finding intentional misstatements concealed by collusion.

D)For reporting all irregularities to outside agencies or parties.

A)For authenticating documents.

B)To report immaterial irregularities to a level of management at least one level above the level where the irregularities occurred.

C)For finding intentional misstatements concealed by collusion.

D)For reporting all irregularities to outside agencies or parties.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

34

The key to integrity in business is:

A)Good financial controls.

B)Good hiring procedures.

C)Accountability.

D)Training.

A)Good financial controls.

B)Good hiring procedures.

C)Accountability.

D)Training.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

35

According to U.S.standards, the external auditor's responsibility for discovering illegal acts involving a law and regulation that is far-removed from events that affect the financial statements does not include

A)Designing audit procedures to detect illegal acts in the absence of specific information brought to the auditors' attention.

B)Performing audit procedures when specific information indicates that possible illegal acts may have a material indirect effect on financial statements.

C)Considering the qualitative materiality of known and suspected illegal acts.

D)Obtaining written management representations concerning the absence of violation of laws and regulations.

A)Designing audit procedures to detect illegal acts in the absence of specific information brought to the auditors' attention.

B)Performing audit procedures when specific information indicates that possible illegal acts may have a material indirect effect on financial statements.

C)Considering the qualitative materiality of known and suspected illegal acts.

D)Obtaining written management representations concerning the absence of violation of laws and regulations.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

36

When an auditor becomes aware of a possible illegal act by a client, the auditor should obtain an understanding of the nature of the act in order to

A)Evaluate the effect on the financial statements.

B)Determine the reliability of management's representations.

C)Consider whether other similar acts may have occurred.

D)Recommend remedial actions to the audit committee.

A)Evaluate the effect on the financial statements.

B)Determine the reliability of management's representations.

C)Consider whether other similar acts may have occurred.

D)Recommend remedial actions to the audit committee.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is not considered one of the three factors that increase the probability of fraud?

A)Motive.

B)Lack of training.

C)Opportunity.

D)Lack of integrity.

A)Motive.

B)Lack of training.

C)Opportunity.

D)Lack of integrity.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

38

Forensic accounting can be defined as:

A)Investigating possible fraud.

B)Designing internal controls and other corporate governance mechanisms.

C)Calculating estimates used in financial reports.

D)Applying accounting and auditing skills in an action under civil law.

A)Investigating possible fraud.

B)Designing internal controls and other corporate governance mechanisms.

C)Calculating estimates used in financial reports.

D)Applying accounting and auditing skills in an action under civil law.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following statements best describes an auditor's responsibility to detect errors and other irregularities?

A)An auditor should design procedures to reduce the risk of not detecting a material misstatement to an appropriately low level.

B)An auditor is responsible to detect material errors, but has no responsibility to detect material irregularities that are concealed through employee collusion or management override of the internal control system.

C)An auditor has no responsibility to detect errors and irregularities unless analytical procedures or tests of transactions identify conditions that would cause a reasonably prudent auditor to suspect that the financial statements were materially misstated.

D)An auditor has no responsibility to detect errors and irregularities because an auditor is not an insurer and an audit does not constitute a guarantee.

A)An auditor should design procedures to reduce the risk of not detecting a material misstatement to an appropriately low level.

B)An auditor is responsible to detect material errors, but has no responsibility to detect material irregularities that are concealed through employee collusion or management override of the internal control system.

C)An auditor has no responsibility to detect errors and irregularities unless analytical procedures or tests of transactions identify conditions that would cause a reasonably prudent auditor to suspect that the financial statements were materially misstated.

D)An auditor has no responsibility to detect errors and irregularities because an auditor is not an insurer and an audit does not constitute a guarantee.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

40

Jones CA is auditing the financial statements of XYZ Retailing, Inc.What assurance does

Jones provide XYZ that illegal acts that are material to financial statements will be detected?

A)A

B)B

C)C

D)D

Jones provide XYZ that illegal acts that are material to financial statements will be detected?

A)A

B)B

C)C

D)D

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

41

What six controls reveal red flags?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

42

A PA's audit client is a small charity which funds development projects in a small foreign country.Most of its donations come in the form of cash, with tax receipts issued to the donors.Included in the cash receipts are weekly donations by one person, Mr.X, whose last

Name is easily identifiable as coming from that foreign country.Some of these cash donations exceed $10,000.The PA once asked about Mr.X and accepted as an answer that Mr.X was a wealthy entrepreneur but the PA has done no other work.

A)Assuming the PA has performed all other necessary and appropriate procedures, he may provide a clean opinion.

B)Assuming the PA does no further investigation of this matter, the PA may be considered willfully blind and complicit in an illegal act.

C)The PA may be associated with misleading information and should withdraw from the audit.

D)The PA should try to count the cash as it comes in in order to avoid issuing a scope limitation report.

Name is easily identifiable as coming from that foreign country.Some of these cash donations exceed $10,000.The PA once asked about Mr.X and accepted as an answer that Mr.X was a wealthy entrepreneur but the PA has done no other work.

A)Assuming the PA has performed all other necessary and appropriate procedures, he may provide a clean opinion.

B)Assuming the PA does no further investigation of this matter, the PA may be considered willfully blind and complicit in an illegal act.

C)The PA may be associated with misleading information and should withdraw from the audit.

D)The PA should try to count the cash as it comes in in order to avoid issuing a scope limitation report.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

43

Post CA accepted an engagement to audit the financial statements of General Ltd., a new client.General is a publicly held retailing company that recently replaced its operating managers.In the course of applying auditing procedures, Post suspected that the financial statements were materially misstated due to the existence of irregularities.

Required:

A) Describe Post's responsibilities in the circumstances described above.

B) Describe Post's responsibilities for reporting on General's financial statements and other communications if Post is precluded from applying additional procedures in searching for irregularities.

C) Describe Post's responsibilities for reporting on General's financial statements and other communications if Post concludes that General's financial statements are materially affected by irregularities.

Required:

A) Describe Post's responsibilities in the circumstances described above.

B) Describe Post's responsibilities for reporting on General's financial statements and other communications if Post is precluded from applying additional procedures in searching for irregularities.

C) Describe Post's responsibilities for reporting on General's financial statements and other communications if Post concludes that General's financial statements are materially affected by irregularities.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

44

Briefly describe the three factors that increase the probability of fraud.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

45

The most effective long run prevention of employee fraud is the practice of management caring for their employees.What can managers do to aid in fraud prevention?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 45 flashcards in this deck.