Deck 13: Cost Accounting and Reporting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

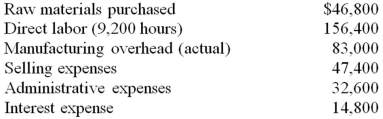

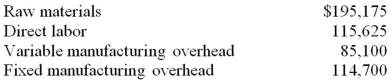

Vincent Custom Graphics estimates the following for 2013:  During 2013 Vincent incurs the following costs and activity:

During 2013 Vincent incurs the following costs and activity:  Vincent uses direct labor hours to calculate the predetermined overhead rate for the year.

Vincent uses direct labor hours to calculate the predetermined overhead rate for the year.

(a.) Calculate the predetermined overhead rate for 2013.

(b.) Calculate the applied overhead for 2013.

(c.) Calculate the amount of overapplied or underapplied overhead for 2013.

During 2013 Vincent incurs the following costs and activity: Vincent uses direct labor hours to calculate the predetermined overhead rate for the year.(a.) Calculate the predetermined overhead rate for 2013.

(b.) Calculate the applied overhead for 2013.

(c.) Calculate the amount of overapplied or underapplied overhead for 2013.

Question

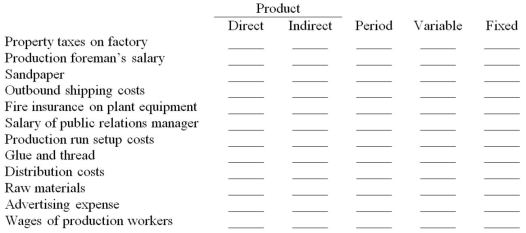

For each of the following costs, check the columns that most likely apply.

Question

Partridge, Inc. incurred the following costs during March:  Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume that overapplied or underapplied overhead is transferred to cost of goods sold only at the end of the year. During the month, 3,500 units of product were manufactured and 3,400 units of product were sold. On March 1 and March 31, Partridge carried the following inventory balances:

Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume that overapplied or underapplied overhead is transferred to cost of goods sold only at the end of the year. During the month, 3,500 units of product were manufactured and 3,400 units of product were sold. On March 1 and March 31, Partridge carried the following inventory balances:  (a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and calculate the average cost per unit produced.

(a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and calculate the average cost per unit produced.

(b.) Calculate the cost of goods sold during March.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume that overapplied or underapplied overhead is transferred to cost of goods sold only at the end of the year. During the month, 3,500 units of product were manufactured and 3,400 units of product were sold. On March 1 and March 31, Partridge carried the following inventory balances: (a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and calculate the average cost per unit produced.(b.) Calculate the cost of goods sold during March.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Question

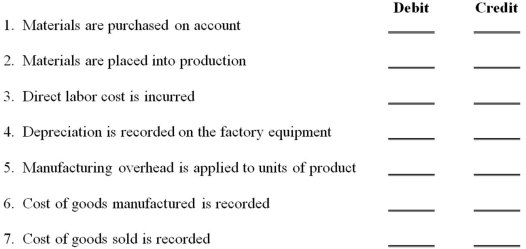

Webster World Products uses the following account titles:  For each transaction described below, indicate which accounts would be debited and credited under a job order cost system:

For each transaction described below, indicate which accounts would be debited and credited under a job order cost system:

For each transaction described below, indicate which accounts would be debited and credited under a job order cost system: Question

Baja Industries has recently switched its method of applying manufacturing overhead from a single predetermined overhead rate based on direct labor hours to activity-based costing (ABC). Assume that the direct labor rate is $18.00 per hour and that there were no beginning inventories. The following cost drivers and rates have been developed for allocating manufacturing overhead costs:  The following production, costs, and activities occurred during the month of August:

The following production, costs, and activities occurred during the month of August:  (a.) Calculate the total manufacturing cost and the cost per unit for the month of August.

(a.) Calculate the total manufacturing cost and the cost per unit for the month of August.

(b.) Assume instead that Baja Industries applies manufacturing overhead on the basis of $40.00 per direct labor hours (rather than the ABC method). Calculate the total manufacturing overhead cost applied for the month of August.

(c.) Which method of applying overhead do you think provides better information for manufacturing managers?

The following production, costs, and activities occurred during the month of August: (a.) Calculate the total manufacturing cost and the cost per unit for the month of August.(b.) Assume instead that Baja Industries applies manufacturing overhead on the basis of $40.00 per direct labor hours (rather than the ABC method). Calculate the total manufacturing overhead cost applied for the month of August.

(c.) Which method of applying overhead do you think provides better information for manufacturing managers?

Question

The following table summarizes the beginning and ending inventories of Ariel Co. for the month of October:  Raw materials purchased during the month of October totaled $112,300. Direct labor costs incurred totaled $234,800 for the month. Actual and applied manufacturing overhead costs for October totaled $145,100 and $149,400, respectively.

Raw materials purchased during the month of October totaled $112,300. Direct labor costs incurred totaled $234,800 for the month. Actual and applied manufacturing overhead costs for October totaled $145,100 and $149,400, respectively.

(a) Calculate the cost of goods manufactured for October.

(b) Calculate the cost of goods sold for October (Ignore under/overapplied overhead).

(c) Given the fact that 25,000 units were produced, what is the cost per unit for October?

Raw materials purchased during the month of October totaled $112,300. Direct labor costs incurred totaled $234,800 for the month. Actual and applied manufacturing overhead costs for October totaled $145,100 and $149,400, respectively.(a) Calculate the cost of goods manufactured for October.

(b) Calculate the cost of goods sold for October (Ignore under/overapplied overhead).

(c) Given the fact that 25,000 units were produced, what is the cost per unit for October?

Question

Question

Question

Question

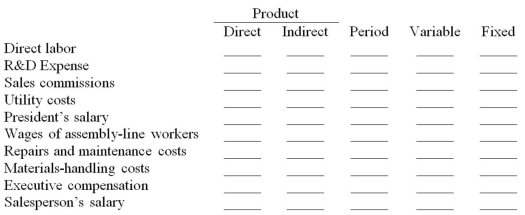

For each of the following costs, check the columns that most likely apply.

Question

Fountain Company uses activity-based costing (ABC) for allocating manufacturing overhead costs to jobs and it has established the following cost drivers and rates:  During April, Job #7598 produced 2,500 units and required the following activity: 1,200 parts, 2 production runs, and 225 direct labor hours.

During April, Job #7598 produced 2,500 units and required the following activity: 1,200 parts, 2 production runs, and 225 direct labor hours.

(a.) Calculate the amount of manufacturing overhead applied to Job #7598.

(b.) Explain the advantage of using the ABC approach.

During April, Job #7598 produced 2,500 units and required the following activity: 1,200 parts, 2 production runs, and 225 direct labor hours.(a.) Calculate the amount of manufacturing overhead applied to Job #7598.

(b.) Explain the advantage of using the ABC approach.

Question

Great Bay Co. manufactures cordless telephones. During 2013, total costs associated with manufacturing 18,500 of the AB-2000 model (introduced this year) were as follows:  (a.) Calculate the cost per phone under both direct (or variable) costing and absorption costing.

(a.) Calculate the cost per phone under both direct (or variable) costing and absorption costing.

(b.) If 2,800 of these phones were in finished goods inventory at the end of 2013, by how much and in what direction (higher or lower) would 2013 operating income be different under direct (or variable) costing than under absorption costing?

(c.) Express the phone cost in a cost formula. What does this formula suggest the total cost of making an additional 1,600 phones would be?

(a.) Calculate the cost per phone under both direct (or variable) costing and absorption costing.(b.) If 2,800 of these phones were in finished goods inventory at the end of 2013, by how much and in what direction (higher or lower) would 2013 operating income be different under direct (or variable) costing than under absorption costing?

(c.) Express the phone cost in a cost formula. What does this formula suggest the total cost of making an additional 1,600 phones would be?

Question

Question

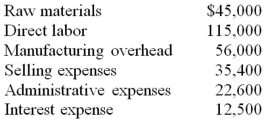

George's Garage incurred the following costs during May:  During the month, 6,000 units of product were manufactured and 5,500 units of product were sold. On May 1, George's carried no inventories.

During the month, 6,000 units of product were manufactured and 5,500 units of product were sold. On May 1, George's carried no inventories.

(a.) Calculate the cost of goods manufactured during May and the average cost per unit of product manufactured.

(b.) Calculate the cost of goods sold during May.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

During the month, 6,000 units of product were manufactured and 5,500 units of product were sold. On May 1, George's carried no inventories.(a.) Calculate the cost of goods manufactured during May and the average cost per unit of product manufactured.

(b.) Calculate the cost of goods sold during May.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/54

Play

Full screen (f)

Deck 13: Cost Accounting and Reporting

1

The overhead component of product cost is:

A) the sum of the actual overhead costs incurred in the manufacture of the product.

B) likely to be the same amount for every product made by the company.

C) an estimated amount based on labor hours, machine hours, or some other activity.

D) determined at the end of the year when actual costs and actual production are known.

A) the sum of the actual overhead costs incurred in the manufacture of the product.

B) likely to be the same amount for every product made by the company.

C) an estimated amount based on labor hours, machine hours, or some other activity.

D) determined at the end of the year when actual costs and actual production are known.

C

2

The sequence of activities that add value to the organization are:

A) the value processes.

B) the chain of production events.

C) the value chain.

D) the strategic cost initiatives.

A) the value processes.

B) the chain of production events.

C) the value chain.

D) the strategic cost initiatives.

C

3

Costs may be allocated to a product or activity for many purposes, but care must be exercised when using allocated costs because:

A) direct costs identified with the product or activity may not be accurately assigned.

B) fixed costs will change in total if the volume of activity changes.

C) all costs may not have been allocated to the product or activity.

D) arbitrarily allocated costs may not behave in the way assumed in the allocation method.

A) direct costs identified with the product or activity may not be accurately assigned.

B) fixed costs will change in total if the volume of activity changes.

C) all costs may not have been allocated to the product or activity.

D) arbitrarily allocated costs may not behave in the way assumed in the allocation method.

D

4

Product costs are inventoried and treated as assets until:

A) the next accounting period.

B) related liabilities no longer exist.

C) the period in which the products they relate to are sold.

D) none of these.

A) the next accounting period.

B) related liabilities no longer exist.

C) the period in which the products they relate to are sold.

D) none of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

5

The production cost of a single unit of a manufactured product is determined by:

A) dividing total direct materials and direct labor for a production run by the number of units made.

B) dividing total direct materials, direct labor, and manufacturing overhead for a production run by the number of units made.

C) dividing total direct materials, direct labor, manufacturing overhead and selling expenses for a production run by the number of units made.

D) dividing the selling price by the gross profit ratio.

A) dividing total direct materials and direct labor for a production run by the number of units made.

B) dividing total direct materials, direct labor, and manufacturing overhead for a production run by the number of units made.

C) dividing total direct materials, direct labor, manufacturing overhead and selling expenses for a production run by the number of units made.

D) dividing the selling price by the gross profit ratio.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

6

An example of a cost that is likely to have a direct relationship with products being manufactured is:

A) sales force salaries.

B) depreciation of production equipment.

C) salaries of production supervisors.

D) production labor costs.

A) sales force salaries.

B) depreciation of production equipment.

C) salaries of production supervisors.

D) production labor costs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

7

Direct costs pertain to costs that:

A) are traceable to a cost object.

B) are not traceable to a cost object.

C) are commonly incurred.

D) are variable costs.

A) are traceable to a cost object.

B) are not traceable to a cost object.

C) are commonly incurred.

D) are variable costs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

8

Common costs pertain to costs that:

A) are directly traceable to a cost object.

B) are not directly traceable to a cost object.

C) are commonly incurred.

D) are direct costs.

A) are directly traceable to a cost object.

B) are not directly traceable to a cost object.

C) are commonly incurred.

D) are direct costs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

9

Cost of Goods Manufactured can be computed as:

A) ending balance of work in process + raw materials used + direct labor costs incurred + manufacturing overhead costs applied ─ beginning balance of work in process.

B) beginning balance of work in process + raw materials purchased + direct labor costs incurred + manufacturing overhead costs applied ─ ending balance of work in process.

C) ending balance of work in process + raw materials purchased + direct labor costs incurred + manufacturing overhead costs applied ─ beginning balance of work in process.

D) beginning balance of work in process + raw materials used + direct labor costs incurred + manufacturing overhead costs applied ─ ending balance of work in process.

A) ending balance of work in process + raw materials used + direct labor costs incurred + manufacturing overhead costs applied ─ beginning balance of work in process.

B) beginning balance of work in process + raw materials purchased + direct labor costs incurred + manufacturing overhead costs applied ─ ending balance of work in process.

C) ending balance of work in process + raw materials purchased + direct labor costs incurred + manufacturing overhead costs applied ─ beginning balance of work in process.

D) beginning balance of work in process + raw materials used + direct labor costs incurred + manufacturing overhead costs applied ─ ending balance of work in process.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

10

The term "cost" means:

A) the price paid for a raw material.

B) the wage paid to a worker.

C) the price charged by an entity for its services.

D) all of these.

A) the price paid for a raw material.

B) the wage paid to a worker.

C) the price charged by an entity for its services.

D) all of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

11

An example of a cost likely to have an indirect relationship with products being manufactured is:

A) production labor costs.

B) raw material costs.

C) electricity costs for packaging equipment.

D) None of these.

A) production labor costs.

B) raw material costs.

C) electricity costs for packaging equipment.

D) None of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

12

Cost accounting is primarily concerned with:

A) accumulation and determination of product or service cost.

B) income measurement and inventory valuation.

C) generally accepted accounting principles.

D) all of these.

A) accumulation and determination of product or service cost.

B) income measurement and inventory valuation.

C) generally accepted accounting principles.

D) all of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

13

An example of a product cost is:

A) advertising expense for the product.

B) a portion of the president's travel expenses.

C) interest expense on a loan to finance inventory.

D) production line maintenance costs.

A) advertising expense for the product.

B) a portion of the president's travel expenses.

C) interest expense on a loan to finance inventory.

D) production line maintenance costs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is more relevant to management accounting than to cost accounting?

A) accumulation and determination of product or service cost.

B) income measurement and inventory valuation.

C) generally accepted accounting principles.

D) providing managers information for planning and control purposes.

A) accumulation and determination of product or service cost.

B) income measurement and inventory valuation.

C) generally accepted accounting principles.

D) providing managers information for planning and control purposes.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

15

In the T-account cost flow diagram of balance sheet inventory accounts and the income statement cost of goods sold account:

A) raw materials purchases are debited to work in process.

B) direct labor costs are credited to work in process.

C) cost of goods manufactured is debited to finished goods inventory.

D) cost of goods sold is debited to finished goods inventory.

A) raw materials purchases are debited to work in process.

B) direct labor costs are credited to work in process.

C) cost of goods manufactured is debited to finished goods inventory.

D) cost of goods sold is debited to finished goods inventory.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following activities is not included in the organization's value chain?

A) marketing.

B) finance.

C) customer service.

D) research and development.

A) marketing.

B) finance.

C) customer service.

D) research and development.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

17

An organization's value chain refers to:

A) the process of using cost information to manage the activities of the organization.

B) the sequence of functions and related activities that add value for the customer.

C) the process of collecting and recording valuable information in the accounting information system.

D) None of these.

A) the process of using cost information to manage the activities of the organization.

B) the sequence of functions and related activities that add value for the customer.

C) the process of collecting and recording valuable information in the accounting information system.

D) None of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

18

For the partial value chain functions given below, which sequence is correct?

A) design, production, marketing.

B) marketing, production, distribution.

C) research and development, production, distribution.

D) customer service, marketing, distribution.

A) design, production, marketing.

B) marketing, production, distribution.

C) research and development, production, distribution.

D) customer service, marketing, distribution.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

19

Cost accounting is a subset of:

A) financial accounting.

B) process cost accounting.

C) job order cost accounting.

D) managerial accounting.

A) financial accounting.

B) process cost accounting.

C) job order cost accounting.

D) managerial accounting.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following costs would be classified as a period cost:

A) production line maintenance costs.

B) advertising expense for the product.

C) plant electricity.

D) indirect labor.

A) production line maintenance costs.

B) advertising expense for the product.

C) plant electricity.

D) indirect labor.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

21

Total manufacturing costs for the month on the statement of costs of goods manufactured equals:

A) variable costs + fixed costs + mixed costs.

B) work in process inventory - finished goods inventory.

C) cost of goods sold - cost of goods manufactured.

D) cost of raw material used + direct labor cost incurred + manufacturing overhead applied.

A) variable costs + fixed costs + mixed costs.

B) work in process inventory - finished goods inventory.

C) cost of goods sold - cost of goods manufactured.

D) cost of raw material used + direct labor cost incurred + manufacturing overhead applied.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is NOT an inventory account for a manufacturing company?

A) Cost of goods sold.

B) Work-in-process.

C) Raw materials.

D) Finished goods.

A) Cost of goods sold.

B) Work-in-process.

C) Raw materials.

D) Finished goods.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following describes the correct sequence of flow of costs for a manufacturing firm?

A) Raw materials, finished goods, work-in-process, cost of goods sold.

B) Work-in-process, raw materials, finished goods, cost of goods sold.

C) Raw materials, work-in-process, finished goods, cost of goods sold.

D) Raw materials, work-in-process, cost of goods sold, finished goods.

A) Raw materials, finished goods, work-in-process, cost of goods sold.

B) Work-in-process, raw materials, finished goods, cost of goods sold.

C) Raw materials, work-in-process, finished goods, cost of goods sold.

D) Raw materials, work-in-process, cost of goods sold, finished goods.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

24

The predetermined overhead application rate based on direct labor hours is computed as:

A) actual total overhead costs divided by actual direct labor hours.

B) estimated total overhead costs divided by estimated direct labor hours.

C) actual total overhead costs divided by estimated direct labor hours.

D) estimated total overhead costs divided by actual direct labor hours.

A) actual total overhead costs divided by actual direct labor hours.

B) estimated total overhead costs divided by estimated direct labor hours.

C) actual total overhead costs divided by estimated direct labor hours.

D) estimated total overhead costs divided by actual direct labor hours.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following is a true statement regarding absorption and/or direct costing?

A) A firm can choose to use either absorption or direct costing for income tax purposes.

B) A firm can choose to use either absorption or direct costing for financial reporting purposes.

C) Direct costing assigns only direct materials and direct labor to products.

D) Absorption costing includes fixed overhead in product costs whereas direct costing does not.

A) A firm can choose to use either absorption or direct costing for income tax purposes.

B) A firm can choose to use either absorption or direct costing for financial reporting purposes.

C) Direct costing assigns only direct materials and direct labor to products.

D) Absorption costing includes fixed overhead in product costs whereas direct costing does not.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

26

An excess of cost of goods manufactured over cost of goods sold for the period represents:

A) an increase in gross profit.

B) a decrease in work in process inventory.

C) overapplied manufacturing overhead.

D) an increase in finished goods inventory.

A) an increase in gross profit.

B) a decrease in work in process inventory.

C) overapplied manufacturing overhead.

D) an increase in finished goods inventory.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

27

A debit balance in the manufacturing overhead account at the end of the period indicates that:

A) manufacturing overhead is overapplied.

B) manufacturing overhead is underapplied.

C) manufacturing overhead has been accurately applied.

D) None of these.

A) manufacturing overhead is overapplied.

B) manufacturing overhead is underapplied.

C) manufacturing overhead has been accurately applied.

D) None of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

28

Direct costing may be used for:

A) internal reporting purposes.

B) external financial reporting purposes.

C) income tax reporting purposes.

D) all of these.

A) internal reporting purposes.

B) external financial reporting purposes.

C) income tax reporting purposes.

D) all of these.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is NOT an account that over/under applied overhead is transferred to at the end of an accounting period?

A) Cost of goods sold.

B) Work-in-process.

C) Raw materials.

D) Finished goods.

A) Cost of goods sold.

B) Work-in-process.

C) Raw materials.

D) Finished goods.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

30

A predetermined overhead rate is used to:

A) keep track of actual overhead costs as they are incurred.

B) assign indirect costs to cost objects.

C) establish prices for manufactured products.

D) allocate selling and administrative expenses to manufactured products.

A) keep track of actual overhead costs as they are incurred.

B) assign indirect costs to cost objects.

C) establish prices for manufactured products.

D) allocate selling and administrative expenses to manufactured products.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

31

In order to achieve higher quality cost information from the assignment of overhead costs to products manufactured, the use of a predetermined overhead rate is being replaced by:

A) absorption costing.

B) job order costing.

C) activity-based costing.

D) process costing.

A) absorption costing.

B) job order costing.

C) activity-based costing.

D) process costing.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following items would not be reported on the statement of cost of goods manufactured?

A) cost of goods sold.

B) purchases.

C) total manufacturing costs.

D) contribution margin.

A) cost of goods sold.

B) purchases.

C) total manufacturing costs.

D) contribution margin.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following costs are included in the "for cost accounting purposes" classification?

A) Variable cost and fixed cost.

B) Direct cost and indirect cost.

C) Product cost and period cost.

D) Committed cost and discretionary cost.

A) Variable cost and fixed cost.

B) Direct cost and indirect cost.

C) Product cost and period cost.

D) Committed cost and discretionary cost.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

34

The primary difference between absorption costing and direct costing is the treatment of:

A) direct material costs.

B) variable manufacturing overhead.

C) fixed manufacturing overhead.

D) direct labor costs.

A) direct material costs.

B) variable manufacturing overhead.

C) fixed manufacturing overhead.

D) direct labor costs.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

35

If all units produced during the month of September are sold, and no additional units are sold from the beginning finished goods inventory, then:

A) income determined with absorption costing will equal income determined with direct costing.

B) ending work in process inventory will increase.

C) income determined with absorption costing will be lower than income determined with direct costing.

D) ending finished goods inventory will decrease.

A) income determined with absorption costing will equal income determined with direct costing.

B) ending work in process inventory will increase.

C) income determined with absorption costing will be lower than income determined with direct costing.

D) ending finished goods inventory will decrease.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

36

An activity-based costing system involves identifying the activity that causes the incurrence of a cost; this activity is known as a:

A) cost driver.

B) cost applier.

C) direct cost.

D) cost object.

A) cost driver.

B) cost applier.

C) direct cost.

D) cost object.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

37

The three components of product costs are:

A) direct material, supervisor salaries, selling expenses.

B) direct labor, manufacturing overhead, indirect material.

C) direct material, direct labor, manufacturing overhead.

D) manufacturing overhead, indirect material, indirect labor.

A) direct material, supervisor salaries, selling expenses.

B) direct labor, manufacturing overhead, indirect material.

C) direct material, direct labor, manufacturing overhead.

D) manufacturing overhead, indirect material, indirect labor.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

38

The three sections of a statement of cost of goods manufactured include:

A) raw material, direct labor, manufacturing overhead.

B) variable expenses, contribution margin, fixed expenses.

C) sales revenue, gross profit, selling and administrative expenses.

D) direct costs, indirect costs, operating profit.

A) raw material, direct labor, manufacturing overhead.

B) variable expenses, contribution margin, fixed expenses.

C) sales revenue, gross profit, selling and administrative expenses.

D) direct costs, indirect costs, operating profit.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

39

The shift in the amount of manufacturing overhead costs applied to the mix of products produced that occurs when using a single cost driver rate as compared to using activity-based costing rates is known as:

A) underapplied overhead.

B) overapplied overhead.

C) cost absorption.

D) cost distortion.

A) underapplied overhead.

B) overapplied overhead.

C) cost absorption.

D) cost distortion.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following will cause income determined with absorption costing to be higher than income determined with direct costing?

A) units produced equal units sold.

B) units produced are greater than units sold.

C) units produced are less than units sold.

D) income determined with absorption costing will always equal income determined with direct costing.

A) units produced equal units sold.

B) units produced are greater than units sold.

C) units produced are less than units sold.

D) income determined with absorption costing will always equal income determined with direct costing.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

41

Vincent Custom Graphics estimates the following for 2013: During 2013 Vincent incurs the following costs and activity: Vincent uses direct labor hours to calculate the predetermined overhead rate for the year.

(a.) Calculate the predetermined overhead rate for 2013.

(b.) Calculate the applied overhead for 2013.

(c.) Calculate the amount of overapplied or underapplied overhead for 2013.

During 2013 Vincent incurs the following costs and activity: Vincent uses direct labor hours to calculate the predetermined overhead rate for the year.(a.) Calculate the predetermined overhead rate for 2013.

(b.) Calculate the applied overhead for 2013.

(c.) Calculate the amount of overapplied or underapplied overhead for 2013.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

42

For each of the following costs, check the columns that most likely apply.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

43

Partridge, Inc. incurred the following costs during March: Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume that overapplied or underapplied overhead is transferred to cost of goods sold only at the end of the year. During the month, 3,500 units of product were manufactured and 3,400 units of product were sold. On March 1 and March 31, Partridge carried the following inventory balances: (a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and calculate the average cost per unit produced.

(b.) Calculate the cost of goods sold during March.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Manufacturing overhead is applied on the basis of $8.50 per direct labor hour. Assume that overapplied or underapplied overhead is transferred to cost of goods sold only at the end of the year. During the month, 3,500 units of product were manufactured and 3,400 units of product were sold. On March 1 and March 31, Partridge carried the following inventory balances: (a.) Prepare a Statement of Cost of Goods Manufactured for the month of March, and calculate the average cost per unit produced.(b.) Calculate the cost of goods sold during March.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

44

Webster World Products uses the following account titles: For each transaction described below, indicate which accounts would be debited and credited under a job order cost system:

For each transaction described below, indicate which accounts would be debited and credited under a job order cost system: Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

45

Baja Industries has recently switched its method of applying manufacturing overhead from a single predetermined overhead rate based on direct labor hours to activity-based costing (ABC). Assume that the direct labor rate is $18.00 per hour and that there were no beginning inventories. The following cost drivers and rates have been developed for allocating manufacturing overhead costs: The following production, costs, and activities occurred during the month of August: (a.) Calculate the total manufacturing cost and the cost per unit for the month of August.

(b.) Assume instead that Baja Industries applies manufacturing overhead on the basis of $40.00 per direct labor hours (rather than the ABC method). Calculate the total manufacturing overhead cost applied for the month of August.

(c.) Which method of applying overhead do you think provides better information for manufacturing managers?

The following production, costs, and activities occurred during the month of August: (a.) Calculate the total manufacturing cost and the cost per unit for the month of August.(b.) Assume instead that Baja Industries applies manufacturing overhead on the basis of $40.00 per direct labor hours (rather than the ABC method). Calculate the total manufacturing overhead cost applied for the month of August.

(c.) Which method of applying overhead do you think provides better information for manufacturing managers?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

46

The following table summarizes the beginning and ending inventories of Ariel Co. for the month of October: Raw materials purchased during the month of October totaled $112,300. Direct labor costs incurred totaled $234,800 for the month. Actual and applied manufacturing overhead costs for October totaled $145,100 and $149,400, respectively.

(a) Calculate the cost of goods manufactured for October.

(b) Calculate the cost of goods sold for October (Ignore under/overapplied overhead).

(c) Given the fact that 25,000 units were produced, what is the cost per unit for October?

Raw materials purchased during the month of October totaled $112,300. Direct labor costs incurred totaled $234,800 for the month. Actual and applied manufacturing overhead costs for October totaled $145,100 and $149,400, respectively.(a) Calculate the cost of goods manufactured for October.

(b) Calculate the cost of goods sold for October (Ignore under/overapplied overhead).

(c) Given the fact that 25,000 units were produced, what is the cost per unit for October?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

47

Erber, Inc. produces men's neckties and dress socks. Manufacturing overhead is assigned to production using an application rate based on direct labor hours.

(a.) For 2013, the company's cost accountant estimated that total overhead costs incurred would be $184,500, and that a total of 24,600 direct labor hours would be worked. Calculate the amount of overhead to be applied for each direct labor hour worked on a production run.

(b.) A production run of 500 neckties required raw materials that cost $3,120, and 140 direct labor hours at a cost of $8.00 per hour. Calculate the cost of each necktie produced.

(c.) At the end of February 2013, 420 neckties made in the above production run had been sold, and the rest were in ending inventory. Calculate the cost of the neckties sold that would have been reported in the income statement and the cost included in the February 28, 2013, finished goods inventory.

(a.) For 2013, the company's cost accountant estimated that total overhead costs incurred would be $184,500, and that a total of 24,600 direct labor hours would be worked. Calculate the amount of overhead to be applied for each direct labor hour worked on a production run.

(b.) A production run of 500 neckties required raw materials that cost $3,120, and 140 direct labor hours at a cost of $8.00 per hour. Calculate the cost of each necktie produced.

(c.) At the end of February 2013, 420 neckties made in the above production run had been sold, and the rest were in ending inventory. Calculate the cost of the neckties sold that would have been reported in the income statement and the cost included in the February 28, 2013, finished goods inventory.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

48

Envision Toy Co. manufactures toy boats. During 2013, total costs incurred in making 27,000 toy boats included $94,500 of fixed manufacturing overhead. The total absorption cost per toy boat was $30.80.

(a.) Calculate the variable cost per toy boat.

(b.) The ending inventory of toy boats was 5,800 units higher at the end of 2013 than at the beginning of the year. By how much and in what direction (higher or lower) would cost of goods sold for 2013 be different under direct costing than under variable costing?

(c.) Express the toy boat cost in a cost formula. What does this formula suggest the total cost of making an additional 2,900 toy boats would be?

(a.) Calculate the variable cost per toy boat.

(b.) The ending inventory of toy boats was 5,800 units higher at the end of 2013 than at the beginning of the year. By how much and in what direction (higher or lower) would cost of goods sold for 2013 be different under direct costing than under variable costing?

(c.) Express the toy boat cost in a cost formula. What does this formula suggest the total cost of making an additional 2,900 toy boats would be?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

49

Erca, Inc. produces automobile bumpers. Overhead is applied on the basis of machine hours required for cutting and fabricating. A predetermined overhead application rate of $15.00 per machine hour was established for 2013.

(a.) If 9,000 machine hours were expected to be used during 2013, how much overhead was expected to be incurred?

(b.) Actual overhead incurred during 2013 totaled $135,000, and 9,200 machine hours were used during 2013. Calculate the amount of over-or underapplied overhead for 2013.

(c.) Explain the accounting necessary for the over- or underapplied overhead for the year.

(a.) If 9,000 machine hours were expected to be used during 2013, how much overhead was expected to be incurred?

(b.) Actual overhead incurred during 2013 totaled $135,000, and 9,200 machine hours were used during 2013. Calculate the amount of over-or underapplied overhead for 2013.

(c.) Explain the accounting necessary for the over- or underapplied overhead for the year.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

50

For each of the following costs, check the columns that most likely apply.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

51

Fountain Company uses activity-based costing (ABC) for allocating manufacturing overhead costs to jobs and it has established the following cost drivers and rates: During April, Job #7598 produced 2,500 units and required the following activity: 1,200 parts, 2 production runs, and 225 direct labor hours.

(a.) Calculate the amount of manufacturing overhead applied to Job #7598.

(b.) Explain the advantage of using the ABC approach.

During April, Job #7598 produced 2,500 units and required the following activity: 1,200 parts, 2 production runs, and 225 direct labor hours.(a.) Calculate the amount of manufacturing overhead applied to Job #7598.

(b.) Explain the advantage of using the ABC approach.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

52

Great Bay Co. manufactures cordless telephones. During 2013, total costs associated with manufacturing 18,500 of the AB-2000 model (introduced this year) were as follows: (a.) Calculate the cost per phone under both direct (or variable) costing and absorption costing.

(b.) If 2,800 of these phones were in finished goods inventory at the end of 2013, by how much and in what direction (higher or lower) would 2013 operating income be different under direct (or variable) costing than under absorption costing?

(c.) Express the phone cost in a cost formula. What does this formula suggest the total cost of making an additional 1,600 phones would be?

(a.) Calculate the cost per phone under both direct (or variable) costing and absorption costing.(b.) If 2,800 of these phones were in finished goods inventory at the end of 2013, by how much and in what direction (higher or lower) would 2013 operating income be different under direct (or variable) costing than under absorption costing?

(c.) Express the phone cost in a cost formula. What does this formula suggest the total cost of making an additional 1,600 phones would be?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

53

The use of activity-based costing information to support the decision-making process is known as:

A) value chain analysis.

B) cost distortion analysis.

C) activity-based management.

D) cost-based management.

A) value chain analysis.

B) cost distortion analysis.

C) activity-based management.

D) cost-based management.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

54

George's Garage incurred the following costs during May: During the month, 6,000 units of product were manufactured and 5,500 units of product were sold. On May 1, George's carried no inventories.

(a.) Calculate the cost of goods manufactured during May and the average cost per unit of product manufactured.

(b.) Calculate the cost of goods sold during May.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

During the month, 6,000 units of product were manufactured and 5,500 units of product were sold. On May 1, George's carried no inventories.(a.) Calculate the cost of goods manufactured during May and the average cost per unit of product manufactured.

(b.) Calculate the cost of goods sold during May.

(c.) Where in the financial statements will the difference between cost of goods manufactured and cost of goods sold be classified?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 54 flashcards in this deck.