Deck 9: Audit Risk, Including the Risk of Fraud

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

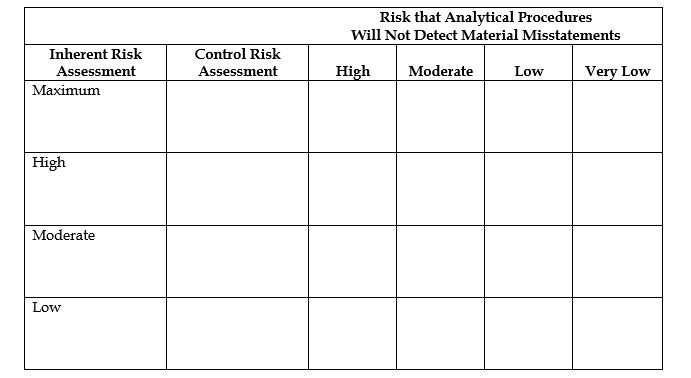

Complete the risk components matrix below, including the explanation for the asterisk.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/42

Play

Full screen (f)

Deck 9: Audit Risk, Including the Risk of Fraud

1

The assessment of inherent risk requires consideration of matters that have a pervasive effect on assertions for all or many accounts and matters that may pertain only to assertions for specific accounts. Which of the following is an example of a "specific account" matter?

A) going concern problems such as lack of sufficient working capital.

B) profitability of the entity relative to the industry.

C) sensitivity of operating results to economic factors.

D) complexity of calculations.

E) management turnover, reputation, and accounting skills.

A) going concern problems such as lack of sufficient working capital.

B) profitability of the entity relative to the industry.

C) sensitivity of operating results to economic factors.

D) complexity of calculations.

E) management turnover, reputation, and accounting skills.

D

2

There is an inverse relationship between audit risk and the amount of evidence needed.

True

3

Inherent risk cannot be greater for some assertions than for others.

False

4

The susceptibility of an assertion to a material misstatement, assuming that there are no controls, is:

A) audit risk.

B) control risk.

C) analytical procedures risk.

D) inherent risk.

E) tests of details risk.

A) audit risk.

B) control risk.

C) analytical procedures risk.

D) inherent risk.

E) tests of details risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

5

The concept of audit risk is the inverse of the concept of reasonable assurance.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

6

Auditors are required to perform risk assessment procedures in every audit to assess the risk of fraud due to both misappropriation and fraudulent financial reporting.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

7

When the preliminary audit strategy calls for the primarily substantive approach, the planned acceptable level of detection risk should be set at moderate or high.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

8

The risk that the auditor will not detect a material misstatement that exists in an assertion is:

A) control risk.

B) audit risk.

C) inherent risk.

D) rejection risk.

E) detection risk.

A) control risk.

B) audit risk.

C) inherent risk.

D) rejection risk.

E) detection risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

9

The risk that the auditor may unknowingly fail to appropriately modify his or her opinion on financial statements that are materially misstated is:

A) analytical procedures risk.

B) control risk.

C) tests of details risk.

D) inherent risk.

E) audit risk.

A) analytical procedures risk.

B) control risk.

C) tests of details risk.

D) inherent risk.

E) audit risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

10

The revised control risk is used in finalizing the design of substantive tests of transactions or tests of balances.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

11

The risk that a material misstatement that could occur in an assertion will not be prevented or detected on a timely basis by the entity's internal controls is:

A) control risk.

B) audit risk.

C) inherent risk.

D) rejection risk.

E) detection risk.

A) control risk.

B) audit risk.

C) inherent risk.

D) rejection risk.

E) detection risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

12

Detection risk is a function of the effectiveness of the controls put into place and their application by client personnel.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

13

The actual level of control risk, but not inherent risk, is directly controllable by the auditor.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

14

The auditor might choose a response to lower inherent risk for audit assertions where the auditor has developed an analytical model by examining the relationship between nonfinancial measures of the volume of business activity such as gross payroll or accrued payroll taxes, and these items are consistent with expectations.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

15

The more certain the auditor wants to be of expressing the correct opinion, the lower will be the acceptable audit risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

16

A primarily substantive approach would usually be chosen when the auditor concludes that the costs of performing additional procedures to obtain a more extensive understanding of internal controls and tests of controls to support a lower assessed level of control risk would exceed the cost of performing more extensive substantive tests.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

17

If inherent risk is assessed at the maximum, control risk as moderate and analytical procedures risk at moderate, the acceptable level of detection risk for tests of details is low.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

18

In practice, many auditors do not attempt to quantify each of the components in the audit risk model.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

19

The auditor might choose a primarily substantive approach when auditing assertions that are affected by a high degree of subjectivity or involve highly complex transactions.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

20

The auditor might choose an approach that places emphasis on inherent risk and analytical procedures when inherent risk is below the maximum and he or she can develop reliable expectations regarding the account balance.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

21

The auditor has chosen the preliminary strategy of lower assessed control risk. Which of the following is not a validly specified component of this strategy?

A) use a planned assessed level of control risk of moderate or low

B) plan tests of controls, probably testing computer controls embedded in the client's system

C) plan restrictive substantive tests

D) plan few, if any, tests of controls

E) use a planned assessed level of analytical procedures risk at a high level

A) use a planned assessed level of control risk of moderate or low

B) plan tests of controls, probably testing computer controls embedded in the client's system

C) plan restrictive substantive tests

D) plan few, if any, tests of controls

E) use a planned assessed level of analytical procedures risk at a high level

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

22

An inaccurate version of the audit risk model would imply that:

A) detection risk is inversely related to inherent risk.

B) detection risk can be determined from audit risk, inherent risk and control risk.

C) detection risk is inversely related to audit risk.

D) audit risk is related to all other risks in the model.

E) increases in the acceptable level of control risk will cause decreases in detection risk.

A) detection risk is inversely related to inherent risk.

B) detection risk can be determined from audit risk, inherent risk and control risk.

C) detection risk is inversely related to audit risk.

D) audit risk is related to all other risks in the model.

E) increases in the acceptable level of control risk will cause decreases in detection risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is a fraud mitigation procedure recently instituted in many companies?

A) Demoted compliance personnel.

B) Performance audits.

C) External audit.

D) Management code of conduct.

E) Employee hotline.

A) Demoted compliance personnel.

B) Performance audits.

C) External audit.

D) Management code of conduct.

E) Employee hotline.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

24

Following are a number of items that may have an impact on one of the components of audit risk.

REQUIRED: For each of the following, indicate the risk component that is directly affected. More than one selection may be correct. Use the following code:I:Inherent Risk

C:Control Risk

A:Analytical Procedures Risk

D:Tests of Details Risk

1.Fixed assets consist primarily of capitalized leasehold items.

2.Policies and procedures in the cash collection area appear ineffective.

3.Evidence from external sources will be obtained in testing the sales cycle.

4.The CPA firm has a sound system of quality controls.

5.In the prior year, numerous errors were detected in the account in question.

6.Limited procedures to obtain an understanding are planned.

7.The auditor has decided to consult a specialist.

8.An internal audit function exists and answers directly to the president.

9.Physical security over blank documents and accounting records is weak.

10.Extensive tests of details of balances are planned.

11.The client is in the savings and loan industry.

12.Working capital levels have declined over the past year.

13.A highly experienced audit staff has been assigned to the engagement.

14.The auditor is planning extensive compliance testing.

15.Management turnovers have been considerable this year.

REQUIRED: For each of the following, indicate the risk component that is directly affected. More than one selection may be correct. Use the following code:I:Inherent Risk

C:Control Risk

A:Analytical Procedures Risk

D:Tests of Details Risk

1.Fixed assets consist primarily of capitalized leasehold items.

2.Policies and procedures in the cash collection area appear ineffective.

3.Evidence from external sources will be obtained in testing the sales cycle.

4.The CPA firm has a sound system of quality controls.

5.In the prior year, numerous errors were detected in the account in question.

6.Limited procedures to obtain an understanding are planned.

7.The auditor has decided to consult a specialist.

8.An internal audit function exists and answers directly to the president.

9.Physical security over blank documents and accounting records is weak.

10.Extensive tests of details of balances are planned.

11.The client is in the savings and loan industry.

12.Working capital levels have declined over the past year.

13.A highly experienced audit staff has been assigned to the engagement.

14.The auditor is planning extensive compliance testing.

15.Management turnovers have been considerable this year.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

25

A risk components matrix or its equivalent is necessary whenever the auditor uses:

A) quantitative expressions for risk.

B) nonqualitative expressions for risk.

C) the risk model in planning an audit.

D) a lower assessment of control risk or inherent risk.

E) nonquantitative expressions for risk.

A) quantitative expressions for risk.

B) nonqualitative expressions for risk.

C) the risk model in planning an audit.

D) a lower assessment of control risk or inherent risk.

E) nonquantitative expressions for risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

26

Following are the three possible audit strategies discussed in the text.

A.A Primarily Substantive Approach

B.A Lower Assessed Level of Control Risk Approach

C.A Response to Lower Inherent Risk Approach

REQUIRED: Using the corresponding letters from the list above, match the audit strategy with the audit strategy components listed below. (Items may be used more than once.)

1.Plan few, if any, tests of controls.

2.Plan to obtain a minimum understanding of relevant portions of internal

controls.

3.Obtain extensive knowledge of the client's business processes relevant to the

assertion.

4.Use a planned assessed level of control risk of moderate or low.

A.A Primarily Substantive Approach

B.A Lower Assessed Level of Control Risk Approach

C.A Response to Lower Inherent Risk Approach

REQUIRED: Using the corresponding letters from the list above, match the audit strategy with the audit strategy components listed below. (Items may be used more than once.)

1.Plan few, if any, tests of controls.

2.Plan to obtain a minimum understanding of relevant portions of internal

controls.

3.Obtain extensive knowledge of the client's business processes relevant to the

assertion.

4.Use a planned assessed level of control risk of moderate or low.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

27

A.Under a lower assessed level of control risk approach, what audit strategy components does the auditor specify?

B.Under a primarily substantive approach, what audit strategy components does the auditor specify?

B.Under a primarily substantive approach, what audit strategy components does the auditor specify?

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

28

The preliminary audit strategy for each assertion:

A) is a detailed specification of auditing procedures.

B) must be set before risk assessment is completed.

C) represents a tentative audit approach.

D) will be uniform throughout the audit.

E) represents a committed audit approach.

A) is a detailed specification of auditing procedures.

B) must be set before risk assessment is completed.

C) represents a tentative audit approach.

D) will be uniform throughout the audit.

E) represents a committed audit approach.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following statements about fraud is not true?

A) Fraud is defined in generally accepted auditing standards as any act that results in a material misstatement in financial statements that are the subject of an audit.

B) Auditors are concerned about two types of misstatements that are relevant to the auditor's consideration of fraud.

C) The types of fraud that are the least frequent are also the most expensive.

D) The fraud triangle includes opportunity, incentives, pressures, attitudes and rationalization.

E) Auditors should conduct discussions about management overrides of internal controls with employees having varying levels of authority including personnel not directly involved in the financial reporting process

A) Fraud is defined in generally accepted auditing standards as any act that results in a material misstatement in financial statements that are the subject of an audit.

B) Auditors are concerned about two types of misstatements that are relevant to the auditor's consideration of fraud.

C) The types of fraud that are the least frequent are also the most expensive.

D) The fraud triangle includes opportunity, incentives, pressures, attitudes and rationalization.

E) Auditors should conduct discussions about management overrides of internal controls with employees having varying levels of authority including personnel not directly involved in the financial reporting process

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

30

The risk that a material misstatement that could occur in an assertion will not be prevented or detected on a timely basis by the entity's internal controls is

A) control risk.

B) analytical procedures risk.

C) tests of details risk.

D) inherent risk.

E) audit risk.

A) control risk.

B) analytical procedures risk.

C) tests of details risk.

D) inherent risk.

E) audit risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is not an example of a significant inherent risk?

A) Management override of internal controls.

B) The impact of technological developments.

C) Inadequate accounting skills.

D) Management turnover.

E) Contentious accounting issues.

A) Management override of internal controls.

B) The impact of technological developments.

C) Inadequate accounting skills.

D) Management turnover.

E) Contentious accounting issues.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is an example of how an analytical procedure may be helpful in identifying accounts and assertions that are likely to contain misstatements?

A) An improvement in the current ratio combined with an increase in the quick ratio.

B) An increase in gross sales combined with an increase in earnings per share.

C) Susceptibility of misappropriation.

D) An increase in gross margins combined with an increase in the number of inventory turn days.

E) Difficult-to-audit accounts or transactions.

A) An improvement in the current ratio combined with an increase in the quick ratio.

B) An increase in gross sales combined with an increase in earnings per share.

C) Susceptibility of misappropriation.

D) An increase in gross margins combined with an increase in the number of inventory turn days.

E) Difficult-to-audit accounts or transactions.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

33

Complete the risk components matrix below, including the explanation for the asterisk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

34

The assessment of inherent risk requires consideration of matters that have a pervasive effect on assertions for all or many accounts and matters that may pertain only to assertions for specific accounts. Which of the following is an example of a "pervasive effects" matter?

A) complexity of calculations.

B) management turnover, reputation, and accounting skills.

C) susceptibility to misappropriation.

D) sensitivity of operating results to economic factors.

E) difficult-to-audit accounts or transactions.

A) complexity of calculations.

B) management turnover, reputation, and accounting skills.

C) susceptibility to misappropriation.

D) sensitivity of operating results to economic factors.

E) difficult-to-audit accounts or transactions.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

35

For which of the following accounts is the primarily substantive testing strategy least likely?

A) bonds payable

B) trade accounts payable

C) equipment

D) capital stock

E) machinery

A) bonds payable

B) trade accounts payable

C) equipment

D) capital stock

E) machinery

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

36

The auditor has some control over:

A) the assessed level of inherent risk.

B) the actual level of inherent risk.

C) both the actual level and the assessed levels of inherent risk.

D) neither the actual level nor the assessed level of inherent risk.

E) the projected level of inherent risk.

A) the assessed level of inherent risk.

B) the actual level of inherent risk.

C) both the actual level and the assessed levels of inherent risk.

D) neither the actual level nor the assessed level of inherent risk.

E) the projected level of inherent risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

37

The auditor has chosen the preliminary strategy of primarily substantive testing. Which of the following is not a validly specified component of this strategy?

A) set control risk at a high level

B) plan tests of controls, probably testing computer controls embedded in the client's system

C) plan few, if any, tests of controls

D) plan extensive substantive tests

E) plan to obtain a minimum understanding of relevant portions of internal controls.

A) set control risk at a high level

B) plan tests of controls, probably testing computer controls embedded in the client's system

C) plan few, if any, tests of controls

D) plan extensive substantive tests

E) plan to obtain a minimum understanding of relevant portions of internal controls.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following risk factors is an example of an assertion specific inherent risk factor?

A) Management override of internal controls.

B) The impact of technological developments.

C) Inadequate accounting skills.

D) Management turnover.

E) Contentious accounting issues.

A) Management override of internal controls.

B) The impact of technological developments.

C) Inadequate accounting skills.

D) Management turnover.

E) Contentious accounting issues.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

39

If inherent risk is assessed as low, control risk is assessed as low and analytical procedures risk is very low, the acceptable levels of test of details risk would be:

A) Maximum

B) High

C) Moderate

D) Low

E) So low that substantive tests of details may not be necessary.

A) Maximum

B) High

C) Moderate

D) Low

E) So low that substantive tests of details may not be necessary.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

40

The auditor has some control over:

A) the actual level of control risk.

B) the assessed level of control risk.

C) both the actual level and the assessed levels of control risk.

D) neither the actual level nor the assessed level of control risk.

E) the projected level of control risk.

A) the actual level of control risk.

B) the assessed level of control risk.

C) both the actual level and the assessed levels of control risk.

D) neither the actual level nor the assessed level of control risk.

E) the projected level of control risk.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

41

For each one of the following risk factors relating to misstatements arising from fraudulent reporting, identify the appropriate category.

1.Inability to generate cash flows from operations while reporting earnings and earnings growth.

2.High degree of competition or market saturation, accompanied by declining margins.

3.High turnover of senior management, counsel, or board members.

4.Difficulty in determining the organization or individual(s) that control(s) the entity.

5.Strained relationship between management and the current or predecessor auditor.

6.Declining industry with increasing business failures and significant declines in customer demand.

1.Inability to generate cash flows from operations while reporting earnings and earnings growth.

2.High degree of competition or market saturation, accompanied by declining margins.

3.High turnover of senior management, counsel, or board members.

4.Difficulty in determining the organization or individual(s) that control(s) the entity.

5.Strained relationship between management and the current or predecessor auditor.

6.Declining industry with increasing business failures and significant declines in customer demand.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

43

Match between columns

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 42 flashcards in this deck.