Deck 1: Conceptual and Case Analysis Frameworks for Financial Reporting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

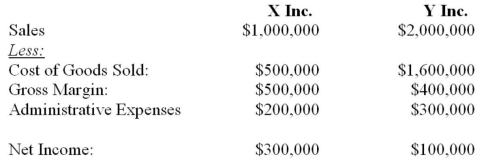

X Inc. and Y Inc. are virtually identical companies with identical cost structures and very similar business practices operating in the same lines of business. X Inc. is based in Canada while Y Inc. is based in Japan. The following were the condensed Income Statements for both companies for the year last year before both adopted IFRS. For the sake of simplicity, Y Inc.'s results have been translated into Canadian Dollars.  Given the information provided, what are some possible causes for the differing results of these companies?

Given the information provided, what are some possible causes for the differing results of these companies?

Given the information provided, what are some possible causes for the differing results of these companies? Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/41

Play

Full screen (f)

Deck 1: Conceptual and Case Analysis Frameworks for Financial Reporting

1

The degree of accounting disclosure required tends to be greater in countries with well-developed capital markets. Why is this?

A) Countries with well-developed capital markets also have well developed legal systems.

B) The disclosure requirements were designed to prevent fraud.

C) These markets tend to have more sophisticated investors who demand more information.

D) Companies in these countries are required to comply with GAAP.

A) Countries with well-developed capital markets also have well developed legal systems.

B) The disclosure requirements were designed to prevent fraud.

C) These markets tend to have more sophisticated investors who demand more information.

D) Companies in these countries are required to comply with GAAP.

C

2

Which decision has Canada made with respect to financial reporting for small and medium sized enterprise?

A) To adopt the IFRS standards for small and medium sized enterprises.

B) To retain the current standards.

C) To look to US GAAP for standards.

D) To develop and maintain its own standards for private enterprises.

A) To adopt the IFRS standards for small and medium sized enterprises.

B) To retain the current standards.

C) To look to US GAAP for standards.

D) To develop and maintain its own standards for private enterprises.

D

3

Accounting policies created in countries governed by code law tend to

A) has greater disclosure requirements on Financial Statements.

B) offer more favourable tax incentives to foreign countries.

C) offer greater protection to creditors and suppliers.

D) favour illicit activity.

A) has greater disclosure requirements on Financial Statements.

B) offer more favourable tax incentives to foreign countries.

C) offer greater protection to creditors and suppliers.

D) favour illicit activity.

C

4

Starting in 2011, what is the definition of a private enterprise (PE) under Canadian GAAP?

A) A corporation that has no public shareholders.

B) A corporation that has less than 500 shareholders and is not listed on a stock exchange.

C) A corporation which is not profit oriented.

D) A profit oriented enterprise that has none of its issued and outstanding financial instruments traded in a public market and does not hold assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses.

A) A corporation that has no public shareholders.

B) A corporation that has less than 500 shareholders and is not listed on a stock exchange.

C) A corporation which is not profit oriented.

D) A profit oriented enterprise that has none of its issued and outstanding financial instruments traded in a public market and does not hold assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

5

IMVAR INC is a U.S.-based Company with subsidiaries in both the United States and in Canada. The Company's Consolidated Financial Statements show a significantly higher net income when prepared under Canadian GAAP than under U.S. GAAP. What is the likely reason for this difference?

A) Different corporate tax rates in each country.

B) Timing differences which will reverse out in the future.

C) Differing reporting requirements in each country.

D) Currency fluctuations.

A) Different corporate tax rates in each country.

B) Timing differences which will reverse out in the future.

C) Differing reporting requirements in each country.

D) Currency fluctuations.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statement is correct?

A) IFRS rules are broader based than U.S. or Canadian GAAP.

B) Canadian accounting rules will be closer to those of the FASB in the next few years than to IFRS.

C) FASB standards are clearly superior to IFRS.

D) IFRS expressly prohibits the use of fair values and optional accounting treatments.

A) IFRS rules are broader based than U.S. or Canadian GAAP.

B) Canadian accounting rules will be closer to those of the FASB in the next few years than to IFRS.

C) FASB standards are clearly superior to IFRS.

D) IFRS expressly prohibits the use of fair values and optional accounting treatments.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

7

If a country's accounting income does not differ significantly from its taxable income, one would reasonably expect:

A) extreme conservatism on the part of accountants.

B) a significant amount of deferred taxes on the balance sheet.

C) that the use of LIFO would be more prevalent.

D) extreme conservatism on the part of accountants as well as increased use of LIFO.

A) extreme conservatism on the part of accountants.

B) a significant amount of deferred taxes on the balance sheet.

C) that the use of LIFO would be more prevalent.

D) extreme conservatism on the part of accountants as well as increased use of LIFO.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is true with respect to the implementation of IASB standards for the European Union?

A) These standards have been in place since 1985.

B) Beginning in 2005, all European companies whose shares trade on stock exchanges were required to prepare their consolidated financial statements in accordance with IFRSs.

C) All members of the European Union are required to comply with these standards with the exception of the United Kingdom.

D) Compliance with these standards by European public companies is strictly optional.

A) These standards have been in place since 1985.

B) Beginning in 2005, all European companies whose shares trade on stock exchanges were required to prepare their consolidated financial statements in accordance with IFRSs.

C) All members of the European Union are required to comply with these standards with the exception of the United Kingdom.

D) Compliance with these standards by European public companies is strictly optional.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

9

Income-smoothing has been applied to a German subsidiary of Company Inc, as it had an abnormally high operating income last year. Which of the following would the accountants working for the subsidiary likely have done?

A) Debited an expense account and credited an equity account.

B) Credited an expense account and debited an equity account.

C) Credited an expense account and debited a provision account appearing under the liabilities section.

D) Debited an expense account and credited a provision account appearing under the liabilities section.

A) Debited an expense account and credited an equity account.

B) Credited an expense account and debited an equity account.

C) Credited an expense account and debited a provision account appearing under the liabilities section.

D) Debited an expense account and credited a provision account appearing under the liabilities section.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

10

Countries are most likely to have similar accounting policies when:

A) they have greater political and economic ties.

B) they share a common language.

C) they are close to each other geographically.

D) their economies are of a similar size.

A) they have greater political and economic ties.

B) they share a common language.

C) they are close to each other geographically.

D) their economies are of a similar size.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is correct with respect to FASB and IFRSs' standards of accounting disclosure?

A) In general, pronouncements of FASB are more detailed, while those in IFRSs tend to rely more on professional judgement.

B) In general, pronouncements of FASB are less detailed, while those in IFRSs tend to rely more on professional judgement.

C) In general, pronouncements of FASB are more detailed, while those in IFRSs tend to rely less on professional judgement.

D) In general, pronouncements of FASB are less detailed, while those in IFRSs tend to rely less on professional judgement.

A) In general, pronouncements of FASB are more detailed, while those in IFRSs tend to rely more on professional judgement.

B) In general, pronouncements of FASB are less detailed, while those in IFRSs tend to rely more on professional judgement.

C) In general, pronouncements of FASB are more detailed, while those in IFRSs tend to rely less on professional judgement.

D) In general, pronouncements of FASB are less detailed, while those in IFRSs tend to rely less on professional judgement.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

12

What monumental decision to change the requirements for foreign registrants and their reporting in the U.S. under certain circumstances did the SEC make in 2007?

A) Foreign registrants could use IFRSs in preparing their financial statements without providing a reconciliation to US GAAP.

B) Foreign registrants must report under U.S. GAAP.

C) Foreign registrants may report under IFRS as long as they provide a reconciliation to U.S. GAAP.

D) The SEC has no jurisdiction over foreign registrants.

A) Foreign registrants could use IFRSs in preparing their financial statements without providing a reconciliation to US GAAP.

B) Foreign registrants must report under U.S. GAAP.

C) Foreign registrants may report under IFRS as long as they provide a reconciliation to U.S. GAAP.

D) The SEC has no jurisdiction over foreign registrants.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is LEAST likely to influence a country's accounting standards?

A) Taxation Policies.

B) Different Legal Systems.

C) The currency used.

D) Ties between countries.

A) Taxation Policies.

B) Different Legal Systems.

C) The currency used.

D) Ties between countries.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

14

In which of the following countries has income tax law had the greatest effect on its accounting policies?

A) Canada

B) The United Kingdom

C) Japan

D) The United States

A) Canada

B) The United Kingdom

C) Japan

D) The United States

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following would be most affected by financial Statements being prepared under different accounting principles?

A) Reduced comparability.

B) Reduced reliability.

C) Increased complexity.

D) Inaccurate asset valuations.

A) Reduced comparability.

B) Reduced reliability.

C) Increased complexity.

D) Inaccurate asset valuations.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following would NOT be a reason to obtain a greater understanding of accounting practices in other nations?

A) Financial results are disclosed in different currencies.

B) One needs to be aware of differing disclosure requirements from nation to nation, as this impacts the preparation of financial statements.

C) Income-smoothing may have affected a foreign subsidiary's results; such smoothing practices are not permitted in North America.

D) Departures from the historical cost principle may be possible in other nations.

A) Financial results are disclosed in different currencies.

B) One needs to be aware of differing disclosure requirements from nation to nation, as this impacts the preparation of financial statements.

C) Income-smoothing may have affected a foreign subsidiary's results; such smoothing practices are not permitted in North America.

D) Departures from the historical cost principle may be possible in other nations.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is a factor that can influence a country's accounting standards?

A) The level of development of capital markets.

B) Political policy.

C) Market practice.

D) Educational standards set for professional accountants.

A) The level of development of capital markets.

B) Political policy.

C) Market practice.

D) Educational standards set for professional accountants.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following bodies is responsible for the harmonization of international accounting standards?

A) The European Union (EU).

B) The Federal Accounting Standards Board (FASB).

C) The International Accounting Standards Board (IASB).

D) The Canadian Institute of Chartered Accountants (CICA).

A) The European Union (EU).

B) The Federal Accounting Standards Board (FASB).

C) The International Accounting Standards Board (IASB).

D) The Canadian Institute of Chartered Accountants (CICA).

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

19

What agreement was signed between the IASB and FASB in September 2002?

A) An agreement to set educational standards for accounting professionals in the United States.

B) An agreement to review US accounting standards to determine their appropriateness.

C) An agreement to develop international accounting standards based on U.S. GAAP.

D) An agreement to acknowledge their commitment to the development of high quality, compatible accounting standards for use in domestic and cross-border financial reporting.

A) An agreement to set educational standards for accounting professionals in the United States.

B) An agreement to review US accounting standards to determine their appropriateness.

C) An agreement to develop international accounting standards based on U.S. GAAP.

D) An agreement to acknowledge their commitment to the development of high quality, compatible accounting standards for use in domestic and cross-border financial reporting.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following nations is NOT governed by code (statute) law?

A) Germany

B) Japan

C) France

D) Canada

A) Germany

B) Japan

C) France

D) Canada

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

21

The European Union has attempted to harmonize accounting principles amongst its member nations by issuing:

A) statutes.

B) standards.

C) bylaws.

D) directives.

A) statutes.

B) standards.

C) bylaws.

D) directives.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

22

The predecessor to the International Accounting Standards Board (IASB) was:

A) the Federal Accounting Standards Board (FASB).

B) the Canadian Institute of Chartered Accountants (CICA).

C) the European Economic Community (EEC).

D) the International Accounting Standards Committee (IASC).

A) the Federal Accounting Standards Board (FASB).

B) the Canadian Institute of Chartered Accountants (CICA).

C) the European Economic Community (EEC).

D) the International Accounting Standards Committee (IASC).

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

23

One of the underlying assumptions of the Historical Cost Principle is that a stable unit of measure (currency) should be used for Financial Reporting. Is this always the case? How have some countries attempted to adjust for any limitations associated with the Historical Cost Principle?

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

24

What choice(s) do private enterprises have in their financial reporting in Canada?

A) They have no choice at all; they will need to report under IFRS.

B) They may elect to continue with differential reporting.

C) They may adopt accounting principles that are appropriate to the circumstances.

D) They may elect to report under either IFRS or ASPE.

A) They have no choice at all; they will need to report under IFRS.

B) They may elect to continue with differential reporting.

C) They may adopt accounting principles that are appropriate to the circumstances.

D) They may elect to report under either IFRS or ASPE.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following is NOT a reason why a Canadian private company would elect to report under IFRS?

A) The company is planning to go public in the near future.

B) The company seeks comparability with public companies of a similar size.

C) It is likely to be less expensive than reporting under ASPE.

D) The company is a subsidiary of a Canadian public company.

A) The company is planning to go public in the near future.

B) The company seeks comparability with public companies of a similar size.

C) It is likely to be less expensive than reporting under ASPE.

D) The company is a subsidiary of a Canadian public company.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

26

What approach did Canada first decide to take with respect to convergence with IFRSs?

A) Harmonization of Canadian GAAP with IFRS.

B) Substituting IFRS's for Canadian GAAP when approved by the IASB.

C) Adopting some but not necessarily all IFRSs by reviewing them on a case by case basis.

D) Reviewing them with all publically accountable entities to see which ones would be acceptable.

A) Harmonization of Canadian GAAP with IFRS.

B) Substituting IFRS's for Canadian GAAP when approved by the IASB.

C) Adopting some but not necessarily all IFRSs by reviewing them on a case by case basis.

D) Reviewing them with all publically accountable entities to see which ones would be acceptable.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

27

What are Canadian companies whose shares trade on U.S. stock exchanges required to do?

A) Provide two sets of Financial Statements -- one under Canadian GAAP and one under U.S. GAAP.

B) Present reconciliations from Canadian GAAP to U.S. GAAP in the footnotes to their financial statements.

C) File reports using either IFRS or US GAAP.

D) Revalue their assets using the lower-of -cost-and-market principle.

A) Provide two sets of Financial Statements -- one under Canadian GAAP and one under U.S. GAAP.

B) Present reconciliations from Canadian GAAP to U.S. GAAP in the footnotes to their financial statements.

C) File reports using either IFRS or US GAAP.

D) Revalue their assets using the lower-of -cost-and-market principle.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

28

The CICA Handbook -- Accounting is the handbook of Canadian accounting standards. Why do companies in Canada ensure that their financial reporting is consistent with Canadian GAAP?

A) Their bank requires them to do so.

B) Their auditors require them to do so.

C) Reporting under the CICA Handbook -- Accounting is required by public companies' boards of directors.

D) Compliance with the CICA Handbook -- Accounting pronouncements is usually required by incorporation statutes and stock exchanges.

A) Their bank requires them to do so.

B) Their auditors require them to do so.

C) Reporting under the CICA Handbook -- Accounting is required by public companies' boards of directors.

D) Compliance with the CICA Handbook -- Accounting pronouncements is usually required by incorporation statutes and stock exchanges.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

29

List 5 factors that can influence a country's accounting standards.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

30

Prior to adoption of IFRS in 2011, Canada's accounting policies most resembled those of which nation?

A) The United Kingdom.

B) The United States.

C) The European Union (EU)

D) Australia

A) The United Kingdom.

B) The United States.

C) The European Union (EU)

D) Australia

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

31

For which of the following types of organizations does the CICA Handbook - Accounting not provide specific accounting standards?

A) Publicly accountable enterprises.

B) Private enterprises.

C) Not-for-profit organizations.

D) Proprietorships.

A) Publicly accountable enterprises.

B) Private enterprises.

C) Not-for-profit organizations.

D) Proprietorships.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following accounting standards have been revised by the FASB to be fully consistent with IFRS?

A) Liabilities and equity.

B) Leases.

C) Research and development costs.

D) Consolidations.

A) Liabilities and equity.

B) Leases.

C) Research and development costs.

D) Consolidations.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

33

X Inc. and Y Inc. are virtually identical companies with identical cost structures and very similar business practices operating in the same lines of business. X Inc. is based in Canada while Y Inc. is based in Japan. The following were the condensed Income Statements for both companies for the year last year before both adopted IFRS. For the sake of simplicity, Y Inc.'s results have been translated into Canadian Dollars. Given the information provided, what are some possible causes for the differing results of these companies?

Given the information provided, what are some possible causes for the differing results of these companies? Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

34

Many large corporations have operation in numerous countries around the world. As a result, they need to raise debt and equity in order to finance their operations in many different countries. Has the movement towards converging global reporting standards made it easier for corporations to raise capital in many different capital markets around the world?

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

35

Which enterprises must report under IFRSs in Canada?

A) All corporations, government agencies and private companies.

B) Public companies and private companies whose shareholders' equity is in excess of $500,000,000 at any particular year end.

C) Public companies, private companies and not-for-profit organizations.

D) Publicly accountable enterprises.

A) All corporations, government agencies and private companies.

B) Public companies and private companies whose shareholders' equity is in excess of $500,000,000 at any particular year end.

C) Public companies, private companies and not-for-profit organizations.

D) Publicly accountable enterprises.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

36

Briefly discuss the anticipated changes to accounting standards in Canada over the next few years.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

37

Canada and the U.S. both experimented with price level accounting in the 1970s. This practice was quickly abandoned largely because

A) inflation rates declined after the 1970s.

B) the cost of providing this information was quite high.

C) it was a clear violation of the Historical Cost Principle.

D) it provided disclosure figure which were not verifiable.

A) inflation rates declined after the 1970s.

B) the cost of providing this information was quite high.

C) it was a clear violation of the Historical Cost Principle.

D) it provided disclosure figure which were not verifiable.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is a major restructuring objective of the IASB?

A) To ensure compliance to a single set of accounting standards.

B) To progressively phase out divergent accounting practices.

C) To promote a greater understanding of the accounting practices of different nations.

D) To cooperate with various national accounting standard-setters in order to achieve convergence in accounting standards around the world.

A) To ensure compliance to a single set of accounting standards.

B) To progressively phase out divergent accounting practices.

C) To promote a greater understanding of the accounting practices of different nations.

D) To cooperate with various national accounting standard-setters in order to achieve convergence in accounting standards around the world.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

39

Asset revaluations, unlike in Canada, have been acceptable in many countries for accounting purposes. Which of the following adjustments have been allowed?

A) Price level adjusted historical costs.

B) Periodic adjustment of asset valuations to current replacement cost.

C) Immediate write off of purchased goodwill to equity.

D) All of the above.

A) Price level adjusted historical costs.

B) Periodic adjustment of asset valuations to current replacement cost.

C) Immediate write off of purchased goodwill to equity.

D) All of the above.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

40

Briefly list the two types of legal systems in existence today and discuss how they would affect the accounting standards of a nation.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

41

What disclosure requirements must be met when a Canadian company adopts IFRS for the first time?

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 41 flashcards in this deck.