Deck 14: Perfect Competition

Full screen (f)

Question

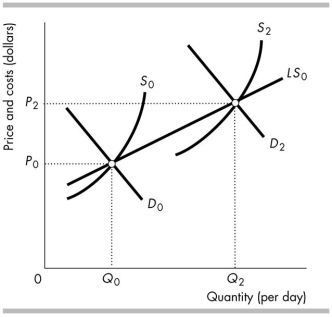

The curve LS0 in the above figure is the long- run supply curve in a perfectly competitive market. The short- run market supply curve shifts from S0 to S2 as the

A) wage rate falls.

B) external economies rise.

C) number of firms increases.

D) number of firms decreases.

Question

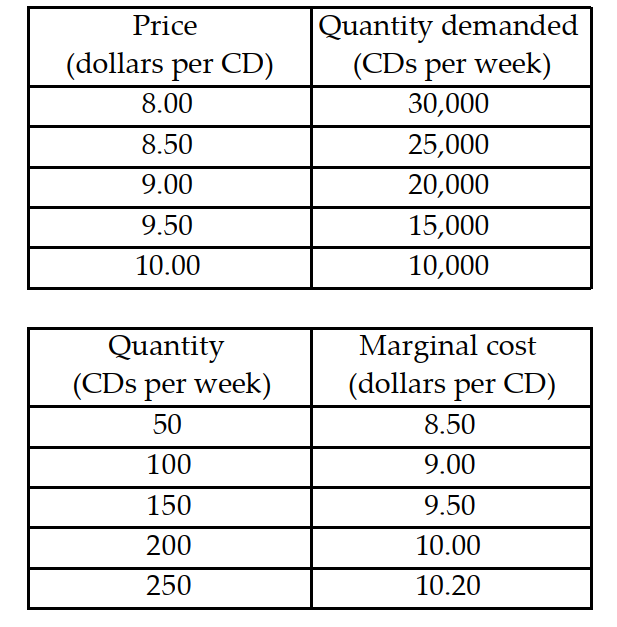

The first table shows the market demand schedule for CDs, and the second table shows the cost structure of each firm. The CD market is perfectly competitive and there are 100 identical firms. The market price of a CD is _______, and _______ CDs are produced and sold.

A) $10.00; 10,000

B) $9.00; 20,000

C) $9.50; 15,000

D) $8.50; 24,000

Question

Question

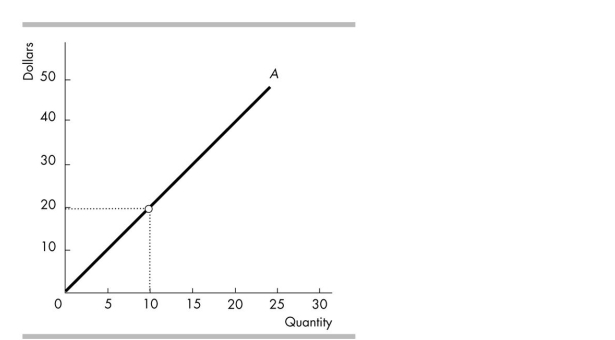

In the above figure showing a perfectly competitive firm's total revenue line, the firm's marginal revenue

A) falls as output increases.

B) rises as output increases.

C) does not change as output increases.

D) cannot be determined.

Question

Question

Question

Question

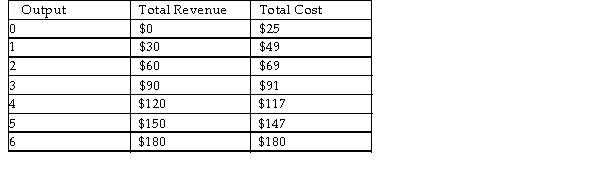

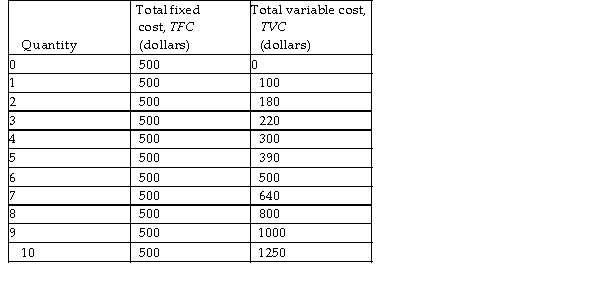

In the above table, if the firm produces 2 units of output, it will

A) make an economic profit of $9.

B) make an economic profit of $60.

C) incur an economic loss of $60.

D) incur an economic loss of $9.

Question

Question

Question

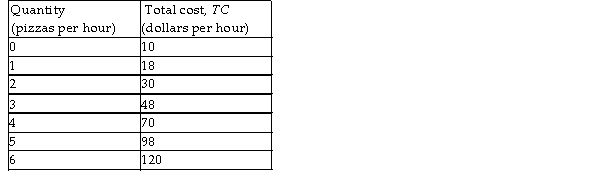

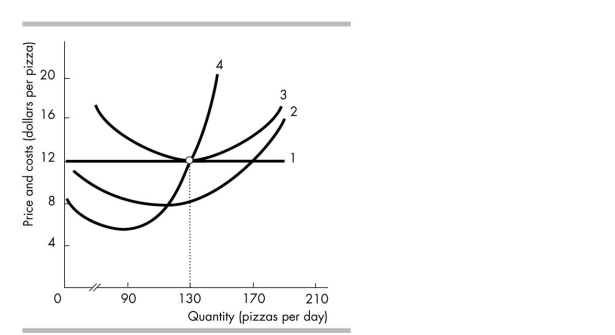

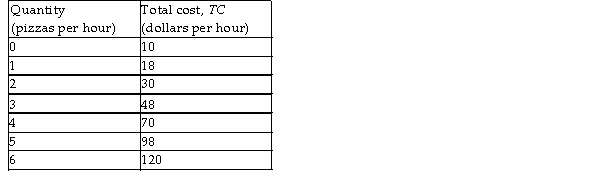

Giuseppe's Pizza is a perfectly competitive firm. The firm's costs are shown in the table above. If the market price is $15, how much economic profit does the firm make?

A) $30

B) - $15

C) - $10

D) $0

Question

Question

Question

Question

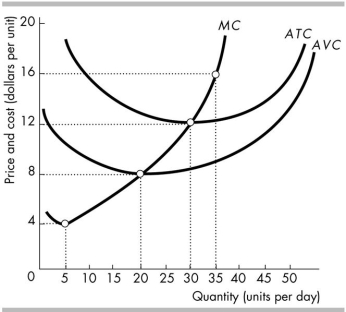

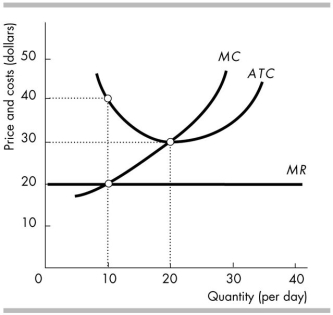

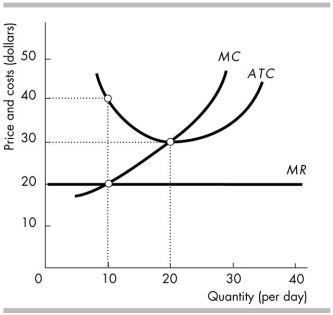

In the above figure, at what price does a perfectly competitive firm make zero economic profit?

A) $4 per unit

B) $12 per unit

C) $16 per unit

D) $8 per unit

Question

Question

The figure above shows a perfectly competitive firm. The firm is operating; that is, the firm has not shut down. The firm is

A) incurring an economic loss of $200.

B) making zero economic profit.

C) making an economic profit of $200.

D) incurring an economic loss of $600.

Question

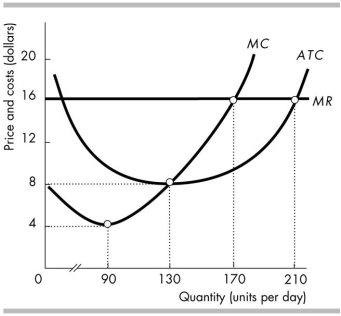

The figure above shows the marginal revenue and costs of a perfectly competitive firm. The firm's profit is maximised when the firm produces

A) 90 units of output.

B) 170 units of output.

C) 210 units of output.

D) 130 units of output.

Question

In the above figure, the firm will produce

A) 20 units.

B) 5 units.

C) 15 units.

D) 0 units.

Question

Question

Question

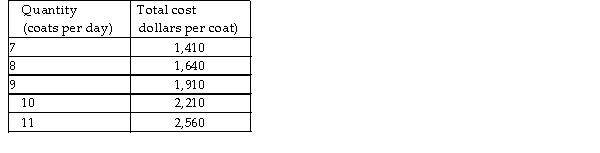

The table above shows the total cost incurred by Sue's Coat Shop, a perfectly competitive firm. If the market price of a coat is $285, Sue's will maximise economic profit by selling _______ coats a day.

A) 7

B) 8

C) 9

D) 11

Question

Question

Question

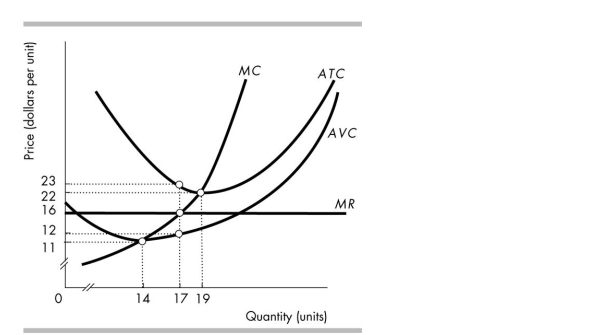

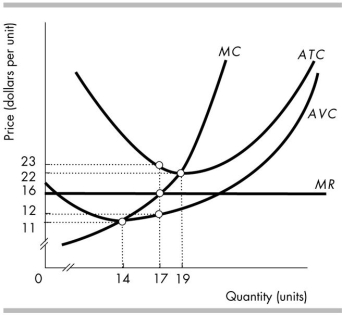

Consider the perfectly competitive firm in the above figure. The shutdown point occurs at a price of

A) $22.00.

B) $16.00.

C) $12.00.

D) $11.00.

Question

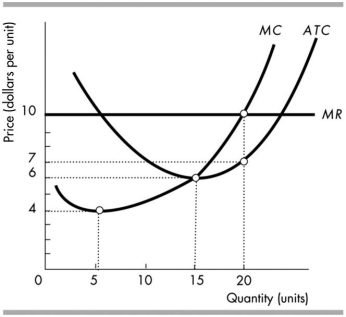

In the above figure, at a price of $6, a perfectly competitive firm produces _______ and it _______.

A) 0; does not incur an economic loss or make an economic profit

B) 0; makes an economic profit

C) some output; incurs an economic loss

D) 0; incurs an economic loss

Question

Question

Question

Question

In the above figure, the firm's total economic profit is equal to

A) $200.

B) MR - MC.

C) $60.

D) $150.

Question

Question

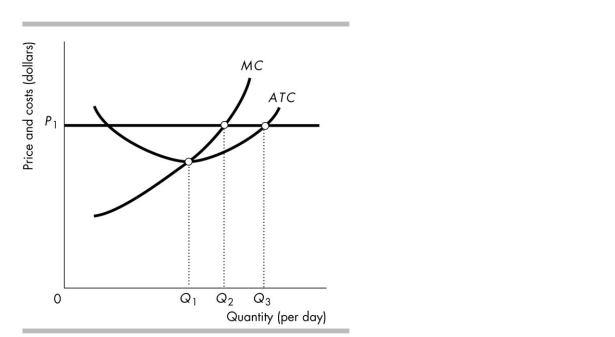

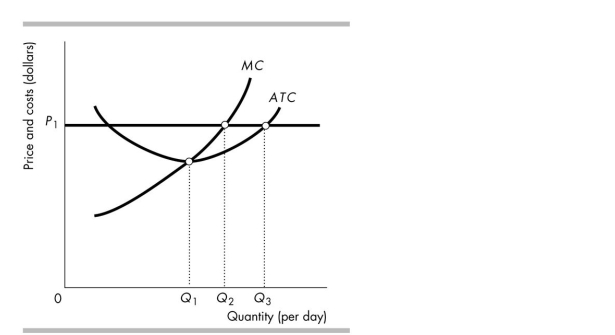

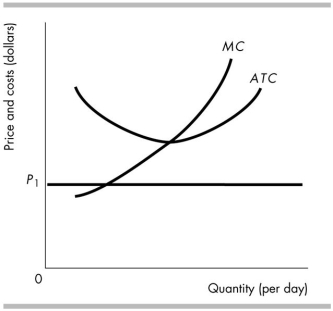

In the above figure, if the price is P1, the firm will produce

A) where ATC equals P1.

B) nothing.

C) where MC equals P1.

D) where MC equals ATC.

Question

Question

Question

Question

Question

Question

In the above figure, the line represented by the '4' is the

A) average total cost.

B) marginal revenue.

C) marginal cost.

D) average fixed cost.

Question

In the above figure, if the price is P1 and the firm produced Q1, the firm's economic profit is _______

Than if it produced Q2 and _______ than if it produced Q3.

A) more; less

B) more; more

C) less; less

D) less; more

Question

Question

Question

Question

Question

Question

Question

Consider the perfectly competitive firm in the above figure. At the profit- maximising level of output, the firm is

A) incurring an economic loss equal to $123.50.

B) incurring an economic loss equal to $187.00.

C) making zero economic profit.

D) incurring an economic loss equal to $119.00.

Question

The figure above shows a perfectly competitive firm. The firm will shut down in the short run if total fixed costs

A) exceed total costs.

B) exceed $401.

C) are less than $200.

D) are between $201 and $400.

Question

The above figure shows the cost curves for a perfectly competitive firm. If all firms in the market have the same cost curves and the price equals $16 per unit,

A) over time, firms will leave this market.

B) over time, the price will fall as new firms enter the market.

C) the market is in its long- run equilibrium.

D) the firm is making zero economic profit.

Question

Question

The table above shows some of the costs for a perfectly competitive firm. The firm will produce 9 units of output if the price per unit is

A) $500.

B) $300.

C) $200.

D) $1750.

Question

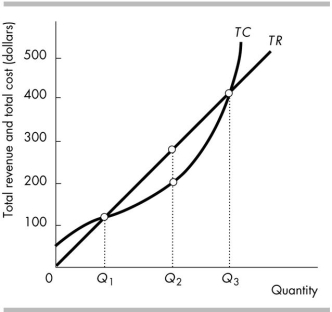

The above figure illustrates a firm's total revenue and total cost curves. Which one of the following statements is FALSE?

A) At an output above Q3 the firm incurs an economic loss.

B) At output Q2 the firm incurs an economic loss.

C) Economic profit is the vertical distance between the total revenue curve and the total cost curve.

D) At output Q1 the firm makes zero economic profit.

Question

Question

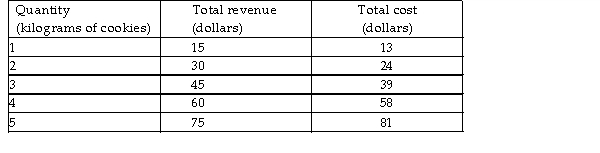

The table above gives the total revenue and total cost for a perfectly competitive firm producing chocolate chip cookies. If the firm is producing 4 kilograms of cookies, to maximise its profit it will

A) continue producing 4 kilograms of cookies.

B) decrease its output.

C) increase its output.

D) shut down.

Question

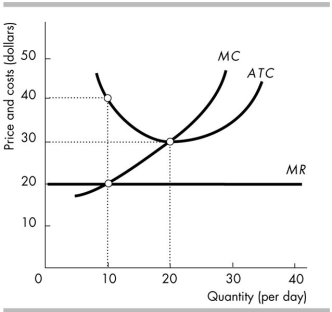

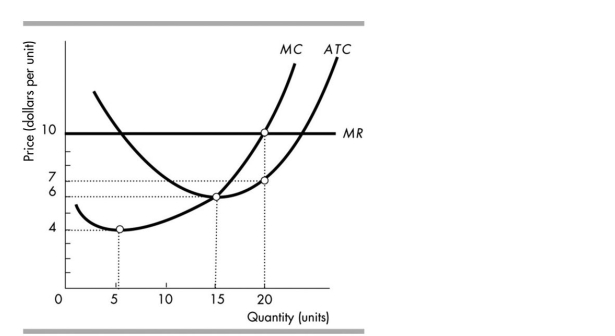

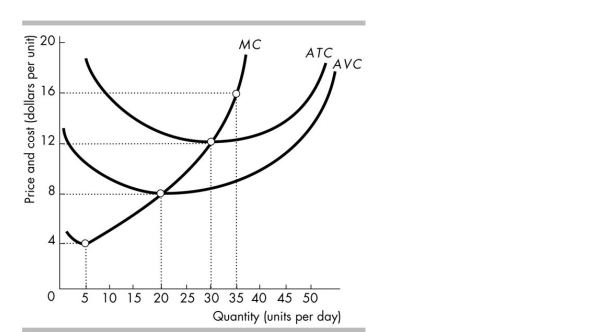

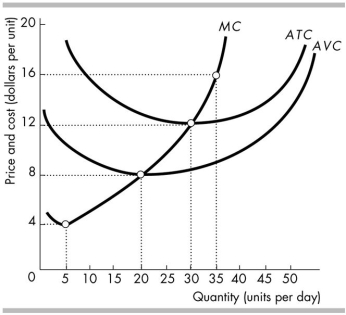

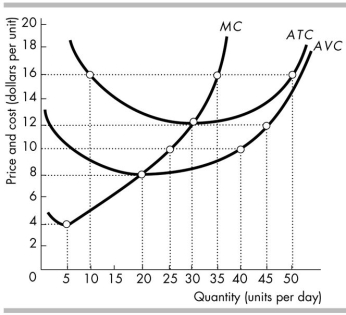

In the above figure, if the price is $16 per unit, how many units will a profit- maximising perfectly competitive firm produce?

A) 30

B) 20

C) 35

D) 0

Question

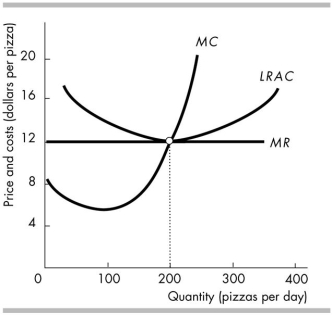

The figure above shows the marginal revenue and long- run cost curves for a perfectly competitive firm. Which of the following statements is true?

A) The firm will eventually decrease its production.

B) Over time, this firm will leave this industry.

C) The firm is earning positive economic profit.

D) The firm is producing at minimum long- run average cost.

Question

Suppose the cost curves in the above figure apply to all firms in the market. Then, if the initial price is P1, in the long run the market

A) supply will increase.

B) supply will decrease.

C) demand will increase.

D) demand will decrease.

Question

Question

Question

Giuseppe's Pizza is a perfectly competitive firm. The firm's costs are shown in the table above. If the market price is $15, what is Giuseppe's profit- maximising output?

A) 2 pizzas per hour

B) 4 pizzas per hour

C) 3 pizzas per hour

D) 0 pizzas per hour

Question

Question

Question

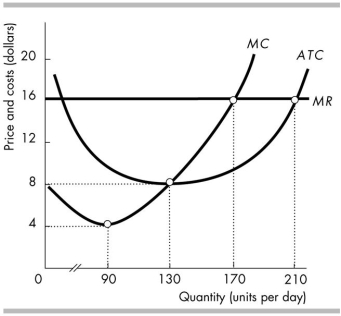

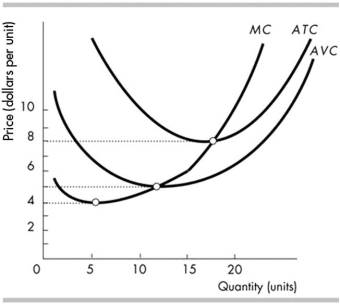

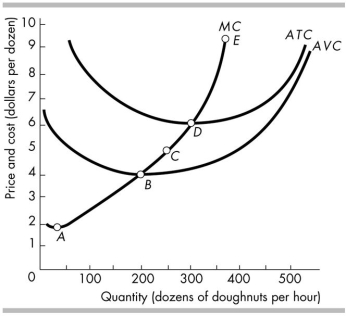

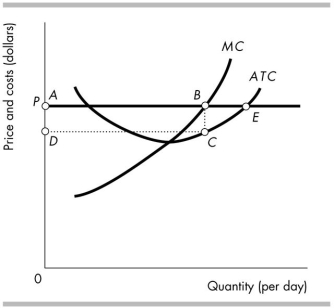

The doughnut market is perfectly competitive. The figure above shows the costs of a typical doughnut producer. In the short run, the doughnut producer's supply curve is the curve running from point _______ to point E.

A) A

B) B

C) C

D) D

Question

Question

The figure above shows the marginal revenue and costs of a perfectly competitive firm. The price the firm charges is

A) $16 per unit.

B) $4 per unit.

C) $8 per unit.

D) None of the above answers is correct.

Question

Question

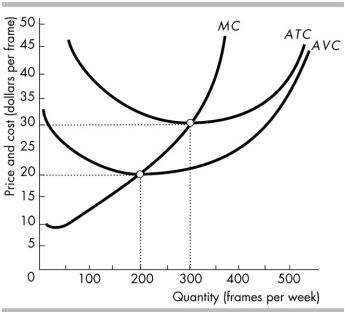

The figure above illustrates the short- run costs of Paul's Picture Frames Inc. The picture frame market is perfectly competitive and the market price is $30 a frame. Paul produces _______ frames each week, makes _______ of total revenue, and makes zero profit.

A) 200; $4,000; normal

B) 200; $4,000; economic

C) 300; $9,000; normal

D) 300; $9,000; economic

Question

Question

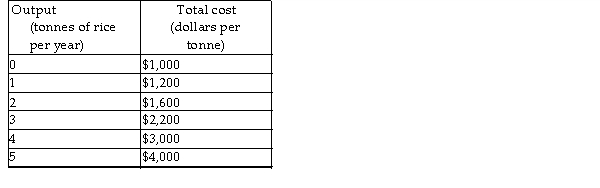

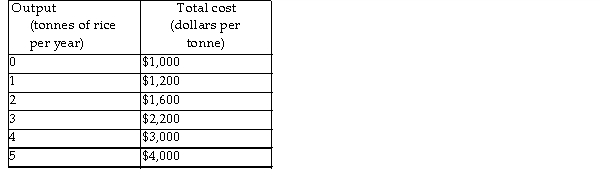

Based on the table above which shows Chip's costs, if rice sells for $600 a tonne, Chip

A) incurs an economic loss and should shut down in the short run.

B) incurs an economic loss, but should stay open in the short run.

C) makes an economic profit, but should shut down in the short run.

D) makes an economic profit and should stay open in the short run.

Question

In the above figure, at a price of $4 per unit, a profit- maximising perfectly competitive firm will

A) shut down because its total revenue is less than its variable costs.

B) incur an economic loss.

C) produce 5 units.

D) Both answers A and B are correct.

Question

Question

Question

Based on the table above which shows Chip's costs, if rice sells for $600 a tonne, Chip's profit- maximising output is

A) between three and four tonnes.

B) less than one tonne.

C) between two and three tonnes.

D) between one and two tonnes.

Question

The figure above shows a perfectly competitive firm. In the short run, the firm will shut down

A) only if the AVC of producing 10 units is more than $20.

B) always.

C) only if the AVC curve reaches its minimum before 10 units are produced.

D) only if the AVC of producing 10 units is less than $20.

Question

Question

Question

Question

Consider the perfectly competitive firm in the figure above. At the profit- maximising level of output, the firm will

A) make an economic profit equal to the area ABCD.

B) incur an economic loss equal to the area ABCD.

C) make an economic profit equal to the area AECD.

D) make zero economic profit.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/150

Play

Full screen (f)

Deck 14: Perfect Competition

1

The curve LS0 in the above figure is the long- run supply curve in a perfectly competitive market. The short- run market supply curve shifts from S0 to S2 as the

A) wage rate falls.

B) external economies rise.

C) number of firms increases.

D) number of firms decreases.

number of firms increases.

2

The first table shows the market demand schedule for CDs, and the second table shows the cost structure of each firm. The CD market is perfectly competitive and there are 100 identical firms. The market price of a CD is _______, and _______ CDs are produced and sold.

A) $10.00; 10,000

B) $9.00; 20,000

C) $9.50; 15,000

D) $8.50; 24,000

$9.50; 15,000

3

External economies and diseconomies explain the shape of the

A) short- run average total cost curve of a firm.

B) long- run market supply curve.

C) long- run average total cost curve of a firm.

D) supply curve of the firm.

A) short- run average total cost curve of a firm.

B) long- run market supply curve.

C) long- run average total cost curve of a firm.

D) supply curve of the firm.

long- run market supply curve.

4

In the above figure showing a perfectly competitive firm's total revenue line, the firm's marginal revenue

A) falls as output increases.

B) rises as output increases.

C) does not change as output increases.

D) cannot be determined.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

5

At a firm's break- even point, its

A) marginal revenue exceeds its marginal cost.

B) marginal revenue equals its average fixed cost.

C) marginal revenue equals its average variable cost.

D) total revenue equals its total opportunity cost.

A) marginal revenue exceeds its marginal cost.

B) marginal revenue equals its average fixed cost.

C) marginal revenue equals its average variable cost.

D) total revenue equals its total opportunity cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

6

In perfect competition, the marginal revenue of an individual firm

A) is zero.

B) exceeds the price of the product.

C) equals the price of the product.

D) is positive but less than the price of the product.

A) is zero.

B) exceeds the price of the product.

C) equals the price of the product.

D) is positive but less than the price of the product.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

7

If a perfectly competitive market has external diseconomies, then the long- run market supply curve is

A) negatively sloped.

B) perfectly inelastic.

C) positively sloped.

D) perfectly elastic.

A) negatively sloped.

B) perfectly inelastic.

C) positively sloped.

D) perfectly elastic.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

8

In the above table, if the firm produces 2 units of output, it will

A) make an economic profit of $9.

B) make an economic profit of $60.

C) incur an economic loss of $60.

D) incur an economic loss of $9.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

9

In perfect competition, _______.

A) only firms know their competitors' prices

B) there are many firms that sell identical products

C) there are restrictions on entry into the market

D) firms in the market have advantages over firms that plan to enter the market

A) only firms know their competitors' prices

B) there are many firms that sell identical products

C) there are restrictions on entry into the market

D) firms in the market have advantages over firms that plan to enter the market

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

10

A perfectly competitive firm is making an economic profit when

A) its total revenue is greater than its total cost.

B) the price is greater than the minimum of its average total cost.

C) the price is greater than the minimum of its average variable cost.

D) Both answers A and B are correct.

A) its total revenue is greater than its total cost.

B) the price is greater than the minimum of its average total cost.

C) the price is greater than the minimum of its average variable cost.

D) Both answers A and B are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

11

Giuseppe's Pizza is a perfectly competitive firm. The firm's costs are shown in the table above. If the market price is $15, how much economic profit does the firm make?

A) $30

B) - $15

C) - $10

D) $0

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

12

Perfect competition implies that

A) all firms are producing the same identical product.

B) there are many firms in the market.

C) all firms are price takers.

D) All of the above answers are correct.

A) all firms are producing the same identical product.

B) there are many firms in the market.

C) all firms are price takers.

D) All of the above answers are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

13

A perfectly competitive firm's marginal revenue exceeds its marginal cost at its current output. To increase its profit, the firm will

A) decrease its output.

B) increase its output.

C) raise its price.

D) lower its price.

A) decrease its output.

B) increase its output.

C) raise its price.

D) lower its price.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

14

In the long run, for a perfectly competitive market, if economic profit is

A) less than zero then some firms will exit the market and the market supply curve will shift leftward.

B) equal to zero then there is no entry or exit of firms into or out of the market.

C) greater than zero then some firms will enter the market and the market supply curve will shift rightward.

D) All of the above answers are correct.

A) less than zero then some firms will exit the market and the market supply curve will shift leftward.

B) equal to zero then there is no entry or exit of firms into or out of the market.

C) greater than zero then some firms will enter the market and the market supply curve will shift rightward.

D) All of the above answers are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

15

In the above figure, at what price does a perfectly competitive firm make zero economic profit?

A) $4 per unit

B) $12 per unit

C) $16 per unit

D) $8 per unit

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

16

In the long- run equilibrium in a perfectly competitive market,

A) the average total cost is maximised.

B) the firms make an economic profit.

C) marginal cost is at a minimum.

D) the firms' owners make a normal profit.

A) the average total cost is maximised.

B) the firms make an economic profit.

C) marginal cost is at a minimum.

D) the firms' owners make a normal profit.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

17

The figure above shows a perfectly competitive firm. The firm is operating; that is, the firm has not shut down. The firm is

A) incurring an economic loss of $200.

B) making zero economic profit.

C) making an economic profit of $200.

D) incurring an economic loss of $600.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

18

The figure above shows the marginal revenue and costs of a perfectly competitive firm. The firm's profit is maximised when the firm produces

A) 90 units of output.

B) 170 units of output.

C) 210 units of output.

D) 130 units of output.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

19

In the above figure, the firm will produce

A) 20 units.

B) 5 units.

C) 15 units.

D) 0 units.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

20

Assuming long- run external economies exist, when demand increases in a perfectly competitive market, in the long run the average total cost curve for a typical firm

A) shifts downward.

B) is no longer U- shaped.

C) shifts upward.

D) stays the same.

A) shifts downward.

B) is no longer U- shaped.

C) shifts upward.

D) stays the same.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

21

In a perfectly competitive market, which of the following will increase the economic profit the firms make in the short run?

A) An increase in market demand

B) An increase in labour costs

C) A decrease in market demand

D) An increase in the number of firms

A) An increase in market demand

B) An increase in labour costs

C) A decrease in market demand

D) An increase in the number of firms

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

22

The table above shows the total cost incurred by Sue's Coat Shop, a perfectly competitive firm. If the market price of a coat is $285, Sue's will maximise economic profit by selling _______ coats a day.

A) 7

B) 8

C) 9

D) 11

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

23

The market for lawn services is perfectly competitive. Larry's Lawn Service cannot increase its total revenue by raising its price because _______.

A) the demand for Larry's services is perfectly elastic

B) Larry's supply of lawn services is inelastic

C) Larry's supply of lawn services is perfectly inelastic

D) the demand for Larry's services is perfectly inelastic

A) the demand for Larry's services is perfectly elastic

B) Larry's supply of lawn services is inelastic

C) Larry's supply of lawn services is perfectly inelastic

D) the demand for Larry's services is perfectly inelastic

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is always true for a perfectly competitive firm?

A) MR = ATC

B) P = MR

C) P = ATC

D) P = AVC

A) MR = ATC

B) P = MR

C) P = ATC

D) P = AVC

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

25

Consider the perfectly competitive firm in the above figure. The shutdown point occurs at a price of

A) $22.00.

B) $16.00.

C) $12.00.

D) $11.00.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

26

In the above figure, at a price of $6, a perfectly competitive firm produces _______ and it _______.

A) 0; does not incur an economic loss or make an economic profit

B) 0; makes an economic profit

C) some output; incurs an economic loss

D) 0; incurs an economic loss

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

27

In a perfectly competitive market, technological advances bring _______ economic profits for producers and _______ lower prices for consumers.

A) temporary; temporarily

B) permanent; permanently

C) temporary; permanently

D) permanent; temporarily

A) temporary; temporarily

B) permanent; permanently

C) temporary; permanently

D) permanent; temporarily

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

28

Perfect competition arises if the _______ efficient scale of a single producer is _______ relative to the demand for the good or service.

A) maximum; small

B) minimum; small

C) minimum; large

D) maximum; large

A) maximum; small

B) minimum; small

C) minimum; large

D) maximum; large

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

29

As perfectly competitive firms leave a market because they are incurring an economic loss, the price of the good _______ and the economic loss of each remaining firm _______.

A) rises; decreases

B) rises; increases

C) falls; increases

D) falls; decreases

A) rises; decreases

B) rises; increases

C) falls; increases

D) falls; decreases

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

30

In the above figure, the firm's total economic profit is equal to

A) $200.

B) MR - MC.

C) $60.

D) $150.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

31

If perfectly competitive firms exit a market, the

A) profits of the remaining firms decrease.

B) output of the industry increases.

C) market supply curve shifts leftward.

D) price of the good or service falls.

A) profits of the remaining firms decrease.

B) output of the industry increases.

C) market supply curve shifts leftward.

D) price of the good or service falls.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

32

In the above figure, if the price is P1, the firm will produce

A) where ATC equals P1.

B) nothing.

C) where MC equals P1.

D) where MC equals ATC.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

33

If a perfectly competitive firm decides to shut down in the short run, its loss will equal its

A) minimum average variable cost, AVC.

B) total variable cost, TVC.

C) average total cost, ATC.

D) total fixed cost, TFC.

A) minimum average variable cost, AVC.

B) total variable cost, TVC.

C) average total cost, ATC.

D) total fixed cost, TFC.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

34

External economies are factors beyond the control of an individual firm that _______ as the total market output increases.

A) lower its profit

B) raise its costs

C) lower its costs

D) raise its marginal revenue

A) lower its profit

B) raise its costs

C) lower its costs

D) raise its marginal revenue

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

35

In the long- run equilibrium, perfectly competitive firms produce where

A) average revenue is zero.

B) average total cost is minimised.

C) marginal cost is minimised.

D) All of the above are correct.

A) average revenue is zero.

B) average total cost is minimised.

C) marginal cost is minimised.

D) All of the above are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

36

In the short run, perfectly competitive firms _______ but in the long run, perfectly competitive firms _______.

A) can incur an economic loss; make zero economic profit

B) can incur an economic loss; incur an economic loss

C) must make an economic profit; make an economic profit

D) can incur economic losses; make an economic profit

A) can incur an economic loss; make zero economic profit

B) can incur an economic loss; incur an economic loss

C) must make an economic profit; make an economic profit

D) can incur economic losses; make an economic profit

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

37

New reports indicate that eating turnips helps people remain healthy. The news shifts the demand curve for turnips rightward. In response, new farms enter the turnip industry. During the period in which the new farms are entering, the price of a turnip _______ and the economic profit of each existing firm _______ .

A) rises; falls

B) falls; rises

C) falls; falls

D) rises; rises

A) rises; falls

B) falls; rises

C) falls; falls

D) rises; rises

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

38

In the above figure, the line represented by the '4' is the

A) average total cost.

B) marginal revenue.

C) marginal cost.

D) average fixed cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

39

In the above figure, if the price is P1 and the firm produced Q1, the firm's economic profit is _______

Than if it produced Q2 and _______ than if it produced Q3.

A) more; less

B) more; more

C) less; less

D) less; more

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

40

A perfectly competitive firm has a total revenue curve that is

A) upward- sloping with a decreasing slope.

B) downward- sloping with a constant slope.

C) upward- sloping with a constant slope.

D) upward- sloping with an increasing slope.

A) upward- sloping with a decreasing slope.

B) downward- sloping with a constant slope.

C) upward- sloping with a constant slope.

D) upward- sloping with an increasing slope.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

41

Suppose firms in a perfectly competitive market are earning an economic profit. As new firms enter, the price _______ and the economic profit of each existing firm _______.

A) falls; decreases

B) rises; decreases

C) rises; increases

D) falls; increases

A) falls; decreases

B) rises; decreases

C) rises; increases

D) falls; increases

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

42

If a perfectly competitive firm finds that it is producing an amount of output such that MR > MC

And P > AVC, it will

A) decrease its output.

B) increase its output.

C) not change its behaviour.

D) leave the industry.

And P > AVC, it will

A) decrease its output.

B) increase its output.

C) not change its behaviour.

D) leave the industry.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

43

The firms in a perfectly competitive market are making an economic profit when new firms enter. The entry shifts the short- run market supply curve _______ , the market price _______, and each firm's economic profit _______.

A) leftward; falls; decreases

B) leftward; rises; decreases

C) rightward; falls; decreases

D) rightward; rises; increases

A) leftward; falls; decreases

B) leftward; rises; decreases

C) rightward; falls; decreases

D) rightward; rises; increases

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

44

A perfectly competitive firm will operate and incur an economic loss in the short run if

A) shareholders do not know about the loss.

B) it knows it can recoup the loss in the long run.

C) the loss can offset future profits.

D) the loss is smaller than its total fixed costs.

A) shareholders do not know about the loss.

B) it knows it can recoup the loss in the long run.

C) the loss can offset future profits.

D) the loss is smaller than its total fixed costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

45

In the long- run equilibrium for a perfectly competitive market,

A) the firms' economic profits are zero.

B) average total costs of production are minimised.

C) there is no incentive for entry or exit.

D) All of the above are correct.

A) the firms' economic profits are zero.

B) average total costs of production are minimised.

C) there is no incentive for entry or exit.

D) All of the above are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

46

Consider the perfectly competitive firm in the above figure. At the profit- maximising level of output, the firm is

A) incurring an economic loss equal to $123.50.

B) incurring an economic loss equal to $187.00.

C) making zero economic profit.

D) incurring an economic loss equal to $119.00.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

47

The figure above shows a perfectly competitive firm. The firm will shut down in the short run if total fixed costs

A) exceed total costs.

B) exceed $401.

C) are less than $200.

D) are between $201 and $400.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

48

The above figure shows the cost curves for a perfectly competitive firm. If all firms in the market have the same cost curves and the price equals $16 per unit,

A) over time, firms will leave this market.

B) over time, the price will fall as new firms enter the market.

C) the market is in its long- run equilibrium.

D) the firm is making zero economic profit.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

49

Because each perfectly competitive firm sells a product identical to that of the other firms,

A) each firm expects to earn some economic profit.

B) each firm tries to cut prices to increase its market share.

C) each firm's output is a perfect substitute for the output of any other firm.

D) the demand for each firm's product is perfectly inelastic.

A) each firm expects to earn some economic profit.

B) each firm tries to cut prices to increase its market share.

C) each firm's output is a perfect substitute for the output of any other firm.

D) the demand for each firm's product is perfectly inelastic.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

50

The table above shows some of the costs for a perfectly competitive firm. The firm will produce 9 units of output if the price per unit is

A) $500.

B) $300.

C) $200.

D) $1750.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

51

The above figure illustrates a firm's total revenue and total cost curves. Which one of the following statements is FALSE?

A) At an output above Q3 the firm incurs an economic loss.

B) At output Q2 the firm incurs an economic loss.

C) Economic profit is the vertical distance between the total revenue curve and the total cost curve.

D) At output Q1 the firm makes zero economic profit.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

52

Perfect competition exists in a market if

A) there are many firms producing an identical product.

B) there are many firms producing similar products, each of which may have unique features.

C) the firm is always at the break- even point where it is earning only a normal profit.

D) the firm is protected by a barrier to entry.

A) there are many firms producing an identical product.

B) there are many firms producing similar products, each of which may have unique features.

C) the firm is always at the break- even point where it is earning only a normal profit.

D) the firm is protected by a barrier to entry.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

53

The table above gives the total revenue and total cost for a perfectly competitive firm producing chocolate chip cookies. If the firm is producing 4 kilograms of cookies, to maximise its profit it will

A) continue producing 4 kilograms of cookies.

B) decrease its output.

C) increase its output.

D) shut down.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

54

In the above figure, if the price is $16 per unit, how many units will a profit- maximising perfectly competitive firm produce?

A) 30

B) 20

C) 35

D) 0

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

55

The figure above shows the marginal revenue and long- run cost curves for a perfectly competitive firm. Which of the following statements is true?

A) The firm will eventually decrease its production.

B) Over time, this firm will leave this industry.

C) The firm is earning positive economic profit.

D) The firm is producing at minimum long- run average cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

56

Suppose the cost curves in the above figure apply to all firms in the market. Then, if the initial price is P1, in the long run the market

A) supply will increase.

B) supply will decrease.

C) demand will increase.

D) demand will decrease.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

57

The short- run market supply curve for a perfectly competitive market is obtained by summing the part of each firm's

A) AVC curve that lies above its MC curve.

B) MC curve that lies above its AVC curve.

C) MC curve that lies below the AVC curve.

D) AVC curve that lies below the MC curve.

A) AVC curve that lies above its MC curve.

B) MC curve that lies above its AVC curve.

C) MC curve that lies below the AVC curve.

D) AVC curve that lies below the MC curve.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

58

If there are 1,000 rutabaga farms, all perfectly competitive, an increase in the price of fertiliser used for growing rutabagas will

A) decrease the total quantity of rutabagas supplied, because each farm's supply curve shifts leftward.

B) have no effect on the total quantity of rutabagas supplied, because each farm's supply curve is a vertical line.

C) have no effect on the total quantity of rutabagas supplied, because no farm has enough market power to raise the price.

D) reduce the total quantity of rutabagas supplied, because each farm's supply curve is a horizontal line and will shift upward.

A) decrease the total quantity of rutabagas supplied, because each farm's supply curve shifts leftward.

B) have no effect on the total quantity of rutabagas supplied, because each farm's supply curve is a vertical line.

C) have no effect on the total quantity of rutabagas supplied, because no farm has enough market power to raise the price.

D) reduce the total quantity of rutabagas supplied, because each farm's supply curve is a horizontal line and will shift upward.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

59

Giuseppe's Pizza is a perfectly competitive firm. The firm's costs are shown in the table above. If the market price is $15, what is Giuseppe's profit- maximising output?

A) 2 pizzas per hour

B) 4 pizzas per hour

C) 3 pizzas per hour

D) 0 pizzas per hour

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

60

A perfectly competitive market is in long- run equilibrium. Then market demand decreases. The decrease in demand leads to

A) firms incurring an economic loss in the short run.

B) firms entering the market in the long run.

C) a rise in the price in the short run.

D) None of the above.

A) firms incurring an economic loss in the short run.

B) firms entering the market in the long run.

C) a rise in the price in the short run.

D) None of the above.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

61

In a perfectly competitive market, which of the following determines the market price?

A) Market supply and a firm's demand

B) A firm's demand and its supply

C) Market demand and market supply

D) Market demand and a firm's supply

A) Market supply and a firm's demand

B) A firm's demand and its supply

C) Market demand and market supply

D) Market demand and a firm's supply

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

62

The doughnut market is perfectly competitive. The figure above shows the costs of a typical doughnut producer. In the short run, the doughnut producer's supply curve is the curve running from point _______ to point E.

A) A

B) B

C) C

D) D

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

63

If firms in a perfectly competitive industry are making zero economic profit, then

A) some of those firms will leave the industry, because firms cannot persistently go without making economic profit.

B) there is no incentive for either entry or exit.

C) some of the firms will temporarily shut down.

D) new firms will enter the industry, because the new entrants would be assured of doing as well as in their best forgone alternative.

A) some of those firms will leave the industry, because firms cannot persistently go without making economic profit.

B) there is no incentive for either entry or exit.

C) some of the firms will temporarily shut down.

D) new firms will enter the industry, because the new entrants would be assured of doing as well as in their best forgone alternative.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

64

The figure above shows the marginal revenue and costs of a perfectly competitive firm. The price the firm charges is

A) $16 per unit.

B) $4 per unit.

C) $8 per unit.

D) None of the above answers is correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

65

In a market with external economies, the long- run supply curve is negatively sloped because

A) of diseconomies of scale.

B) when demand increases, more firms join the market thereby driving up the cost of inputs.

C) the firms' costs fall as the market output increases.

D) in the long run a decrease in demand results in a lower price.

A) of diseconomies of scale.

B) when demand increases, more firms join the market thereby driving up the cost of inputs.

C) the firms' costs fall as the market output increases.

D) in the long run a decrease in demand results in a lower price.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

66

The figure above illustrates the short- run costs of Paul's Picture Frames Inc. The picture frame market is perfectly competitive and the market price is $30 a frame. Paul produces _______ frames each week, makes _______ of total revenue, and makes zero profit.

A) 200; $4,000; normal

B) 200; $4,000; economic

C) 300; $9,000; normal

D) 300; $9,000; economic

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is true regarding perfect competition?

I. The firms are price takers.

II. Marginal revenue equals the price of the product.

III. Established firms have no advantage over new firms.

A) I only

B) I, II and III

C) I and II

D) II and III

I. The firms are price takers.

II. Marginal revenue equals the price of the product.

III. Established firms have no advantage over new firms.

A) I only

B) I, II and III

C) I and II

D) II and III

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

68

Based on the table above which shows Chip's costs, if rice sells for $600 a tonne, Chip

A) incurs an economic loss and should shut down in the short run.

B) incurs an economic loss, but should stay open in the short run.

C) makes an economic profit, but should shut down in the short run.

D) makes an economic profit and should stay open in the short run.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

69

In the above figure, at a price of $4 per unit, a profit- maximising perfectly competitive firm will

A) shut down because its total revenue is less than its variable costs.

B) incur an economic loss.

C) produce 5 units.

D) Both answers A and B are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

70

If there is a permanent decrease in demand in a perfectly competitive market, then there is an initial _______ in price and existing firms _______.

A) rise; incur an economic loss

B) rise; make an economic profit

C) fall; incur an economic loss

D) fall; make an economic profit

A) rise; incur an economic loss

B) rise; make an economic profit

C) fall; incur an economic loss

D) fall; make an economic profit

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

71

A perfectly competitive firm maximises its profit by

A) setting its price so that it exceeds the marginal revenue.

B) cutting wages.

C) manipulating demand.

D) choosing to produce the quantity that sets MC equal to MR.

A) setting its price so that it exceeds the marginal revenue.

B) cutting wages.

C) manipulating demand.

D) choosing to produce the quantity that sets MC equal to MR.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

72

Based on the table above which shows Chip's costs, if rice sells for $600 a tonne, Chip's profit- maximising output is

A) between three and four tonnes.

B) less than one tonne.

C) between two and three tonnes.

D) between one and two tonnes.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

73

The figure above shows a perfectly competitive firm. In the short run, the firm will shut down

A) only if the AVC of producing 10 units is more than $20.

B) always.

C) only if the AVC curve reaches its minimum before 10 units are produced.

D) only if the AVC of producing 10 units is less than $20.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

74

Suppose firms in a perfectly competitive market are incurring an economic loss. As firms exit, the price _______ and the economic loss of the surviving firms _______.

A) falls; decreases

B) falls; increases

C) rises; increases

D) rises; decreases

A) falls; decreases

B) falls; increases

C) rises; increases

D) rises; decreases

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

75

In a perfectly competitive market you observe that, after a permanent increase in demand in the long run, price increases. You can conclude that this market exhibits _______.

A) external diseconomies

B) economies of scale

C) diseconomies of scale

D) external economies

A) external diseconomies

B) economies of scale

C) diseconomies of scale

D) external economies

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

76

A perfectly competitive firm that is producing a positive quantity of a good maximises its economic profit if it produces so that

A) marginal revenue = marginal cost.

B) total revenue = total cost.

C) average revenue = average total cost.

D) average total cost = average variable cost.

A) marginal revenue = marginal cost.

B) total revenue = total cost.

C) average revenue = average total cost.

D) average total cost = average variable cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

77

Consider the perfectly competitive firm in the figure above. At the profit- maximising level of output, the firm will

A) make an economic profit equal to the area ABCD.

B) incur an economic loss equal to the area ABCD.

C) make an economic profit equal to the area AECD.

D) make zero economic profit.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

78

Assuming long- run external diseconomies exist, when demand increases in a perfectly competitive market, in the long run the price of the product _______ the initial price (before the increase in demand) and the quantity _______.

A) rises above; increases

B) equals; increases

C) equals; decreases

D) falls below; decreases

A) rises above; increases

B) equals; increases

C) equals; decreases

D) falls below; decreases

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

79

In the long- run equilibrium, perfectly competitive firms produce the level of output such that

A) marginal cost is minimised.

B) average total cost is minimised.

C) marginal cost equals the price.

D) Both answers B and C are correct.

A) marginal cost is minimised.

B) average total cost is minimised.

C) marginal cost equals the price.

D) Both answers B and C are correct.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

80

The market for maple syrup is perfectly competitive. Suppose that the market is in long- run equilibrium when the market demand for maple syrup increases. What happens in the short run?

A) Firms will enter the market.

B) The existing firms increase production.

C) The existing firms decrease production.

D) Some of the existing firms shut down.

A) Firms will enter the market.

B) The existing firms increase production.

C) The existing firms decrease production.

D) Some of the existing firms shut down.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 150 flashcards in this deck.