Deck 18: Investments

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on July 1, 2014, is

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on July 1, 2014, is

Question

Question

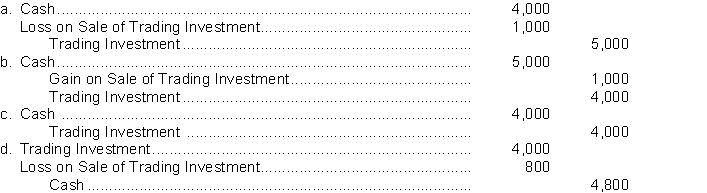

Chan Corporation sells 100 common shares being held as a trading investment. The shares were acquired six months ago at a cost of $50 a share Chan sold the shares for $40 a share. The entry to record the sale is:

Question

Use the following information for questions 56-57.

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

At the end of the year, Fanning Corporation normally would

A) make no entry.

B) increase trading investments to market value.

C) report an loss on the income statement for $3,000 under "Other Expenses".

D) report an loss on the income statement for $1,000 under "Other Expenses".

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

At the end of the year, Fanning Corporation normally would

A) make no entry.

B) increase trading investments to market value.

C) report an loss on the income statement for $3,000 under "Other Expenses".

D) report an loss on the income statement for $1,000 under "Other Expenses".

Question

Question

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The adjusting entry on December 31, 2014, is

A) not required.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The adjusting entry on December 31, 2014, is

A) not required.

Question

Question

Question

Question

Question

Use the following information for questions 56-57.

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

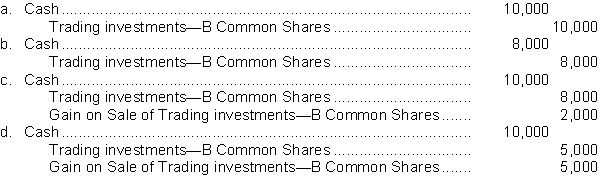

Fanning subsequently sells B common shares for $10,000. What entry is made to record the sale?

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

Fanning subsequently sells B common shares for $10,000. What entry is made to record the sale?

Question

Question

Question

Question

Question

Question

Match between columns

Premises:

Bonds

Bonds

60% of the common shares of the investee

60% of the common shares of the investee

Responses:

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

Question

Question

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on January 1, 2015, is

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on January 1, 2015, is

Question

Question

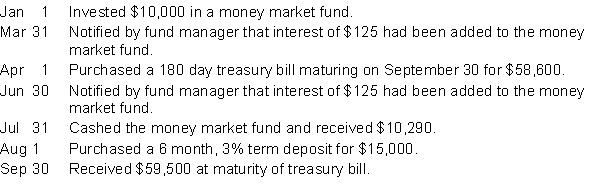

Anil Denim Products had the following transactions during the year ended December 31, 2014. The debt investments were purchased to earn interest income.  Instructions

Instructions

Record the transactions and prepare any December 31, 2014 adjusting entries.

InstructionsRecord the transactions and prepare any December 31, 2014 adjusting entries.

Question

On January 5, 2013, Barker Limited purchased the following securities as trading investments:

300 McRae Corporation common shares for $4,200

500 Gupta Corporation common shares for $10,000

600 May Corporation common shares for $19,800

On June 30, 2013, Barker received the following cash dividends: On November 15, 2013, Barker sold 100 May Corporation common shares for $4,000.

On November 15, 2013, Barker sold 100 May Corporation common shares for $4,000.

On December 31, 2013, the market value of the securities held by Barker is as follows: Instructions

Instructions

Prepare the appropriate journal entries that Barker Limited should make on the following dates: January 5, 2013; June 30, 2013; November 15, 2013; and December 31, 2013.

300 McRae Corporation common shares for $4,200

500 Gupta Corporation common shares for $10,000

600 May Corporation common shares for $19,800

On June 30, 2013, Barker received the following cash dividends:

On November 15, 2013, Barker sold 100 May Corporation common shares for $4,000.On December 31, 2013, the market value of the securities held by Barker is as follows:

InstructionsPrepare the appropriate journal entries that Barker Limited should make on the following dates: January 5, 2013; June 30, 2013; November 15, 2013; and December 31, 2013.

Question

Question

Question

Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/68

Play

Full screen (f)

Deck 18: Investments

1

If there is a bond premium, interest revenue is increased by the amortization amount.

False

2

Investments in equity securities bought for the purposes of trading are reported at amortized cost.

False

3

For companies reporting under IFRS, a short-term debt instrument which is held for trading will be valued at fair value on the balance sheet.

True

4

An equity investment which is held for trading will be valued at cost on the balance sheet.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

5

If an investment is valued at an amount that is most relevant to the type of investment, it will allow investors to better predict future cash flows of the company.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

6

A fair value adjustment at the balance sheet date is required only on investments which will be sold within 30 days of the balance sheet date.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

7

When a debt instrument is reported at amortized cost, the interest expense is calculated by multiplying the market rate of interest by the carrying value of the investment.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

8

Companies purchase investments as a strategic investment with the intention of establishing and maintaining a long-term operating relationship with another company.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

9

The purpose of a strategic investment is to generate investment income.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

10

The percentage of ownership or the degree of influence determines how a strategic investment is classified.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

11

If a long-term bond investment is sold before maturity, an entry must be made to update any unrecorded interest and amortization of the discount or premium.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

12

A short-term debt instrument which is held to earn interest will be valued at fair value on the balance sheet.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

13

At acquisition, a debt instrument is recorded at its fair value on the date of purchase.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

14

When investing excess cash for short periods of time, corporations usually invest in shares of other companies.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

15

When a long-term bond investment is sold, a gain will be recorded when amortized cost of the bond is less than the cash received.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

16

Investments which are purchased principally for selling in the near future are called trading investments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

17

Interest revenue is reported under other revenues on the Income statement.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

18

Under IFRS, trading investments are valued at amortized cost on the balance sheet.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

19

If a debt instrument is sold before maturity, then a gain is recorded if the cash received is less than the carrying amount of the instruments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

20

The purchaser of the bonds, or the bondholder, is known as the investor.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

21

Equity instruments held for trading are recorded as

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

22

If the market rate changes after a public company purchases bonds to trade, the bonds carrying amount will not change.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is the most accurate?

A) Non-strategic investments maintain a long-term operating relationship with another company.

B) Non-strategic investments are purchased to generate investment income.

C) Preferred shares and common shares are debt instruments.

D) Strategic investments are always short-term instruments.

A) Non-strategic investments maintain a long-term operating relationship with another company.

B) Non-strategic investments are purchased to generate investment income.

C) Preferred shares and common shares are debt instruments.

D) Strategic investments are always short-term instruments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

24

Excess cash may be invested for the long-term to

A) generate dividend income on bonds.

B) generate interest income on bonds.

C) generate interest income on shares.

D) generate additional operating income.

A) generate dividend income on bonds.

B) generate interest income on bonds.

C) generate interest income on shares.

D) generate additional operating income.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

25

Short- or long-term debt instruments held for trading are recorded as

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

26

Under ASPE, only debt instruments will be reported at fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

27

An investee must record a fair value adjustment on trading investments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is a true statement regarding an investment in short-term debt instruments?

A) The instruments usually do not pay interest.

B) They are often made when the company has surplus cash on hand.

C) This type of investment is never traded in the securities market.

D) A chequing account is a type of short-term debt investment.

A) The instruments usually do not pay interest.

B) They are often made when the company has surplus cash on hand.

C) This type of investment is never traded in the securities market.

D) A chequing account is a type of short-term debt investment.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

29

Debt & Equity securities that are purchased for the purpose of selling in the short-term at a gain are referred to as

A) debt instruments.

B) equity instruments.

C) long-term instruments.

D) trading investments.

A) debt instruments.

B) equity instruments.

C) long-term instruments.

D) trading investments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

30

Under IFRS, trading investments reported at fair value may include investments in common shares, preferred shares, and debt investments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

31

For companies reporting under IFRS, debt instruments purchased to trade are reported on the balance sheet at

A) amortized cost.

B) cost.

C) fair value.

D) lower of cost and market.

A) amortized cost.

B) cost.

C) fair value.

D) lower of cost and market.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

32

Long-term debt instruments held to earn interest income are recorded as

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements is INCORRECT with regards to non-strategic instruments?

A) They can be debt instruments.

B) They maintain an operating relationship with another company.

C) They can be equity instruments.

D) They generate investment income.

A) They can be debt instruments.

B) They maintain an operating relationship with another company.

C) They can be equity instruments.

D) They generate investment income.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following would NOT normally be considered a motive for making an equity investment in another corporation?

A) to invest surplus cash

B) use of the investment for expanding its own operations

C) use of the investment to diversify its own operations

D) an increase in the amount of interest revenue from the equity investment

A) to invest surplus cash

B) use of the investment for expanding its own operations

C) use of the investment to diversify its own operations

D) an increase in the amount of interest revenue from the equity investment

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

35

Short-term debt instruments that are held to earn interest income are recorded as

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

A) current assets at amortized cost.

B) non-current assets at amortized cost.

C) current asset at fair value.

D) non-current assets at fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

36

Companies reporting under IFRS will report all investments in debt instruments at amortized cost.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

37

Short-term and long-term debt instruments purchased to earn interest are reported at

A) cost.

B) unamortized cost.

C) fair value.

D) amortized cost.

A) cost.

B) unamortized cost.

C) fair value.

D) amortized cost.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

38

Dividend revenue is reported under revenues from operations on the Income statement.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

39

All of the following are considered debt instruments EXCEPT

A) term deposits.

B) treasury bills.

C) bonds.

D) preferred shares.

A) term deposits.

B) treasury bills.

C) bonds.

D) preferred shares.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

40

The advantage of using fair value for trading investments is that it allows users to better predict future cash flows.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

41

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on July 1, 2014, is

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on July 1, 2014, is

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

42

Interest income is calculated by multiplying

A) market rate of interest by the face value of the investment.

B) contract rate of interest by the face value of the investment.

C) market rate of interest by the carrying value of the investment.

D) stated interest rate by the carrying value of the investment.

A) market rate of interest by the face value of the investment.

B) contract rate of interest by the face value of the investment.

C) market rate of interest by the carrying value of the investment.

D) stated interest rate by the carrying value of the investment.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

43

Chan Corporation sells 100 common shares being held as a trading investment. The shares were acquired six months ago at a cost of $50 a share Chan sold the shares for $40 a share. The entry to record the sale is:

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

44

Use the following information for questions 56-57.

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

At the end of the year, Fanning Corporation normally would

A) make no entry.

B) increase trading investments to market value.

C) report an loss on the income statement for $3,000 under "Other Expenses".

D) report an loss on the income statement for $1,000 under "Other Expenses".

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

At the end of the year, Fanning Corporation normally would

A) make no entry.

B) increase trading investments to market value.

C) report an loss on the income statement for $3,000 under "Other Expenses".

D) report an loss on the income statement for $1,000 under "Other Expenses".

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is a true statement about the accounting for trading investments under IFRS?

A) The investment is initially recorded at fair value.

B) Gains and losses are recorded in OCI when the market value is different from the purchase price.

C) The accounting for trading investments is the same as the accounting for short-term investments in debt instruments purchased to earn interest.

D) The investment is initially recorded at face value.

A) The investment is initially recorded at fair value.

B) Gains and losses are recorded in OCI when the market value is different from the purchase price.

C) The accounting for trading investments is the same as the accounting for short-term investments in debt instruments purchased to earn interest.

D) The investment is initially recorded at face value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

46

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The adjusting entry on December 31, 2014, is

A) not required.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The adjusting entry on December 31, 2014, is

A) not required.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements is correct?

A) A debt instrument purchased to earn interest will be valued at fair value.

B) A debt instrument which is purchased to earn interest will be valued at amortized cost.

C) Gains or losses on trading investments are not recorded until the trading investments are sold and the gains or losses are realized.

D) All gains and losses on fair value adjustment arising from trading investments are charged to operating income.

A) A debt instrument purchased to earn interest will be valued at fair value.

B) A debt instrument which is purchased to earn interest will be valued at amortized cost.

C) Gains or losses on trading investments are not recorded until the trading investments are sold and the gains or losses are realized.

D) All gains and losses on fair value adjustment arising from trading investments are charged to operating income.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

48

Companies make strategic investments for several reasons. Which of the following reasons is INCORRECT?

A) to speculate that their investment will increase in value and result in a gain when it is sold

B) to become a part of a different industry

C) to expand operations

D) to eliminate competition

A) to speculate that their investment will increase in value and result in a gain when it is sold

B) to become a part of a different industry

C) to expand operations

D) to eliminate competition

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

49

If a bond is sold at a price which is greater than the amortized cost of the bond

A) a loss is reported in balance sheet.

B) a gain is reported in balance sheet.

C) a gain is reported on the income statement.

D) a loss is reported on the income statement.

A) a loss is reported in balance sheet.

B) a gain is reported in balance sheet.

C) a gain is reported on the income statement.

D) a loss is reported on the income statement.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

50

Trading investments in equity instruments are reported on the balance sheet at

A) amortized cost.

B) cost.

C) fair value.

D) lower of cost and fair value.

A) amortized cost.

B) cost.

C) fair value.

D) lower of cost and fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

51

Use the following information for questions 56-57.

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

Fanning subsequently sells B common shares for $10,000. What entry is made to record the sale?

At the end of Fanning Corporation's fiscal year, its portfolio of trading investments purchased during the year is as follows:

Fanning subsequently sells B common shares for $10,000. What entry is made to record the sale?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

52

Losses and gains on the sale of instruments are reported on

A) the income statement under current operations.

B) the balance sheet with long-term investments.

C) the income statement under other revenue and expenses.

D) the balance sheet with short-term investments.

A) the income statement under current operations.

B) the balance sheet with long-term investments.

C) the income statement under other revenue and expenses.

D) the balance sheet with short-term investments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

53

Regardless of the bonds purchase price, their amortized cost at maturity will equal

A) face value.

B) face value less premium amounts.

C) purchase price.

D) face value plus discount amounts.

A) face value.

B) face value less premium amounts.

C) purchase price.

D) face value plus discount amounts.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

54

Instruments that will mature within 12 months of the balance sheet date are

A) long-term debt instruments.

B) fair value instruments.

C) short-term debt instruments.

D) unamortized instruments.

A) long-term debt instruments.

B) fair value instruments.

C) short-term debt instruments.

D) unamortized instruments.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

55

If the cost of a trading investment exceeds its fair value by $40,000, the entry to recognize the loss

A) is not required since the share prices will likely rebound in the long run.

B) will show a debit to an expense account in the operating section of the income statement.

C) will show a credit to a contra-asset account that appears in the shareholders' equity section of the balance sheet.

D) will show a debit to an loss account that appears in the other expenses section of the income statement.

A) is not required since the share prices will likely rebound in the long run.

B) will show a debit to an expense account in the operating section of the income statement.

C) will show a credit to a contra-asset account that appears in the shareholders' equity section of the balance sheet.

D) will show a debit to an loss account that appears in the other expenses section of the income statement.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

56

Any premium or discount on an investment in bonds to earn interest is amortized

A) to interest expense over the remaining term of the bonds.

B) only if the effective-interest method is used.

C) to interest revenue over the remaining term of the bonds.

D) only if the investor owns 20% or more of the bonds.

A) to interest expense over the remaining term of the bonds.

B) only if the effective-interest method is used.

C) to interest revenue over the remaining term of the bonds.

D) only if the investor owns 20% or more of the bonds.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

57

Match between columns

Premises:

Bonds

Bonds

60% of the common shares of the investee

60% of the common shares of the investee

Responses:

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

non-strategic investment

strategic investment

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

58

In recognizing a decline in the market value of a trading investment, Loss on Fair value adjustment account is debited

A) because management intends to realize this loss in the near future.

B) to reflect the fair value of the investment on the balance sheet.

C) because the company is no longer a going concern.

D) because there is a permanent decline in the fair value.

A) because management intends to realize this loss in the near future.

B) to reflect the fair value of the investment on the balance sheet.

C) because the company is no longer a going concern.

D) because there is a permanent decline in the fair value.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

59

Use the following information for questions 42-44.

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on January 1, 2015, is

On January 1, 2014, Connors Landscaping Ltd. purchased at face value, a $1,000, 5%, bond that pays interest on January 1 and July 1. Connors has a calendar year end.

The entry for the receipt of interest on January 1, 2015, is

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

60

Nickel District Company purchased the following instruments during the year. Assume the company's fiscal year end is January 31, 2015.

Dec 1 2014 Purchased a $5,000 120 day treasury bill for $4,935. The treasury bills are trading at a market rate of interest of 4% annually.

Feb 1, 2015 Purchased at 101 a $15,000, 5% 5 year Laurentian Bond. Interest is paid semi-annually. The market rate of interest was 3.5%. The bonds were purchased to trade.

Mar 30, 2015 Treasury bill matured.

Aug 1, 2015 Received interest on the Laurentian Bond.

Aug 2, 2015 Sold the Laurentian Bonds at 99.

Instructions

Record the above transactions and any necessary adjusting entries for Nickel District required at January 31, 2015.

Dec 1 2014 Purchased a $5,000 120 day treasury bill for $4,935. The treasury bills are trading at a market rate of interest of 4% annually.

Feb 1, 2015 Purchased at 101 a $15,000, 5% 5 year Laurentian Bond. Interest is paid semi-annually. The market rate of interest was 3.5%. The bonds were purchased to trade.

Mar 30, 2015 Treasury bill matured.

Aug 1, 2015 Received interest on the Laurentian Bond.

Aug 2, 2015 Sold the Laurentian Bonds at 99.

Instructions

Record the above transactions and any necessary adjusting entries for Nickel District required at January 31, 2015.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

61

Anil Denim Products had the following transactions during the year ended December 31, 2014. The debt investments were purchased to earn interest income. Instructions

Record the transactions and prepare any December 31, 2014 adjusting entries.

InstructionsRecord the transactions and prepare any December 31, 2014 adjusting entries.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

62

On January 5, 2013, Barker Limited purchased the following securities as trading investments:

300 McRae Corporation common shares for $4,200

500 Gupta Corporation common shares for $10,000

600 May Corporation common shares for $19,800

On June 30, 2013, Barker received the following cash dividends: On November 15, 2013, Barker sold 100 May Corporation common shares for $4,000.

On December 31, 2013, the market value of the securities held by Barker is as follows: Instructions

Prepare the appropriate journal entries that Barker Limited should make on the following dates: January 5, 2013; June 30, 2013; November 15, 2013; and December 31, 2013.

300 McRae Corporation common shares for $4,200

500 Gupta Corporation common shares for $10,000

600 May Corporation common shares for $19,800

On June 30, 2013, Barker received the following cash dividends:

On November 15, 2013, Barker sold 100 May Corporation common shares for $4,000.On December 31, 2013, the market value of the securities held by Barker is as follows:

InstructionsPrepare the appropriate journal entries that Barker Limited should make on the following dates: January 5, 2013; June 30, 2013; November 15, 2013; and December 31, 2013.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

63

The following is information about O'Hara Corporation's, a public company, trading investments. O'Hara has a September 30 year end.

Sep 1: On hand:

$50,000, 5% FMC Co. bond, purchased previously by O'Hara at 101. Interest on the bond is payable semi-annually on January 1 and July 1.

$100,000 3% Government of Canada bond, previously purchased by O'Hara at 98. Interest on the bond is payable semi-annually on March 31, and September 30.

Sep 1: Purchased $40,000 4% Alpha Inc. bond at 99. Interest is payable annually on August 31.

Sep 30: Received interest on Government of Canada bond.

Sep 30: Sold the Government of Canada bond at 97.

Sep 30: Fair value on FMC Co. bond is $52,500 and fair value of Alpha Inc. bond is $38,700.

Instructions

Record the transactions that occurred in September and prepare any adjusting entries required at September 30.

Sep 1: On hand:

$50,000, 5% FMC Co. bond, purchased previously by O'Hara at 101. Interest on the bond is payable semi-annually on January 1 and July 1.

$100,000 3% Government of Canada bond, previously purchased by O'Hara at 98. Interest on the bond is payable semi-annually on March 31, and September 30.

Sep 1: Purchased $40,000 4% Alpha Inc. bond at 99. Interest is payable annually on August 31.

Sep 30: Received interest on Government of Canada bond.

Sep 30: Sold the Government of Canada bond at 97.

Sep 30: Fair value on FMC Co. bond is $52,500 and fair value of Alpha Inc. bond is $38,700.

Instructions

Record the transactions that occurred in September and prepare any adjusting entries required at September 30.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

64

Sanajevah Corp. had the following transactions pertaining to its trading investments:

Jan 1 Purchased 900 Punji Inc. shares for $9,450.

Jun 1 Received cash dividends of $0.50 per share on Punji shares.

Sep 15 Sold 400 Punji shares for $4,300.

Dec 1 Received cash dividends of $0.50 per share on Punji shares.

On December 31, the shares of Punji Inc. were trading for $10 each.

Instructions

a. Journalize the transactions.

b. Indicate the income statement and/or comprehensive income effects of the transactions.

Jan 1 Purchased 900 Punji Inc. shares for $9,450.

Jun 1 Received cash dividends of $0.50 per share on Punji shares.

Sep 15 Sold 400 Punji shares for $4,300.

Dec 1 Received cash dividends of $0.50 per share on Punji shares.

On December 31, the shares of Punji Inc. were trading for $10 each.

Instructions

a. Journalize the transactions.

b. Indicate the income statement and/or comprehensive income effects of the transactions.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

65

Trainor Inc., a public company, had the following transactions pertaining to debt investments held as trading investments:

Jan 1 Purchased 60, 8%, $1,000 Terry Corp. bonds for $60,000. Interest is payable semi-annually on July 1 and January 1. On December 31 the bonds were trading at 101.

Jul 1 Received semi-annual interest on Terry Corp. bonds.

1 Sold 30 Terry Corp. bonds for $32,000.

Instructions

a. Journalize the transactions.

b. Prepare the required adjusting journal entries at December 31.

Jan 1 Purchased 60, 8%, $1,000 Terry Corp. bonds for $60,000. Interest is payable semi-annually on July 1 and January 1. On December 31 the bonds were trading at 101.

Jul 1 Received semi-annual interest on Terry Corp. bonds.

1 Sold 30 Terry Corp. bonds for $32,000.

Instructions

a. Journalize the transactions.

b. Prepare the required adjusting journal entries at December 31.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

66

On July 2, 2014, Midtown Corp. purchased at 101, $100,000 of 6%, 10 year bonds issued by Smallville Inc., with the intention of holding the bonds to earn interest income. The bonds pay interest semi-annually on January 1 and July 1. Both companies have December 31 year ends. The relevant amortization amount for the period ending December 31, 2014 is $50.

Instructions

a. Record the purchase of the bond by Midtown and record any entries it will make related to this investment for the year end December 31, 2014.

b. Record the issue of the bond by Smallville and record any entries they will make related to this liability for the year end December 31, 2014.

c. Record the receipt of interest by Midtown on January 1, 2015.

d. Record the payment of interest by Smallville on January 1, 2015.

Instructions

a. Record the purchase of the bond by Midtown and record any entries it will make related to this investment for the year end December 31, 2014.

b. Record the issue of the bond by Smallville and record any entries they will make related to this liability for the year end December 31, 2014.

c. Record the receipt of interest by Midtown on January 1, 2015.

d. Record the payment of interest by Smallville on January 1, 2015.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

67

The following transactions were made by Weiss Inc., a public company. Assume all investments are trading investments.

Jun 2 Purchased 200 Avery Corporation common shares for $45 per share.

Jul 1 Purchased 200 Lewis Corporation bonds for $220,000.

30 Received a cash dividend of $2 per share from Avery Corporation.

Sep 15 Sold 60 shares of Avery Corporation for $50 per share.

Dec 31 Received semi-annual interest cheque for $11,000 from Lewis Corporation.

31 Received a cash dividend of $2 per share from Avery Corporation.

31 The shares of Avery Corporation are worth $60 each on this date. The Bonds are worth $237,000.

Instructions

Journalize the transactions and required adjusting journal entries at December 31, the company's fiscal year end.

Jun 2 Purchased 200 Avery Corporation common shares for $45 per share.

Jul 1 Purchased 200 Lewis Corporation bonds for $220,000.

30 Received a cash dividend of $2 per share from Avery Corporation.

Sep 15 Sold 60 shares of Avery Corporation for $50 per share.

Dec 31 Received semi-annual interest cheque for $11,000 from Lewis Corporation.

31 Received a cash dividend of $2 per share from Avery Corporation.

31 The shares of Avery Corporation are worth $60 each on this date. The Bonds are worth $237,000.

Instructions

Journalize the transactions and required adjusting journal entries at December 31, the company's fiscal year end.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

68

Match between columns

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 68 flashcards in this deck.