Deck 18: Auditing Investments and

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

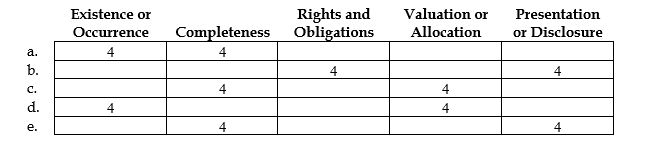

The performance of cash cutoff tests provides evidence for which of the following assertions?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/91

Play

Full screen (f)

Deck 18: Auditing Investments and

1

The tracing of bank transfers provides reliable evidence concerning the existence or occurrence and valuation or allocation assertions.

False

2

An entity's investments pertain to the activities relating to the ownership of securities issued by the entity.

False

3

A broker's advice is issued monthly by a broker specifying securities held in safekeeping by the broker, their cost, and their fair market value at the end of the month.

False

4

The auditor should coordinate the inspection of all material negotiable instruments on hand.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

5

The substantive testing of investments does not ordinarily employ analytical procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

6

During the count of a cash fund, the auditor should insist that the custodian of the fund be present throughout the count.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

7

Kiting is possible when the same individual can issue and record checks.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

8

Authorization for the purchase and sale of marketable securities should be found in the minutes the audit committee meetings.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

9

In the cash area, the auditor is usually more concerned about controls than about year-end balances.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

10

The bank transfer schedule should list all transfer checks issued at or near year-end.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

11

Calculation of the dividend payout ratio is an important analytical procedure for testing assertions related to both short-term and long-term investments.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

12

When detection risk for an assertion in the cash area is low, the auditor may perform all relevant tests at an interim date or well after year-end.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

13

The date of the bank cutoff statement is usually seven to ten days preceding the balance sheet date.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

14

Confirmation of cash on deposit will provide evidence for the existence or occurrence assertion since there is written acknowledgment that the balance exists.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

15

The fact that the quantity of transactions affecting cash are greater than any other account in the financial statements relates to control risk.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

16

Bank transfers may result in a misstatement of the bank balance per books if the disbursement and receipt are not recorded in the same journal.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

17

Substantive tests of cash balances result in evidential matter that has a high degree of reliability.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

18

The primary audit procedure for cash on hand and undeposited receipts is to perform a cash count.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

19

Bank confirmation requests should be mailed to all banks in which the client has an account, except those with zero balances at year-end.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

20

Substantive tests of investment balances provide evidential matter that has a high degree of reliability.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

21

The primary source document for recording investing transactions is the:

A) bond contract.

B) broker's advice.

C) stock certificate.

D) bond certificate.

E) bond indenture.

A) bond contract.

B) broker's advice.

C) stock certificate.

D) bond certificate.

E) bond indenture.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

22

The company officer who is assigned the authority and responsibility for investing transactions should have all of the following characteristics except:

A) is of unquestioned integrity.

B) possesses the knowledge and skills required of a person charged with executing such transactions.

C) has the ability to understand the auditor's procedures relating to investing transactions.

D) realizes the importance of observing all prescribed control procedures.

E) can assist other participating members of management in making initial and ongoing assessments of risks associated with individual investments.

A) is of unquestioned integrity.

B) possesses the knowledge and skills required of a person charged with executing such transactions.

C) has the ability to understand the auditor's procedures relating to investing transactions.

D) realizes the importance of observing all prescribed control procedures.

E) can assist other participating members of management in making initial and ongoing assessments of risks associated with individual investments.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

23

The confirmation process for securities held in safekeeping by others is substantially different from the process of confirming accounts receivable.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

24

Tests to detect lapping are only performed when control risk for cash receipts transactions is moderate or low.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

25

The specific audit objective for the audit of investments, all recorded investments are owned by the reporting entity, relates to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

26

It is not unusual for auditors to obtain significant assurance from analytical procedures applied to cash balances.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

27

Analyzing ratio results relative to expectations based on prior year, budgeted, or other data relates to:

A) initial procedures.

B) analytical procedures.

C) tests of details of transactions.

D) tests of details of balances.

E) presentation and disclosure.

A) initial procedures.

B) analytical procedures.

C) tests of details of transactions.

D) tests of details of balances.

E) presentation and disclosure.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

28

The specific audit objective for the audit of investments, recorded investment asset and equity balances represent investments that exist at the balance sheet date, relates to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

29

The nature of cash balances and the ability to obtain confirmations from banks minimize inherent risk for most cash balance assertions, especially existence or occurrence and completeness.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

30

The specific audit objective for the audit of investments, investment balances are properly identified and classified in the financial statements, relates to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

31

The specific audit objective for the audit of investments, all investments are included in the balance sheet investment accounts, relates to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

32

Conditions conducive to lapping exist when an individual who handles cash receipts also maintains the accounts receivable ledger.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

33

The specific audit objective for the audit of investments, investment revenues, and realized and unrealized gains and losses, are reported at proper amounts, relates to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is correct concerning the inspecting and counting of securities on hand?

A) All securities should be controlled by the auditor until the count is completed.

B) The custodian need not be present during the count.

C) A receipt should be provided by the auditor to the custodian when the securities are returned.

D) The auditor should observe the broker's advice number on the document.

E) The auditor should observe the name of the broker.

A) All securities should be controlled by the auditor until the count is completed.

B) The custodian need not be present during the count.

C) A receipt should be provided by the auditor to the custodian when the securities are returned.

D) The auditor should observe the broker's advice number on the document.

E) The auditor should observe the name of the broker.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

35

Which one of the following is a contract stating the terms of the bonds issued by a corporation?

A) bond contract

B) broker's advice

C) stock certificate

D) bond certificate

E) bond indenture

A) bond contract

B) broker's advice

C) stock certificate

D) bond certificate

E) bond indenture

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

36

Investing in marketable securities interfaces with the:

A) revenue cycle and the expenditure cycle.

B) production cycle and expenditure cycle.

C) production cycle and the revenue cycle.

D) financing cycle and the revenue cycle.

E) financing cycle and the expenditure cycle.

A) revenue cycle and the expenditure cycle.

B) production cycle and expenditure cycle.

C) production cycle and the revenue cycle.

D) financing cycle and the revenue cycle.

E) financing cycle and the expenditure cycle.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

37

The term window dressing refers to the client's deliberate attempt to overstate short-term solvency at year-end.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

38

Inspecting and counting securities on hand relates to:

A) initial procedures.

B) analytical procedures.

C) tests of details of transactions.

D) tests of details of balances.

E) presentation and disclosure.

A) initial procedures.

B) analytical procedures.

C) tests of details of transactions.

D) tests of details of balances.

E) presentation and disclosure.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

39

The inspecting and counting of securities on hand is ordinarily performed simultaneously with the auditor's:

A) observing of the inventory counting.

B) inspecting of major additions to plant assets.

C) confirming of securities held by others.

D) counting of cash.

E) recalculating of investment revenue earned.

A) observing of the inventory counting.

B) inspecting of major additions to plant assets.

C) confirming of securities held by others.

D) counting of cash.

E) recalculating of investment revenue earned.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

40

The auditor should make inquiries if the deposit in transit on the year-end bank reconciliation is not shown on the bank cutoff statement.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

41

The specific audit objective, cash balances are properly identified and classified in the balance sheet, is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following bank transfers appears to be an example of kiting aimed at concealing a cash shortage?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

43

In auditing investments, auditors may compare current-year and prior-year balances or compare actual results for the amount of investments and investment income with budgets or the documentation of management's plans. Unexpected differences would would be least likely to pertain to assertions about:

A) existence of occurrence.

B) completeness.

C) rights and obligations.

D) valuation or allocation.

E) presentation and disclosure.

A) existence of occurrence.

B) completeness.

C) rights and obligations.

D) valuation or allocation.

E) presentation and disclosure.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

44

In working with the bank reconciliation and the bank cutoff statement, the auditor finds that a prior-period check was not on the reconciliation as an outstanding check. This may be an indication of:

A) window dressing.

B) lapping.

C) kiting.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

A) window dressing.

B) lapping.

C) kiting.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

45

The auditor should trace bank transfers using a bank transfer schedule primarily to determine if:

A) cash has been understated due to kiting.

B) cash has been overstated due to kiting.

C) cash has been understated due to lapping.

D) cash has been overstated due to lapping.

E) any unusual cash receipts or payments occurred.

A) cash has been understated due to kiting.

B) cash has been overstated due to kiting.

C) cash has been understated due to lapping.

D) cash has been overstated due to lapping.

E) any unusual cash receipts or payments occurred.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

46

The performance of cash cutoff tests provides evidence for which of the following assertions?

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

47

The specific audit objective, the entity has legal title to all cash balances shown at the balance sheet date, is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

48

During the count of cash on hand, it is not necessary for the auditor to:

A) control both cash and non-cash negotiable instruments held by the client.

B) insist on the presence of an internal auditor throughout the count.

C) insist on the presence of the custodian of the cash throughout the count.

D) obtain a signed receipt from the custodian on return of the funds.

E) ascertain that all undeposited funds are payable to the order of the client, either directly or through endorsement.

A) control both cash and non-cash negotiable instruments held by the client.

B) insist on the presence of an internal auditor throughout the count.

C) insist on the presence of the custodian of the cash throughout the count.

D) obtain a signed receipt from the custodian on return of the funds.

E) ascertain that all undeposited funds are payable to the order of the client, either directly or through endorsement.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

49

The specific audit objective, recorded cash balances exist at the balance sheet date, is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

50

The control of all funds during the count of cash on hand is meant primarily to prevent:

A) transfers by the client.

B) any chance of double counting.

C) unauthorized disbursements.

D) client personnel from viewing the count procedure.

E) lapping or kiting by the client.

A) transfers by the client.

B) any chance of double counting.

C) unauthorized disbursements.

D) client personnel from viewing the count procedure.

E) lapping or kiting by the client.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following is not true concerning the confirmation of securities held by outsiders for safekeeping?

A) Confirmations should be requested as of the date other securities are counted.

B) The auditor must control the mailings.

C) The auditor should receive responses directly from the custodian.

D) The data confirmed are the same as the data that should be noted when the auditor is able to inspect the securities.

E) Either positive or negative confirmations can be used.

A) Confirmations should be requested as of the date other securities are counted.

B) The auditor must control the mailings.

C) The auditor should receive responses directly from the custodian.

D) The data confirmed are the same as the data that should be noted when the auditor is able to inspect the securities.

E) Either positive or negative confirmations can be used.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following bank transfers appears to be an example of kiting aimed at overstating the cash position at year-end?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

53

The confirmation of bank deposit and loan balances with banks provides evidence for which of the following assertions?

A) 4 4 4

B) 4 4 4 4

C) 4 4 4

D) 4 4 4

A) 4 4 4

B) 4 4 4 4

C) 4 4 4

D) 4 4 4

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

54

The specific audit objective, year-end transfers of cash between banks are recorded in the proper period, is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

55

Initial procedures for substantive tests of investments would not ordinarily include:

A) understanding investment policies regarding the proportion of investments in government securities, corporate bonds, and equity securities.

B) understanding an entity's policy for investing excess cash, its financing activities, and its ability to generate free cash flow.

C) checking the mathematical accuracy of client-prepared schedules of investments.

D) determining that subsidiary investment ledgers agree with related general ledger control account balances.

E) understanding economic drivers that allow an entity to engage in investing activities.

A) understanding investment policies regarding the proportion of investments in government securities, corporate bonds, and equity securities.

B) understanding an entity's policy for investing excess cash, its financing activities, and its ability to generate free cash flow.

C) checking the mathematical accuracy of client-prepared schedules of investments.

D) determining that subsidiary investment ledgers agree with related general ledger control account balances.

E) understanding economic drivers that allow an entity to engage in investing activities.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

56

The specific audit objective, recorded cash balances are realizable at the amounts stated on the balance sheet and agree with supporting schedules, is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

57

Evidence of kiting is least likely to come from:

A) bank transfer schedules.

B) cash cutoff tests.

C) tested reconciliations.

D) confirmation of bank balances.

E) bank cutoff statements.

A) bank transfer schedules.

B) cash cutoff tests.

C) tested reconciliations.

D) confirmation of bank balances.

E) bank cutoff statements.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

58

The use of bank cutoff statements to verify bank reconciliation items, detect any unrecorded checks that have cleared the bank, and look for evidence of window dressing provides evidence for which of the following assertions for cash in bank?

A) 4 4 4 4

B) 4 4 4 4

C) 4 4 4 4

D) 4 4 4 4

A) 4 4 4 4

B) 4 4 4 4

C) 4 4 4 4

D) 4 4 4 4

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

59

Verification procedures for investment income is least likely to include:

A) recalculation by the auditor.

B) reference to published investment information.

C) inspection of bond certificates.

D) review of any bond premium amortization schedules.

E) direct confirmation with the investee.

A) recalculation by the auditor.

B) reference to published investment information.

C) inspection of bond certificates.

D) review of any bond premium amortization schedules.

E) direct confirmation with the investee.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

60

The transaction cycle that does not interface directly with cash is the:

A) revenue cycle.

B) expenditure cycle.

C) production cycle.

D) financing cycle.

E) investing cycle.

A) revenue cycle.

B) expenditure cycle.

C) production cycle.

D) financing cycle.

E) investing cycle.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

61

When detection risk is very low, the auditor should:

A) scan the client's bank reconciliation and verify the mathematical accuracy of the reconciliation.

B) review the client's bank reconciliation.

C) prepare the reconciliation from data in the client's possession.

D) prepare the reconciliation from information obtained directly from the bank.

E) prepare the proof of cash from data in the client's possession.

A) scan the client's bank reconciliation and verify the mathematical accuracy of the reconciliation.

B) review the client's bank reconciliation.

C) prepare the reconciliation from data in the client's possession.

D) prepare the reconciliation from information obtained directly from the bank.

E) prepare the proof of cash from data in the client's possession.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

62

Misappropriation of assets is always present when an employee is involved with:

A) kiting.

B) window dressing.

C) an attempt to conceal a cash shortage.

D) an attempt to overstate cash.

E) lapping.

A) kiting.

B) window dressing.

C) an attempt to conceal a cash shortage.

D) an attempt to overstate cash.

E) lapping.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

63

In working with the bank reconciliation and the bank cutoff statement, the auditor finds that many of the checks on the outstanding checklist did not clear during the cutoff period. This may be an indication of:

A) lapping.

B) kiting.

C) window dressing.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

A) lapping.

B) kiting.

C) window dressing.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

64

For investments accounted for using the equity method:

A) audited financial statements of the investee generally constitute sufficient evidence regarding the underlying net assets and the results of operations of the investee.

B) post acquisition debits and credits can be tested using statistical sampling where control risk is low.

C) brokers' advices would provide most of the evidence necessary to satisfy audit objectives pertaining to all five categories of financial statement assertions.

D) initial procedures would involve obtaining an understanding of the rationale behind management's classification of the investments.

E) analytical procedures may reduce the amount of evidence needed from other substantive tests.

A) audited financial statements of the investee generally constitute sufficient evidence regarding the underlying net assets and the results of operations of the investee.

B) post acquisition debits and credits can be tested using statistical sampling where control risk is low.

C) brokers' advices would provide most of the evidence necessary to satisfy audit objectives pertaining to all five categories of financial statement assertions.

D) initial procedures would involve obtaining an understanding of the rationale behind management's classification of the investments.

E) analytical procedures may reduce the amount of evidence needed from other substantive tests.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

65

When material in amount, a bank overdraft should be treated as a:

A) current asset.

B) current liability.

C) current contra-asset.

D) reduction in current assets.

E) reduction in current liabilities.

A) current asset.

B) current liability.

C) current contra-asset.

D) reduction in current assets.

E) reduction in current liabilities.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

66

Consider the following financial statement assertions:

A:EO ─ Existence or Occurrence

B:VA ─ Valuation or Allocation

C:C ─ Completeness

D:RO ─ Rights and Obligations

E:PD ─ Presentation and Disclosure

F:EO, C and VA

G:EO, VA, C, and PD

H:EO, VA and RO

J:EO, VA, C, RO, and PD

K:EO, VA, C and RO

I:EO, C and RO

REQUIRED: For each of the following substantive tests of balances, indicate the financial statement assertions, using the above letters to indicate your choice. Answers may be used once, more than once, or not at all.

_____

Recalculate investment revenue earned.

_____

A:EO ─ Existence or Occurrence

B:VA ─ Valuation or Allocation

C:C ─ Completeness

D:RO ─ Rights and Obligations

E:PD ─ Presentation and Disclosure

F:EO, C and VA

G:EO, VA, C, and PD

H:EO, VA and RO

J:EO, VA, C, RO, and PD

K:EO, VA, C and RO

I:EO, C and RO

REQUIRED: For each of the following substantive tests of balances, indicate the financial statement assertions, using the above letters to indicate your choice. Answers may be used once, more than once, or not at all.

_____

Recalculate investment revenue earned.

_____

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

67

Consider the following financial statement assertions:

-Inspect and count securities on hand.

_____

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

-Inspect and count securities on hand.

_____

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following would not normally be done by the auditor in connection with the bank cutoff statement?

A) receive the bank statement directly from the bank

B) trace all checks dated in the subsequent period to the outstanding check list on the reconciliation

C) trace deposits in transit on the bank reconciliation to deposits on the bank statement

D) scan the cutoff statement for unusual items

E) scan the enclosed data for unusual items

A) receive the bank statement directly from the bank

B) trace all checks dated in the subsequent period to the outstanding check list on the reconciliation

C) trace deposits in transit on the bank reconciliation to deposits on the bank statement

D) scan the cutoff statement for unusual items

E) scan the enclosed data for unusual items

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

69

The auditor may obtain the year-end bank statement directly from the bank and prepare the reconciliation personally. This step is most likely when:

A) the auditor suspects possible material misstatements.

B) it is impracticable to obtain confirmations.

C) detection risk is set at high.

D) detection risk is set at moderate.

E) detection risk is set at low.

A) the auditor suspects possible material misstatements.

B) it is impracticable to obtain confirmations.

C) detection risk is set at high.

D) detection risk is set at moderate.

E) detection risk is set at low.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

70

The standard bank confirmation, developed jointly by the AICPA, the American Bankers Association, and the Bank Administration Institute, requests information about all of the following except:

A) deposit balances.

B) loan interest rates.

C) loan balances.

D) other deposit or loan accounts that may have come to the attention of the bank official.

E) secondary endorsements.

A) deposit balances.

B) loan interest rates.

C) loan balances.

D) other deposit or loan accounts that may have come to the attention of the bank official.

E) secondary endorsements.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

71

In confirming bank deposits, the auditor need not:

A) send two copies of the standard confirmation to the bank.

B) send requests for accounts with zero balances at the end of the year.

C) have the bank return the original to the client.

D) personally mail the requests.

E) make sure the bank returns the response to him or her directly.

A) send two copies of the standard confirmation to the bank.

B) send requests for accounts with zero balances at the end of the year.

C) have the bank return the original to the client.

D) personally mail the requests.

E) make sure the bank returns the response to him or her directly.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

72

Consider the following financial statement assertions:

-Perform analytical procedures on investment balances.

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

-Perform analytical procedures on investment balances.

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

73

The auditor is most likely to review the client's bank reconciliation when the acceptable level of detection risk is:

A) high.

B) low.

C) very high.

D) very low.

E) moderate.

A) high.

B) low.

C) very high.

D) very low.

E) moderate.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

74

A surprise confirmation of accounts receivable at an interim date is useful when the auditor suspects:

A) kiting.

B) window dressing.

C) lapping.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

A) kiting.

B) window dressing.

C) lapping.

D) an attempt to conceal a cash shortage.

E) an attempt to overstate cash.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

75

Misrepresentation of the class of investment of equity securities, as held-to-maturity versus available-for-sale :

A) makes no difference because all marketable equity securities are marked to market.

B) would be readily detected by standard analytical procedures applicable to investments in equity securities.

C) would not materially effect presentation and disclosure assertions for investments.

D) is an important consideration in designing substantive tests of balances of investments in equity securities.

E) allows management to defer or accelerate the recognition of unrealized gains and losses in income.

A) makes no difference because all marketable equity securities are marked to market.

B) would be readily detected by standard analytical procedures applicable to investments in equity securities.

C) would not materially effect presentation and disclosure assertions for investments.

D) is an important consideration in designing substantive tests of balances of investments in equity securities.

E) allows management to defer or accelerate the recognition of unrealized gains and losses in income.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

76

Information concerning other arrangements with banks is usually obtained from the client's banks in separate communications. This information is likely to include:

A) compensating liabilities.

B) contingent balances.

C) lines of credit.

D) average daily balances.

E) credit limits.

A) compensating liabilities.

B) contingent balances.

C) lines of credit.

D) average daily balances.

E) credit limits.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

77

Common documents and records relating to the investing cycle would not ordinarily include:

A) stock certificates.

B) bond certificates.

C) bond indentures.

D) stock indentures.

E) brokers' statements.

A) stock certificates.

B) bond certificates.

C) bond indentures.

D) stock indentures.

E) brokers' statements.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following would not be included in the current asset section of the balance sheet?

A) bond sinking fund cash

B) cash on deposit

C) cash in bank ─ general

D) cash in bank ─ payroll

E) petty cash

A) bond sinking fund cash

B) cash on deposit

C) cash in bank ─ general

D) cash in bank ─ payroll

E) petty cash

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

79

Consider the following financial statement assertions:

-Vouch entries in investment accounts.

_____

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

-Vouch entries in investment accounts.

_____

A)EO ? Existence or Occurrence

B)VA ? Valuation or Allocation

C)C ? Completeness

D)RO ? Rights and Obligations

E)PD ? Presentation and Disclosure

F)EO, C and VA

G)EO, VA, C, and PD

H)EO, VA and RO

I)EO, C and RO

J)EO, VA, C, RO, and PD

K)EO, VA, C and RO

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

80

Audit tests to detect lapping involve which of the following?

A) confirm accounts payable

B) compare details of cash disbursements journal entries with the details of corresponding daily deposit slips

C) prepare a bank transfer schedule

D) make a surprise cash count

E) use a bank cutoff statement

A) confirm accounts payable

B) compare details of cash disbursements journal entries with the details of corresponding daily deposit slips

C) prepare a bank transfer schedule

D) make a surprise cash count

E) use a bank cutoff statement

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 91 flashcards in this deck.