Deck 12: Audit Procedures in Response to Assessed Risks: Substantive Tests

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

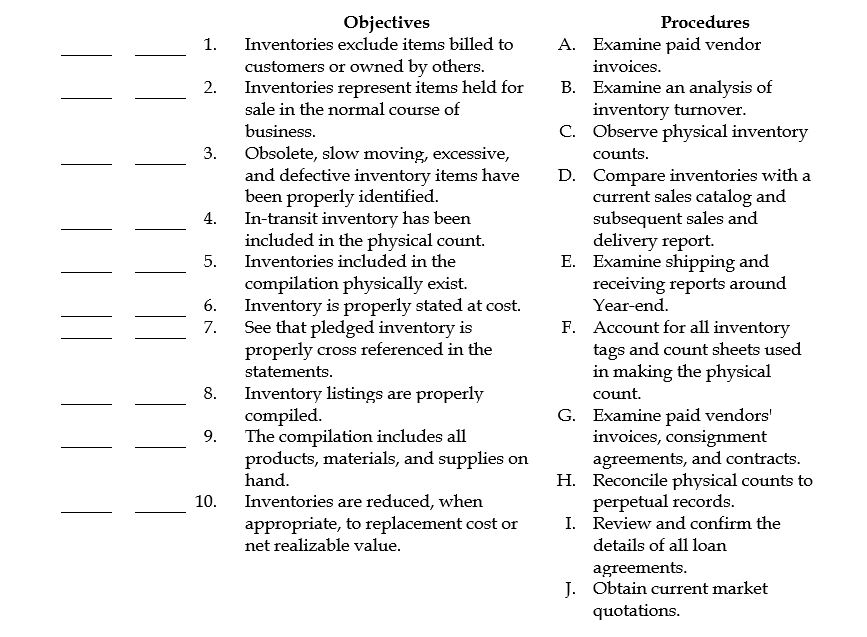

Following is a list of specific audit objectives, accompanied by a list of possible audit procedures for inventory.

REQUIRED: For each specific objective, indicate the assertion from which it was derived, and the audit procedure that best meets that objective. (Each procedure can only be used once.) Use the appropriate letters for the procedures and the following letters for the assertions:

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

REQUIRED: For each specific objective, indicate the assertion from which it was derived, and the audit procedure that best meets that objective. (Each procedure can only be used once.) Use the appropriate letters for the procedures and the following letters for the assertions:

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/81

Play

Full screen (f)

Deck 12: Audit Procedures in Response to Assessed Risks: Substantive Tests

1

For some assertions, analytical procedures may be more effective in detecting misstatement than tests of detail.

True

2

The traditional audit focuses on the test of details of balances for income statement accounts rather than balance sheet accounts.

False

3

Analytical procedures are a required form of substantive testing in the testing phase of the audit.

False

4

The use of generalized audit software enables the auditor to deal effectively with large quantities of data.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

5

In auditing identified related party transactions, the auditor is expected to determine whether a particular transaction would have occurred if the parties had not been related or what the exchange price and terms would have been.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

6

In some audits, the auditor may elect to use analytical procedures as the only direct test of some income statement balances.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

7

Detection risk is inversely related to assessed levels of control risk and inherent risk.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

8

The focus of tests of details of transactions is on finding deviations from control policies and procedures.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

9

Measuring the amount of monetary errors in transactions and balances is a primary purpose of substantive tests.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

10

Smaller amounts of sampling risk should result in larger sample size.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

11

An accounting estimate is a guess in the absence of an exact measurement.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

12

Analytical procedures are usually the most costly tests to perform.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

13

Generalized audit software packages available at high cost from software vendors.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

14

When the acceptable level of detection risk for an assertion is low, the substantive tests will usually be performed at or near the balance sheet date.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

15

When the preliminary audit strategy calls for the primarily substantive approach, planned detection risk should be set at moderate or high.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

16

An auditor must always an independent expectation in the process of obtaining evidence of reasonableness for every material estimate.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

17

Evidence for related party transactions should extend beyond inquiry of management.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

18

The more homogeneous the population, the smaller the sample size should be.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

19

Professional standards do not allow the performing of substantive audit procedures at an interim date.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

20

Detection risk can be broken down into tests of controls risk and analytical procedures risk.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

21

AU 342.09 explains that the auditor should normally concentrate on the key factors and assumptions used by management including all of the following except those that are:

A) insignificant to the accounting estimate.

B) sensitive to variations.

C) subject to misstatement and bias.

D) deviations from historical patterns.

E) susceptible to misstatement and bias.

A) insignificant to the accounting estimate.

B) sensitive to variations.

C) subject to misstatement and bias.

D) deviations from historical patterns.

E) susceptible to misstatement and bias.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

22

The extent of substantive tests, in practice means the length of time during which substantive tests are to be performed.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

23

In performing tests of details of balances, the auditor would obtain the bank statement directly from the bank, prepare the bank reconciliation, and verify all reconciling items and mathematical accuracy if detection risk was:

A) very high.

B) high.

C) moderate.

D) low.

E) very low.

A) very high.

B) high.

C) moderate.

D) low.

E) very low.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

24

SAS 57 lists all of the following objectives in evaluating accounting estimates except:

A) the accounting estimates follow standard industry practices.

B) all accounting estimates that could be material to the financial statements have been developed.

C) the accounting estimates are reasonable in the circumstances.

D) the accounting estimates are presented in conformity with applicable accounting principles.

E) the accounting estimates are properly disclosed.

A) the accounting estimates follow standard industry practices.

B) all accounting estimates that could be material to the financial statements have been developed.

C) the accounting estimates are reasonable in the circumstances.

D) the accounting estimates are presented in conformity with applicable accounting principles.

E) the accounting estimates are properly disclosed.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

25

Tests of details of balances generally tend to be the:

A) most costly, and least effective audit procedures.

B) most costly, and most effective audit procedures.

C) least costly, yet most effective audit procedures.

D) least costly, and least effective audit procedures.

E) least costly, and least efficient audit procedures.

A) most costly, and least effective audit procedures.

B) most costly, and most effective audit procedures.

C) least costly, yet most effective audit procedures.

D) least costly, and least effective audit procedures.

E) least costly, and least efficient audit procedures.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

26

The primary means by which the auditor meets the requirements of the third field work standard is through:

A) designing substantive tests.

B) gathering evidence to support the assessed level of control risk.

C) preparing a detailed audit program.

D) evaluating the results of substantive tests.

E) performing substantive tests.

A) designing substantive tests.

B) gathering evidence to support the assessed level of control risk.

C) preparing a detailed audit program.

D) evaluating the results of substantive tests.

E) performing substantive tests.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

27

Who is responsible for establishing the process and controls for preparing accounting estimates?

A) the independent auditor

B) the internal auditor

C) management

D) the audit committee

E) the controller

A) the independent auditor

B) the internal auditor

C) management

D) the audit committee

E) the controller

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

28

The least costly form of testing is usually:

A) tests of controls.

B) tests of detail of transactions.

C) analytical procedures.

D) tests of detail of balances.

E) tests of compliance.

A) tests of controls.

B) tests of detail of transactions.

C) analytical procedures.

D) tests of detail of balances.

E) tests of compliance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

29

Revision of the planned level of detection risk will be necessary whenever:

A) accounts are affected by more than one transaction class.

B) the multiple control risk assessments for the same account balance assertion differ.

C) the lower assessed control risk approach is used.

D) the final assessed control risk does not support the planned level.

E) the final assessed control risk is not the same as the actual level.

A) accounts are affected by more than one transaction class.

B) the multiple control risk assessments for the same account balance assertion differ.

C) the lower assessed control risk approach is used.

D) the final assessed control risk does not support the planned level.

E) the final assessed control risk is not the same as the actual level.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

30

Use of auditor judgment or of a risk matrix is necessary in revising planned detection risk whenever:

A) risk assessments are not quantified.

B) assessed control risk at the account balance level does not support the planned level of control risk.

C) control risk is assessed above the minimum.

D) control risk is assessed below the maximum.

E) tests of controls reveal substantial deviations from prescribed policies.

A) risk assessments are not quantified.

B) assessed control risk at the account balance level does not support the planned level of control risk.

C) control risk is assessed above the minimum.

D) control risk is assessed below the maximum.

E) tests of controls reveal substantial deviations from prescribed policies.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

31

The auditor would prepare a bank reconciliation using the bank statement obtained from the client and verify major reconciling items and mathematical accuracy when detection risk is:

A) very high.

B) high.

C) moderate.

D) very low.

E) low.

A) very high.

B) high.

C) moderate.

D) very low.

E) low.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

32

Confirmation and direct knowledge by the auditor are most associated with:

A) analytical procedures.

B) tests of controls.

C) tests of details of balances.

D) tests of details of transactions.

E) tests of compliance.

A) analytical procedures.

B) tests of controls.

C) tests of details of balances.

D) tests of details of transactions.

E) tests of compliance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

33

Which standards of fieldwork primarily affect substantive tests and tests of controls?

A) The first standard primarily affects substantive tests and the third primarily affects tests of controls.

B) The second standard primarily affects substantive tests and the third primarily affects tests of controls.

C) The third standard primarily affects substantive tests and the second primarily affects tests of controls.

D) All of the fieldwork standards equally affect substantive tests and tests of controls.

E) None of the fieldwork standards affect substantive tests or tests of controls.

A) The first standard primarily affects substantive tests and the third primarily affects tests of controls.

B) The second standard primarily affects substantive tests and the third primarily affects tests of controls.

C) The third standard primarily affects substantive tests and the second primarily affects tests of controls.

D) All of the fieldwork standards equally affect substantive tests and tests of controls.

E) None of the fieldwork standards affect substantive tests or tests of controls.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

34

Assume the preliminary audit strategy was based on a planned assessed level of control risk at a low level. Based on the final assessed level of control risk, the auditor would need to move substantive tests from interim to year-end and increase the extent of tests of details in order to accommodate a lower acceptable level of detection risk if:

A) the final assessed level of control risk was moderate or high.

B) the final assessed level of control risk was low or very low.

C) the final assessed level of inherent risk was high or very high.

D) the final assessed level of inherent risk was low or very low.

E) the final assessed level of analytical procedures risk was moderate of high.

A) the final assessed level of control risk was moderate or high.

B) the final assessed level of control risk was low or very low.

C) the final assessed level of inherent risk was high or very high.

D) the final assessed level of inherent risk was low or very low.

E) the final assessed level of analytical procedures risk was moderate of high.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

35

An inaccurate form of the audit risk model would show that:

A) detection risk can be determined from audit risk, inherent risk, and control risk.

B) detection risk is inversely related to audit risk.

C) increases in control risk will cause decreases in detection risk.

D) audit risk is directly related to all other risks in the model.

E) detection risk is inversely related to inherent risk.

A) detection risk can be determined from audit risk, inherent risk, and control risk.

B) detection risk is inversely related to audit risk.

C) increases in control risk will cause decreases in detection risk.

D) audit risk is directly related to all other risks in the model.

E) detection risk is inversely related to inherent risk.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

36

An auditor has computed the revised level of detection risk by direct use of the audit risk model. This means that the auditor must have:

A) assessed control risk at the maximum.

B) used a flowchart to document the understanding of the complete internal control structure.

C) used the primarily substantive approach in planning the audit.

D) quantified all the relevant risk assessments.

E) assessed detection risk at the minimum.

A) assessed control risk at the maximum.

B) used a flowchart to document the understanding of the complete internal control structure.

C) used the primarily substantive approach in planning the audit.

D) quantified all the relevant risk assessments.

E) assessed detection risk at the minimum.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

37

When evaluating the planned level of substantive tests for each significant financial statement assertion, the auditor will consider the evidence obtained from all of the following except:

A) procedures to understand the business and industry and related analytical procedures that have been completed.

B) evidence about the effectiveness of internal controls gained while obtaining an understanding of internal controls.

C) the assessment of detection risk.

D) the assessment of inherent risk.

E) evidence of effectiveness of computer control procedures and related manual follow-up.

A) procedures to understand the business and industry and related analytical procedures that have been completed.

B) evidence about the effectiveness of internal controls gained while obtaining an understanding of internal controls.

C) the assessment of detection risk.

D) the assessment of inherent risk.

E) evidence of effectiveness of computer control procedures and related manual follow-up.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

38

In practice, the use of analytical procedures has proven to be:

A) totally ineffective in detecting misstatements.

B) quite effective in detecting the largest of misstatements.

C) useful in the planning phase, but not in the testing phase of the audit.

D) too costly to apply in most audit situations.

E) moderately effective in detecting most misstatements.

A) totally ineffective in detecting misstatements.

B) quite effective in detecting the largest of misstatements.

C) useful in the planning phase, but not in the testing phase of the audit.

D) too costly to apply in most audit situations.

E) moderately effective in detecting most misstatements.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

39

In performing tests of details of balances, the auditor would scan the client-prepared bank reconciliation, and verify the mathematical accuracy of the reconciliation if detection risk was:

A) very high.

B) high.

C) moderate.

D) low.

E) very low.

A) very high.

B) high.

C) moderate.

D) low.

E) very low.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

40

Tests of details of transactions generally use evidence from:

A) documents obtained directly from external sources.

B) direct observation on the part of the auditor.

C) inquiry directed to top management personnel.

D) documents found in the client's files.

E) the body of the client rep letter.

A) documents obtained directly from external sources.

B) direct observation on the part of the auditor.

C) inquiry directed to top management personnel.

D) documents found in the client's files.

E) the body of the client rep letter.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

41

Each audit program should have a column for all of the following except:

A) audit procedures to be performed.

B) a cross-reference to other working papers containing the evidence obtained from each procedure.

C) the initials of the auditor who performed each procedure.

D) the date the performance of the procedure was completed.

E) the test of controls related to each procedure.

A) audit procedures to be performed.

B) a cross-reference to other working papers containing the evidence obtained from each procedure.

C) the initials of the auditor who performed each procedure.

D) the date the performance of the procedure was completed.

E) the test of controls related to each procedure.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

42

Under which set of circumstances may it not be necessary to perform tests of details?

A) When inherent risk is low and the acceptable level of detection risk is very high.

B) When the cost of tests of details outweigh the benefits of performing them.

C) When the results of substantive analytical procedures conform to expectations and the acceptable level of detection risk for the assertion is high.

D) When the results of substantive analytical procedures conform to expectations and the acceptable level of detection risk for the assertion is low or very low.

E) A minimum level of tests of details must always be performed

A) When inherent risk is low and the acceptable level of detection risk is very high.

B) When the cost of tests of details outweigh the benefits of performing them.

C) When the results of substantive analytical procedures conform to expectations and the acceptable level of detection risk for the assertion is high.

D) When the results of substantive analytical procedures conform to expectations and the acceptable level of detection risk for the assertion is low or very low.

E) A minimum level of tests of details must always be performed

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following is not an example of an initial procedure to be performed before other substantive tests are performed?

A) Tracing beginning balances in the general ledger to the closing balances in the prior year's trial balance.

B) Summing and agreeing detail balances in subsidiary ledgers to the general ledger.

C) Referring to prior year's workpapers.

D) Understanding the economic substance of transactions.

E) Ascertaining the accounting principals used in the preceding period.

A) Tracing beginning balances in the general ledger to the closing balances in the prior year's trial balance.

B) Summing and agreeing detail balances in subsidiary ledgers to the general ledger.

C) Referring to prior year's workpapers.

D) Understanding the economic substance of transactions.

E) Ascertaining the accounting principals used in the preceding period.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following income statement accounts is least likely to be subjected to extensive detailed tests of balances?

A) legal and professional fees

B) officers' salaries

C) employees' wages

D) cost of sales

E) contributions

A) legal and professional fees

B) officers' salaries

C) employees' wages

D) cost of sales

E) contributions

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

45

The balance sheet account Inventories is related to which one of the following income statement accounts?

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

46

The audit program is basically a list of:

A) detailed audit objectives.

B) account balances and their related assertions.

C) control policies and procedures to be tested.

D) audit procedures to be performed.

E) audit controls.

A) detailed audit objectives.

B) account balances and their related assertions.

C) control policies and procedures to be tested.

D) audit procedures to be performed.

E) audit controls.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

47

The auditor would be least likely to perform early substantive testing of account balances when:

A) a number of significant deviations from control policies and procedures were detected during tests of controls.

B) variance reports do not distinguish between price and quantity variances.

C) due to economic factors, fourth quarter activity this year is expected to be somewhat lower than prior year's.

D) the client uses a natural business year instead of the calendar year.

E) the taking of the client's inventory is performed at an early date.

A) a number of significant deviations from control policies and procedures were detected during tests of controls.

B) variance reports do not distinguish between price and quantity variances.

C) due to economic factors, fourth quarter activity this year is expected to be somewhat lower than prior year's.

D) the client uses a natural business year instead of the calendar year.

E) the taking of the client's inventory is performed at an early date.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

48

An audit program should be sufficiently detailed to provide all of the following except:

A) evidential support for the audit opinion.

B) an outline of the work to be done.

C) a record of the work performed.

D) a basis for controlling the audit.

E) a basis for supervising the audit.

A) evidential support for the audit opinion.

B) an outline of the work to be done.

C) a record of the work performed.

D) a basis for controlling the audit.

E) a basis for supervising the audit.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

49

In practice, early substantive testing of account balances is done only when:

A) the client has a calendar year end.

B) the client has reporting requirements under the Securities Acts.

C) evidence indicates effective control policies and procedures.

D) the primarily substantive approach is taken.

E) internal controls are weak.

A) the client has a calendar year end.

B) the client has reporting requirements under the Securities Acts.

C) evidence indicates effective control policies and procedures.

D) the primarily substantive approach is taken.

E) internal controls are weak.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following assertions is least likely to be tested exclusively at an interim date?

A) existence or occurrence for plant assets.

B) valuation for cash.

C) completeness for accounts payable.

D) existence or occurrence for inventory.

E) rights and obligations for inventory.

A) existence or occurrence for plant assets.

B) valuation for cash.

C) completeness for accounts payable.

D) existence or occurrence for inventory.

E) rights and obligations for inventory.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

51

In practice, extent of testing applies:

A) exclusively to the number of items tested.

B) to both the number of items tested and the number of tests performed.

C) exclusively to the number of substantive tests performed.

D) to both the number of items tested and the nature of the tests performed.

E) to both the nature of items tested and the number of tests performed.

A) exclusively to the number of items tested.

B) to both the number of items tested and the number of tests performed.

C) exclusively to the number of substantive tests performed.

D) to both the number of items tested and the nature of the tests performed.

E) to both the nature of items tested and the number of tests performed.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

52

In obtaining evidence concerning the cash balance, the auditor performs the following procedures: Scan client-prepared bank reconciliations and verify the mathematical accuracy of the reconciliation. In this case, it is likely that:

A) detection risk is set at moderate to high.

B) detection risk is set at low to very low.

C) control risk is set at slightly below maximum to maximum.

D) control risk is set at moderate to high.

E) control risk is set at minimum to high.

A) detection risk is set at moderate to high.

B) detection risk is set at low to very low.

C) control risk is set at slightly below maximum to maximum.

D) control risk is set at moderate to high.

E) control risk is set at minimum to high.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

53

In obtaining evidence concerning the cash balance, the auditor performs the following procedures: Obtain bank statements directly from bank, prepare bank reconciliation, and verify all reconciling items. In this case, it is most likely that:

A) detection risk is set at moderate to high.

B) detection risk is set at low to very low.

C) inherent risk is set at low.

D) control risk is set at moderate to low.

E) detection risk is set at minimum to moderate.

A) detection risk is set at moderate to high.

B) detection risk is set at low to very low.

C) inherent risk is set at low.

D) control risk is set at moderate to low.

E) detection risk is set at minimum to moderate.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

54

The auditor is performing substantive tests several months before the end of the year. This most likely means that:

A) inherent risk is set at moderate to high.

B) detection risk is set at low to very low.

C) control risk is set at slightly below maximum to maximum.

D) control risk is set at maximum.

E) detection risk is set at moderate to high.

A) inherent risk is set at moderate to high.

B) detection risk is set at low to very low.

C) control risk is set at slightly below maximum to maximum.

D) control risk is set at maximum.

E) detection risk is set at moderate to high.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

55

The balance sheet account Accounts Receivable is related to which one of the following income statement accounts?

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

56

When substantive tests are performed before the balance sheet date, at a minimum the auditor should, at or after the balance sheet date:

A) obtain a letter from management stating that no significant changes occurred in the account balances between the two dates.

B) perform analytical procedures, including comparison of the account balances at the two dates.

C) reconfirm all balances that were confirmed at interim.

D) confirm all balances that were not confirmed at interim.

E) perform tests of reasonableness on all balances that were not confirmed at interim.

A) obtain a letter from management stating that no significant changes occurred in the account balances between the two dates.

B) perform analytical procedures, including comparison of the account balances at the two dates.

C) reconfirm all balances that were confirmed at interim.

D) confirm all balances that were not confirmed at interim.

E) perform tests of reasonableness on all balances that were not confirmed at interim.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

57

Compared to balance sheet accounts, the audit of income statement accounts generally relies more heavily on:

A) tests of detail of balances.

B) tests of detail of transactions.

C) analytical procedures.

D) both tests of detail of balances and of transactions.

E) tests of controls.

A) tests of detail of balances.

B) tests of detail of transactions.

C) analytical procedures.

D) both tests of detail of balances and of transactions.

E) tests of controls.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

58

Extensive tests of detail for an income statement account is least likely to be required when:

A) inherent risk is high.

B) control risk is high.

C) analytical procedures reveal some unexpected fluctuations.

D) detection risk is high.

E) the account requires analysis.

A) inherent risk is high.

B) control risk is high.

C) analytical procedures reveal some unexpected fluctuations.

D) detection risk is high.

E) the account requires analysis.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

59

The balance sheet account Investments is related to which one of the following income statement accounts?

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

A) Investment Income

B) Cost of Sales

C) Interest Expense

D) Depreciation Expense

E) Sales

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

60

The decision on the part of the auditor to perform substantive tests during the interim period will be based upon:

A) staffing considerations.

B) the cooperation of client personnel, especially internal auditors.

C) audit risk control and cost effectiveness.

D) the approach followed in the past.

E) his or her own availability.

A) staffing considerations.

B) the cooperation of client personnel, especially internal auditors.

C) audit risk control and cost effectiveness.

D) the approach followed in the past.

E) his or her own availability.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

61

Following is a list of specific audit objectives, accompanied by a list of possible audit procedures for inventory.

REQUIRED: For each specific objective, indicate the assertion from which it was derived, and the audit procedure that best meets that objective. (Each procedure can only be used once.) Use the appropriate letters for the procedures and the following letters for the assertions:

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

REQUIRED: For each specific objective, indicate the assertion from which it was derived, and the audit procedure that best meets that objective. (Each procedure can only be used once.) Use the appropriate letters for the procedures and the following letters for the assertions:

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

62

Why is the understanding of the client's business and industry important in tests of details for accounting estimates?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

63

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine consignment agreements.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine consignment agreements.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

64

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Inquire of accounting and purchasing personnel about unrecorded payables.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Inquire of accounting and purchasing personnel about unrecorded payables.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

65

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine vehicle registration forms to determine the registered owner.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine vehicle registration forms to determine the registered owner.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

66

Describe the contents and use of an audit program.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

67

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Trace beginning balance for accounts payable to prior year's working papers.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Trace beginning balance for accounts payable to prior year's working papers.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

68

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Reperform check on accuracy of sales invoice pricing.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Reperform check on accuracy of sales invoice pricing.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

69

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Obtain the market value of short term securities as of the balance sheet date from

published records.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Obtain the market value of short term securities as of the balance sheet date from

published records.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

70

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Observe procedures, including segregation of duties, for approving sales orders.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Observe procedures, including segregation of duties, for approving sales orders.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

71

In auditing related party transactions, the auditor is expected to determine:

A) whether a particular transaction would have occurred if the parties had not been related.

B) what the exchange price and terms would have been if the parties had not been related.

C) if the related parties acted fraudulently.

D) the substance of the transaction and its effects on the financial statements.

E) the nature of the transaction by simply inquiring of management.

A) whether a particular transaction would have occurred if the parties had not been related.

B) what the exchange price and terms would have been if the parties had not been related.

C) if the related parties acted fraudulently.

D) the substance of the transaction and its effects on the financial statements.

E) the nature of the transaction by simply inquiring of management.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

72

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Test the aging of accounts receivable, discussing long-overdue accounts with the

credit manager.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Test the aging of accounts receivable, discussing long-overdue accounts with the

credit manager.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

73

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Inspect major new additions to plant assets during the current period.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Inspect major new additions to plant assets during the current period.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

74

The nature of substantive tests refers to the type and effectiveness of the auditing procedures to be performed.

REQUIRED: Identify and discuss the three types of substantive procedures, addressing the

relative effectiveness and cost of each.

REQUIRED: Identify and discuss the three types of substantive procedures, addressing the

relative effectiveness and cost of each.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

75

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Select vendor accounts with high activity during the year, and low balance at

year-end for confirmation.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Select vendor accounts with high activity during the year, and low balance at

year-end for confirmation.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

76

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Ascertain that the financial statements comply with the industry practice of

presenting a classified balance sheet.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Ascertain that the financial statements comply with the industry practice of

presenting a classified balance sheet.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

77

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Trace shipping documents to sales invoices.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Trace shipping documents to sales invoices.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

78

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Select high dollar items from the perpetual inventory records for

inspection/counting during the physical inventory.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Select high dollar items from the perpetual inventory records for

inspection/counting during the physical inventory.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

79

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine check register for the month following year end for disbursements

relating to the audit period.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Examine check register for the month following year end for disbursements

relating to the audit period.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

80

Substantive tests must be designed to tests specific audit objectives.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Review bond indenture agreement and ascertain client compliance with any

restrictive covenants.

REQUIRED: For the following specific audit procedures, indicate the assertion that is being tested. Use the following letters, placing your response in the space provideD.

A.Existence or occurrence

B.Completeness

C.Valuation or allocation

D.Rights and obligations

E.Presentation and disclosure

Review bond indenture agreement and ascertain client compliance with any

restrictive covenants.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 81 flashcards in this deck.