Deck 2: Basics of Fixed Income Securities

Full screen (f)

Question

Question

Question

Question

Question

For the following scenario, check if there is a mispriced security:

Question

Question

Question

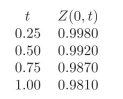

What is the price of a 0.75-year ?oating rate bond that pays a semiannual coupon equal to ?oating rate plus 2% spread? We know the following:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/20

Play

Full screen (f)

Deck 2: Basics of Fixed Income Securities

1

What is the price on a 5.75-year floating rate bond that pays a semiannual coupon (no spread)? We know the following:

a. There is a coupon bond paying 3% quarterly P (0, 0.25) = 100.0448.

b. Last quarter the semiannually compounded rate was 3%.

a. There is a coupon bond paying 3% quarterly P (0, 0.25) = 100.0448.

b. Last quarter the semiannually compounded rate was 3%.

The price of the floating rate bond is 100.7895.

2

What effect does inflation have on discount factors?

Higher inflation makes less appealing money in the future, so discount factors will go down.

3

From the following data obtain the discount curve:

a. A zero coupon bond Pz(0, 0.5) = 99.20.

b. A coupon bond paying 3% quarterly P (0, 0.25) = 100.5485.

c. A coupon bond paying 6% quarterly P (0, 0.75) = 100.1655.

d. A coupon bond paying 5% semiannually P (0, 1) = 103.0325.

a. A zero coupon bond Pz(0, 0.5) = 99.20.

b. A coupon bond paying 3% quarterly P (0, 0.25) = 100.5485.

c. A coupon bond paying 6% quarterly P (0, 0.75) = 100.1655.

d. A coupon bond paying 5% semiannually P (0, 1) = 103.0325.

The discount factors are the following:

4

A Treasury dealer quotes the following 91-day bill at a 3.956% discount. What is the price of the security?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

5

For the following scenario, check if there is a mispriced security:

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

6

You have two coupon bonds with same maturity, one pays 5% semiannu- ally and the other 5% quarterly. Which one has a higher yield?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

7

What is the price on a 4.5-year ?oating rate bond that pays a semiannual coupon (no spread)?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

8

What is the price of a 0.75-year ?oating rate bond that pays a semiannual coupon equal to ?oating rate plus 2% spread? We know the following:

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

9

For the following scenario, check if there is a mispriced security:

a. A zero coupon bond Pz(0, 0.5) = 99.00.

b. A coupon bond paying 6% quarterly P (0, 0.25) = 101.1955.

c. A coupon bond paying 4% quarterly P (0, 0.50) = 102.0830.

d. A coupon bond paying 7% semiannually P (0, 0.75) = 105.8440.

a. A zero coupon bond Pz(0, 0.5) = 99.00.

b. A coupon bond paying 6% quarterly P (0, 0.25) = 101.1955.

c. A coupon bond paying 4% quarterly P (0, 0.50) = 102.0830.

d. A coupon bond paying 7% semiannually P (0, 0.75) = 105.8440.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

10

Using the previous discount curve price the following: A 1-year coupon bond paying 4% quarterly.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

11

What is the price of a 0.5-year floating rate bond that pays a quarterly coupon equal to floating rate plus a 1% spread? We know the following:

a. There is a zero coupon bond Pz(0, 0.25) = 99.80.

b. There is a coupon bond paying 2% quarterly P (0, 0.5) = 100.3960.

a. There is a zero coupon bond Pz(0, 0.25) = 99.80.

b. There is a coupon bond paying 2% quarterly P (0, 0.5) = 100.3960.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

12

Can a bond be quoted in more than one interest rate?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

13

Do discount factors depend on compounding frequency? Why?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

14

For the following scenario, check if there is a mispriced security:

a. A coupon bond paying 1% quarterly P (0, 0.25) = 100.6498.

b. A coupon bond paying 4% semiannually P (0, 0.25) = 101.8980.

c. A coupon bond paying 3% quarterly P (0, 0.50) = 101.2978.

d. A coupon bond paying 5% quarterly P (0, 0.75) = 103.4425.

e. A coupon bond paying 4% semiannually P (0, 1.00) = 103.5880.

a. A coupon bond paying 1% quarterly P (0, 0.25) = 100.6498.

b. A coupon bond paying 4% semiannually P (0, 0.25) = 101.8980.

c. A coupon bond paying 3% quarterly P (0, 0.50) = 101.2978.

d. A coupon bond paying 5% quarterly P (0, 0.75) = 103.4425.

e. A coupon bond paying 4% semiannually P (0, 1.00) = 103.5880.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

15

For the following scenario, check if there is a mispriced security:

a. A zero coupon bond Pz(0, 0.5) = 99.50.

b. A coupon bond paying 3% quarterly P (0, 0.50) = 100.9948.

c. A coupon bond paying 5% quarterly P (0, 0.75) = 102.7288.

d. A coupon bond paying 2% semiannually P (0, 1.25) = 102.8720.

e. A zero coupon bond Pz(0, 1.25) = 98.4.

a. A zero coupon bond Pz(0, 0.5) = 99.50.

b. A coupon bond paying 3% quarterly P (0, 0.50) = 100.9948.

c. A coupon bond paying 5% quarterly P (0, 0.75) = 102.7288.

d. A coupon bond paying 2% semiannually P (0, 1.25) = 102.8720.

e. A zero coupon bond Pz(0, 1.25) = 98.4.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

16

Using the previous discount curve price the following: A zero coupon bond expiring at t =0.75.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

17

Using the previous discount curve price the following: A 9-month coupon bond paying 5% semiannually.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

18

Using the previous discount curve price the following: A 6-month coupon bond paying 7% semiannually.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

19

For the following scenario, check if there is a mispriced security:

a. A zero coupon bond Pz(0, 0.25) = 99.30.

b. A zero coupon bond Pz(0, 0.50) = 98.70.

c. A coupon bond paying 3% semiannually P (0, 0.50) = 100.1850.

d. A coupon bond paying 2% semiannually P (0, 0.75) = 101.4880.

a. A zero coupon bond Pz(0, 0.25) = 99.30.

b. A zero coupon bond Pz(0, 0.50) = 98.70.

c. A coupon bond paying 3% semiannually P (0, 0.50) = 100.1850.

d. A coupon bond paying 2% semiannually P (0, 0.75) = 101.4880.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

20

A Treasury dealer quotes the following 182-day bill at a 3.956% discount. What is the price of the security?

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 20 flashcards in this deck.