Deck 1: The Government and Not-For-Profit Environment

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

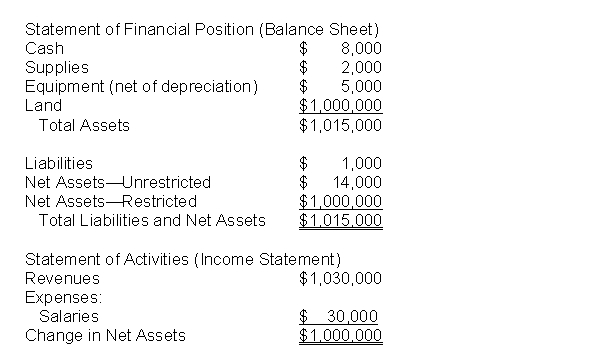

Save-the-Birds (STB), a not-for-profit entity dedicated to acquiring and preserving habitat for upland birds, prepares financial statements in accordance with generally accepted accounting principles. Currently, standards require that a not-for-profit entity report virtually all contributions as revenue in the year received. During the current year STB received a donation of several hundred acres of prime habitat for upland birds. STB will require several hundred thousand dollars in additional donations in order to make the land completely suitable for the birds. Before embarking on its fund-raising campaign STB prepares financial statements which are summarized as follows.  What difficulties, if any, will STB encounter in its new fund-raising drive? Knowing that the donation of the land accounted for $1,000,000 of the revenue reported by STB, do you think the financial statements present fairly the financial position and results of operations of this not-for-profit entity?

What difficulties, if any, will STB encounter in its new fund-raising drive? Knowing that the donation of the land accounted for $1,000,000 of the revenue reported by STB, do you think the financial statements present fairly the financial position and results of operations of this not-for-profit entity?

What difficulties, if any, will STB encounter in its new fund-raising drive? Knowing that the donation of the land accounted for $1,000,000 of the revenue reported by STB, do you think the financial statements present fairly the financial position and results of operations of this not-for-profit entity? Question

Question

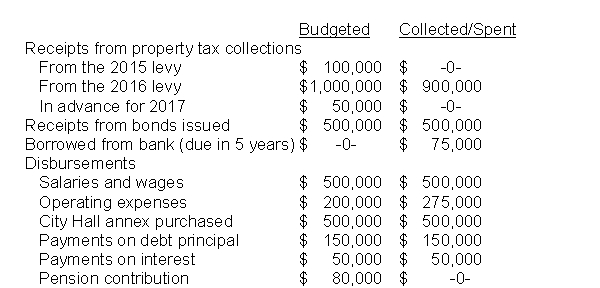

Thorn County adopted a cash budget for FY2016 as follows. The City budget laws prohibit budgeting or operating at a deficit. During the year the County collected or spent the following amounts. Was the County in compliance with budget laws? Did the County accomplish the goal of interperiod equity? Explain your answers in detail.  Explanations provided by the City for the differences between budget and actual are as follows. Property tax collections are down because the major industry in the community closed and many citizens are currently unemployed. Operating expenses are up because the only bridge over a river bisecting the City sustained damages by an uninsured motorist and had to be repaired immediately. The repair was not budgeted.

Explanations provided by the City for the differences between budget and actual are as follows. Property tax collections are down because the major industry in the community closed and many citizens are currently unemployed. Operating expenses are up because the only bridge over a river bisecting the City sustained damages by an uninsured motorist and had to be repaired immediately. The repair was not budgeted.

Explanations provided by the City for the differences between budget and actual are as follows. Property tax collections are down because the major industry in the community closed and many citizens are currently unemployed. Operating expenses are up because the only bridge over a river bisecting the City sustained damages by an uninsured motorist and had to be repaired immediately. The repair was not budgeted. Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 1: The Government and Not-For-Profit Environment

1

Sarbanes-Oxley was passed in 2002 to enhance the independence of the GASB.

True

2

Which of the following statements is true? a. Governments may engage in activities like activities engaged in by for-profit entities.

B) There are a small number of different types of governments.

C) All governments engage in the same activities.

D) Managers may have a long-term focus and thereby sacrifice the short-term liquidity of the entity.

B) There are a small number of different types of governments.

C) All governments engage in the same activities.

D) Managers may have a long-term focus and thereby sacrifice the short-term liquidity of the entity.

A

3

The Federal Accounting Standards Advisory Board's standards do not apply to the federal Department of the Treasury.

False

4

Governments have no need for an accounting system.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following activities is NOT an activity in which a government might engage? a. Selling electric power.

B) Operating a golf course.

C) Operating a bookstore.

D) All of the above are activities that might be carried out by a government.

B) Operating a golf course.

C) Operating a bookstore.

D) All of the above are activities that might be carried out by a government.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

A primary characteristic that distinguishes governments from businesses is a. The need to generate revenues equal to or more than expenditures/expenses.

B) The importance of the budget in the governing process.

C) The need to provide goods or services.

D) The correlation between revenues generated and demand for goods or services.

B) The importance of the budget in the governing process.

C) The need to provide goods or services.

D) The correlation between revenues generated and demand for goods or services.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

To obtain a comprehensive understanding of a government's fiscal health, a financial analyst should obtain an understanding of which of the following? a. All the resources owned by the government.

B) All the resources that may be summoned by the government.

C) Demographic data about the residents served by the government.

D) All of the above.

B) All the resources that may be summoned by the government.

C) Demographic data about the residents served by the government.

D) All of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

A government's constituants rely on general purpose financial statements for a considerable amount of information about their government.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Lenders use the financial statements of governments and not-for-profit entities just as they would those of businesses, that is, to help assess the borrower's credit-worthiness.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Governments and not-for-profit entities may never engage in business-type activities.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following characteristics distinguishes a government or not-for-profit entity from a business? a. There is always a direct link between revenues generated and expenditures/expenses incurred.

B) Capital assets are used to produce revenues and save costs.

C) Revenues are always indicative of demand for goods and services.

D) The mission of the entity may include goals other than maximizing profit.

B) Capital assets are used to produce revenues and save costs.

C) Revenues are always indicative of demand for goods and services.

D) The mission of the entity may include goals other than maximizing profit.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

The objective of a typical government or not-for-profit entity includes goals that are difficult to quantify

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

In which of the following activities is a not-for-profit entity least likely to engage? a. Providing educational services.

B) Providing health-care services.

C) Providing for terrorism defense.

D) Retail sales of cookies

B) Providing health-care services.

C) Providing for terrorism defense.

D) Retail sales of cookies

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following can be affected by GAAP? a. Legal ability to issue bonds.

B) Ability to balance the budget.

C) Amount reported as employee pension plan contributions.

D) Claims and judgments settled.

B) Ability to balance the budget.

C) Amount reported as employee pension plan contributions.

D) Claims and judgments settled.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

The most significant financial document provided by a government is the a. Balance sheet.

B) Operating statement.

C) Operating budget.

D) Cash flow statement.

B) Operating statement.

C) Operating budget.

D) Cash flow statement.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following characteristics is unique to governments? a. The ability to have activities financed with tax-exempt debt.

B) The power to impose fees.

C) The ability to issue tax-exempt debt.

D) The ability to have activities financed by Federal grants.

B) The power to impose fees.

C) The ability to issue tax-exempt debt.

D) The ability to have activities financed by Federal grants.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

A primary characteristic that distinguishes government from not-for-profits is a. The need to generate revenues equal to or more than expenditures/expenses.

B) The ability to levy taxes.

C) The need to provide goods or services.

D) The correlation between revenues generated and demand for goods or services.

B) The ability to levy taxes.

C) The need to provide goods or services.

D) The correlation between revenues generated and demand for goods or services.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Financial statements, no matter how prepared, do not directly affect the economic worth of an entity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

The Governmental Accounting Standards Board establishes generally accepted accounting principles for all state and local governments and all not-for-profit entities.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

A government's budget may be backed by the force of law.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following are objectives of financial reporting by state and local governments as established by the GASB? i. Accountability

Ii) Evaluation of legislative results

Iii) Level of service and ability to meet obligations

A) I only

B) II only

C) I and III

D) I, II and III

Ii) Evaluation of legislative results

Iii) Level of service and ability to meet obligations

A) I only

B) II only

C) I and III

D) I, II and III

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

As used by the GASB, interperiod equity refers to which of the following? a. Demonstrate compliance with finance-related contractual requirements.

B) Provide information to determine whether the constituents pay for what they receive.

C) Demonstrate whether resources were obtained and used in accordance with the government's legally adopted budget.

D) Provide information to assist users in assessing the government's economy, efficiency, and effectiveness.

B) Provide information to determine whether the constituents pay for what they receive.

C) Demonstrate whether resources were obtained and used in accordance with the government's legally adopted budget.

D) Provide information to assist users in assessing the government's economy, efficiency, and effectiveness.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

The primary standard-setting body for accounting and financial reporting by a state-supported college or university is: a. GASB.

B) FASB.

C) AICPA.

D) All of the above.

B) FASB.

C) AICPA.

D) All of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

The Governmental Accounting Standards Board is the primary standard-setting body for: a. All governments.

B) All state and local governments.

C) All governments and all not-for-profit entities.

D) All state and local governments and all not-for-profit entities.

B) All state and local governments.

C) All governments and all not-for-profit entities.

D) All state and local governments and all not-for-profit entities.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

Under certain circumstances a government might use standards established by which of the following standard-setting bodies? a. GASB.

B) FASB.

C) AICPA.

D) All of the above.

B) FASB.

C) AICPA.

D) All of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

Given a specific set of data, the basis of accounting selected by or imposed on a government will impact which of the following the LEAST? a. Determining whether the government has a balanced budget.

B) Determining whether the government has the ability to issue debt.

C) Determining whether certain economic events occurred.

D) Determining the annual payments to a government-sponsored pension plan.

B) Determining whether the government has the ability to issue debt.

C) Determining whether certain economic events occurred.

D) Determining the annual payments to a government-sponsored pension plan.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

A regulatory agency would use the external financial statements of a local government for which of the following purposes? a. To ensure that the entity is spending and receiving resources in accordance with laws, regulations or policies.

B) To determine how resources should be allocated.

C) To exercise general oversight responsibility.

D) To do all of the above.

B) To determine how resources should be allocated.

C) To exercise general oversight responsibility.

D) To do all of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is NOT a purpose of external financial reporting by governments? a. Assess financial condition.

B) Compare actual results with the budget.

C) Assess the ability of elected officials to effectively manage people.

D) Evaluate efficiency and effectiveness.

B) Compare actual results with the budget.

C) Assess the ability of elected officials to effectively manage people.

D) Evaluate efficiency and effectiveness.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

The basis of accounting selected by or imposed on a government can influence which of the following? a. A decision to contract-out a specific service rather than provide that service itself.

B) The amount of annual contribution to keep pension fully funded.

C) The amount that is available to spend on a donor-specified project or service.

D) All of the above.

B) The amount of annual contribution to keep pension fully funded.

C) The amount that is available to spend on a donor-specified project or service.

D) All of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

Users of government financial statements should be interested in information about compliance with laws and regulations for which of the following reasons? a. To determine if the government has complied with bond covenants.

B) To determine if the government has complied with taxing limitations.

C) To determine if the government has complied with donor restrictions on the use of funds.

D) To determine all of the above.

B) To determine if the government has complied with taxing limitations.

C) To determine if the government has complied with donor restrictions on the use of funds.

D) To determine all of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

A primary tool of both governments and not-for-profit to acquire funds to finance long-term projects is a. Levy of special purpose tax.

B) Have a city-wide gala.

C) Obtain line of credit on current assets.

D) Issue bonds to individuals and institutional investors.

B) Have a city-wide gala.

C) Obtain line of credit on current assets.

D) Issue bonds to individuals and institutional investors.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is a probable use an individual donor would make of the external financial statements of a not-for-profit entity? a. To determine the proportion of entity resources directed to programs as opposed to fund-raising.

B) To determine the creditworthiness of the entity for investment purposes.

C) To determine the salaries paid to all employees of the entity.

D) To determine the budget of the entity.

B) To determine the creditworthiness of the entity for investment purposes.

C) To determine the salaries paid to all employees of the entity.

D) To determine the budget of the entity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is an objective of financial reporting by nongovernmental not-for-profit entities as established by the FASB? a. Assessing the types of services provided and the need for those services.

B) Assessing the services provided and the entity's ability to earn a profit.

C) Making rational decisions about the allocation of resources to those organizations.

D) Assessing how managers have managed personnel.

B) Assessing the services provided and the entity's ability to earn a profit.

C) Making rational decisions about the allocation of resources to those organizations.

D) Assessing how managers have managed personnel.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is NOT a typical external user of a government or not-for-profit financial statements? a. Governing boards

B) Securities and Exchange Commission

C) Donors and grantors

D) Taxpayers/citizens or organization members

B) Securities and Exchange Commission

C) Donors and grantors

D) Taxpayers/citizens or organization members

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is common to both governments and not-for-profit entities but distinguishes these entities from for-profit entities? a. The budget is a legal, financial document.

B) Revenues are usually indicative of demand for goods or services.

C) There is direct matching of revenues and expenses.

D) There are no defined ownership interests.

B) Revenues are usually indicative of demand for goods or services.

C) There is direct matching of revenues and expenses.

D) There are no defined ownership interests.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following entities was a principal in creating the FASAB? a. U.S. Congress.

B) Office of Management and Budget.

C) Governmental Accounting Standards Board.

D) Securities and Exchange Commission.

B) Office of Management and Budget.

C) Governmental Accounting Standards Board.

D) Securities and Exchange Commission.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following objectives is considered the cornerstone of financial reporting by a state or local government? a. Accountability.

B) Budgetary compliance.

C) Interperiod equity.

D) Service efforts and accomplishments.

B) Budgetary compliance.

C) Interperiod equity.

D) Service efforts and accomplishments.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

The purpose of the FASAB is to establish accounting standards for a. Not-for-profit entities.

B) Federal government.

C) All governments.

D) Non-federal governments.

ANSWERS TO MULTIPLE CHOICE (CHAPTER 1)

B) Federal government.

C) All governments.

D) Non-federal governments.

ANSWERS TO MULTIPLE CHOICE (CHAPTER 1)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is NOT generally considered a main user of government and not-for-profit entity external financial statements? a. Investors and creditors.

B) Taxpayers.

C) Donors.

D) Internal managers.

B) Taxpayers.

C) Donors.

D) Internal managers.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

In descending order, the hierarchy of GAAP applicable to a church-owned college may be: a. FASB Statements and Interpretations, AICPA Accounting Research Bulletins, Accounting Principles Board Opinion, FASB Technical Bulletins, AICPA Industry Audit Guides, FASB Implementation Guides, other accounting literature-including GASB standards.

B) FASB Statements and Interpretations, GASB standards, AICPA Practice Bulletins (if cleared by FASB).

C) GASB Statements and Interpretations, AICPA Industry Audit Guides, GASB Implementation Guides, other accounting literature-including FASB standards.

D) GASB Statements and Interpretations, GASB Technical Bulletins, AICPA Industry Audit Guides, AICPA Practice Bulletins (if cleared by GASB), GASB Implementation Guides, other accounting literature-including FASB standards.

B) FASB Statements and Interpretations, GASB standards, AICPA Practice Bulletins (if cleared by FASB).

C) GASB Statements and Interpretations, AICPA Industry Audit Guides, GASB Implementation Guides, other accounting literature-including FASB standards.

D) GASB Statements and Interpretations, GASB Technical Bulletins, AICPA Industry Audit Guides, AICPA Practice Bulletins (if cleared by GASB), GASB Implementation Guides, other accounting literature-including FASB standards.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

In the United States, educational services can be provided by federal government entities, by non-federal government entities, by not-for-profit entities, and by for-profit entities. Are the accounting and financial reporting standards the same for each of these entities? Should they be the same?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

What are some of the definitional criteria that distinguish a state or local government from a not-for-profit entity?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Save-the-Birds (STB), a not-for-profit entity dedicated to acquiring and preserving habitat for upland birds, prepares financial statements in accordance with generally accepted accounting principles. Currently, standards require that a not-for-profit entity report virtually all contributions as revenue in the year received. During the current year STB received a donation of several hundred acres of prime habitat for upland birds. STB will require several hundred thousand dollars in additional donations in order to make the land completely suitable for the birds. Before embarking on its fund-raising campaign STB prepares financial statements which are summarized as follows. What difficulties, if any, will STB encounter in its new fund-raising drive? Knowing that the donation of the land accounted for $1,000,000 of the revenue reported by STB, do you think the financial statements present fairly the financial position and results of operations of this not-for-profit entity?

What difficulties, if any, will STB encounter in its new fund-raising drive? Knowing that the donation of the land accounted for $1,000,000 of the revenue reported by STB, do you think the financial statements present fairly the financial position and results of operations of this not-for-profit entity? Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

Johnson City prepares its budget on the cash basis and prepares its external financial statements on the accrual basis. From the following data prepare statements of activity (income statements) on both the cash basis and the accrual basis. Which statement best represents the results of operations of the City? Which statement best demonstrates compliance with laws and regulations? Which statement would you rather see? Which conveys the best information to the citizens of Johnson City?

The City levies taxes in the current year of $1 million. Of this amount $.9 million is collected during the current year, $.05 will be collected next year, and $.04 will be collected in the future. $.01 will never be collected. During the current year the City pays bills from prior periods $.06 million, bills of the current period $.8 million, and defers payment until future periods on bills that were received for services consumed during the current period $.1 million.

The City levies taxes in the current year of $1 million. Of this amount $.9 million is collected during the current year, $.05 will be collected next year, and $.04 will be collected in the future. $.01 will never be collected. During the current year the City pays bills from prior periods $.06 million, bills of the current period $.8 million, and defers payment until future periods on bills that were received for services consumed during the current period $.1 million.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Thorn County adopted a cash budget for FY2016 as follows. The City budget laws prohibit budgeting or operating at a deficit. During the year the County collected or spent the following amounts. Was the County in compliance with budget laws? Did the County accomplish the goal of interperiod equity? Explain your answers in detail. Explanations provided by the City for the differences between budget and actual are as follows. Property tax collections are down because the major industry in the community closed and many citizens are currently unemployed. Operating expenses are up because the only bridge over a river bisecting the City sustained damages by an uninsured motorist and had to be repaired immediately. The repair was not budgeted.

Explanations provided by the City for the differences between budget and actual are as follows. Property tax collections are down because the major industry in the community closed and many citizens are currently unemployed. Operating expenses are up because the only bridge over a river bisecting the City sustained damages by an uninsured motorist and had to be repaired immediately. The repair was not budgeted. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

What is the significance-for financial reporting purposes-of the fact that neither not-for-profits nor governments have owners (stockholders)?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Certain fiscal practices of governments promote interperiod equity while others do not. For the situations listed below, indicate whether interperiod equity is promoted or undermined. Why?

a. Issuing 30-year serial bonds to finance the construction of capital assets with estimated 30-year lives.

b. Paying for the pensions of retired employees out of resources provided by current-period taxpayers.

c. Charging the cost of supplies as expenditures in the year in which they were used rather than when they were purchased.

d. Issuing 30-year bonds to finance a portion of the current-period operating costs of a city's school system

e. Charging payments of wages and salaries made in the first week of a new year to the previous fiscal year, the year in which the wages and salaries were earned.

a. Issuing 30-year serial bonds to finance the construction of capital assets with estimated 30-year lives.

b. Paying for the pensions of retired employees out of resources provided by current-period taxpayers.

c. Charging the cost of supplies as expenditures in the year in which they were used rather than when they were purchased.

d. Issuing 30-year bonds to finance a portion of the current-period operating costs of a city's school system

e. Charging payments of wages and salaries made in the first week of a new year to the previous fiscal year, the year in which the wages and salaries were earned.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

The Governmental Accounting Standards Board (GASB) stated that an objective of financial reporting is to measure interperiod equity, that is-"Financial reporting should provide information to determine whether current-year revenues were sufficient to pay for current-year services." What is your understanding of interperiod equity? What costs incurred in the current year should be paid for by the taxpayers of the current period? What costs incurred in the current year should be paid for by future taxpayers?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

How does the FASB influence generally accepted accounting principles for state and local governments?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

A not-for-profit entity raises funds to support specific programs, services, and activities. The recipients of the programs, services, and activities are frequently not the providers of the resources needed to deliver the programs, services, and activities. What information would donors to these not-for-profit entities be interested in seeing? What information would program beneficiaries be interested in seeing? Identify other users of the financial statements of a not-for-profit and the types of information in which they would be interested.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.