Deck 12: Financial Liabilities and Provisions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Jake Co.includes three coupons in each bag of dog food it sells.In return for fifteen coupons, customers receive a dog leash.The leashes cost Jones $2.00 each.Jake estimate that 50% of the coupons will be redeemed.Data for 2014 and 2015 are as follows:  The estimated liability for premiums for Jake Co.as at December 31, 2015 is:

The estimated liability for premiums for Jake Co.as at December 31, 2015 is:

A)$50,000.

B)$160,000.

C)$20,000.

D)$80,000.

The estimated liability for premiums for Jake Co.as at December 31, 2015 is:A)$50,000.

B)$160,000.

C)$20,000.

D)$80,000.

Question

Question

Question

Question

Question

Question

Question

Question

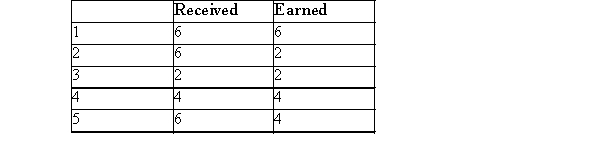

You are an investor and have just purchased a bond on July 1 which pays interest every March 1 and September 1.When you receive your first interest cheque, you will receive and have earned how many months interest?

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

E)Choice 5

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

E)Choice 5

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

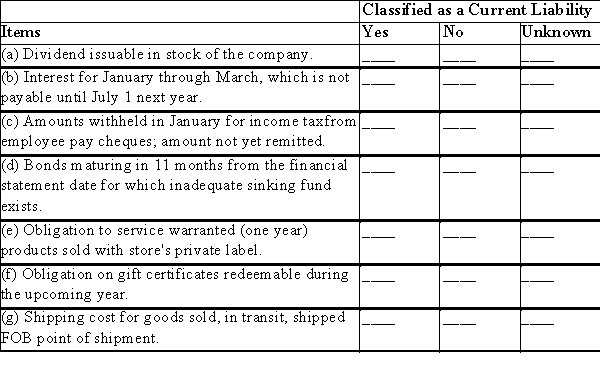

A retail store has completed certain transactions that management believes may have caused current liabilities.Indicate by check mark whether the following items should be classified as current liabilities.Assume a December 31 year-end.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/78

Play

Full screen (f)

Deck 12: Financial Liabilities and Provisions

1

Contingent liabilities will or will not become actual liabilities depending on:

A)Whether they are probable and estimable

B)The outcome of a future event

C)The present condition suggesting a liability

D)The degree of uncertainty

A)Whether they are probable and estimable

B)The outcome of a future event

C)The present condition suggesting a liability

D)The degree of uncertainty

B

2

On November 7, 2014 local residents sued Brimley Corporation for excess chemical emissions that caused some of them to seek medical attention.The total lawsuit is $8,000,000.Brimley Corporation's lawyers believe that the lawsuit will be successful and that the amount to be paid to the residents will be $4,000,000.On its December 31, 2014 financial statements Brimley should:

A)Accrue a provision loss of $4,000,000 and note disclose.

B)Do nothing as the lawsuit has not yet ended.

C)Simply disclose the details regarding the lawsuit in a note.

D)Accrue a provision loss of $8,000,000 with no financial statement disclosure necessary.

A)Accrue a provision loss of $4,000,000 and note disclose.

B)Do nothing as the lawsuit has not yet ended.

C)Simply disclose the details regarding the lawsuit in a note.

D)Accrue a provision loss of $8,000,000 with no financial statement disclosure necessary.

A

3

On January 1, 2014, JG purchased a machine and gave a $30,000 three-year, 8% note.The market or "going" interest rate was 12%.The annual interest payments are to be paid on each December 31.On January 1, 2014, JG should record the net liability amount determined as follows:

A)Use its face amount, $30,000 minus $7,200 interest.

B)Compute the present value of its face amount and the three $2,400 interest amounts by using a discount rate of 8%.

C)Use its face amount, $30,000 plus the $7,200 interest.

D)Compute the present value of its face amount and the three $2,400 interest amounts by using a discount rate of 12%.

A)Use its face amount, $30,000 minus $7,200 interest.

B)Compute the present value of its face amount and the three $2,400 interest amounts by using a discount rate of 8%.

C)Use its face amount, $30,000 plus the $7,200 interest.

D)Compute the present value of its face amount and the three $2,400 interest amounts by using a discount rate of 12%.

D

4

Long-term obligations (i.e., debts)that is callable for early payment:

A)Must be reported as current liabilities by the debtor if callable on demand.

B)Must continue to be classified as a long-term liability in all situations.

C)Can be reported as current liabilities by the debtor only if callable because a provision of the debt covenant has been violated.

D)Must continue to be classified as a long-term liability by the debtor, if a provision of the debt covenant has been violated.

A)Must be reported as current liabilities by the debtor if callable on demand.

B)Must continue to be classified as a long-term liability in all situations.

C)Can be reported as current liabilities by the debtor only if callable because a provision of the debt covenant has been violated.

D)Must continue to be classified as a long-term liability by the debtor, if a provision of the debt covenant has been violated.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

5

Ryan Company borrow $45,000 US when the exchange rate for US $1.00 is Cdn.$1.46.When the debt was repaid the exchange rate changes to US $1.00 = Cdn.$1.38.Ryan Company records the amount on the date of exchange as:

A)A foreign exchange gain of $3,600.

B)A foreign exchange gain of $62,100.

C)A foreign exchange loss of $3,600.

D)A foreign exchange loss of $62,100.

A)A foreign exchange gain of $3,600.

B)A foreign exchange gain of $62,100.

C)A foreign exchange loss of $3,600.

D)A foreign exchange loss of $62,100.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

6

Information obtained prior to the issuance of the current period's financial statements of KG Company indicates that it is probable that, at the date of the financial statements, a liability will be incurred for obligations related to product warranties on products sold during the current period.During the past three years, product warranty costs have been approximately 1 1/2 percent of annual sales revenue.An estimated loss contingency should be:

A)Neither accrued nor disclosed in the financial statements.

B)Accrued in the accounts and reported in the financial statements.

C)Disclosed in the financial statements but not accrued.

D)Recognized as an appropriation of retained earnings.

A)Neither accrued nor disclosed in the financial statements.

B)Accrued in the accounts and reported in the financial statements.

C)Disclosed in the financial statements but not accrued.

D)Recognized as an appropriation of retained earnings.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

7

A firm sells products covered by a three-year warranty.From the past experience of the other firms in the industry, the firm expects to incur warranty costs equal to 1% of sales.Firm sales were $40,000 and $50,000 in 2013 and 2014 respectively.In 2014, the firm spent $200 to repair goods sold in 2013, and $300 to repair goods sold in 2014.The firm received no warranty servicing demands from customers in 2013, the firm's first year of operations.What is the balance in the warranty liability account on January 1, 2014?

A)$300

B)$0

C)$500

D)$400

A)$300

B)$0

C)$500

D)$400

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

8

Under IFRS, which of the following will only require only a note disclosure as a contingency?

A)Remote chance of loss from a lawsuit in process

B)Loss from an investment in equity securities that is certain

C)Cash discounts given for early payment by customers; almost always taken

D)Probable claim for an income tax refund

A)Remote chance of loss from a lawsuit in process

B)Loss from an investment in equity securities that is certain

C)Cash discounts given for early payment by customers; almost always taken

D)Probable claim for an income tax refund

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

9

A company had sales of $1 million.Coupons in the amount of $1 per $10 in sales were given to paying customers.History has shown that 50% of all coupons are redeemed.Which of the following statements is correct?

A)No provision is necessary.

B)A provision for $100,000 must be recognized.

C)A provision for $1 million must be recognized.

D)A provision for $50,000 must be recognized.

A)No provision is necessary.

B)A provision for $100,000 must be recognized.

C)A provision for $1 million must be recognized.

D)A provision for $50,000 must be recognized.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

10

KR Corporation was involved in a lawsuit with the Government alleging inadequate air pollution control facilities at its Glowworm plant site during 2013.At December 31, 2016, it appeared probable the Government would settle for approximately $150,000.This event should be recorded (i.e., recognized)in 2016 as a(n):

A)Unusual loss.

B)Loss on the lawsuit (operating expense).

C)Prior period adjustment.

D)Disclosure of contingency loss only in a note.

E)Unusual gain.

A)Unusual loss.

B)Loss on the lawsuit (operating expense).

C)Prior period adjustment.

D)Disclosure of contingency loss only in a note.

E)Unusual gain.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

11

A company has commenced work on a non-cancellable fixed price construction contract in the amount of $6 million.Costs of $4 million have been incurred to date, and it is expected that $3.2 million in additional costs will have to be incurred to complete the contract.The company adheres to IFRS.Which of the following statements with respect to the contract are correct?

A)The company has a constructive obligation to accrue a loss of $1.2 million plus any previously recognized profit.

B)This is an onerous contract, so the company must accrue a loss of $1.2 million plus any previously recognized profit.

C)There is a constructive obligation to finish the contract.

D)The company will have recognized $3 million in profit on the contract to date.

A)The company has a constructive obligation to accrue a loss of $1.2 million plus any previously recognized profit.

B)This is an onerous contract, so the company must accrue a loss of $1.2 million plus any previously recognized profit.

C)There is a constructive obligation to finish the contract.

D)The company will have recognized $3 million in profit on the contract to date.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

12

On January 1, 2014, DWW borrowed $400,000 cash and signed a one-year, 12 percent interest-bearing note payable.Assuming a 40 percent average income tax rate for DWW Corporation, the net effective interest rate on this note was:

A)7)2 percent.

B)12.0 percent.

C)4)8 percent.

D)6)0 percent.

A)7)2 percent.

B)12.0 percent.

C)4)8 percent.

D)6)0 percent.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following contingencies should be accrued in the accounts and reported in the financial statements?

A)The estimated expenses of a one-year product warranty.

B)An accommodation endorsement involving a remote loss.

C)The company is forcefully contesting a personal injury suit and a loss is possible and reasonably estimable.

D)It is probable that the company will receive $50,000 in settlement of a lawsuit.

A)The estimated expenses of a one-year product warranty.

B)An accommodation endorsement involving a remote loss.

C)The company is forcefully contesting a personal injury suit and a loss is possible and reasonably estimable.

D)It is probable that the company will receive $50,000 in settlement of a lawsuit.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

14

VCR Company owed a $73,311 debt due on January 1, 2012.An agreement was reached to pay it off in three equal annual payments of $30,000 each, starting on December 31, 2012.The interest rate was 11 percent.The balance in the liability account of VCR Company on January 1, 2014 is (round annual payment to nearest $1):

A)$90,000

B)$27,026

C)$73,311

D)$51,875

A)$90,000

B)$27,026

C)$73,311

D)$51,875

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements is correct?

A)Under IFRS, content gains should be recognized if they are reasonably certain to occur.

B)A contingency is more likely to require an accrual than a provision.

C)Under IFRS, contingencies may be accrued, but not under ASPE.

D)Litigation for which the company will probably be found guilty would normally be accrued as a provision.

A)Under IFRS, content gains should be recognized if they are reasonably certain to occur.

B)A contingency is more likely to require an accrual than a provision.

C)Under IFRS, contingencies may be accrued, but not under ASPE.

D)Litigation for which the company will probably be found guilty would normally be accrued as a provision.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

16

XYZ borrowed $60,000 for one year and signed an 18 percent, interest-bearing note payable.Assuming XYZ has an income tax rate of 45 percent, the net effective rate was:

A)8)1 percent.

B)9)9 percent.

C)18 percent.

D)11.7 percent.

A)8)1 percent.

B)9)9 percent.

C)18 percent.

D)11.7 percent.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

17

Jake Co.includes three coupons in each bag of dog food it sells.In return for fifteen coupons, customers receive a dog leash.The leashes cost Jones $2.00 each.Jake estimate that 50% of the coupons will be redeemed.Data for 2014 and 2015 are as follows: The estimated liability for premiums for Jake Co.as at December 31, 2015 is:

A)$50,000.

B)$160,000.

C)$20,000.

D)$80,000.

The estimated liability for premiums for Jake Co.as at December 31, 2015 is:A)$50,000.

B)$160,000.

C)$20,000.

D)$80,000.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

18

A firm sold $100,000 worth of goods during 2014.The firm extends warranty coverage on these goods.Historically, warranty costs have averaged 2% of total sales.During 2014, the firm incurred $1,000 to service goods sold in 2013 and $200 to service goods sold in 2014.What is warranty expense for 2014?

A)$1,200

B)$3,200

C)$2,000

D)$200

A)$1,200

B)$3,200

C)$2,000

D)$200

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

19

A brewing company operating in an Ontario city experiencing water shortages received its water bill for December 2013, on December 31, 2013.The bill ($8,000)represents the cost of water used in December to make its product.The company will not publish the 2013 financial statements until February 2014.Therefore, the adjusting entry as of December 31, 2013 includes which of the following?

A)cr.utilities expense $8,000

B)cr.cash $8,000

C)cr.utilities payable $8,000

D)no adjusting entry needed because the bill will not be paid until January 2014

A)cr.utilities expense $8,000

B)cr.cash $8,000

C)cr.utilities payable $8,000

D)no adjusting entry needed because the bill will not be paid until January 2014

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

20

XY Company owed a $45,489 due on January 1, 2015.An agreement was reached to pay it off in five equal annual payments, starting on December 31, 2015.The interest rate was 10 percent.The total amount of interest paid under the terms of the agreement was (round annual payment to nearest $1):

A)$14,511

B)$6,000

C)$25,000

D)$22,745

A)$14,511

B)$6,000

C)$25,000

D)$22,745

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

21

For a large population, the best estimate for the amount of a provision that must be recognized is the most likely outcome with respect to the expected value and cumulative probabilities.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

22

Self-insurance costs for expected losses must never be provided for.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

23

On September 1, 2012, Company B signed a $7,392, two-year non-interest-bearing note payable in full on August 31, 2014.Company B received $6,000 cash.What was the yield or effective rate of interest?

A)11 percent

B)18 percent

C)23 percent

D)14 percent

A)11 percent

B)18 percent

C)23 percent

D)14 percent

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

24

A lawsuit in progress wherein the defendant will probably be found guilty would likely be accounted for as a provision.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

25

You are an investor and have just purchased a bond on July 1 which pays interest every March 1 and September 1.When you receive your first interest cheque, you will receive and have earned how many months interest?

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

E)Choice 5

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

E)Choice 5

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

26

Under ASPE, only legal obligations are recognized.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following statements is correct?

A)Contingent assets are only recorded when it is virtually certain that the benefits relating to the contingent assets will be received.

B)There is no guidance for self-insurance under IFRS.

C)Contingent assets are only recorded when it is reasonably certain that the benefits relating to the contingent assets will be received.

D)For companies that are self-insured, a provision must be established for events taking place prior to the reporting period if known.

A)Contingent assets are only recorded when it is virtually certain that the benefits relating to the contingent assets will be received.

B)There is no guidance for self-insurance under IFRS.

C)Contingent assets are only recorded when it is reasonably certain that the benefits relating to the contingent assets will be received.

D)For companies that are self-insured, a provision must be established for events taking place prior to the reporting period if known.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

28

A short-term note payable may include all of the following except:

A)A current portion of a long-term liability.

B)Unearned revenue.

C)Trade notes payable.

D)Non trade notes payable.

A)A current portion of a long-term liability.

B)Unearned revenue.

C)Trade notes payable.

D)Non trade notes payable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

29

Constructive obligations may arise from:

A)Unearned Revenues.

B)Warranty obligations.

C)Accrued Liabilities resulting from operations.

D)Notes Payable.

A)Unearned Revenues.

B)Warranty obligations.

C)Accrued Liabilities resulting from operations.

D)Notes Payable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

30

Under ASPE, disclosure in the footnotes to the financial statements is the only way to properly report contingent losses.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

31

Under ASPE, contingent liabilities which are more likely than not, are accrued at the lowest end of the range.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

32

Which one of the following items is not a liability?

A)The portion of long-term debt due within one year

B)Advances from customers on contracts

C)Accrued estimated warranty costs

D)Dividends payable in shares

A)The portion of long-term debt due within one year

B)Advances from customers on contracts

C)Accrued estimated warranty costs

D)Dividends payable in shares

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

33

Contingent assets may be recorded under ASPE but not under IFRS.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

34

A decline in value of a company's reporting currency relative to the foreign currency in which it has payables will result in a foreign exchange gain on the reporting company's books.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

35

ABC Inc.has 50 pending lawsuits for which it may be found liable.The expected value (sum of the probabilities of the outcomes multiplied by their respective payouts)amounts to $100,000.However, the company's controller believes that the most likely outcome will be a payout of $120,000.Which of the following statements pertaining to the accrual of the provision is correct?

A)There is a small population of lawsuits, so a provision of $100,000 must be accrued.

B)There is a large population of lawsuits, so a provision of $100,000 must be accrued.

C)There is a large population of lawsuits, so a provision of $120,000 must be accrued.

D)There is a small population of lawsuits, so a provision of $120,000 must be accrued.

A)There is a small population of lawsuits, so a provision of $100,000 must be accrued.

B)There is a large population of lawsuits, so a provision of $100,000 must be accrued.

C)There is a large population of lawsuits, so a provision of $120,000 must be accrued.

D)There is a small population of lawsuits, so a provision of $120,000 must be accrued.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

36

A contingency may become a provision if the likelihood of the contingent event greatly increases.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

37

Normal business risks that are insured must be provided for.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

38

By law, a fleet of aircraft must be subject to a major overhaul every 5 years as part of its scheduled maintenance program.Which of the following statements is correct?

A)The estimated cost of the overhaul should be disclosed as part of a continuity schedule in the notes to the financial statements.

B)The cost of the overhaul should be deferred and amortized.

C)The costs of the overhaul should be expensed as incurred.

D)An accrual should be made in each of the 5 years preceding the overhaul.

A)The estimated cost of the overhaul should be disclosed as part of a continuity schedule in the notes to the financial statements.

B)The cost of the overhaul should be deferred and amortized.

C)The costs of the overhaul should be expensed as incurred.

D)An accrual should be made in each of the 5 years preceding the overhaul.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

39

Under IFRS, a loss contingency must be credited to a liability account only if the occurrence of the contingent event is probable and if the amount of loss can be reasonably estimated.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

40

An administrative fee pertaining to an unsuccessful loan application is to be immediately expensed.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

41

For a small population, the best estimate for the amount of a provision that must be recognized is the expected value of the possible outcomes.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

42

Once a company has formally decided to restructure its operations, a provision must be made for the restructuring.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

43

Under IFRS, most financial liabilities are valued at Fair Value.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

44

Warranties provisions may arise from legal or constructive obligations.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

45

A reasonable expectation on the part of a company's stakeholders arising from a company's past practices or behaviour may constitute a constructive obligation in certain instances.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

46

Executory contracts seldom require a journal entry, while onerous contracts do.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

47

Capitalization of borrowing costs on qualifying assets will continue even if work on the asset has temporarily ceased.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

48

Current liabilities are usually discounted.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

49

Loan guarantees must be provided for; the amount of the provision is the probability of payout multiplied by the fair value of the loan guarantee.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

50

An improvement to a company's credit rating under IFRS will lead to a reduction in the carrying amount of any financial liabilities and a gain being reported in OCI.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

51

Under the warranty expense approach, there should be no income statement effects for warranty repairs performed after the year of sale (assuming that accrued warranty expenses and expenditures equal one another).

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

52

Accounts payable should include only obligations directly related to the primary and continuing operations of an entity.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

53

Loan guarantees are only recorded if they are likely to be paid.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

54

An onerous contract is one where the unavoidable costs of meeting the contract may or may not exceed the benefits derived from the contract.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

55

Debt issue costs may be expensed or included in the cost of the debt.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

56

A company may reclassify a current financial liability to a long-term one only if there is a contractual agreement in place by the reporting date to replace the financing.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

57

Accrued liabilities made due to routine operating expenses are not normally discounted.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

58

Under IFRS, provisions are always recorded at their expected value.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

59

A company decides to relocate a group from a discontinued business segment to a division with ongoing operations.The expenses incurred in doing so would qualify as a restructuring charge.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

60

A gain contingency will usually not be recorded in the accounts and reported in the financial statements even though its occurrence is probable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

61

On September 1, 2014, XYZ borrowed $100,000 on a 9%, two-year, note payable.Simple interest is payable on August 31, 2015 and 2016.XYZ's reporting year ends December 31 and the company does not use reversing entries for interest.The required entry on August 31, 2001, is:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

62

On September 1, 2020, a company purchased a machine and paid for it by signing a two-year noninterest-bearing note, face $4,000.The note is payable August 31, 2022.The going rate of interes was 18% per year.The accounting period ends December 31.

(a)Compute the cost of the machine.

(b)Give all appropriate entries throughout the term of the note.

Use the net method.

(a)Compute the cost of the machine.

(b)Give all appropriate entries throughout the term of the note.

Use the net method.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

63

Under IFRS, a continuity schedule must be provided for both provisions and contingencies.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

64

Quality 9000 International Inc., which began operations in 1996, sells 20,000 units of its product each year under the following warranty: defective units will be fixed free of charge during the calendar year of purchase and the next two calendar years.(This means it is best to buy from this company early in the year.)Only 1% of units sold have required warranty service in the past.The average cost has been $200 per unit for servicing.Units require service only once and the likelihood of a unit requiring service is the same during each year in the warranty period.What is the balance in the warranty liability account at December 31, 1999?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

65

A retail store has completed certain transactions that management believes may have caused current liabilities.Indicate by check mark whether the following items should be classified as current liabilities.Assume a December 31 year-end.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

66

Under the warranty revenue approach, there should be no income statement effects for warranty repairs performed after the year of sale (assuming that accrued warranty expenses and expenditures equal one another).

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

67

Loyalty points are provided (accrued)for and reversed once the points are redeemed.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

68

A company has been sued for damages as a result of illness caused to local residents due to the emission of highly toxic chemicals from its plant.The company's legal firm advises that it is probable that the company will lose the suit and that it probably will result in a judgment of $2 million to $10 million in damages.However, the legal firm believes that the most probable amount o the loss will be $6 million, and that the suit will be terminated about three years hence.The company has no other lawsuits pending.

(a)Should the company disclose this event in the year the suit was filed? (check one)No;

________ Note only; A loss in the income statement.

(b)If a loss should be reported, give the journal entry required:

(a)Should the company disclose this event in the year the suit was filed? (check one)No;

________ Note only; A loss in the income statement.

(b)If a loss should be reported, give the journal entry required:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

69

Financial liabilities are initially recognized at fair value and at cost, amortized cost or fair value post-acquisition.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

70

BRIEFLY explain how the treatment of contingencies differs under IFRS and ASPE.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

71

Conceptually, liabilities constitute a present obligation as a result of a past event and entail an expected future sacrifice of assets or services.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

72

Capitalization of borrowing costs on qualifying assets is mandatory under both IFRS and ASPE.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

73

On September 1, 2020, a company signed a $6,540, one-year, non-interest-bearing note payable and received $6,000 cash.

(a)What was the imputed rate of interest? %.

(b)Give the entry required at September 1, 2020, to record the receipt of the cash (record on net basis).

(c)Give the adjusting entry required at the end of the accounting year, December 31, 2020.

(d)Give the entry required on the due date, August 31, 2021, assuming no reversing entries were made.

(a)What was the imputed rate of interest? %.

(b)Give the entry required at September 1, 2020, to record the receipt of the cash (record on net basis).

(c)Give the adjusting entry required at the end of the accounting year, December 31, 2020.

(d)Give the entry required on the due date, August 31, 2021, assuming no reversing entries were made.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

74

On January 1, 2012, a company purchased a machine that had a list price of $23,500.The purchase terms agreed upon were: cash down payment $12,000 plus a 15% note payable of $9,132 (its present value).The note is payable in three equal annual instalments (interest plus principal)on each December 31.Round to the nearest dollar.

Required:

(a)Give the entry to record the acquisition of the machine.

(b)Give the adjusting entry required on September 30, 2014, for interest assuming this is the end of the accounting period.

Required:

(a)Give the entry to record the acquisition of the machine.

(b)Give the adjusting entry required on September 30, 2014, for interest assuming this is the end of the accounting period.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

75

Discounting is not required when the time value of money is immaterial or if the amount and timing of cash flows is highly uncertain.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

76

Adjustments to fair value relating to FVTPL liabilities will always flow through earnings.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

77

On January 1, 2000, a corporation purchased a machine (10 year estimated useful life; no residual value; straight-line method)by paying cash $1,500 and signing a note payable with a face amount of

$4,500, 8% interest payable each December 31.The maturity date is December 31, 2002.The going market rate of interest was 10%.Give all required entry (entries)at each of the following dates:

January 1, 2000:

December 31, 2000:

$4,500, 8% interest payable each December 31.The maturity date is December 31, 2002.The going market rate of interest was 10%.Give all required entry (entries)at each of the following dates:

January 1, 2000:

December 31, 2000:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

78

At December 31, 2015, ABC Company has the following three separate lawsuits pending against it: Suit A-Plaintiffs seek damages of $40,000; Suit B-Plaintiff seeks damages of $200,000; and Suit

C-Plaintiff seeks damages of $20,000.

ABC management and legal counsel have made the assessments indicated below.For each suit, taking into account the assessment, you are to (a)give the accrual entry if it is required (if not, state why)and (b)indicate whether a disclosure note is required and explain the reason.

CASE A-Remote that ABC will lose the suit.

(a)Accrual entry:

(b)Disclosure note Yes

________No.

C-Plaintiff seeks damages of $20,000.

ABC management and legal counsel have made the assessments indicated below.For each suit, taking into account the assessment, you are to (a)give the accrual entry if it is required (if not, state why)and (b)indicate whether a disclosure note is required and explain the reason.

CASE A-Remote that ABC will lose the suit.

(a)Accrual entry:

(b)Disclosure note Yes

________No.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 78 flashcards in this deck.