Deck 3: Professional Ethics

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

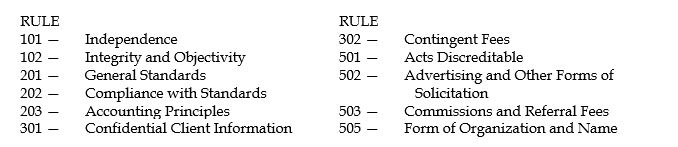

Question

Question

Question

Question

Question

Question

Question

For each of the following actions by a member CPA, indicate (1) the rule of conduct that is applicable and (2) whether the actions does (yes) or does not (no) violate the rule. You may identify the rule by number on your answer sheet. Your selections can be made from the following list:  1.Discriminates in employment.

1.Discriminates in employment.

2.Makes recommendations but not the decisions in an MCS engagement for a nonpublic client.

3.Permits a non-CPA to be the chairman of the board of a CPA firm organized as a professional corporation.

4.Fails to make inquiries in a review of interim financial information.

5.Accepts a commission from a vendor, with the permission of the audit client, for

recommending the vendor's product.

6.Indicates that he will perform the audit of a city's united fund charity for a nominal fee.

7.Transfers working papers, with the client's permission, to the client's new auditors.

8.Subordinates his judgment in favor of the client in tax practice when there is little support for the client's position.

9.Indicates the number of partners, CPAs and offices in his or her firm in an advertisement.

10.States that the fee in a tax case will be based on the amount of tax saving realized.

11.Fails to conform to a recently issued SAS, which has an immaterial effect on the financial statements.

12.A personnel manager in the office doing the audit of a client has a financial interest in the client.

13.Fails to adequately plan and supervise an MCS engagement.

14.Agrees to serve as an honorary director of a charitable foundation.

15.Knowingly misrepresents facts in an engagement.

1.Discriminates in employment.2.Makes recommendations but not the decisions in an MCS engagement for a nonpublic client.

3.Permits a non-CPA to be the chairman of the board of a CPA firm organized as a professional corporation.

4.Fails to make inquiries in a review of interim financial information.

5.Accepts a commission from a vendor, with the permission of the audit client, for

recommending the vendor's product.

6.Indicates that he will perform the audit of a city's united fund charity for a nominal fee.

7.Transfers working papers, with the client's permission, to the client's new auditors.

8.Subordinates his judgment in favor of the client in tax practice when there is little support for the client's position.

9.Indicates the number of partners, CPAs and offices in his or her firm in an advertisement.

10.States that the fee in a tax case will be based on the amount of tax saving realized.

11.Fails to conform to a recently issued SAS, which has an immaterial effect on the financial statements.

12.A personnel manager in the office doing the audit of a client has a financial interest in the client.

13.Fails to adequately plan and supervise an MCS engagement.

14.Agrees to serve as an honorary director of a charitable foundation.

15.Knowingly misrepresents facts in an engagement.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

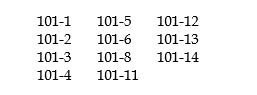

The thirteen current Interpretations of Rule 101 are listed below. Place the following numbers in the spaces provided:

1.Explains circumstances in which independence may be considered to be

impaired as a result of litigation or the expressed intention to commence litigation.

2.Provides guidance on how various alternatives to "traditional structures" effect

independence due to changes in the manner in which CPAs are structuring their practices.

3.Addresses financial interests and business relationships that impair

independence.

4.A member issuing a report on a governmental client's general purpose financial

statements generally must be independent of the client, but independence is not required with respect to a related organization if the client is not financially accountable for the organization and the required disclosure does not include financial information.

5.Provides guidance when a member is asked to serve as an honorary or trustee

for an attest client.

6.Independence will generally be considered to be impaired if, during the period

of a professional engagement or at the time of expressing an opinion, a member's firm had any joint business activity with the client that was material to the CPA's firm or to the client.

7.Provides guidance on independence for engagements that are more limited in

scope than an audit of general purpose financial statements.

8.Explains various ways in which a financial interest in a nonclient that has a

significant influence on a client may impair independence with respect to a client.

9.Outlines important responsibility the client's management must take in order to

preserve independence.

10.Explains some specific exceptions to the general rule concerning the situation in

which a member has a loan to or from the enterprise or any officer, director, or principal stockholder of the enterprise.

11.Addresses circumstances in which the activities of a former partner or

shareholder of an auditing firm would impair the firm's independence.

1.Explains circumstances in which independence may be considered to be

impaired as a result of litigation or the expressed intention to commence litigation.

2.Provides guidance on how various alternatives to "traditional structures" effect

independence due to changes in the manner in which CPAs are structuring their practices.

3.Addresses financial interests and business relationships that impair

independence.

4.A member issuing a report on a governmental client's general purpose financial

statements generally must be independent of the client, but independence is not required with respect to a related organization if the client is not financially accountable for the organization and the required disclosure does not include financial information.

5.Provides guidance when a member is asked to serve as an honorary or trustee

for an attest client.

6.Independence will generally be considered to be impaired if, during the period

of a professional engagement or at the time of expressing an opinion, a member's firm had any joint business activity with the client that was material to the CPA's firm or to the client.

7.Provides guidance on independence for engagements that are more limited in

scope than an audit of general purpose financial statements.

8.Explains various ways in which a financial interest in a nonclient that has a

significant influence on a client may impair independence with respect to a client.

9.Outlines important responsibility the client's management must take in order to

preserve independence.

10.Explains some specific exceptions to the general rule concerning the situation in

which a member has a loan to or from the enterprise or any officer, director, or principal stockholder of the enterprise.

11.Addresses circumstances in which the activities of a former partner or

shareholder of an auditing firm would impair the firm's independence.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/85

Play

Full screen (f)

Deck 3: Professional Ethics

1

Within the context of the AICPA's Code of Professional Conduct, the "public interest" is defined as the collective well being of the community of people and institutions served by CPAs.

True

2

When disclosures in the financial statements are inadequate, Rule 301 prohibits the member from disclosing the required information in the report without the direct consent of the client.

False

3

A member can permit non-CPAs to carry out acts in his behalf that, if carried out by the member, would violate the rules.

False

4

With some important exceptions, Rule 301 requires the member to obtain specific consent of the AICPA before disclosing confidential client information.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

5

Under the "Joint Ethics Enforcement Program" (JEEP), the jurisdictional groups may act independently or jointly.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

6

There is a single joint trial board consisting of at least thirty-six AICPA members elected by Council from present or former Council members.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

7

The unpaid fees ruling does not apply to unbilled fees.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

8

The AICPA Professional Ethics Team performs four major functions.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

9

One of the distinguishing characteristics of any profession is the existence of a code of professional conduct for its members.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

10

Due professional care, planning and supervision, and sufficient relevant data codify practices that must be followed in performing any service.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

11

For covered members, the prohibition against a direct financial interest under Rule 101 is absolute.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

12

In order for a gift from a client to impair independence, it would have to be material in relation to the assets of the client.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

13

A firm may designate itself as "Members of the American Institute of Certified Public Accountants" if a majority of the partners or shareholders are members.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

14

Rule 501 - Acts Discreditable in the AICPA's Code of Professional Conduct, enables disciplinary action to be taken for unethical acts of a member not specifically covered by other rules.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

15

Enforcement of the Rules of the AICPA Code of Professional Conduct rests with three groups.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

16

To be meaningful, codes of ethics should be above the law but below the ideal.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

17

The unpaid fees ruling does not apply to fees outstanding from a client in bankruptcy.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

18

As in the case of the AICPA, the most severe sanction to be imposed by a state society is loss of membership in the society.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

19

For a material indirect financial interest to impair a member's independence, the member must have knowledge of the interest.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

20

CPAs can be required to comply with, at most, a single code of ethics.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

21

Under the automatic disciplinary provision of the bylaws, suspension results when the Secretary of the Institute is notified that a judgment or conviction has been imposed on a member for a crime punishable by imprisonment for more than two years.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

22

An immediate family member of a covered member does not include a parent to the covered member.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

23

Which one of the following is not true of the Principles in the AICPA's Code of Professional Conduct?

A) They provide a framework for the Rules.

B) They are set forth as enforceable standards.

C) They express the basic tenets of ethical conduct.

D) They are expressions of ideals of professional conduct.

E) They are minimum standards of acceptable conduct.

A) They provide a framework for the Rules.

B) They are set forth as enforceable standards.

C) They express the basic tenets of ethical conduct.

D) They are expressions of ideals of professional conduct.

E) They are minimum standards of acceptable conduct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

24

The AICPA's Code of Professional Conduct governs all accountants.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

25

Ethics deals with how people act towards one another.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

26

Which one of the following Principles relates to being impartial and unbiased in all matters pertaining to an engagement?

A) Responsibilities

B) Objectivity and Independence

C) The Public Interest

D) Scope and Nature of Services

E) Due Care

A) Responsibilities

B) Objectivity and Independence

C) The Public Interest

D) Scope and Nature of Services

E) Due Care

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

27

The main need for a professional code of ethics is to:

A) foster professional harmony.

B) avoid regulation from external sources.

C) keep the level of competition within the profession to a minimum.

D) increase public confidence in the profession.

E) avoid regulation from internal sources.

A) foster professional harmony.

B) avoid regulation from external sources.

C) keep the level of competition within the profession to a minimum.

D) increase public confidence in the profession.

E) avoid regulation from internal sources.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

28

The two main sections of the AICPA's Code of Professional Conduct are:

A) Principles and Rules of Conduct.

B) Rules of Conduct and Interpretations of the Rules of Conduct.

C) Principles and Ethics Rulings.

D) Interpretations of the Rules of Conduct and Ethics Rulings.

E) Principles and Interpretations of the Rules of Conduct.

A) Principles and Rules of Conduct.

B) Rules of Conduct and Interpretations of the Rules of Conduct.

C) Principles and Ethics Rulings.

D) Interpretations of the Rules of Conduct and Ethics Rulings.

E) Principles and Interpretations of the Rules of Conduct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

29

The Rules of Conduct consist of 15 enforceable rules.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

30

The AICPA's Rules of Conduct are never changed or modified.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

31

Under the automatic disciplinary provisions of the bylaws, membership in the AICPA is terminated without a hearing if a member's CPA certificate is revoked as a disciplinary measure by any governmental agency.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

32

The Due Care Principle in the AICPA's Code of Professional Conduct does not require of the auditor:

A) freedom from errors in judgment.

B) thoroughness in their work.

C) completion of the service promptly.

D) observation of technical and ethical standards.

E) continual improvement in competence.

A) freedom from errors in judgment.

B) thoroughness in their work.

C) completion of the service promptly.

D) observation of technical and ethical standards.

E) continual improvement in competence.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

33

Besides consideration of all of the other principles, in deciding whether to provide specific services, which of the following is also required by the Scope and Nature of Services principle:

A) Determine that the requested service is not currently being provided by any other professional.

B) Determine whether any service requested of an audit client would create reasonable assurance.

C) Practice only in a firm that has implemented internal quality control procedures.

D) Assess whether the requested service is in conflict with the role of a professional.

E) Determine whether any service requested of a consulting client would create a conflict of interest.

A) Determine that the requested service is not currently being provided by any other professional.

B) Determine whether any service requested of an audit client would create reasonable assurance.

C) Practice only in a firm that has implemented internal quality control procedures.

D) Assess whether the requested service is in conflict with the role of a professional.

E) Determine whether any service requested of a consulting client would create a conflict of interest.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

34

Which one of the following Principles applies only to an individual who renders service to the public?

A) Responsibilities

B) Objectivity and Independence

C) The Public Interest

D) Scope and Nature of Services

E) Due Care

A) Responsibilities

B) Objectivity and Independence

C) The Public Interest

D) Scope and Nature of Services

E) Due Care

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

35

Under the automatic disciplinary provision of the bylaws, termination of membership occurs when the member has been convicted.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

36

During the 1990's there has been an increase in the percentage of consulting services provided by the Large CPA firms.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

37

The Principle of Integrity in the AICPA's Code of Professional Conduct would be violated in cases of:

A) inadvertent error.

B) genuine differences in opinion.

C) unintentional distortion of facts.

D) straightforwardness.

E) subordination of judgment.

A) inadvertent error.

B) genuine differences in opinion.

C) unintentional distortion of facts.

D) straightforwardness.

E) subordination of judgment.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

38

In general, except when explicitly stated otherwise, the Rules of Conduct in the AICPA's Code of Professional Conduct are applicable to:

A) all members.

B) all professional services.

C) all members in public practice.

D) all members in private practice.

E) all members and all professional services.

A) all members.

B) all professional services.

C) all members in public practice.

D) all members in private practice.

E) all members and all professional services.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

39

A code of professional ethics should be designed to elicit professional behavior that is:

A) equal to that required by the law.

B) ideal.

C) below the ideal but above the law.

D) not directly addressed by the law.

E) equal to the ideal.

A) equal to that required by the law.

B) ideal.

C) below the ideal but above the law.

D) not directly addressed by the law.

E) equal to the ideal.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

40

The AICPA's joint trial board may take the disciplinary action of expelling a member.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

41

When the client is a financial institution, and the loan is made under normal lending conditions, which of the following loan types would be considered a violation of the independence rule?

A) home mortgages that are a material percent of the appraised value of the property

B) direct loans that are not material in relation to the borrower's net worth

C) unsecured loans obtained by the member and guaranteed by her firm

D) loans of any type, as there are no exceptions to this rule

E) indirect loans that are not material in relation to the borrower's net worth

A) home mortgages that are a material percent of the appraised value of the property

B) direct loans that are not material in relation to the borrower's net worth

C) unsecured loans obtained by the member and guaranteed by her firm

D) loans of any type, as there are no exceptions to this rule

E) indirect loans that are not material in relation to the borrower's net worth

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

42

Which one of the following Interpretations of Rule 101 on Independence explains specific exceptions to a general rule?

A) 101-5 - Loans from financial institution clients and related terminology

B) 101-2 - Former practitioners and firm independence

C) 101-13 - Extended audit services

D) 101-3 - Accounting services

E) 101-4 - Honorary directorships and trusteeships of not-for-profit organizations

A) 101-5 - Loans from financial institution clients and related terminology

B) 101-2 - Former practitioners and firm independence

C) 101-13 - Extended audit services

D) 101-3 - Accounting services

E) 101-4 - Honorary directorships and trusteeships of not-for-profit organizations

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

43

Under Rule 101 in the AICPA's Code of Professional Conduct, independence would not be required in which of the following types of engagements?

A) accounting services, management advisory services, or tax services

B) compilations, examinations, or reviews

C) accounting services, examinations, or tax services

D) compilations, examinations, or management advisory services

E) compilations, examinations, or audits

A) accounting services, management advisory services, or tax services

B) compilations, examinations, or reviews

C) accounting services, examinations, or tax services

D) compilations, examinations, or management advisory services

E) compilations, examinations, or audits

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

44

Which one of the following is not required by Rule 201?

A) Obtain sufficient relevant data to afford a reasonable basis for conclusions or recommendations in relation to any professional services performed.

B) Exercise due professional care in the performance of professional services.

C) Do not disclose any confidential client information without the specific consent of the client.

D) Adequately plan and supervise the performance of professional services.

E) Undertake only those professional services that the member or the member's firm can reasonably expect to be completed with professional competence.

A) Obtain sufficient relevant data to afford a reasonable basis for conclusions or recommendations in relation to any professional services performed.

B) Exercise due professional care in the performance of professional services.

C) Do not disclose any confidential client information without the specific consent of the client.

D) Adequately plan and supervise the performance of professional services.

E) Undertake only those professional services that the member or the member's firm can reasonably expect to be completed with professional competence.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

45

Which one of the following is an incorrect quote from Rule 102?

A) "in the performance of any professional service . . ."

B) "and integrity, shall be free of conflicts of interest, and . . ."

C) "shall not knowingly misrepresent facts . . ."

D) "an auditor shall maintain independence . . ."

E) "shall not knowingly. . . subordinate his or her judgment to others. . ."

A) "in the performance of any professional service . . ."

B) "and integrity, shall be free of conflicts of interest, and . . ."

C) "shall not knowingly misrepresent facts . . ."

D) "an auditor shall maintain independence . . ."

E) "shall not knowingly. . . subordinate his or her judgment to others. . ."

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

46

In which one of the following situations would independence not be impaired?

A) direct financial interest in a partnership that invests in a client

B) stock owned in client is put in a trust created as an education fund for the member's minor child

C) attorney/CPA provides legal service as general counsel for an auditing client

D) membership held in a trade association that is a client; member does not serve in a management capacity

E) full participation in the managerial decision-making process of an audit client

A) direct financial interest in a partnership that invests in a client

B) stock owned in client is put in a trust created as an education fund for the member's minor child

C) attorney/CPA provides legal service as general counsel for an auditing client

D) membership held in a trade association that is a client; member does not serve in a management capacity

E) full participation in the managerial decision-making process of an audit client

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

47

It is fundamental that a CPA in public practice hold in strict confidence:

A) all material financial information.

B) balance sheet information.

C) all information about a client's affairs.

D) all financial information.

E) current year information.

A) all material financial information.

B) balance sheet information.

C) all information about a client's affairs.

D) all financial information.

E) current year information.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

48

Unpaid fees for professional services will impair independence if:

A) the previous year's fee has not been paid by the start of the current year's engagement.

B) the previous year's fee has not been paid by the time the current year's report is issued.

C) the previous year's fee has not been paid by the financial statement date.

D) the current year's fee has not been paid by the time the report is issued.

E) the previous year's fee has not been paid by the time the current year's field work has been completed.

A) the previous year's fee has not been paid by the start of the current year's engagement.

B) the previous year's fee has not been paid by the time the current year's report is issued.

C) the previous year's fee has not been paid by the financial statement date.

D) the current year's fee has not been paid by the time the report is issued.

E) the previous year's fee has not been paid by the time the current year's field work has been completed.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

49

Rule 203 ─ Accounting Principles applies to:

A) audits of GAAP-based financial statements.

B) all attest services with GAAP-based financial statements.

C) all services with GAAP-based financial statements.

D) all services with GAAP and GAAS.

E) all services for which standards have been promulgated regarding GAAP, including engagements to report on a comprehensive basis of accounting other than GAAP. .

A) audits of GAAP-based financial statements.

B) all attest services with GAAP-based financial statements.

C) all services with GAAP-based financial statements.

D) all services with GAAP and GAAS.

E) all services for which standards have been promulgated regarding GAAP, including engagements to report on a comprehensive basis of accounting other than GAAP. .

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

50

A member in public practice may be held responsible for compliance with Rules of Conduct in the AICPA's Code of Professional Conduct of:

A) the member only.

B) all persons under the member's supervision.

C) all the member's partners or shareholders in the practice.

D) all persons under the member's supervision or all the member's partners or shareholders in the practice.

E) the member or all persons under the member's supervision.

A) the member only.

B) all persons under the member's supervision.

C) all the member's partners or shareholders in the practice.

D) all persons under the member's supervision or all the member's partners or shareholders in the practice.

E) the member or all persons under the member's supervision.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

51

Rule 203 applies to accounting principles:

A) promulgated by bodies designated by AICPA Council.

B) promulgated by the FASB.

C) promulgated by the GASB.

D) within the current body of GAAP.

E) deemed to apply in the circumstances.

A) promulgated by bodies designated by AICPA Council.

B) promulgated by the FASB.

C) promulgated by the GASB.

D) within the current body of GAAP.

E) deemed to apply in the circumstances.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

52

Reflecting concern over the effect management consulting services (MCS) provided to an audit client may have on independence, the following are now prohibited:

A) all MCS for audit clients

B) certain MCS for audit clients

C) certain MCS for SEC audit clients

D) all MCS for SEC audit clients

E) all MCS for publicly-held audit clients

A) all MCS for audit clients

B) certain MCS for audit clients

C) certain MCS for SEC audit clients

D) all MCS for SEC audit clients

E) all MCS for publicly-held audit clients

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

53

A direct or material indirect financial interest in the client would impair independence if the interest were held during which of the following time periods?

A) at the time of issuing the opinion

B) from the statement date to the time of issuing the opinion

C) from the beginning of the period covered by the statements to the time of issuing the opinion

D) during the engagement up to the date that auditing field work is completed

E) during the engagement or at the time of issuing the opinion

A) at the time of issuing the opinion

B) from the statement date to the time of issuing the opinion

C) from the beginning of the period covered by the statements to the time of issuing the opinion

D) during the engagement up to the date that auditing field work is completed

E) during the engagement or at the time of issuing the opinion

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

54

In Interpretation 101?1, the term "A member or a member's firm" would include all of the following except:

A) partners in other offices, not directly involved on the engagement.

B) all managerial personnel located in the office performing the engagement.

C) the nondependent spouse of the member.

D) the dependent son of the member.

E) clerical staff members working on the engagement.

A) partners in other offices, not directly involved on the engagement.

B) all managerial personnel located in the office performing the engagement.

C) the nondependent spouse of the member.

D) the dependent son of the member.

E) clerical staff members working on the engagement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following would not be considered an indirect financial interest for a given CPA?

A) The CPA owns stock in a mutual fund, which owns stock in the client.

B) The CPA owns stock in a bank that provides the line of credit to the client company.

C) The CPA's nondependent close relative has a financial interest in the client company.

D) The CPA's dependent child owns an immaterial amount of stock in the client

Company.

E) The CPA received cash advances totaling eight thousand dollars from a bank that is a client.

A) The CPA owns stock in a mutual fund, which owns stock in the client.

B) The CPA owns stock in a bank that provides the line of credit to the client company.

C) The CPA's nondependent close relative has a financial interest in the client company.

D) The CPA's dependent child owns an immaterial amount of stock in the client

Company.

E) The CPA received cash advances totaling eight thousand dollars from a bank that is a client.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

56

Which one of the following is not an MCS service that a CPA firm is required to refrain from performing for its SEC audit clients?

A) human resource functions

B) actuarial services

C) expert services unrelated to the audit

D) appraisal or services

E) auditing services to insurance companies

A) human resource functions

B) actuarial services

C) expert services unrelated to the audit

D) appraisal or services

E) auditing services to insurance companies

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

57

Currently, the technical standards that fall under Rule 202 ─ Compliance With Standards include those issued by the:

A) Auditing Standards Board (ASB).

B) Accounting and Review Services Committee (ARSC).

C) Management Consulting Services Executive Committee (MCSEC).

D) ASB, ARSC, and MCSEC.

E) FASB, GASB and CASB.

A) Auditing Standards Board (ASB).

B) Accounting and Review Services Committee (ARSC).

C) Management Consulting Services Executive Committee (MCSEC).

D) ASB, ARSC, and MCSEC.

E) FASB, GASB and CASB.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

58

Rule 101 makes independence a requirement for:

A) all services provided by members.

B) audits, tax services, and management advisory services.

C) audits, reviews, and examinations of prospective statements.

D) audits, reviews, and accounting services.

E) audits, reviews, and consulting services.

A) all services provided by members.

B) audits, tax services, and management advisory services.

C) audits, reviews, and examinations of prospective statements.

D) audits, reviews, and accounting services.

E) audits, reviews, and consulting services.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

59

The unpaid fees ruling would not apply to:

A) unbilled fees.

B) fees for nonaudit services.

C) fees outstanding from a client in bankruptcy.

D) unbilled fees from a client that has recently emerged from bankruptcy.

E) fees outstanding from a client that has performed a troubled debt restructure.

A) unbilled fees.

B) fees for nonaudit services.

C) fees outstanding from a client in bankruptcy.

D) unbilled fees from a client that has recently emerged from bankruptcy.

E) fees outstanding from a client that has performed a troubled debt restructure.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

60

Which section of the AICPA's Rules of Conduct currently has no rules within it? Responsibilities to Colleagues.

Other Responsibilities and Practices.

Responsibilities to Clients.

Independence, Integrity, and Objectivity.

General Standards and Accounting Principles.

Other Responsibilities and Practices.

Responsibilities to Clients.

Independence, Integrity, and Objectivity.

General Standards and Accounting Principles.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

61

Under the "Joint Ethics Enforcement Program" (JEEP), the AICPA normally has jurisdiction over cases involving:

A) proven fraud.

B) narrow national issues.

C) alleged ethical violations.

D) more than one member.

E) more than one state.

A) proven fraud.

B) narrow national issues.

C) alleged ethical violations.

D) more than one member.

E) more than one state.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

62

The Joint Trial Board may take which one of the following disciplinary actions against a member?

A) revoke the member's license

B) suspend membership for no more than three years

C) admonish the member

D) fine the member

E) convict the member

A) revoke the member's license

B) suspend membership for no more than three years

C) admonish the member

D) fine the member

E) convict the member

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

63

The CPA Vision Project identified five core values associated with the CPA profession. Which one of the following is not one of the five core values.

A) Integrity.

B) Objectivity

C) Competence.

D) Consistency

E) Continuing education and lifelong learning.

A) Integrity.

B) Objectivity

C) Competence.

D) Consistency

E) Continuing education and lifelong learning.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

64

Rule 503 in the AICPA's Code of Professional Conduct prohibits commissions and referral fees from:

A) any client.

B) audit clients.

C) attest clients.

D) accounting clients.

E) attest clients and some accounting clients.

A) any client.

B) audit clients.

C) attest clients.

D) accounting clients.

E) attest clients and some accounting clients.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

65

For each of the following actions by a member CPA, indicate (1) the rule of conduct that is applicable and (2) whether the actions does (yes) or does not (no) violate the rule. You may identify the rule by number on your answer sheet. Your selections can be made from the following list: 1.Discriminates in employment.

2.Makes recommendations but not the decisions in an MCS engagement for a nonpublic client.

3.Permits a non-CPA to be the chairman of the board of a CPA firm organized as a professional corporation.

4.Fails to make inquiries in a review of interim financial information.

5.Accepts a commission from a vendor, with the permission of the audit client, for

recommending the vendor's product.

6.Indicates that he will perform the audit of a city's united fund charity for a nominal fee.

7.Transfers working papers, with the client's permission, to the client's new auditors.

8.Subordinates his judgment in favor of the client in tax practice when there is little support for the client's position.

9.Indicates the number of partners, CPAs and offices in his or her firm in an advertisement.

10.States that the fee in a tax case will be based on the amount of tax saving realized.

11.Fails to conform to a recently issued SAS, which has an immaterial effect on the financial statements.

12.A personnel manager in the office doing the audit of a client has a financial interest in the client.

13.Fails to adequately plan and supervise an MCS engagement.

14.Agrees to serve as an honorary director of a charitable foundation.

15.Knowingly misrepresents facts in an engagement.

1.Discriminates in employment.2.Makes recommendations but not the decisions in an MCS engagement for a nonpublic client.

3.Permits a non-CPA to be the chairman of the board of a CPA firm organized as a professional corporation.

4.Fails to make inquiries in a review of interim financial information.

5.Accepts a commission from a vendor, with the permission of the audit client, for

recommending the vendor's product.

6.Indicates that he will perform the audit of a city's united fund charity for a nominal fee.

7.Transfers working papers, with the client's permission, to the client's new auditors.

8.Subordinates his judgment in favor of the client in tax practice when there is little support for the client's position.

9.Indicates the number of partners, CPAs and offices in his or her firm in an advertisement.

10.States that the fee in a tax case will be based on the amount of tax saving realized.

11.Fails to conform to a recently issued SAS, which has an immaterial effect on the financial statements.

12.A personnel manager in the office doing the audit of a client has a financial interest in the client.

13.Fails to adequately plan and supervise an MCS engagement.

14.Agrees to serve as an honorary director of a charitable foundation.

15.Knowingly misrepresents facts in an engagement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

66

The maximum sanction that the AICPA can impose if to:

A) expel the member.

B) admonish the member.

C) suspend the member.

D) fine the member.

E) warn the member.

A) expel the member.

B) admonish the member.

C) suspend the member.

D) fine the member.

E) warn the member.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following ethical principles is at the center of the profession's ongoing quest for excellence in the performance of professional services?

A) Responsibilities.

B) The Public Interest.

C) Integrity.

D) Objectivity and Independence.

E) Due Care.

A) Responsibilities.

B) The Public Interest.

C) Integrity.

D) Objectivity and Independence.

E) Due Care.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

68

The FTC's 1990 Order to the AICPA required change in the wording of implementation of which of the following Rules?

A) advertising, contingent fees, and acts discreditable

B) contingent fees, commissions, and acts discreditable

C) advertising, commissions, and acts discreditable

D) advertising, contingent fees, and commissions

E) contingent fees, commissions, and accounting principles

A) advertising, contingent fees, and acts discreditable

B) contingent fees, commissions, and acts discreditable

C) advertising, commissions, and acts discreditable

D) advertising, contingent fees, and commissions

E) contingent fees, commissions, and accounting principles

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

69

Interpretation 505-3 requires all of the following except:

A) enrollment in an SEC-approved practice monitoring program.

B) compliance with all aspects of applicable state laws or regulations.

C) membership in the SEC practice section if the attest work is for SEC clients.

D) compliance with the independence rules prescribed by Rule 101.

E) compliance with applicable standards promulgated by Council-designated bodies and all other applicable provisions of the Code.

A) enrollment in an SEC-approved practice monitoring program.

B) compliance with all aspects of applicable state laws or regulations.

C) membership in the SEC practice section if the attest work is for SEC clients.

D) compliance with the independence rules prescribed by Rule 101.

E) compliance with applicable standards promulgated by Council-designated bodies and all other applicable provisions of the Code.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

70

Trial board hearings are generally held by subboards comprised of at least how many board members?

A) 5

B) 10

C) 12

D) 15

E) 3

A) 5

B) 10

C) 12

D) 15

E) 3

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

71

The AICPA's Code of Professional Conduct governs AICPA members and is administered by the:

A) SEC.

B) State Boards of Accountancy.

C) AICPA Emerging Issues Task Force.

D) AICPA Professional Ethics Team

E) SEC ethical advisors

A) SEC.

B) State Boards of Accountancy.

C) AICPA Emerging Issues Task Force.

D) AICPA Professional Ethics Team

E) SEC ethical advisors

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

72

The AICPA's Code of Professional Conduct prohibits contingent fees from:

A) any client.

B) audit clients.

C) attest clients and some accounting clients.

D) attest clients.

E) accounting clients.

A) any client.

B) audit clients.

C) attest clients and some accounting clients.

D) attest clients.

E) accounting clients.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

73

Rule 301? Confidential Client Information contains explicit exceptions for all of the following efforts by a member except to:

A) comply with a subpoena.

B) respond to an inquiry by a recognized investigative body.

C) cooperate with a review of the member's practice.

D) comply with applicable laws and government regulations.

E) sell a practice.

A) comply with a subpoena.

B) respond to an inquiry by a recognized investigative body.

C) cooperate with a review of the member's practice.

D) comply with applicable laws and government regulations.

E) sell a practice.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

74

Enforcement of the Rules in the Code of Professional Conduct rests with the:

A) AICPA.

B) AICPA and the state societies.

C) AICPA and the state boards.

D) state societies.

E) state boards.

A) AICPA.

B) AICPA and the state societies.

C) AICPA and the state boards.

D) state societies.

E) state boards.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

75

The Joint Trial Board consists of at least how many members?

A) 50

B) 20

C) 40

D) 36

E) 43

A) 50

B) 20

C) 40

D) 36

E) 43

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

76

The thirteen current Interpretations of Rule 101 are listed below. Place the following numbers in the spaces provided:

1.Explains circumstances in which independence may be considered to be

impaired as a result of litigation or the expressed intention to commence litigation.

2.Provides guidance on how various alternatives to "traditional structures" effect

independence due to changes in the manner in which CPAs are structuring their practices.

3.Addresses financial interests and business relationships that impair

independence.

4.A member issuing a report on a governmental client's general purpose financial

statements generally must be independent of the client, but independence is not required with respect to a related organization if the client is not financially accountable for the organization and the required disclosure does not include financial information.

5.Provides guidance when a member is asked to serve as an honorary or trustee

for an attest client.

6.Independence will generally be considered to be impaired if, during the period

of a professional engagement or at the time of expressing an opinion, a member's firm had any joint business activity with the client that was material to the CPA's firm or to the client.

7.Provides guidance on independence for engagements that are more limited in

scope than an audit of general purpose financial statements.

8.Explains various ways in which a financial interest in a nonclient that has a

significant influence on a client may impair independence with respect to a client.

9.Outlines important responsibility the client's management must take in order to

preserve independence.

10.Explains some specific exceptions to the general rule concerning the situation in

which a member has a loan to or from the enterprise or any officer, director, or principal stockholder of the enterprise.

11.Addresses circumstances in which the activities of a former partner or

shareholder of an auditing firm would impair the firm's independence.

1.Explains circumstances in which independence may be considered to be

impaired as a result of litigation or the expressed intention to commence litigation.

2.Provides guidance on how various alternatives to "traditional structures" effect

independence due to changes in the manner in which CPAs are structuring their practices.

3.Addresses financial interests and business relationships that impair

independence.

4.A member issuing a report on a governmental client's general purpose financial

statements generally must be independent of the client, but independence is not required with respect to a related organization if the client is not financially accountable for the organization and the required disclosure does not include financial information.

5.Provides guidance when a member is asked to serve as an honorary or trustee

for an attest client.

6.Independence will generally be considered to be impaired if, during the period

of a professional engagement or at the time of expressing an opinion, a member's firm had any joint business activity with the client that was material to the CPA's firm or to the client.

7.Provides guidance on independence for engagements that are more limited in

scope than an audit of general purpose financial statements.

8.Explains various ways in which a financial interest in a nonclient that has a

significant influence on a client may impair independence with respect to a client.

9.Outlines important responsibility the client's management must take in order to

preserve independence.

10.Explains some specific exceptions to the general rule concerning the situation in

which a member has a loan to or from the enterprise or any officer, director, or principal stockholder of the enterprise.

11.Addresses circumstances in which the activities of a former partner or

shareholder of an auditing firm would impair the firm's independence.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

77

The main purpose of the "Joint Ethics Enforcement Program" (JEEP) is to:

A) coordinate efforts among the AICPA, state societies and the SEC.

B) make enforcement of the Rules more effective and disciplinary action more uniform.

C) shift the role of enforcement to the AICPA.

D) shift the role of enforcement to the state societies.

E) shift the role of enforcement to the state boards.

A) coordinate efforts among the AICPA, state societies and the SEC.

B) make enforcement of the Rules more effective and disciplinary action more uniform.

C) shift the role of enforcement to the AICPA.

D) shift the role of enforcement to the state societies.

E) shift the role of enforcement to the state boards.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

78

Rule 502 in the AICPA's Code of Professional Conduct currently can be used to prevent the use of:

A) materials considered to be deceptive.

B) materials not considered professionally dignified.

C) materials considered to be in poor taste.

D) self-laudatory claims, endorsements, or testimonials.

E) direct solicitation.

A) materials considered to be deceptive.

B) materials not considered professionally dignified.

C) materials considered to be in poor taste.

D) self-laudatory claims, endorsements, or testimonials.

E) direct solicitation.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

79

Under Rule 505 in the AICPA's Code of Professional Conduct, the name of the firm cannot be:

A) fictitious.

B) an indication of a specialty.

C) fictitious, an indication of a specialty, or misleading.

D) facetious.

E) misleading.

A) fictitious.

B) an indication of a specialty.

C) fictitious, an indication of a specialty, or misleading.

D) facetious.

E) misleading.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

80

Which one of the following points out that members are often asked to render professional services to clients of third parties who may have obtained the clients as the result of their own advertising and solicitation efforts?

A) Interpretation 502-3

B) Interpretation 502-2

C) Interpretation 502-4

D) Interpretation 502-5

E) Interpretation 502-1

A) Interpretation 502-3

B) Interpretation 502-2

C) Interpretation 502-4

D) Interpretation 502-5

E) Interpretation 502-1

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 85 flashcards in this deck.