Deck 12: Intangibles

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which of the following sets describes the appropriate accounting for intangible assets with a finite life?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Question

Question

Question

Question

Question

Question

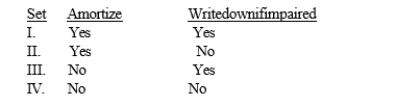

Which of the following sets represents a false relationship regarding the accounting for the cost of intangibles according to GAAP?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Question

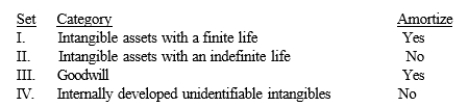

Which of the following relationships between category of intangibles and amortization is false?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Burger Prince incurred the following costs during 2017 in the development and production of a new product:

How much should be included in R&D expense for 2017?

A) $300,000

B) $630,000

C) $680,000

D) $700,000

How much should be included in R&D expense for 2017?

A) $300,000

B) $630,000

C) $680,000

D) $700,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/134

Play

Full screen (f)

Deck 12: Intangibles

1

Engineering follow-through in an early stage of commercial production can be included in R&D.

False

2

Purchased intangible assets are generally expensed at their acquisition costs because the future economic benefits associate with them are difficult to measure.

False

3

Technological feasibility of software products is established when the product is ready for general use.

False

4

Start-up costs are an intangible asset with an indefinite life and should be amortized over the expected life of the business.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

5

Trademarks are considered to have an indefinite life and are therefore not subject to amortization.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

6

Unidentifiable intangible assets are intangible assets that can be separated from the company and sold, transferred, licensed, rented, or exchanged.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

7

Purchased identifiable intangible assets are accounted for in a similar manner to that of tangible assets..

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

8

GAAP requires companies to disclose any costs of research and development acquired and written off as well as where the information can be found on the income statement.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

9

Legal work in connection with patent applications or litigation, and the sale or licensing of patents is excluded from

R & D.

R & D.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

10

GAAP requires that a company expense all of its research and development costs as they are incurred.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

11

A patent is granted by the federal government giving the owner control of the manufacture or other use of an invention for 20 years.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

12

Identifiable intangible assets are intangible assets that can be separated from the company and sold, transferred, licensed, rented, or exchanged.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

13

An intangible asset with an indefinite life is not amortized but is periodically reviewed for impairment.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

14

Software development costs are treated as R&D expense until technological feasibility of the product is established.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

15

The costs associated with internally developed goodwill are capitalized.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

16

An identifiable intangible asset that has a finite life is not amortized but is periodically reviewed for impairment.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

17

For intangible assets that are amortized, the total cost, accumulated amortization, amortization expense, and estimated amortization expense for the next 5 years needs to be disclosed.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

18

Development is the planned search for new knowledge with the hope that such knowledge will be useful in developing a new product or process.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

19

Identifiable intangible assets are accounted for in a similar manner to that of tangible assets.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

20

A copyright is granted by the federal government giving the owner exclusive rights to sell, publish, and control the artistic product for the life of the creator.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

21

The costs associated with purchased goodwill are capitalized and amortized over a period not to exceed 20 years.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following groups would be classified as intangible assets for financial accounting and reporting purposes?

A) long-term notes receivable, copyrights, goodwill, and trademarks

B) patents, software development costs, franchises, copyrights, and trademarks

C) computer software costs, development costs for internally developed patents, research, and goodwill

D) start-up costs, goodwill, costs of employee training programs, and trademarks

A) long-term notes receivable, copyrights, goodwill, and trademarks

B) patents, software development costs, franchises, copyrights, and trademarks

C) computer software costs, development costs for internally developed patents, research, and goodwill

D) start-up costs, goodwill, costs of employee training programs, and trademarks

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

23

_______occurs when the fair value of an asset is less than its carrying value.

A) Unidentification

B) Amortization

C) Goodwill

D) Impairment

A) Unidentification

B) Amortization

C) Goodwill

D) Impairment

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

24

U.S. GAAP allows a company to capitalize more of the costs of internally generated assets than allowed under

IFRS.

IFRS.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following is not required to be disclosed in an entity's financial statements or accompanying footnotes?

A) the total amount of research and development costs charged to expense during the current year

B) the method used to amortize the entity's intangible assets

C) a material amount of internally developed goodwill

D) accumulated amortization on the entity's intangibles as of its year-end

A) the total amount of research and development costs charged to expense during the current year

B) the method used to amortize the entity's intangible assets

C) a material amount of internally developed goodwill

D) accumulated amortization on the entity's intangibles as of its year-end

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

26

Identifiable intangible assets would include all of the following except

A) patents.

B) trademarks.

C) goodwill.

D) franchises.

A) patents.

B) trademarks.

C) goodwill.

D) franchises.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following sets describes the appropriate accounting for intangible assets with a finite life?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

28

All of the following characteristics are common to both tangible and intangible noncurrent assets with finite lives except

A) held for use and not for investment.

B) expensed in the periods in which the assets are used in operations.

C) have either a physical or financial nature.

D) derive value from the ability to generate economic benefits.

A) held for use and not for investment.

B) expensed in the periods in which the assets are used in operations.

C) have either a physical or financial nature.

D) derive value from the ability to generate economic benefits.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following characteristics is not common to both tangible and intangible assets?

A) held for use and not for investment

B) Have an expected life of more than one year

C) derive value from the ability to generate revenue

D) may have value only to a particular company

A) held for use and not for investment

B) Have an expected life of more than one year

C) derive value from the ability to generate revenue

D) may have value only to a particular company

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following methods is commonly used to amortize intangible assets over their useful lives?

A) declining balance

B) straight line

C) annual review for impairment

D) none of these since intangible assets are not amortized

A) declining balance

B) straight line

C) annual review for impairment

D) none of these since intangible assets are not amortized

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

31

________ cannot be separated from the entity and sold, transferred, licensed, rented, or exchanged.

A) Internally developed identifiable intangible asset

B) Tangible asset

C) Purchased identifiable intangible asset

D) Unidentifiable intangible asset

A) Internally developed identifiable intangible asset

B) Tangible asset

C) Purchased identifiable intangible asset

D) Unidentifiable intangible asset

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

32

Purchased goodwill is the difference between the acquisition price of an acquired company and the fair value of its identifiable net assets.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following sets represents a false relationship regarding the accounting for the cost of intangibles according to GAAP?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following relationships between category of intangibles and amortization is false?

A) Set I

B) Set II

C) Set III

D) Set IV

A) Set I

B) Set II

C) Set III

D) Set IV

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

35

Negative goodwill is recognized as the difference between the fair value of the net assets of an acquired company and the lower bargain purchase price.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following costs should always be expensed as incurred?

A) the costs of externally acquired identifiable intangible assets

B) the costs incurred directly associated with establishing and successfully defending the rights associated with internally developed identifiable intangible assets

C) the costs of internally developed unidentifiable intangible assets

D) the costs of externally acquired unidentifiable intangible assets

A) the costs of externally acquired identifiable intangible assets

B) the costs incurred directly associated with establishing and successfully defending the rights associated with internally developed identifiable intangible assets

C) the costs of internally developed unidentifiable intangible assets

D) the costs of externally acquired unidentifiable intangible assets

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

37

Which amortization method should be used for intangibles that are amortized?

A) a method based on the expected pattern of benefits to be produced by the asset

B) a method based on an annual review for impairment

C) the straight-line method; all others are inappropriate

D) any method is appropriate

A) a method based on the expected pattern of benefits to be produced by the asset

B) a method based on an annual review for impairment

C) the straight-line method; all others are inappropriate

D) any method is appropriate

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

38

Goodwill is tested for impairment only within the context of its reporting unit.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

39

Intangible assets are initially recorded at

A) cost.

B) expected future value.

C) present value.

D) fair value.

A) cost.

B) expected future value.

C) present value.

D) fair value.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

40

The cost of an internally developed unidentifiable intangible is expensed as incurred. Accordingly, which one of the following costs would be expensed in the year it was incurred?

A) legal cost of obtaining a patent

B) cost of improvements with a three-year life made to an asset that is being leased by the company for a five- year period

C) costs of developing new software products with proven technological feasibility

D) Costs of developing knowledge and skill levels for new management-level employees

A) legal cost of obtaining a patent

B) cost of improvements with a three-year life made to an asset that is being leased by the company for a five- year period

C) costs of developing new software products with proven technological feasibility

D) Costs of developing knowledge and skill levels for new management-level employees

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following research and development costs should always be capitalized?

A) costs of intangibles purchased from others

B) costs of materials, equipment, and intangibles with alternative future uses purchased from others

C) costs of equipment with an expected life greater than three years

D) costs of contract services purchased from others

A) costs of intangibles purchased from others

B) costs of materials, equipment, and intangibles with alternative future uses purchased from others

C) costs of equipment with an expected life greater than three years

D) costs of contract services purchased from others

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

42

Related to in-process R&D, an acquiring company may not

A) capitalize in-process R&D.

B) treat in-process R&D as an intangible asset.

C) increase the amount of goodwill for in-process R&D.

D) establish a patent for in-process R&D.

A) capitalize in-process R&D.

B) treat in-process R&D as an intangible asset.

C) increase the amount of goodwill for in-process R&D.

D) establish a patent for in-process R&D.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

43

Costs for which of the following activities would not be included as part of research and development R&D) costs?

A) testing in search for or evaluation of product or process alternatives.

B) adaptation of an existing capability to a particular requirement or customer's need as part of a continuing commercial activity.

C) searching for applications of new research findings or of other knowledge.

D) design, construction, and testing or preproduction prototypes and models.

A) testing in search for or evaluation of product or process alternatives.

B) adaptation of an existing capability to a particular requirement or customer's need as part of a continuing commercial activity.

C) searching for applications of new research findings or of other knowledge.

D) design, construction, and testing or preproduction prototypes and models.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

44

GAAP requires that research and development costs must be

A) capitalized.

B) expensed as incurred.

C) accumulated until the existence of future benefits is determined.

D) expensed in part and capitalized in part.

A) capitalized.

B) expensed as incurred.

C) accumulated until the existence of future benefits is determined.

D) expensed in part and capitalized in part.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

45

______are capitalized and amortized over their useful life.

A) Purchased identifiable intangible assets with finite life

B) Research and development costs

C) Purchased identifiable intangible assets with indefinite life

D) Unidentifiable intangible assets

A) Purchased identifiable intangible assets with finite life

B) Research and development costs

C) Purchased identifiable intangible assets with indefinite life

D) Unidentifiable intangible assets

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following expenditures cannot be included in R&D costs?

A) indirect costs

B) intangibles purchased from others

C) personnel costs

D) contract services performed for others

A) indirect costs

B) intangibles purchased from others

C) personnel costs

D) contract services performed for others

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

47

The Chambers Corporation was formed in early 2017. At the time of formation, Chamber spent the following amounts: accounting fees, $4,000; legal fees, $8,000; stock certificate costs, $3,000; initial franchise fee, $10,000; initial lease payment, $5,000; promotional fees, $3,000. Chamber intends to capitalize and amortize intangibles over the maximum allowable period in accordance with generally accepted accounting principles. Based on this strategy, what is Chambers's expense associated with organization costs in 2017?

A) $ 6,000

B) $18,000

C) $28,000

D) $33,000

A) $ 6,000

B) $18,000

C) $28,000

D) $33,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

48

_____are expensed as incurred.

A) Purchased identifiable intangible assets with finite life

B) Research and development costs

C) Purchased identifiable intangible assets with indefinite life

D) Unidentifiable intangible assets

A) Purchased identifiable intangible assets with finite life

B) Research and development costs

C) Purchased identifiable intangible assets with indefinite life

D) Unidentifiable intangible assets

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

49

If a research and development cost has alternative future uses, then the company

A) expenses the cost in the period incurred.

B) follows normal accrual procedures.

C) adds the cost to inventory.

D) adds the cost to property, plant, and equipment.

A) expenses the cost in the period incurred.

B) follows normal accrual procedures.

C) adds the cost to inventory.

D) adds the cost to property, plant, and equipment.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

50

At the date of purchase, materials, equipment, facilities, and intangibles purchased from others that have no alternative future uses in research and development or other activities should be

A) capitalized.

B) charged directly to retained earnings.

C) included in R&D expense immediately.

D) charged as a loss from continuing operations.

A) capitalized.

B) charged directly to retained earnings.

C) included in R&D expense immediately.

D) charged as a loss from continuing operations.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

51

Burger Prince incurred the following costs during 2017 in the development and production of a new product:

How much should be included in R&D expense for 2017?

A) $300,000

B) $630,000

C) $680,000

D) $700,000

How much should be included in R&D expense for 2017?

A) $300,000

B) $630,000

C) $680,000

D) $700,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

52

The Wagner Company made the following expenditures for research and development early in 2014: $80,000 for materials, $100,000 for contract services, $80,000 for employee salaries, and $800,000 for a building with an expected life of 20 years to be used for current and future research projects. Wagner uses straight-line depreciation. The company allocated $20,000 in overhead to research and development. What is Wagners' research and development expense for 2014?

A) $200,000

B) $220,000

C) $320,000

D) $960,000

A) $200,000

B) $220,000

C) $320,000

D) $960,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

53

The following items are excluded from research and development costs except

A) ongoing efforts to refine an existing product.

B) design of tools involving new technology.

C) introducing a new product.

D) quality control during commercial production.

A) ongoing efforts to refine an existing product.

B) design of tools involving new technology.

C) introducing a new product.

D) quality control during commercial production.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

54

Research and development costs are

A) capitalized and depreciated over the period which they benefit.

B) expensed as incurred.

C) added to the cost of the invented product.

D) added to the cost of the invented product if a reliable date of actual production is known.

A) capitalized and depreciated over the period which they benefit.

B) expensed as incurred.

C) added to the cost of the invented product.

D) added to the cost of the invented product if a reliable date of actual production is known.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

55

At the date of purchase, materials, equipment, facilities, and intangibles purchased from others that have alternative future uses in research and development should be

A) capitalized

B) charged directly to retained earnings

C) included in R&D expense immediately

D) charged as a loss from continuing operations

A) capitalized

B) charged directly to retained earnings

C) included in R&D expense immediately

D) charged as a loss from continuing operations

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

56

When a company that is performing R&D activities is acquired by another company, the acquiring company must allocate a portion of the purchase price to the R&D activities that are purchased, creating an intangible asset called

A) intangible development.

B) in-process research and development.

C) goodwill.

D) start-up costs.

A) intangible development.

B) in-process research and development.

C) goodwill.

D) start-up costs.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

57

Costs for which of the following activities should not be included in research and development R&D)?

A) modification of the formulation or design of a product or process

B) design of tools, jigs, molds, and dies involving new technology

C) design, construction, and testing of preproduction prototypes and models

D) trouble-shooting in connection with breakdowns during commercial production

A) modification of the formulation or design of a product or process

B) design of tools, jigs, molds, and dies involving new technology

C) design, construction, and testing of preproduction prototypes and models

D) trouble-shooting in connection with breakdowns during commercial production

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following accounting principles or conventions is contradictory to the GAAP requirement to expense R&D costs immediately?

A) historical cost principle

B) comparability

C) conservatism

D) matching principle

A) historical cost principle

B) comparability

C) conservatism

D) matching principle

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

59

The allocation of the cost of intangible assets in a systematic manner over the asset's useful life is called

A) depreciation.

B) systemization.

C) amortization.

D) impairment.

A) depreciation.

B) systemization.

C) amortization.

D) impairment.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

60

For financial reporting purposes, GAAP requires organization costs to be

A) expensed in the period in which they are incurred.

B) capitalized and amortized over 20 years.

C) capitalized and amortized over the first five years of the company's existence.

D) capitalized and treated as an intangible asset with an indefinite life.

A) expensed in the period in which they are incurred.

B) capitalized and amortized over 20 years.

C) capitalized and amortized over the first five years of the company's existence.

D) capitalized and treated as an intangible asset with an indefinite life.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following is not a required disclosure regarding goodwill for each period a company presents a balance sheet?

A) the amount of goodwill acquired

B) the amount of goodwill sold

C) the amount of any impairment loss recognized

D) the amount of any goodwill included in the disposal of a reporting unit

A) the amount of goodwill acquired

B) the amount of goodwill sold

C) the amount of any impairment loss recognized

D) the amount of any goodwill included in the disposal of a reporting unit

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

62

In January 2014, Western Co. purchased a patent for $750,000 that had an estimated remaining economic life of ten years. On January 2, 2017, the company incurred $140,000 in legal fees to successfully defend the validity of the patent. In January 2019, the company incurred $88,000 in legal fees in a new infringement lawsuit. In this situation, the lawsuit was lost, and the patent was determined to be worthless as a result. What is the expense to be recognized in 2019 by Western with regard to the patent?

A) $750,000

B) $150,000

C) $475,000

D) $563,000

A) $750,000

B) $150,000

C) $475,000

D) $563,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

63

During 2016, Debbie Company incurred $240,000 in legal fees in defending a patent with a carrying value of $4,500,000 against an infringement. Debbie's lawyers were not successful with the defense of the patent. The legal fees should be

A) expensed in 2016 and classified as ordinary expense.

B) classified as an extraordinary item on the income statement for 2016.

C) capitalized and amortized over the remaining legal life of the patent.

D) capitalized and amortized over the remaining economic life or legal life of the patent, whichever is shorter.

A) expensed in 2016 and classified as ordinary expense.

B) classified as an extraordinary item on the income statement for 2016.

C) capitalized and amortized over the remaining legal life of the patent.

D) capitalized and amortized over the remaining economic life or legal life of the patent, whichever is shorter.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

64

All of the following items are expensed as start-up costs except

A) promotional costs for opening a new facility.

B) one-time costs for conducting business in a new territory.

C) licensing fees for starting a new franchise.

D) accounting fees for forming a new company.

A) promotional costs for opening a new facility.

B) one-time costs for conducting business in a new territory.

C) licensing fees for starting a new franchise.

D) accounting fees for forming a new company.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

65

R Company registered a patent on January 1, 2015. P Company purchased the patent from R Company for $450,000 on January 1, 2020, and began to amortize the patent over its remaining legal life. In early 2021, P Company determined that the patent's economic benefits would last only until the end of 2025. What amount should P Company record for patent amortization in 2021?

A) $90,000

B) $84,000

C) $70,000

D) $30,000

A) $90,000

B) $84,000

C) $70,000

D) $30,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

66

All of the following items are included in research and development costs except

A) legal work in connection with patent application.

B) design of prototype models.

C) evaluation of a potential new product.

D) research aimed at discovery of new knowledge.

A) legal work in connection with patent application.

B) design of prototype models.

C) evaluation of a potential new product.

D) research aimed at discovery of new knowledge.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

67

Trademarks or trade names

A) must be renewed every 35 years.

B) can be considered intangibles with indefinite lives.

C) are developed internally and thus should not have any related costs capitalized and amortized.

D) are synonymous with internally developed goodwill.

A) must be renewed every 35 years.

B) can be considered intangibles with indefinite lives.

C) are developed internally and thus should not have any related costs capitalized and amortized.

D) are synonymous with internally developed goodwill.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following statements regarding intangible assets is true?

A) The expected useful life of an intangible asset is generally easier to estimate than the expected useful life of a tangible noncurrent asset.

B) The cost of an intangible asset is not permitted to be amortized for income tax purposes.

C) Intangible assets have a lower degree of uncertainty with regard to their expected future benefits than tangible noncurrent assets.

D) The accumulated amortization for intangible assets that are amortized must be disclosed.

A) The expected useful life of an intangible asset is generally easier to estimate than the expected useful life of a tangible noncurrent asset.

B) The cost of an intangible asset is not permitted to be amortized for income tax purposes.

C) Intangible assets have a lower degree of uncertainty with regard to their expected future benefits than tangible noncurrent assets.

D) The accumulated amortization for intangible assets that are amortized must be disclosed.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

69

In January 2014, the Jennifer Corporation purchased a patent for $231,000 from Travis Company that had a remaining legal life of 14 years. Jennifer estimated that the remaining economic life would be seven years. In January 2018, the company incurred $30,000 in legal costs to defend the patent from an infringement. Jennifer's lawyers were successful, and the remaining years of benefit from the patent were estimated to be six years. What is the patent amortization expense for 2018?

A) $7,615

B) $9,923

C) $16,500

D) $21,500

A) $7,615

B) $9,923

C) $16,500

D) $21,500

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following is not a required disclosure regarding intangible assets in the period a company acquires intangible assets?

A) the cost of any intangible assets acquired, separated into assets subject to amortization, assets not subject to amortization, and goodwill

B) for assets subject to amortization, the residual value and the weighted-average amortization period

C) the rate of return used to estimate the value of goodwill purchased

D) the cost of any research and development acquired and written off, and where it is included in the income statement

A) the cost of any intangible assets acquired, separated into assets subject to amortization, assets not subject to amortization, and goodwill

B) for assets subject to amortization, the residual value and the weighted-average amortization period

C) the rate of return used to estimate the value of goodwill purchased

D) the cost of any research and development acquired and written off, and where it is included in the income statement

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

71

In 1975, Riveria Company had acquired copyrights for $750,000 on several literary works from some obscure 18th century authors. These copyrights were fully amortized by 2015. In early 2015, a new anthropological discovery made these copyrights worth $2,500,000. As a result, Riveria should report which of the following in its financial statements for 2015?

A) $2,500,000 as a holding gain

B) $750,000 as copyrights-based recovery of value limited to historical cost

C) $2,500,000 as an extraordinary item

D) cannot be recognized under U.S. GAAP in the financial statements

A) $2,500,000 as a holding gain

B) $750,000 as copyrights-based recovery of value limited to historical cost

C) $2,500,000 as an extraordinary item

D) cannot be recognized under U.S. GAAP in the financial statements

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

72

The amortization period for a patent is

A) indefinite; patents should be reviewed for impairment annually.

B) 20 years.

C) 20 years or the expected useful life of the patent, whichever is longer.

D) 20 years or the expected useful life of the patent, whichever is shorter.

A) indefinite; patents should be reviewed for impairment annually.

B) 20 years.

C) 20 years or the expected useful life of the patent, whichever is longer.

D) 20 years or the expected useful life of the patent, whichever is shorter.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

73

_____are contractual agreements which grant the right to perform certain functions or sell certain products or services.

A) Noncompete agreements

B) Franchises

C) Trademarks

D) Customer acquisition lists

A) Noncompete agreements

B) Franchises

C) Trademarks

D) Customer acquisition lists

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following is an intangible asset that is not typically amortized?

A) patent

B) copyright

C) franchise

D) goodwill

A) patent

B) copyright

C) franchise

D) goodwill

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

75

All of the following are considered marketing-related intangible assets except

A) copyright.

B) internet domain name.

C) noncompete agreement.

D) trademark.

A) copyright.

B) internet domain name.

C) noncompete agreement.

D) trademark.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

76

During 2016, Frank Company incurred $200,000 in legal fees in defending a patent with a carrying value of $3,500,000 against an infringement. Farver's lawyers were successful with the defense of the patent. The legal fees should be

A) expensed in 2016 and classified as ordinary expense.

B) classified as an extraordinary item on the income statement for 2016.

C) capitalized and amortized over the remaining legal life of the patent.

D) capitalized and amortized over the remaining economic life or legal life of the patent, whichever is shorter.

A) expensed in 2016 and classified as ordinary expense.

B) classified as an extraordinary item on the income statement for 2016.

C) capitalized and amortized over the remaining legal life of the patent.

D) capitalized and amortized over the remaining economic life or legal life of the patent, whichever is shorter.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

77

The cost of a copyright should

A) be amortized over a period not to exceed the life of the author plus 50 years.

B) be amortized over a period not to exceed 20 years, unless the right is renewed.

C) not be amortized and the cost should be capitalized as an asset with indefinite life.

D) be amortized over a period not to exceed its economic life.

A) be amortized over a period not to exceed the life of the author plus 50 years.

B) be amortized over a period not to exceed 20 years, unless the right is renewed.

C) not be amortized and the cost should be capitalized as an asset with indefinite life.

D) be amortized over a period not to exceed its economic life.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

78

Debbie acquired a franchise to operate a donut shop from Dollar Donuts, Inc., for $100,000. She incurred an additional $4,000 in legal costs to negotiate the terms with the franchiser. In five years, the franchise contract will be renegotiated. The current contract also states that there will be a $3,000 annual fee plus a two percent charge based on the store's annual revenue, which is expected to average 90,000 per year. What is the franchise cost that should be capitalized?

A) $88,000

B) $92,000

C) $100,000

D) $104,000

A) $88,000

B) $92,000

C) $100,000

D) $104,000

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

79

A patent is amortized over its expected useful life or 20 years. The expected useful life can be impacted by all of the following except

A) a unsuccessful lawsuit against a competitor.

B) the federal government renewing the original patent.

C) technical innovations by a competitor.

D) product improvements by the patent holder.

A) a unsuccessful lawsuit against a competitor.

B) the federal government renewing the original patent.

C) technical innovations by a competitor.

D) product improvements by the patent holder.

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following is not a required disclosure regarding intangible assets that are amortized for each period a company presents a balance sheet?

A) the total cost

B) the accumulated amortization

C) the amortization expense

D) the estimated amortization expense for the next ten years

A) the total cost

B) the accumulated amortization

C) the amortization expense

D) the estimated amortization expense for the next ten years

Unlock Deck

Unlock for access to all 134 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 134 flashcards in this deck.