Deck 11: Risk Neutral Trees and Derivative Pricing

Full screen (f)

Question

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a ?oor that pays at time t + 1 the following cash ?ow:

Question

You are given the following interest rate tree. Use it when required in the

exercises.

What is the benefit of using an interest rate model when compared to empirical estimates?

exercises.

What is the benefit of using an interest rate model when compared to empirical estimates?

Question

Question

Question

Question

You are given the following interest rate tree. Use it when required in the

exercises.

What are the main differences between the Ho-Lee model and the Black- Derman-Toy model?

exercises.

What are the main differences between the Ho-Lee model and the Black- Derman-Toy model?

Question

Question

Question

Question

Question

Question

You are given the following interest rate tree. Use it when required in the

exercises.

What advantage does the Black-Derman-Toy model have over the Ho-Lee model, when comparing the plausibility of the modeled interest rates?

exercises.

What advantage does the Black-Derman-Toy model have over the Ho-Lee model, when comparing the plausibility of the modeled interest rates?

Question

Question

Question

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a 2-year cap that pays at time t + 1 the following cash ?ow:

Question

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a ?oor that pays at time t + 1 the following cash ?ow:

Question

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a 2-year cap that pays at time t + 1 the following cash ?ow:

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/18

Play

Full screen (f)

Deck 11: Risk Neutral Trees and Derivative Pricing

1

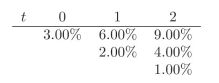

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a ?oor that pays at time t + 1 the following cash ?ow:

The price is 0.9357.

2

You are given the following interest rate tree. Use it when required in the

exercises.

What is the benefit of using an interest rate model when compared to empirical estimates?

exercises.

What is the benefit of using an interest rate model when compared to empirical estimates?

Interest rate models such as Ho-Lee and Black-Derman-Toy eliminate the posibilities for negative interest probabilities that may occur in simple empirical estimates.

3

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Compute the current zero coupon spot curve for all possible maturities.

We have: Z(0, 1) = 0.9704; Z(0, 2) = 0.9326; and Z(0, 3) = 0.8923.

4

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a 2-year swap with N = 100 and c =3%.

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

5

How do you compute the swap rate at initiation?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

6

You are given the following interest rate tree. Use it when required in the

exercises.

What are the main differences between the Ho-Lee model and the Black- Derman-Toy model?

exercises.

What are the main differences between the Ho-Lee model and the Black- Derman-Toy model?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

7

Suppose you want to hedge the cap with the swap, what is the hedge ratio?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

8

In the context of the futures market, what does 'cheapest-to-deliver' mean?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

9

What is the difference between flat volatility and forward volatility?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

10

What is the difference between empirical volatility and implied volatility?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

11

Does empirical σ (based on past realizations) price caps, floors and swap- tions acurately? On average does it overprice or underprice these securi- ties?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

12

You are given the following interest rate tree. Use it when required in the

exercises.

What advantage does the Black-Derman-Toy model have over the Ho-Lee model, when comparing the plausibility of the modeled interest rates?

exercises.

What advantage does the Black-Derman-Toy model have over the Ho-Lee model, when comparing the plausibility of the modeled interest rates?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

13

You find that the Black-Derman-Toy model predicts a rise in the short rate for both the next up period and the next down period. Given this information you decide to short Treasuries, since a future rise in interest rates will bring bond prices down. Is this right?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

14

If you use caps and bonds to fit the Black-Derman-Toy model, can you use the model to price the same caps and bonds?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

15

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a 2-year cap that pays at time t + 1 the following cash ?ow:

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

16

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a ?oor that pays at time t + 1 the following cash ?ow:

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

17

Assume that after you estimate the risk neutral model for the continously compounded rate you arrive at the tree presented at the beginning of this chapter. There is equal probability of moving up or down on the tree. Price a 2-year cap that pays at time t + 1 the following cash ?ow:

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

18

You find the implied volatility for a 5-year cap and you use it as an input for your model (Ho-Lee). Does this solve the problem with volatility when you want to price 1-year securities?

Unlock Deck

Unlock for access to all 18 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 18 flashcards in this deck.