Deck 12: Not-For-Profit Organizations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

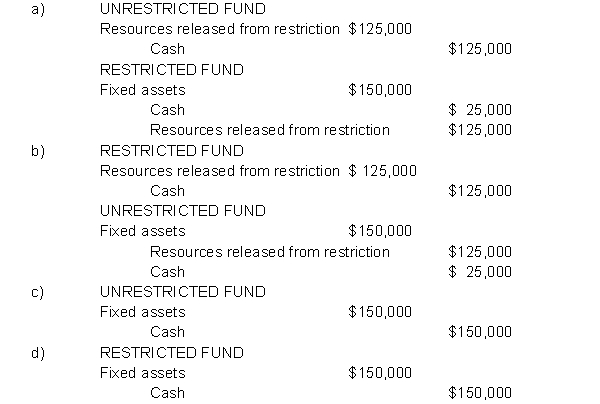

In a prior year, United Charities received a $125,000 gift to be used to acquire vans to provide transportation for physically challenged adults. During the current year, United acquired two vans at a cost of $75,000 each. The appropriate entry(ies) to record the acquisition is

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/66

Play

Full screen (f)

Deck 12: Not-For-Profit Organizations

1

The focus on donor-mandated restrictions imposes special responsibilities on management to utilize the funds as the donor requested.

True

2

Whether a not-for-profit's resources are classified as restricted or unrestricted depends on the presence or absence of donor stipulations.

True

3

The primary source of authoritative accounting and financial reporting guidance for a private college is the AICPA.

False

4

FASB Statement No. 95 requires not-for-profits to use the direct method in their statements of cash flows.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

5

FASB Statement No. 93 makes the recognition of depreciation on plant and equipment assets optional at the discretion of the not-for-profit.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

6

Donor restrictions are only recognized when there is a specific purpose for the donated resources.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

7

Traditional financial ratios, such as measures of liquidity and debt burden, are seldom useful for assessing the fiscal health of not-for-profits.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

8

Assets without donor restrictions cannot be restricted, including by the governing board or other outside parties

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

9

Temporarily restricted funds related to plant and equipment generally account only for resources restricted to their purchase or construction, not for the plant and equipment itself, which are typically reported in the unrestricted fund.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

10

The FASB requires external financial reports to provide information about

A) Donor-imposed restrictions on resources.

B) All restrictions on resources.

C) Donor and creditor restrictions on resources.

D) None of the above.

A) Donor-imposed restrictions on resources.

B) All restrictions on resources.

C) Donor and creditor restrictions on resources.

D) None of the above.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

11

FASB Statement No. 117 directs that revenues and expenses be reported in a statement of financial position.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

12

Expenses should be classified as unrestricted or temporarily restricted, consistent with the classification of the resources used to finance them.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

13

The basis of accounting used by not-for-profit organizations in their external financial reports is

A) Industry-specific basis of accounting.

B) Cash basis of accounting.

C) Modified accrual basis of accounting.

D) Accrual basis of accounting.

A) Industry-specific basis of accounting.

B) Cash basis of accounting.

C) Modified accrual basis of accounting.

D) Accrual basis of accounting.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

14

All not-for-profit organizations, including city-owned museums and two-year community colleges, must adhere to FASB accounting and financial reporting standards.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

15

Unlike governments, not-for-profits should not recognize contributions of art collections as revenue unless they capitalize them.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

16

The FASB requires the balance sheets of not-for-profits to display

A) Net assets in two separate categories-donor-imposed restrictions and unrestricted.

B) Four separate funds-unrestricted, partially restricted, temporarily restricted, and permanently restricted net assets.

C) Six totals-total assets, total liabilities, total net assets, total unrestricted net assets, total temporarily restricted net assets, and total permanently restricted net assets.

D) Unrestricted and restricted retained earnings.

A) Net assets in two separate categories-donor-imposed restrictions and unrestricted.

B) Four separate funds-unrestricted, partially restricted, temporarily restricted, and permanently restricted net assets.

C) Six totals-total assets, total liabilities, total net assets, total unrestricted net assets, total temporarily restricted net assets, and total permanently restricted net assets.

D) Unrestricted and restricted retained earnings.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

17

In accounting for investments, not-for-profits, like businesses, must report their investments at fair value and classify the investments as trading, or available-for-sale, or held-to-maturity.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

18

Not-for-profits generally should not recognize as revenues contributions that they have agreed to pass along to other specific beneficiaries.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

19

FASB standards require not-for-profit organizations to classify their resources into three categories: unrestricted, temporarily restricted, and permanently restricted.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

20

In the statement of activities, FASB ASU 2016-14 requires net assets to be classified in one of the two categories of net assets - net assets without donor restrictions and net assets with donor restrictions.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following characteristics most clearly distinguishes an exchange transaction from a contribution?

A) A contribution is always in cash.

B) An exchange transaction is a reciprocal transfer of resources.

C) An exchange transaction is a nonreciprocal transfer of assets.

D) Contributions of assets always have restrictions attached as to their use.

A) A contribution is always in cash.

B) An exchange transaction is a reciprocal transfer of resources.

C) An exchange transaction is a nonreciprocal transfer of assets.

D) Contributions of assets always have restrictions attached as to their use.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

22

Expenses incurred by not-for-profit organizations should be reported as

A) Decreases in one of the two categories of net assets.

B) Decreases in unrestricted net assets.

C) Decreases in revenue

D) Decreases in donor restricted net assets.

A) Decreases in one of the two categories of net assets.

B) Decreases in unrestricted net assets.

C) Decreases in revenue

D) Decreases in donor restricted net assets.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

23

The increase in unrestricted net assets in 2016 as a result of the fund-raising drive is

A) $1,200,000.

B) $1,050,000.

C) $800,000.

D) $250,000.

A) $1,200,000.

B) $1,050,000.

C) $800,000.

D) $250,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

24

Revenue from an exchange transaction may be classified as an increase in which class of net assets?

A) Unrestricted net assets when performance obligation is met.

B) Unrestricted restricted net assets when performance obligation is defined.

C) Restricted net assets.

D) Any of the above.

A) Unrestricted net assets when performance obligation is met.

B) Unrestricted restricted net assets when performance obligation is defined.

C) Restricted net assets.

D) Any of the above.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

25

In the current year a not-for-profit entity received a contribution of $100,000 to use for scholarships. The entity had budgeted $400,000 for scholarships in the current year and it disbursed $350,000 for scholarships. The amount the entity can consider as 'released from restriction' in the current year is

A) $0.

B) $100,000.

C) $350,000.

D) $400,000.

A) $0.

B) $100,000.

C) $350,000.

D) $400,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

26

St. Mary's Extended Care Center, a not-for-profit entity, enjoys the services of a group of high-school-age people who each agree to work three afternoons a week for three hours each afternoon performing a variety of patient-related services, such as writing letters for those who are unable to do so, delivering mail to the patient rooms, and pushing wheel-chair patients across the grounds. The services rendered by these young people enhance the quality of life for the residents. They could not be provided if they were not donated because there are not enough resources to do so. The past year the young people donated 5,000 hours in total. The services would have cost $6.00 per hour if they had been purchased but they were worth $10 an hour to St. Mary's. What is the amount of contributed revenue that should be recognized by St. Mary's related to these services?

A) $50,000.

B) $30,000

C) $0.

D) Cannot determine.

A) $50,000.

B) $30,000

C) $0.

D) Cannot determine.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

27

In 2017, the change in unrestricted net assets is

A) $0

B) $200,000 increase.

C) $200,000 decrease.

D) $1,000,000 increase.

A) $0

B) $200,000 increase.

C) $200,000 decrease.

D) $1,000,000 increase.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

28

In a prior year, United Charities received a $125,000 gift to be used to acquire vans to provide transportation for physically challenged adults. During the current year, United acquired two vans at a cost of $75,000 each. The appropriate entry(ies) to record the acquisition is

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

29

Revenues of a not-for-profit organization should be reported as

A) Increases in one of the two categories of net assets.

B) Increases in unrestricted net assets.

C) Increases in expenses.

D) Increases in permanently restricted net assets.

A) Increases in one of the two categories of net assets.

B) Increases in unrestricted net assets.

C) Increases in expenses.

D) Increases in permanently restricted net assets.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

30

In the current year National Pet Charities, which uses fund-type accounting to maintain its books and records, received a $30,000 contribution to help educate people on responsible pet ownership. During the current year, the entry to record this donation is

A) UNRESTRICTED FUND. No entry. RESTRICTED FUND. Debit Cash $30,000; Credit Revenues $30,000.

B) UNRESTRICTED FUND. No entry. RESTRICTED FUND. Debit Cash $30,000; Credit Net assets $30,000.

C) UNRESTICTED FUND. Debit Cash $30,000; Credit Revenues $30,000. RESTRICTED FUND. No entry.

D) UNRESTRICTED FUND. Debit Cash $30,000; Credit Net assets $30,000. RESTRICTED FUND. No entry.

A) UNRESTRICTED FUND. No entry. RESTRICTED FUND. Debit Cash $30,000; Credit Revenues $30,000.

B) UNRESTRICTED FUND. No entry. RESTRICTED FUND. Debit Cash $30,000; Credit Net assets $30,000.

C) UNRESTICTED FUND. Debit Cash $30,000; Credit Revenues $30,000. RESTRICTED FUND. No entry.

D) UNRESTRICTED FUND. Debit Cash $30,000; Credit Net assets $30,000. RESTRICTED FUND. No entry.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

31

The FASB requires that all not-for-profit organizations report expenses

A) By object.

B) By function.

C) By natural classification.

D) By budget code.

A) By object.

B) By function.

C) By natural classification.

D) By budget code.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

32

Gifts restricted by the donor to not-for-profit organizations

A) Must be recorded in restricted net assets.

B) Must always be shown as an increase in unrestricted net assets.

C) May be shown as unrestricted if the board votes to release the restrictions.

D) May be shown as an increase in unrestricted net assets at the discretion of management.

A) Must be recorded in restricted net assets.

B) Must always be shown as an increase in unrestricted net assets.

C) May be shown as unrestricted if the board votes to release the restrictions.

D) May be shown as an increase in unrestricted net assets at the discretion of management.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

33

Simplex Games, a not-for-profit entity organized to provide athletic competition opportunities for high school students, utilizes a number of volunteers in carrying out its mission. At the 2017 Games 50 volunteers provided a total of 1,000 hours of service performing tasks such as picking up litter and delivering water to the athletes. A local CPA firm donates its services to prepare the annual tax return and other federal and state required paperwork which must be filed to maintain its status as a tax-exempt organization. During 2017 the CPA firm provided 50 hours of service. If purchased, the CPA services would have cost $60 per hour and the game workers would have cost $6 per hour. How much contributed service revenue should Simplex Games recognize in 2017?

A) $9,000.

B) $6,000.

C) $3,000.

D) $0.

A) $9,000.

B) $6,000.

C) $3,000.

D) $0.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

34

During the annual fund-raising drive, the Cancer Society raised $900,000 in pledges of financial support for general operations. By fiscal year-end, the society had collected $600,000 of the pledges. The society estimates that 10% of the remaining pledges will be uncollectible. The NET amount of revenue the society should recognize during the current year from this pledge drive is

A) $900,000.

B) $870,000.

C) $810,000.

D) $600,000.

A) $900,000.

B) $870,000.

C) $810,000.

D) $600,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

35

The National Association for the Preservation of Wildlife received $10,000 from a benefactor to support the overall objective of the organization. This amount will be recognized as revenue

A) In the period received.

B) In the period spent.

C) Never, because it is not earned.

D) When the not-for-profit satisfies any performance obligation.

A) In the period received.

B) In the period spent.

C) Never, because it is not earned.

D) When the not-for-profit satisfies any performance obligation.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

36

Not-for-profit organizations should report interest and dividends earned and restricted for long-term purposes in which of the following cash flows categories?

A) Operating

B) Financing.

C) Capital financing.

D) Investing.

A) Operating

B) Financing.

C) Capital financing.

D) Investing.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

37

Not-for-profit organizations report their cash flows in which of the following categories?

A) Operating, noncapital financing, capital financing, investing.

B) Operating, noncapital financing, investing.

C) Operating, capital financing, investing.

D) Operating, financing, investing.

A) Operating, noncapital financing, capital financing, investing.

B) Operating, noncapital financing, investing.

C) Operating, capital financing, investing.

D) Operating, financing, investing.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

38

Grace Church, a not-for-profit entity, operates a school in connection with the church. This year members of the church decided to construct a new wing on the school with six classrooms. The church hired an architect and a construction supervisor. The bulk of the labor for construction was donated by church members who were willing workers but not necessarily skilled carpenters. Materials for the construction cost $600,000 and the paid labor was $200,000. The fair value of the completed building is $2 million. When the building is completed what should be the balance in the asset account "Building" and the account "Contributed revenue"?

A) Building $800,000; Contributed Revenue $0.

B) Building $800,000; Contributed Revenue $1,200,000.

C) Building $2 million; Contributed Revenue $1,200,000.

D) Building $2 million; Contributed Revenue $0.

A) Building $800,000; Contributed Revenue $0.

B) Building $800,000; Contributed Revenue $1,200,000.

C) Building $2 million; Contributed Revenue $1,200,000.

D) Building $2 million; Contributed Revenue $0.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

39

The increase in unrestricted net assets in 2016 as a result of the fund-raising drive is

A) $1,200,000.

B) $1,050,000.

C) $800,000.

D) $250,000.

A) $1,200,000.

B) $1,050,000.

C) $800,000.

D) $250,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

40

Not-for-profit organizations should report contributions not restricted to long-term purposes in which of the following cash flows categories?

A) Operating

B) Financing.

C) Capital financing.

D) Investing.

A) Operating

B) Financing.

C) Capital financing.

D) Investing.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

41

A not-for-profit art museum that has elected not to capitalize its art collection receives a donation of a rare piece of Tlinket Indian art. The donor paid $8,000 for the piece several years ago. Today the piece has an estimated fair value of $50,000. What entry should the art museum make upon receipt of this donation?

A) Debit Collection items $50,000; Credit restricted revenue $50,000.

B) Debit Collection items $8,000; Credit unrestricted net asset $8,000.

C) Debit Collection items $50,000; Credit Unrestricted net assets $50,000.

D) No entry required.

A) Debit Collection items $50,000; Credit restricted revenue $50,000.

B) Debit Collection items $8,000; Credit unrestricted net asset $8,000.

C) Debit Collection items $50,000; Credit Unrestricted net assets $50,000.

D) No entry required.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

42

United Charities, a not-for-profit entity, supports activities for lower-income families. They have regularly engaged in activities such as providing transportation for physically challenged individuals, shelters for the temporarily homeless, group meals for the homeless, and shelters for abused women and children.

REQUIRED:

Record the following transactions. Your entries should clearly indicate the fund in which the entry is made or the class of net assets to which the entry will be closed. If no entry is required, write "No entry required."

a. United Charities engaged in a fund-raising campaign that resulted in pledges of $600,000 to support activities of the current year. During the year, United collected $450,000 on these pledges.

b. A local citizen pledged $50,000 to purchase and equip a van to provide transportation for physically challenged individuals. This citizen has donated regularly and there is no reason to believe that this pledge will not be collectible.

c. In prior years, an advocacy group for abused women donated $10,000 to be used to furnish a "safe-house" for abused women and children. During the current year renovation of the safe house was completed and furniture was acquired at a total cost of $25,000.

d. A wealthy benefactor pledged to give $100,000 to United if United successfully raises a matching amount in a capital asset fund-raising drive being conducted over a 12-month period.

e. Cash of $60,000 is received from a donor who specifies that the money must be spent to provide educational activities for children who will be living in the "safe-house." It will be next year before the "safe-house" has its first residents.

f. A local attorney has agreed to provide legal services to United on a pro bono basis. During the current period the attorney provided services for which she would have billed $1,500.

g. Several older housewives provide services at the United Charities group meal facility. The women work in the kitchen serving meals and cleaning up the kitchen. If these services were not donated United would have to purchase them. The cost of the services at the prevailing wage rate for similar employees would be $50,000 for the current year.

h. Fixed assets belonging to United Charities had an original cost of $370,000, an estimated salvage value of $70,000, and an estimated useful life of 20 years. Record depreciation if applicable.

i. Cash of $90,000 is received from a donor who specifies that $30,000 is for use by United Charities and $60,000 is to be used by Zimbabwe Charities, United's sister organization in Africa.

REQUIRED:

Record the following transactions. Your entries should clearly indicate the fund in which the entry is made or the class of net assets to which the entry will be closed. If no entry is required, write "No entry required."

a. United Charities engaged in a fund-raising campaign that resulted in pledges of $600,000 to support activities of the current year. During the year, United collected $450,000 on these pledges.

b. A local citizen pledged $50,000 to purchase and equip a van to provide transportation for physically challenged individuals. This citizen has donated regularly and there is no reason to believe that this pledge will not be collectible.

c. In prior years, an advocacy group for abused women donated $10,000 to be used to furnish a "safe-house" for abused women and children. During the current year renovation of the safe house was completed and furniture was acquired at a total cost of $25,000.

d. A wealthy benefactor pledged to give $100,000 to United if United successfully raises a matching amount in a capital asset fund-raising drive being conducted over a 12-month period.

e. Cash of $60,000 is received from a donor who specifies that the money must be spent to provide educational activities for children who will be living in the "safe-house." It will be next year before the "safe-house" has its first residents.

f. A local attorney has agreed to provide legal services to United on a pro bono basis. During the current period the attorney provided services for which she would have billed $1,500.

g. Several older housewives provide services at the United Charities group meal facility. The women work in the kitchen serving meals and cleaning up the kitchen. If these services were not donated United would have to purchase them. The cost of the services at the prevailing wage rate for similar employees would be $50,000 for the current year.

h. Fixed assets belonging to United Charities had an original cost of $370,000, an estimated salvage value of $70,000, and an estimated useful life of 20 years. Record depreciation if applicable.

i. Cash of $90,000 is received from a donor who specifies that $30,000 is for use by United Charities and $60,000 is to be used by Zimbabwe Charities, United's sister organization in Africa.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

43

The Save the Animals Foundation received a gift of $500,000 from a donor who wanted the gift used to acquire habitat for endangered snails. The money may be invested but all earnings are restricted to habitat acquisition. During the year the entire gift was invested in corporate securities. At year-end, the securities had a value of $501,000. The appropriate way to recognize the change in fair value is

A) Debit Investments $1,000; Credit Unrestricted revenue $1,000.

B) Debit Investments $1,000; Credit Restricted revenue $1,000.

C) Debit Investments $1,000; Credit Gain Loss adjustent $1,000.

D) No entry should be made until the securities are sold.

A) Debit Investments $1,000; Credit Unrestricted revenue $1,000.

B) Debit Investments $1,000; Credit Restricted revenue $1,000.

C) Debit Investments $1,000; Credit Gain Loss adjustent $1,000.

D) No entry should be made until the securities are sold.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

44

A not-for-profit would include which of the following financial statements in its basic financial statements?

A) Statement of financial position and statement of activities.

B) Statement of financial position, statement of activities, and statement of cash flows.

C) Statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses.

D) Statement of financial position, statement of activities, and statement of functional expenses.

A) Statement of financial position and statement of activities.

B) Statement of financial position, statement of activities, and statement of cash flows.

C) Statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses.

D) Statement of financial position, statement of activities, and statement of functional expenses.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

45

Liquidity is reported by the not-for-profit with

A) quantitative information about the ability of the not-for-profit to meet obligations

B) an assessment signed by the executive director that the not-for-profit can meet its obligations

C) via a press release

D) measures of liquidity do not have to be reported

ANSWERS TO MULTIPLE CHOICE (CHAPTER 12)

A) quantitative information about the ability of the not-for-profit to meet obligations

B) an assessment signed by the executive director that the not-for-profit can meet its obligations

C) via a press release

D) measures of liquidity do not have to be reported

ANSWERS TO MULTIPLE CHOICE (CHAPTER 12)

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

46

According to AICPA guidance, a not-for-profit organization (X) is required to consolidate a related not-for-profit organization (Y) in its financial statements when

A) The relationship results from a merger of X and Y.

B) X has a controlling financial interest in Y through direct or indirect ownership of a majority voting interest.

C) X can control Y through a contract or affiliation agreement, even though X does not have a majority ownership or voting interest.

D) Any of the above.

A) The relationship results from a merger of X and Y.

B) X has a controlling financial interest in Y through direct or indirect ownership of a majority voting interest.

C) X can control Y through a contract or affiliation agreement, even though X does not have a majority ownership or voting interest.

D) Any of the above.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

47

The Heritage Art Museum, a not-for-profit entity specializing in art items created by natives of the Pacific Northwest, has a December 31 fiscal year-end. The museum has a policy of NOT capitalizing collection items.

REQUIRED:

Your entries should clearly indicate the fund in which the entry is made or to which class of net assets the account would be closed. If no entry is required, write "No entry required."

a. During the current year the museum received admissions fees of $500,000 in cash.

b. Citizens of the local community are encouraged to participate in a program called "Friends of the Museum." For a yearly contribution of $25 per family, a family is entitled to free admission to the museum during the calendar year. A "friend of the museum" also receives a monthly one-page newsletter announcing upcoming events. At year-end, there were 1,000 members in "Friends of the Museum."

c. During the current year the museum incurred salaries expense of $1 million of which $40,000 remains unpaid at year-end.

d. During the year the museum incurred operating expenses of $450,000 of which $30,000 remains unpaid at year-end. Of the $450,000, $50,000 was used to buy supplies and $20,000 of supplies remain on hand at year-end.

e. Office equipment owned by the museum has a historical cost of $140,000 and a salvage value of $20,000 and is being depreciated over 8 years on the straight-line basis.

f. During the year the museum conducted a fund-raising drive to raise money to acquire new art items for the museum. The museum received pledges of $200,000 of which the museum had collected $160,000 by year-end and expected to ultimately collect another $20,000.

g. The museum had a small portfolio of investments in equity securities.. At the beginning of the year the portfolio had a fair value of $60,000. During the year the Museum collected $3,000 in dividends on the securities. At year-end the portfolio had a market value of $62,000.

h. During the year a citizen died and willed his wonderful collection of native art to the museum. The appraised value of the collection was $600,000.

i. To balance its collection, the museum sold two of its collection items for $250,000, which approximates fair value. These items had a historical cost to the museum of $10,000.

j. The proceeds of the sale and additional cash were used to acquire two new items at a cost of $310,000.

REQUIRED:

Your entries should clearly indicate the fund in which the entry is made or to which class of net assets the account would be closed. If no entry is required, write "No entry required."

a. During the current year the museum received admissions fees of $500,000 in cash.

b. Citizens of the local community are encouraged to participate in a program called "Friends of the Museum." For a yearly contribution of $25 per family, a family is entitled to free admission to the museum during the calendar year. A "friend of the museum" also receives a monthly one-page newsletter announcing upcoming events. At year-end, there were 1,000 members in "Friends of the Museum."

c. During the current year the museum incurred salaries expense of $1 million of which $40,000 remains unpaid at year-end.

d. During the year the museum incurred operating expenses of $450,000 of which $30,000 remains unpaid at year-end. Of the $450,000, $50,000 was used to buy supplies and $20,000 of supplies remain on hand at year-end.

e. Office equipment owned by the museum has a historical cost of $140,000 and a salvage value of $20,000 and is being depreciated over 8 years on the straight-line basis.

f. During the year the museum conducted a fund-raising drive to raise money to acquire new art items for the museum. The museum received pledges of $200,000 of which the museum had collected $160,000 by year-end and expected to ultimately collect another $20,000.

g. The museum had a small portfolio of investments in equity securities.. At the beginning of the year the portfolio had a fair value of $60,000. During the year the Museum collected $3,000 in dividends on the securities. At year-end the portfolio had a market value of $62,000.

h. During the year a citizen died and willed his wonderful collection of native art to the museum. The appraised value of the collection was $600,000.

i. To balance its collection, the museum sold two of its collection items for $250,000, which approximates fair value. These items had a historical cost to the museum of $10,000.

j. The proceeds of the sale and additional cash were used to acquire two new items at a cost of $310,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

48

Music Lovers Foundation, a not-for-profit governed by an independent board, was founded to support the Northern State University Choir until such time as the state legislature adequately funds the choir. When the choir is adequately funded by appropriation, the Foundation may direct resources to other music projects that it deems acceptable. When Music Lovers accepts a contribution from a donor it should debit cash and/or other assets and credit

A) Unrestricted revenue.

B) Temporarily restricted revenue.

C) Liability.

D) It should not make an entry.

A) Unrestricted revenue.

B) Temporarily restricted revenue.

C) Liability.

D) It should not make an entry.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

49

"Net assets released from restriction" for a not-for-profit organization is comparable to which of the following for a government?

A) Other financing sources (uses)-Nonreciprocal transfer

B) Expenditures

C) Expenses

D) Unassigned fund balance

A) Other financing sources (uses)-Nonreciprocal transfer

B) Expenditures

C) Expenses

D) Unassigned fund balance

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

50

Native Art Museum, a not-for-profit entity that elects not to capitalize its collection items, purchased for $10,000 a wonderful totem pole for display near the door of the museum. As a result of this transaction, which of the following entries should be made?

A) Debit Collection items $10,000; Credit Cash $10,000.

B) Debit Collection expense $10,000; Credit Cash $10,000.

C) Debit Unrestricted net assets $10,000; Credit Cash $10,000.

D) No entry is required.

A) Debit Collection items $10,000; Credit Cash $10,000.

B) Debit Collection expense $10,000; Credit Cash $10,000.

C) Debit Unrestricted net assets $10,000; Credit Cash $10,000.

D) No entry is required.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

51

The Midwest Circulatory Diseases Society placed an advertisement in prominent publications in the region. The advertisement provided information about symptoms of the diseases and offered practical advice for controlling their immediate effects. The society's accountants estimate that about 75 percent of the advertising copy was devoted to information about the disease and the remainder was an appeal for funds. The advertisement cost $20,000. Using the physical units method of separating joint costs, how much of the cost of the advertisement should be reported as program costs?

A) $20,000.

B) $15,000.

C) $10,000.

D) $5,000.

A) $20,000.

B) $15,000.

C) $10,000.

D) $5,000.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

52

United Charities accepted a contribution from a donor and agreed to transfer the assets to Aid for Friends, a not-for-profit that provides temporary shelter to the homeless. United Charities should debit cash or other assets and credit

A) Unrestricted revenue.

B) Restricted revenue.

C) Liability to Aid for Friends.

D) United Charities should not make an entry.

A) Unrestricted revenue.

B) Restricted revenue.

C) Liability to Aid for Friends.

D) United Charities should not make an entry.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

53

Open Air Conservatory, a not-for-profit entity, held a fund-raising drive to raise money to buy land to provide a habitat for the endangered Sleepy Eagle. A donor pledged $1 million to the project provided that Open Air Conservatory was able to raise an additional $1.5 million from other sources. What entry should Open Air Conservatory make at the time of the $1 million pledge?

A) Debit Pledge receivable $1 million; Credit Unrestricted revenue $1 million.

B) Debit Pledges receivable $1 million; Credit Restricted revenue $1 million.

C) Debit Pledges receivable $1 million; Credit Grant revenue $1 million.

D) No entry is made at the time of the pledge.

A) Debit Pledge receivable $1 million; Credit Unrestricted revenue $1 million.

B) Debit Pledges receivable $1 million; Credit Restricted revenue $1 million.

C) Debit Pledges receivable $1 million; Credit Grant revenue $1 million.

D) No entry is made at the time of the pledge.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

54

Nelson County Historical museum, a not-for-profit entity that capitalizes its collection items, received a gift of several Civil War artifacts to be used for display and research. The donor found these items while cleaning out the closet of an old house. The fair value is hard to estimate but a dealer in these types of artifacts estimates their value at $2,000. The entry to record this donation is

A) Debit Collection expense, $2,000; Credit Contributions revenue $2,000.

B) Debit Collection items $2,000; Credit Contributions revenue $2,000.

C) No entry is required because the cost to the donor was $0.

D) No entry required because the value of the items is estimated.

A) Debit Collection expense, $2,000; Credit Contributions revenue $2,000.

B) Debit Collection items $2,000; Credit Contributions revenue $2,000.

C) No entry is required because the cost to the donor was $0.

D) No entry required because the value of the items is estimated.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

55

The Friends of the Library (FOL), a not-for-profit entity, received a gift restricted to the acquisition of a special piece of equipment used to restore books. Late last year FOL acquired the machine at a total cost of $19,000. The machine is estimated to have a useful life of eight years and a salvage value of $3,000. In what fund should FOL make the entry to record the depreciation for the current year?

A) Unrestricted fund.

B) Fiduciary fund.

C) Permanently restricted fund.

D) FOL should not recognize depreciation.

A) Unrestricted fund.

B) Fiduciary fund.

C) Permanently restricted fund.

D) FOL should not recognize depreciation.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

56

When should a not-for-profit entity recognize pledge revenue that is contingent upon raising a matching amount?

A) When the pledge is made.

B) When the cash is received.

C) When the matching funds have been raised.

D) When the project is completed.

A) When the pledge is made.

B) When the cash is received.

C) When the matching funds have been raised.

D) When the project is completed.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

57

A donor pledges $100,000 to the Shakespeare Foundation to be used only to support the summer Shakespeare Theater-an event that has been held every summer for 38 years. This is an example of a

A) Conditional Contribution.

B) Unconditional contribution.

C) Donor restricted contribution.

D) Unrestricted contribution.

A) Conditional Contribution.

B) Unconditional contribution.

C) Donor restricted contribution.

D) Unrestricted contribution.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

58

During the year, a not-for-profit entity received $30,000 in dividends and $24,000 in interest on its investment portfolio. The entity also accrued $6,000 in interest on the portfolio. The increase in fair value of the portfolio during the year was $8,000. How much should the entity report as investment earnings during the year?

A) $62,000.

B) $54,000.

C) $8,000.

D) $0.

A) $62,000.

B) $54,000.

C) $8,000.

D) $0.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

59

Save the Children Foundation had the following types of cash receipts and disbursements during its current fiscal year.

REQUIRED:

Indicate in which categories each of these flows would be reported in the foundation's statement of cash flows.

a. Unrestricted contributions

b. Sales of handmade crafts

c. Contributions restricted to capital asset acquisition

d. Contributions to endowments

e. Investment earnings on endowments, not required to be added to the endowment

f. Salaries

g. Interest paid on short-term loan

h. Capital asset purchases

i. Investments sold

j. Short-term loan proceeds

k. Contributions made to other organizations

l. Capital lease payments.

REQUIRED:

Indicate in which categories each of these flows would be reported in the foundation's statement of cash flows.

a. Unrestricted contributions

b. Sales of handmade crafts

c. Contributions restricted to capital asset acquisition

d. Contributions to endowments

e. Investment earnings on endowments, not required to be added to the endowment

f. Salaries

g. Interest paid on short-term loan

h. Capital asset purchases

i. Investments sold

j. Short-term loan proceeds

k. Contributions made to other organizations

l. Capital lease payments.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following entities should recognize depreciation expense on its operating statement?

A) Not-for-profit university.

B) Not-for-profit foundation.

C) Not-for-profit hospital.

D) All of the above.

A) Not-for-profit university.

B) Not-for-profit foundation.

C) Not-for-profit hospital.

D) All of the above.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

61

Per FASB standards, not-for-profits must classify their net assets into three classes. What is the basis for distinguishing the three classes? What is the rationale for this basis? How is each class defined?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

62

A generous benefactor pledges $1 million to The R. J. Smith Foundation, a not-for-profit entity that promotes the arts. The gift is to be used to provide scholarships for talented musicians at a music camp operated by the Foundation. The gift was given in August 2013 to support the Summer 2014 music program. The foundation director argues that the gift is a conditional restricted gift and therefore cannot be recognized as revenue in 2013. The accountant argues that the gift is an unconditional restricted gift and must be recognized in the current year. What is the basis for the director's argument? What is the basis for the accountant's argument? In your answer provide an explanation of the terms conditional, unconditional, restricted and unrestricted.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

63

What is a charitable remainder trust? How should it be accounted for?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

64

For each of the cases below, state whether the contributed services would be recognized and, if so, how much would be recognized and how it would be recognized. Explain your answer in terms of the existing standards. Also explain why, in your opinion, the standards permit or prohibit recognition of this particular type of contribution.

a. A church votes to construct a new educational wing on its existing facility. The church will hire an architect to design the new wing and a construction supervisor to oversee the construction. Church members will provide most of the labor for the construction. Labor donated by members who have construction experience or who are considered professional craftsmen at the prevailing wage for their trade or craft is $500,000. Labor donated by persons possessing non-building specialized skills (doctors, teachers, lawyers, etc.) at their prevailing wage rates is $700,000. Labor donated by non-professionals measured at the minimum wage is $300,000. The appraised value of the building when completed is $3 million. The architect was paid $700,000, the construction supervisor was paid $50,000 and the materials purchased for use in the building cost $1 million.

b. An investment advisor, a member of the board of No Fleas Please, a not-for-profit animal care organization, provides pro bono investment advice to NFP. NFP does not have a particularly large investment portfolio and, without the advice of the board member, NFP probably would invest its idle cash in certificates of deposit at an insured commercial bank to protect itself against loss of principal. If the investment advisor had provided similar services to his customers he would have charged $2,000.

c. Members of a religious order provide professional nursing services for a healthcare facility that is run by their order. The members are not compensated but their order provides lodging, food, and other necessities, the cost of which is paid by the healthcare entity and classified as nursing services expense. At the end of the year the balance in the nursing services expense account is $3 million. The value of the nursing services provided, measured at the prevailing wage for nurses, is $5 million.

a. A church votes to construct a new educational wing on its existing facility. The church will hire an architect to design the new wing and a construction supervisor to oversee the construction. Church members will provide most of the labor for the construction. Labor donated by members who have construction experience or who are considered professional craftsmen at the prevailing wage for their trade or craft is $500,000. Labor donated by persons possessing non-building specialized skills (doctors, teachers, lawyers, etc.) at their prevailing wage rates is $700,000. Labor donated by non-professionals measured at the minimum wage is $300,000. The appraised value of the building when completed is $3 million. The architect was paid $700,000, the construction supervisor was paid $50,000 and the materials purchased for use in the building cost $1 million.

b. An investment advisor, a member of the board of No Fleas Please, a not-for-profit animal care organization, provides pro bono investment advice to NFP. NFP does not have a particularly large investment portfolio and, without the advice of the board member, NFP probably would invest its idle cash in certificates of deposit at an insured commercial bank to protect itself against loss of principal. If the investment advisor had provided similar services to his customers he would have charged $2,000.

c. Members of a religious order provide professional nursing services for a healthcare facility that is run by their order. The members are not compensated but their order provides lodging, food, and other necessities, the cost of which is paid by the healthcare entity and classified as nursing services expense. At the end of the year the balance in the nursing services expense account is $3 million. The value of the nursing services provided, measured at the prevailing wage for nurses, is $5 million.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

65

In June 2016, the wealthy parents of a college sophomore pledge to donate $1.5

million to the college she attends, making payments of $0.5 million at the end of each of her remaining years at the school until her expected graduation in 2019. The college applies a discount rate of 3 percent. At that rate, the present value of $1 for three periods is $2.82861.

REQUIRED:

What entry, if any, would be required to recognize the pledge? What entry(ies), if any, would be required to record the receipt of the first $0.5 million at the end of year 2016? Assume that the college uses separate funds to track restricted resources and indicate in which fund each entry is made.

million to the college she attends, making payments of $0.5 million at the end of each of her remaining years at the school until her expected graduation in 2019. The college applies a discount rate of 3 percent. At that rate, the present value of $1 for three periods is $2.82861.

REQUIRED:

What entry, if any, would be required to recognize the pledge? What entry(ies), if any, would be required to record the receipt of the first $0.5 million at the end of year 2016? Assume that the college uses separate funds to track restricted resources and indicate in which fund each entry is made.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

66

In December 2016, Technology University received a $2 million grant from the National Hockey Association to develop an effective neck brace to prevent injuries in its non-goalie hockey players. The NHA grant was intended to cover $1.5 million of direct costs and $0.5 million of overhead costs. The grant stipulated that the NHA would be the sole beneficiary of the research. Technology carried out the research in 2017. As anticipated, direct costs were $1.5 million.

REQUIRED:

a. What accounting entries, if any, should Technology make when notified of the grant?

b. What accounting entries, if any, should Technology make in 2017? (Be sure to indicate in which funds the entries would be recorded.)

c. Would your answer be different if the research were made available to the general public and not just the NHA? Explain.

d. Would your answer be different if the NHA indicated it would not make any payments on the research until Technology delivered the final research product?

REQUIRED:

a. What accounting entries, if any, should Technology make when notified of the grant?

b. What accounting entries, if any, should Technology make in 2017? (Be sure to indicate in which funds the entries would be recorded.)

c. Would your answer be different if the research were made available to the general public and not just the NHA? Explain.

d. Would your answer be different if the NHA indicated it would not make any payments on the research until Technology delivered the final research product?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 66 flashcards in this deck.