Deck 15: Financial Instruments: Complex Debt and Equity

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

ABC Inc., a publicly traded company, 100,000 granted stock options on January 1, Year 1, with a total value of $150,000.The option will vest over a three-year period, and employees may exercise their options as of year 4.On December 31, Year 1, it is estimated that 80% of the options will fully vest.During Year 2, an executive suddenly quit, forfeiting 20,000 options.On December 31st, Year 2 the estimate of the number of options that will fully vest by the end of Year 3 was revised to 50,000.The December 31st, Year 2 year-end accrual required with respect to these stock options would include a compensation expense amount of:

A)$10,000.

B)$30,000.

C)$20,000.

D)$25,000.

A)$10,000.

B)$30,000.

C)$20,000.

D)$25,000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

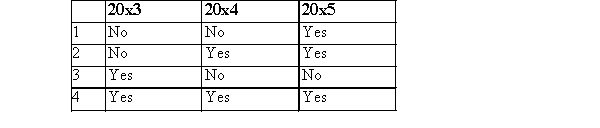

Compensatory stock options were granted to executives on January 1, 20x3, with a measurement date of June 30, 20x4, for services to be rendered during 20x3, 20x4, and 20x5.The excess of the market value of the shares over the option price at the measurement date was reasonably estimable at the date of grant.The stock option was exercised on October 31, 20x5.Compensation expense should be recognized in the income statement in which of the following years?

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/135

Play

Full screen (f)

Deck 15: Financial Instruments: Complex Debt and Equity

1

The incremental method to accounting for convertible bonds means that:

A)The proceeds of the bond are allocated on the basis of the book values of the straight bond and imbedded stock option

B)The proceeds of the bond are allocated on the basis of the relative market values of the straight bond and imbedded stock option

C)The stock option is valued at the difference between the total proceeds of the bond issue and the market value of an equivalent straight bond issue

D)None of these answers are correct

A)The proceeds of the bond are allocated on the basis of the book values of the straight bond and imbedded stock option

B)The proceeds of the bond are allocated on the basis of the relative market values of the straight bond and imbedded stock option

C)The stock option is valued at the difference between the total proceeds of the bond issue and the market value of an equivalent straight bond issue

D)None of these answers are correct

C

2

At the end of 2014, interest on a perpetual loan is paid to the holder.The perpetual debt is shown as an equity instrument.Based on the above the interest is:

A)Added for income tax purposes

B)Deducted on the income statement

C)Added to the income statement

D)Deducted for income tax purposes

A)Added for income tax purposes

B)Deducted on the income statement

C)Added to the income statement

D)Deducted for income tax purposes

D

3

In order to determine if, in substance, a complex financial instrument is debt, the answer should be yes to all of the following except:

A)Is the debtor legally obligated to repay the principal at the option of the creditor?

B)Is the debtor legally obligated to repay the principal at a fixed rate?

C)Is the amount convertible into common shares?

D)Is the periodic return on capital obligatory?

A)Is the debtor legally obligated to repay the principal at the option of the creditor?

B)Is the debtor legally obligated to repay the principal at a fixed rate?

C)Is the amount convertible into common shares?

D)Is the periodic return on capital obligatory?

C

4

Which of the following is an example of a financial asset?

A)Prepaid expenses

B)accounts receivable

C)Inventory

D)Capital assets

A)Prepaid expenses

B)accounts receivable

C)Inventory

D)Capital assets

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

5

On January 1, Year 1, ABC Inc., a publicly traded enterprise, issued $4,000,000 worth of bonds with detachable stock warrants.The bonds mature on December 31st, Year 4 and pay interest annually on December 31st at a coupon rate of 6% per annum.The yield to maturity on similar bonds was 5% at the date of issue.The bonds were issued at 108. Based on the information provided, which of the following statements is most correct?

A)On the date of issue, the bonds would be valued at $4,141,838 and the warrants would be valued at $178,162.

B)On the date of issue, the bonds would be valued at $3,821,838 and the warrants would be valued at $178,162.

C)On the date of issue, the bonds would be valued at $4,000,000 and the warrants would be valued at $320,000.

D)On the date of issue, the bonds would be valued at $4,000,000 and the warrants would be valued at $178,162.

A)On the date of issue, the bonds would be valued at $4,141,838 and the warrants would be valued at $178,162.

B)On the date of issue, the bonds would be valued at $3,821,838 and the warrants would be valued at $178,162.

C)On the date of issue, the bonds would be valued at $4,000,000 and the warrants would be valued at $320,000.

D)On the date of issue, the bonds would be valued at $4,000,000 and the warrants would be valued at $178,162.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

6

S Corporation created a stock option plan for its two top executives.The plan provided that each executive would receive 1,000 options, which would enable him or her to purchase 100 shares at 75 percent of the market price on the date the options, became exercisable.The options were exercisable in two years.At the date of granting the options, the market price of the shares was $12 per share.The date of measurement for the stock option plan was the:

A)date the employees' exercise their options.

B)end of the second year.

C)end of the first year.

D)date of grant.

A)date the employees' exercise their options.

B)end of the second year.

C)end of the first year.

D)date of grant.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

7

An option is:

A)The right to buy or sell something in the future.

B)A debt instrument.

C)An obligation to buy something in the future.

D)An obligation to sell something in the future.

A)The right to buy or sell something in the future.

B)A debt instrument.

C)An obligation to buy something in the future.

D)An obligation to sell something in the future.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

8

On January 1st, 2014 ABC Inc.had invoiced a client in New York for $10,000 US for services rendered that day.ABC did not hedge this receivable.The receivable is due in 60 days.On January 1st, 2014, the spot rate was $1US = $1.02CDN.On January 31st, 2014, the spot rate was $1US = $1.05CDN.What is the effect of the above information on ABC's January financial statements?

A)A $300 debit to OCI.

B)A $300 foreign exchange loss.

C)A $300 credit to OCI.

D)A $300 foreign exchange gain.

A)A $300 debit to OCI.

B)A $300 foreign exchange loss.

C)A $300 credit to OCI.

D)A $300 foreign exchange gain.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

9

JMR Ltd.issued $100,000 of 8%, 8 year, non-convertible bond with detachable stock purchase warrants.KER Corp.purchased the entire issue.Each $1,000 bond carries 10 warrants.Each warrant entitles KER to purchase one common share for $20.The bond issue sells for 104 exclusive of accrued interest.Shortly after issuance, the warrants trade for $5 each and the bonds were quoted at 103 ex-warrants.The market value of the bonds and warrants using the proportional method was:

A)$321,000

B)$605,000

C)$107,000

D)$108,000

A)$321,000

B)$605,000

C)$107,000

D)$108,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

10

The crucial aspect of debt on the financial statements is:

A)that the creditors can demand payment.

B)the interest payments.

C)the maturity date.

D)the legal agreement.

A)that the creditors can demand payment.

B)the interest payments.

C)the maturity date.

D)the legal agreement.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

11

JMR Ltd.issued $300,000 of 7%, 8 year, non-convertible bond with detachable stock purchase warrants.KER Corp.purchased the entire issue.Each $1,000 bond carries 20 warrants.Each warrant entitles KER to purchase one common share for $20.The bond issue sells for 104 exclusive of accrued interest.Shortly after issuance, the warrants trade for $5 each and there was no market value for the bond.In the journal entry, the amount of the payable for the bond is:

A)$321,000

B)$350,000

C)$339,000

D)$300,000

A)$321,000

B)$350,000

C)$339,000

D)$300,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

12

If a company issues debt that is convertible at the shareholder's option, in substance, the debt is:

A)Equity

B)Debt

C)Subordinated

D)Debt or Equity

A)Equity

B)Debt

C)Subordinated

D)Debt or Equity

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

13

Credit risk is an issue for financial instruments and must be disclosed because:

A)the company may default on its loan

B)the company may not perform their obligations

C)the company may not have enough cash flow to pay suppliers

D)the other parties to financial instruments may not perform their obligations

A)the company may default on its loan

B)the company may not perform their obligations

C)the company may not have enough cash flow to pay suppliers

D)the other parties to financial instruments may not perform their obligations

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

14

Stock Appreciation Rights (SARS)earned by employees may be settled by issuing (choose the best answer):

A)Shares

B)Cash

C)Promissory notes

D)Cash or Shares

A)Shares

B)Cash

C)Promissory notes

D)Cash or Shares

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following forms part of the definition of a financial liability?

A)Cash

B)A contractual right to receive cash or another financial asset from another party

C)An equity instrument of another entity

D)To deliver cash or another financial asset to another party

A)Cash

B)A contractual right to receive cash or another financial asset from another party

C)An equity instrument of another entity

D)To deliver cash or another financial asset to another party

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

16

On the statement of cash flows, a hybrid financial instrument should be:

A)Reported as an operating activity

B)Reported as an investing activity

C)Reported as a financial activity

D)Reported according to its individual components

A)Reported as an operating activity

B)Reported as an investing activity

C)Reported as a financial activity

D)Reported according to its individual components

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

17

ABC Inc., a publicly traded company, 100,000 granted stock options on January 1, Year 1, with a total value of $150,000.The option will vest over a three-year period, and employees may exercise their options as of year 4.On December 31, Year 1, it is estimated that 80% of the options will fully vest.During Year 2, an executive suddenly quit, forfeiting 20,000 options.On December 31st, Year 2 the estimate of the number of options that will fully vest by the end of Year 3 was revised to 50,000.The December 31st, Year 2 year-end accrual required with respect to these stock options would include a compensation expense amount of:

A)$10,000.

B)$30,000.

C)$20,000.

D)$25,000.

A)$10,000.

B)$30,000.

C)$20,000.

D)$25,000.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

18

JMR Ltd.issued $300,000 of 7%, 8 year, non-convertible bond with detachable stock purchase warrants.KER Corp.purchased the entire issue.Each $1,000 bond carries 20 warrants.Each warrant entitles KER to purchase one common share for $20.The bond issue sells for 104 exclusive of accrued interest.Shortly after issuance, the warrants trade for $5 each and the bonds were quoted at 103 ex-warrants.The market value of the bonds and warrants using the proportional method was:

A)$605,000

B)$321,000

C)$350,000

D)$339,000

A)$605,000

B)$321,000

C)$350,000

D)$339,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

19

$10,000 (face value)of bonds was sold with a total of 200 detachable stock warrants attached.Each warrant conveys the right to purchase one common share at a specified price during a specified time period.The market immediately valued the warrants at $2 each.The issue sold for 102.The entry to record the bond issuance would include:

A)dr.bond premium $200

B)cr.bonds payable $10,200

C)dr.owners' equity account $400

D)dr.bond discount $200

A)dr.bond premium $200

B)cr.bonds payable $10,200

C)dr.owners' equity account $400

D)dr.bond discount $200

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

20

All of the following are characteristics of stock rights except:

A)Stock warrants can be exercised without having to redeem the bond

B)Stock warrants can be exercised without having to trade in the bond

C)Stock warrants never expire

D)The warrants are usually detachable

A)Stock warrants can be exercised without having to redeem the bond

B)Stock warrants can be exercised without having to trade in the bond

C)Stock warrants never expire

D)The warrants are usually detachable

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

21

In order to determine if, in substance, a complex financial instrument is equity, the answer should be no to all of the following except:

A)Is the periodic return on capital obligatory?

B)Is the debtor legally obligated to repay the principal at the option of the creditor?

C)Is the amount convertible into common shares?

D)Is the debtor legally obligated to repay the principal at a fixed rate?

A)Is the periodic return on capital obligatory?

B)Is the debtor legally obligated to repay the principal at the option of the creditor?

C)Is the amount convertible into common shares?

D)Is the debtor legally obligated to repay the principal at a fixed rate?

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

22

VB Ltd.raises $150,000 by issuing a financial instrument that pays interest at a rate of 8% per year to the investor.At the end of the fourth year, the financial instrument is retired for $155,000.If the financial instrument is treated as equity then:

A)The repayment will decrease owners' equity

B)Long-term liabilities is increased at issuance

C)The interest payment decreases retained earnings

D)If premium on repayment was not known, it is recorded as a loss on the income statement

A)The repayment will decrease owners' equity

B)Long-term liabilities is increased at issuance

C)The interest payment decreases retained earnings

D)If premium on repayment was not known, it is recorded as a loss on the income statement

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

23

A financial asset has any of the following characteristics except:

A)A debt instrument of another entity

B)A contractual right to exchange financial instruments with another party under conditions that are potentially favourable

C)An equity instrument of another entity

D)Cash

A)A debt instrument of another entity

B)A contractual right to exchange financial instruments with another party under conditions that are potentially favourable

C)An equity instrument of another entity

D)Cash

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

24

VB Ltd.raises $150,000 by issuing a financial instrument that pays interest at a rate of 8% per year to the investor.At the end of the fourth year, the financial instrument is retired for $155,000.If the financial instrument is treated as debt then:

A)Retained Earnings is reduced as the interest payment is treated as a dividend distribution

B)The repayment will decrease owners' equity

C)Shareholders' equity is increased at issuance

D)The interest payment decreases retained earnings

A)Retained Earnings is reduced as the interest payment is treated as a dividend distribution

B)The repayment will decrease owners' equity

C)Shareholders' equity is increased at issuance

D)The interest payment decreases retained earnings

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

25

A forward contract is:

A)The right to sell something in the future.

B)An obligation to buy or sell something in the future.

C)A debt instrument.

D)The right to buy something in the future.

A)The right to sell something in the future.

B)An obligation to buy or sell something in the future.

C)A debt instrument.

D)The right to buy something in the future.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

26

When convertible bonds are submitted for conversion, all of the following must be updated except:

A)Cash

B)Bond premium or discount

C)Foreign exchange gains and losses on foreign currency denominated debt

D)Accrued interest

A)Cash

B)Bond premium or discount

C)Foreign exchange gains and losses on foreign currency denominated debt

D)Accrued interest

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following are requirements for hedge accounting?

A)Reasonable expectation of hedge effectiveness.

B)An existing risk management strategy involving hedging.

C)Designation and documentation of the hedging relationship.

D)All of these answers are correct.

A)Reasonable expectation of hedge effectiveness.

B)An existing risk management strategy involving hedging.

C)Designation and documentation of the hedging relationship.

D)All of these answers are correct.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

28

Silo Corp.granted to Donna, its superstar accountant, the option to purchase Silo common shares for $10, on Jan.1, 20x1.The market price of the shares on that date was $20.The options can be exercised during the period Jan.1, 20x4 through Jan.1, 20x6.The number of shares under option is determined by a formula based on Silo earnings each year.The number of shares actually under option will be the formula value on Dec.31, 20x3.That formula estimated the following number of shares under option at the end of years: 20x1, 200; 20x2, 300.The formula determined the number of shares at Dec.31, 20x3 to be 400.The market prices for Silo shares at the end of years: 20x1, $25; 20x2,

$40, 20x3, $50.What is the recorded compensation expense for 20x2, for Donna?

A)$4,500

B)$3,000

C)$4,000

D)$7,250

E)$5,000

$40, 20x3, $50.What is the recorded compensation expense for 20x2, for Donna?

A)$4,500

B)$3,000

C)$4,000

D)$7,250

E)$5,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

29

JKC initiated a stock option plan for its three top executives.The plan provided that each executive would receive 6,000 options that would enable each one to purchase 600 shares at the option price.The option price was set at 10 percent below market price at the first exercise date.The options could be exercised after the executives remained as employees of the company for 3 more years.The market price of the shares on the date that the options were granted was $10 per share.The amount of compensation expense the company incurred for the three executives due to the option plan was:

A)$0

B)$600

C)$8,100

D)$3,000

E)Cannot be determined from the information provided.

A)$0

B)$600

C)$8,100

D)$3,000

E)Cannot be determined from the information provided.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

30

Why would a corporation issue retractable preferred share in a private placement rather than a normal debt arrangement?

A)The tax treatment of intercorporate dividends

B)Income minimization

C)Cash flow

D)None of these answers are correct.

A)The tax treatment of intercorporate dividends

B)Income minimization

C)Cash flow

D)None of these answers are correct.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

31

All of the following are common reasons for a company to issue convertible bonds except:

A)The company prefers to issue shares, but is unsure of the present stock market and the timing.

B)A bond that has a favourable component such as a conversion privilege, can carry a lower interest rate than a "straight" bond.

C)The bonds are issued to controlling shareholders so that they can receive interest payments in preference to other shareholders.

D)All of these answers are correct.

A)The company prefers to issue shares, but is unsure of the present stock market and the timing.

B)A bond that has a favourable component such as a conversion privilege, can carry a lower interest rate than a "straight" bond.

C)The bonds are issued to controlling shareholders so that they can receive interest payments in preference to other shareholders.

D)All of these answers are correct.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

32

All of the following are examples of derivative instruments except:

A)Currency swaps

B)Retractable preferred shares

C)Foreign exchange forward contracts

D)Interest rate swaps

A)Currency swaps

B)Retractable preferred shares

C)Foreign exchange forward contracts

D)Interest rate swaps

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

33

General characteristics of convertible bonds that will be converted include all of the following except:

A)the company will no longer have to repay the principal amount of the bonds.

B)management fully intends that the conversion privilege will eventually be attractive to the investors.

C)the investors will convert at or before maturity date.

D)the market price of the shares will drop below the conversion price.

A)the company will no longer have to repay the principal amount of the bonds.

B)management fully intends that the conversion privilege will eventually be attractive to the investors.

C)the investors will convert at or before maturity date.

D)the market price of the shares will drop below the conversion price.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

34

A stock option plan is a compensatory plan if:

A)The employee must work for the company until retirement.

B)It involves a cost to the grantor.

C)The employee must report the option on the employee's current tax return.

D)The employee must have worked for the company for one year.

A)The employee must work for the company until retirement.

B)It involves a cost to the grantor.

C)The employee must report the option on the employee's current tax return.

D)The employee must have worked for the company for one year.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

35

For each type of financial instrument, the reporting enterprise should disclose:

A)Significant conditions.

B)Significant terms.

C)The extent and nature of the financial instruments.

D)All of these answers are correct.

A)Significant conditions.

B)Significant terms.

C)The extent and nature of the financial instruments.

D)All of these answers are correct.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

36

Primary securities that have both debt and equity characteristics are called:

A)options

B)convertible debt

C)hybrid securities

D)discount bonds

A)options

B)convertible debt

C)hybrid securities

D)discount bonds

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

37

Compensatory stock options were granted to executives on January 1, 20x3, with a measurement date of June 30, 20x4, for services to be rendered during 20x3, 20x4, and 20x5.The excess of the market value of the shares over the option price at the measurement date was reasonably estimable at the date of grant.The stock option was exercised on October 31, 20x5.Compensation expense should be recognized in the income statement in which of the following years?

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

38

A company issues a convertible bond.Management can essentially force conversion as long as:

A)The share price is lower than the conversion price

B)The share price is higher than the conversion price

C)The share price is equal to the conversion price

D)None of these answers are correct

A)The share price is lower than the conversion price

B)The share price is higher than the conversion price

C)The share price is equal to the conversion price

D)None of these answers are correct

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

39

If a company issues debt that is convertible at the corporation's option, in substance, the debt is:

A)Equity

B)An Asset

C)Debt

D)Subordinated

A)Equity

B)An Asset

C)Debt

D)Subordinated

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

40

On January 1, Year 1, ABC Inc., a publicly traded enterprise, issued $4,000,000 worth of bonds with detachable stock warrants.The bonds mature on December 31st, Year 4 and pay interest annually on December 31st at a coupon rate of 6% per annum.The yield to maturity on similar bonds was 5% at the date of issue.The bonds were issued at 108. Based on the information provided, which of the following statements is most correct?

A)A gain of $51,294.

B)A loss of $39,776.

C)A gain of $39,776.

D)A loss of $51,294.

A)A gain of $51,294.

B)A loss of $39,776.

C)A gain of $39,776.

D)A loss of $51,294.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

41

The tax status of a financial instrument is determined by its legal form and not its substance.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

42

When interest is repayable to investors at a fixed amount per share, the financial instrument in question would be considered debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

43

An equity item is classified as debt in the financial statements and dividend payments were shown on the financial statements.For income tax purposes, the amounts will not be tax deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

44

With respect to convertible bonds, whose conversion is mandatory, only the interest stream is valued as debt; the bond principal and conversion features are considered equity.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

45

Under ASPE, preferred shares must be classified as equity while shareholder loans must be classified as debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

46

Even if the underlying share value of a convertible bond never reaches the conversion price, management can still force conversion.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

47

If a company issues debt that is convertible at the corporation's option, in substance, the debt is equity.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

48

Under ASPE, convertible debt must always be treated as debt in its entirety.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

49

Securities issued as debt but intended by the issuing company to be exchanged for shares by the investor prior to maturity are called:

A)convertible debt

B)discount bonds

C)hybrid securities

D)options

A)convertible debt

B)discount bonds

C)hybrid securities

D)options

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

50

The crucial aspect of debt is that the creditors can demand payment.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

51

The bifurcation of the proceeds from the issue of a complex financial instrument between debt and equity components will be the same, regardless of whether or not the conversion is mandatory.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

52

Poison pills serve to thwart a takeover bid from an outside (hostile)takeover group.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

53

When preferred shares are classified as debt, their dividends are deducted from Retained Earnings, thus bypassing earnings.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

54

Redeemable preferred shares are always classified as debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

55

JMR Ltd.issued $100,000 of 8%, 8 year, non-convertible bond with detachable stock purchase warrants.KER Corp.purchased the entire issue.Each $1,000 bond carries 10 warrants.Each warrant entitles KER to purchase one common share for $20.The bond issue sells for 104 exclusive of accrued interest.Shortly after issuance, the warrants trade for $5 each and the bonds were quoted at 103 ex-warrants.The allocation of the proceeds to bonds using the proportional method was:

A)$108,000

B)$107,000

C)$99,185

D)$100,000

A)$108,000

B)$107,000

C)$99,185

D)$100,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

56

A non-compensatory stock option plan means that:

A)Top executives are given shares in the company.

B)Any employee can purchase shares at a discount from the prevailing market price.

C)No shares are given but shareholders are allowed to be purchased on the open market.

D)None of these answers are correct.

A)Top executives are given shares in the company.

B)Any employee can purchase shares at a discount from the prevailing market price.

C)No shares are given but shareholders are allowed to be purchased on the open market.

D)None of these answers are correct.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

57

Hedge accounting is often performed to minimize any accounting mismatch between the hedged and hedging items and is strictly voluntary.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

58

At the end of 2014, interest on a perpetual loan is paid to the holder.The perpetual debt is shown as an equity instrument.Based on the above the interest is:

A)Added for income tax purposes

B)Deducted on the income statement

C)Added to the statement of retained earnings

D)Deducted on the statement of retained earnings

A)Added for income tax purposes

B)Deducted on the income statement

C)Added to the statement of retained earnings

D)Deducted on the statement of retained earnings

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

59

Stock appreciation rights (SARS)and share based payments are only payable in common shares or other equity instruments.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

60

Derivatives may be described as:

A)Promissory notes

B)Common shares

C)Executory contracts

D)Executed contracts

A)Promissory notes

B)Common shares

C)Executory contracts

D)Executed contracts

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

61

Under ASPE, forfeitures which occur under a stock-based compensation structure are accrued throughout the vesting period.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

62

General debt carries a firm commitment to interest payments and repayment of capital at maturity.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

63

To be classified as retractable preferred shares, the cash repayment must either be contractually required or at the option of the investor.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

64

Under IFRS, forfeitures which occur under a stock-based compensation structure are accrued throughout the vesting period.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

65

Assume that a company wishes to grant stock options to a supplier in exchange for services rendered.The company chose to value this exchange at the going market rate charged by the suppliers' competitors.This is an example of a Level 2 Fair Value Hierarchy application.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

66

Share-based payments to suppliers are valued at the value of the goods or services received.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

67

Perpetual debt is valued as debt because it has no equity component.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

68

Embedded derivatives are those that can be detached and separately sold from their host contracts.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

69

When stock rights are issued to current shareholders, it may require more than one such right to later acquire one additional share of the stock covered by the rights.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

70

Retractable preferred shares are those which can be redeemed only at the investor's discretion.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

71

When bonds are converted, it is first necessary to update any accounts relating to bond premium or discount, accrued interest, and foreign exchange gains and losses on foreign currency denominated debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

72

An instrument may be classified as equity even though the investor can demand payment.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

73

Futures contracts are traded on public exchanges while forward contracts are not.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

74

Convertible bonds with a floating conversion price is treated solely as debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

75

Management of a company that has convertible bonds outstanding would likely force conversion of its bonds of the fair market value of the shares upon conversion exceeds the fair value of the bonds.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

76

When a bond matures, an investor will convert if the market price of the convertible bond is higher than the conversion price of the bond.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

77

If cash payments to investors are dependent on one or more future events, the instrument in question would be considered equity.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

78

The proceeds of any bonds sold with detachable stock warrants must be pro-rated between the bonds and the warrants.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

79

The measurement date of a compensatory stock option must precede the date of grant.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

80

An escalation clause will normally cause preferred shares to trade as debt.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 135 flashcards in this deck.