Deck 13: The Complete Income Statement

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Mountain Corp. experienced the following events and transactions during 2010:  Using the numbers of the events and transactions, identify which of the following sequences is the correct order for presenting the items on the income statement.

Using the numbers of the events and transactions, identify which of the following sequences is the correct order for presenting the items on the income statement.

A) 5, 1, 3, 2

B) 4, 3, 5, 2

C) 4, 5, 2, 3

D) 1, 4, 3, 5, 2

Using the numbers of the events and transactions, identify which of the following sequences is the correct order for presenting the items on the income statement.A) 5, 1, 3, 2

B) 4, 3, 5, 2

C) 4, 5, 2, 3

D) 1, 4, 3, 5, 2

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before change in accounting principle?

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before change in accounting principle?

a. $55,000

b. $60,000

c. $65,700

d. $42,160

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before change in accounting principle? a. $55,000

b. $60,000

c. $65,700

d. $42,160

Question

The following are the revenue and expense accounts for the year ending August 31, 2009, for Hammer Corporation:

A. Calculate the amount of gross profit for Hammer Corporation for the year ending August 31, 2009.

A. Calculate the amount of gross profit for Hammer Corporation for the year ending August 31, 2009.

B. How much should be reported as 'Other Revenues'?

A. Calculate the amount of gross profit for Hammer Corporation for the year ending August 31, 2009.B. How much should be reported as 'Other Revenues'?

Question

Question

Question

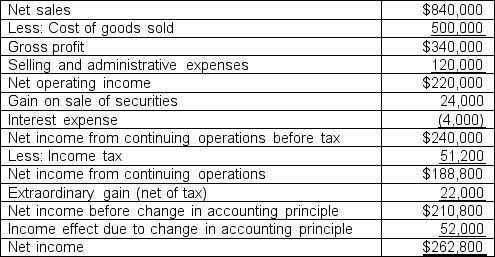

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of net operating income?

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of net operating income?

a. $44,000

b. $60,000

c. $47,200

d. $52,700

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of net operating income? a. $44,000

b. $60,000

c. $47,200

d. $52,700

Question

The following income statement was reported by Snappy Seacraft Company for the year ending December 31, 2010:

Assume Snappy has an average of 25,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

Assume Snappy has an average of 25,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

a. $0.12

b. $0.20

c. $0.08

d. $0.60

Assume Snappy has an average of 25,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment? a. $0.12

b. $0.20

c. $0.08

d. $0.60

Question

Question

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before extraordinary items and change in accounting principle?

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before extraordinary items and change in accounting principle?

a. $37,760

b. $60,000

c. $65,700

d. $52,700

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before extraordinary items and change in accounting principle? a. $37,760

b. $60,000

c. $65,700

d. $52,700

Question

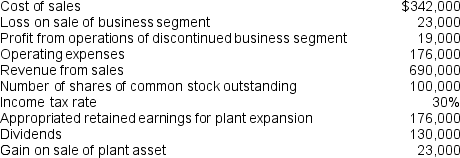

Gleeson Industries consists of four separate divisions: compressed wood products, chemicals, stone products, and plastics. On March 15, 2010, Gleeson sold the chemicals division for $625,000 cash. Financial information related to the chemicals division follows:

The journal entry to record the sale of the chemicals division will include:

The journal entry to record the sale of the chemicals division will include:

a. a debit to Loss on Disposal of Business Segment for $175,000.

b. a debit to Assets for $1,850,000.

c . a debit to Extraordinary Gain for $175,000.

d. a credit to Gain on Disposal of Business Segment for $175,000.

The journal entry to record the sale of the chemicals division will include: a. a debit to Loss on Disposal of Business Segment for $175,000.

b. a debit to Assets for $1,850,000.

c . a debit to Extraordinary Gain for $175,000.

d. a credit to Gain on Disposal of Business Segment for $175,000.

Question

Gleeson Industries consists of four separate divisions: compressed wood products, chemicals, stone products, and plastics. On March 15, 2010, Gleeson sold the chemicals division for $625,000 cash. Financial information related to the chemicals division follows:

If the income tax rate for the company is 35%, what amount of income tax liability on the disposal of the business segment will be recognized?

If the income tax rate for the company is 35%, what amount of income tax liability on the disposal of the business segment will be recognized?

a. $218,750

b. $61,250

c. $5,250

d. $157,500

If the income tax rate for the company is 35%, what amount of income tax liability on the disposal of the business segment will be recognized? a. $218,750

b. $61,250

c. $5,250

d. $157,500

Question

Question

Question

The following income statement was reported by Snappy Seacraft Company for the year ending December 31, 2010:

Assume Snappy has an average of 15,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

Assume Snappy has an average of 15,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

a. $0.33

b. $0.20

c. $1.00

d. $0.73

Assume Snappy has an average of 15,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment? a. $0.33

b. $0.20

c. $1.00

d. $0.73

Question

Question

Question

The following information was taken from the 2010 financial records of Hopewell Company.

The company's income tax rate is 35 percent, and the items above are treated identically for the financial reporting and tax purposes.

The company's income tax rate is 35 percent, and the items above are treated identically for the financial reporting and tax purposes.

REQUIRED:

Prepare an income statement using this information.

The company's income tax rate is 35 percent, and the items above are treated identically for the financial reporting and tax purposes.REQUIRED:

Prepare an income statement using this information.

Question

Question

Question

Question

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant associated with the credit line is expressed as 20 percent of net income?

What is the maximum amount of dividends Sunrise can pay if the covenant associated with the credit line is expressed as 20 percent of net income?

a. $55,000

b. $60,000

c. $52,560

d. $53,700

What is the maximum amount of dividends Sunrise can pay if the covenant associated with the credit line is expressed as 20 percent of net income? a. $55,000

b. $60,000

c. $52,560

d. $53,700

Question

Question

Question

Jarvis Company provided the following information for the year ending December 31, 2009:

Prepare an income statement in good form. You may omit the heading. Include all earnings per share amounts required for the year ending December 31, 2009.

Prepare an income statement in good form. You may omit the heading. Include all earnings per share amounts required for the year ending December 31, 2009.

Prepare an income statement in good form. You may omit the heading. Include all earnings per share amounts required for the year ending December 31, 2009. Question

Question

Question

Hilton Corporation's income statement for the year ending December 31, 2009, appears below.  Compute the maximum amount of dividends Hilton can pay if it has a debt covenant expressed as 20 percent of net income, and as 20 percent of net operating income. Which amount would a creditor more likely use as the restriction on dividends? Explain.

Compute the maximum amount of dividends Hilton can pay if it has a debt covenant expressed as 20 percent of net income, and as 20 percent of net operating income. Which amount would a creditor more likely use as the restriction on dividends? Explain.

Compute the maximum amount of dividends Hilton can pay if it has a debt covenant expressed as 20 percent of net income, and as 20 percent of net operating income. Which amount would a creditor more likely use as the restriction on dividends? Explain. Question

Question

Question

Question

Question

Question

Question

Question

The following are the revenue and expense accounts of the current year for ABCO Corporation:

All items are before income taxes. The income tax rate is 20%. Calculate any extraordinary gain or loss that should be disclosed on the income statement.

All items are before income taxes. The income tax rate is 20%. Calculate any extraordinary gain or loss that should be disclosed on the income statement.

All items are before income taxes. The income tax rate is 20%. Calculate any extraordinary gain or loss that should be disclosed on the income statement. Question

Question

Question

The following are some accounts for Marvell Corp. for 2009:

All amounts are before income taxes. Marvell has a 30% tax rate. Determine the amount of Marvell' 'other revenue' and 'other expenses' for 2009. List all non-income statement items and indicate on which financial statement they are reported.

All amounts are before income taxes. Marvell has a 30% tax rate. Determine the amount of Marvell' 'other revenue' and 'other expenses' for 2009. List all non-income statement items and indicate on which financial statement they are reported.

All amounts are before income taxes. Marvell has a 30% tax rate. Determine the amount of Marvell' 'other revenue' and 'other expenses' for 2009. List all non-income statement items and indicate on which financial statement they are reported. Question

Question

Balance sheet information of Digital Solutions, Inc. at December 31, 2008, is provided below.

During 2009, the company entered into the following transactions:

During 2009, the company entered into the following transactions:

A. Which transactions are operating?

A. Which transactions are operating?

B. Compute net income for the year ending December 31, 2009.

C. Compute comprehensive income for the year ending December 31, 2009.

During 2009, the company entered into the following transactions: A. Which transactions are operating?B. Compute net income for the year ending December 31, 2009.

C. Compute comprehensive income for the year ending December 31, 2009.

Question

The following information was taken from the accounting records of ABCO Corporation for the year ending December 31, 2009.

A. In good form, prepare the section of the income statement that begins immediately under 'income from continuing operations'. Do not be concerned with calculating the amount reported as 'income from continuing operations.'

A. In good form, prepare the section of the income statement that begins immediately under 'income from continuing operations'. Do not be concerned with calculating the amount reported as 'income from continuing operations.'

B. List all the items that would appear in the 'Other Revenue/Other Expenses' section of the income statement.

C. How is the number of shares of common stock outstanding used on the income statement?

A. In good form, prepare the section of the income statement that begins immediately under 'income from continuing operations'. Do not be concerned with calculating the amount reported as 'income from continuing operations.'B. List all the items that would appear in the 'Other Revenue/Other Expenses' section of the income statement.

C. How is the number of shares of common stock outstanding used on the income statement?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/85

Play

Full screen (f)

Deck 13: The Complete Income Statement

1

On the income statement, the result of changing from double-declining-balance to straight-line depreciation is found in

A) operating revenues and expenses.

B) other revenues or expenses.

C) extraordinary gains or losses.

D) cumulative effects.

A) operating revenues and expenses.

B) other revenues or expenses.

C) extraordinary gains or losses.

D) cumulative effects.

D

2

Which one of the following events is an operating transaction?

A) Purchase of equipment

B) Payment for equipment rental

C) Purchase of land

D) Issuing bonds for cash

A) Purchase of equipment

B) Payment for equipment rental

C) Purchase of land

D) Issuing bonds for cash

B

3

Which of the following statements is false regarding diluted earnings per share?

A) Reporting diluted earnings per share is required by GAAP when potentially significant dilution of EPS exists.

B) Diluted earnings per share can be used to reflect the extent of potential share dilution.

C) Diluted earnings per share is not reported by some companies.

D) Diluted earnings per share is always the same as basic earnings per share.

A) Reporting diluted earnings per share is required by GAAP when potentially significant dilution of EPS exists.

B) Diluted earnings per share can be used to reflect the extent of potential share dilution.

C) Diluted earnings per share is not reported by some companies.

D) Diluted earnings per share is always the same as basic earnings per share.

D

4

On the income statement, a gain from the sale of stock is reported as

A) operating revenues and expenses.

B) other revenues or expenses.

C) a disposal of a business segment.

D) an extraordinary gain or loss.

E) a cumulative effect of a change in accounting principle.

A) operating revenues and expenses.

B) other revenues or expenses.

C) a disposal of a business segment.

D) an extraordinary gain or loss.

E) a cumulative effect of a change in accounting principle.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

5

On the income statement, usual and frequent income events are found in

A) operating revenues and expenses.

B) other revenues or expenses.

C) disposal of a business segment.

D) extraordinary gains or losses.

E) cumulative effects.

A) operating revenues and expenses.

B) other revenues or expenses.

C) disposal of a business segment.

D) extraordinary gains or losses.

E) cumulative effects.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

6

Which one of the following is a nonoperating event that must be reported on the income statement?

A) Acquisition of a plant asset to be used in operations

B) Extraordinary items

C) Recognition of inventory expense

D) Consumption of office supplies

A) Acquisition of a plant asset to be used in operations

B) Extraordinary items

C) Recognition of inventory expense

D) Consumption of office supplies

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

7

On the income statement, the result of selling equipment is reported as a(n)

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

E) cumulative effect of a change in accounting principle.

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

E) cumulative effect of a change in accounting principle.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

8

On the income statement, the loss of equipment caused by the eruption of a volcano in the Northeastern United States is found in

A) operating revenues and expenses.

B) extraordinary gains or losses.

C) disposal of a business segment.

D) other revenues or expenses.

A) operating revenues and expenses.

B) extraordinary gains or losses.

C) disposal of a business segment.

D) other revenues or expenses.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

9

Recognition of bad debt expense is an event considered to be

A) an operating activity cash flow.

B) both unusual and infrequent.

C) neither unusual nor infrequent.

D) a financing cash flow.

A) an operating activity cash flow.

B) both unusual and infrequent.

C) neither unusual nor infrequent.

D) a financing cash flow.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

10

A summary of operating events is found

A) only in the asset section of the balance sheet.

B) only in the investment and financing sections of the cash flow statement.

C) only in the cash flows from operations section of the cash flow statement.

D) only in the income statement.

E) in the cash flows from operations section of the cash flow statement, and in the income statement.

A) only in the asset section of the balance sheet.

B) only in the investment and financing sections of the cash flow statement.

C) only in the cash flows from operations section of the cash flow statement.

D) only in the income statement.

E) in the cash flows from operations section of the cash flow statement, and in the income statement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

11

On the income statement, marketing expenses are reported as

A) operating revenues and expenses.

B) other revenues or expenses.

C) the disposal of a business segment.

D) an extraordinary gain or loss.

E) a cumulative effect.

A) operating revenues and expenses.

B) other revenues or expenses.

C) the disposal of a business segment.

D) an extraordinary gain or loss.

E) a cumulative effect.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

12

Operating events include

A) the payment of dividends and accounting principle changes.

B) inflows and outflows of assets due to the generation of revenues.

C) purchases, sales, and exchanges of long-term assets.

D) expenses and costs of acquiring plant assets .

A) the payment of dividends and accounting principle changes.

B) inflows and outflows of assets due to the generation of revenues.

C) purchases, sales, and exchanges of long-term assets.

D) expenses and costs of acquiring plant assets .

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

13

All of the following are termed considered to be operating revenues or expenses that are usual and frequent except

A) the sale of furniture by a furniture company.

B) interest expense related to financing with bonds.

C) depreciation expense on machinery.

D) delivery cost of goods .

A) the sale of furniture by a furniture company.

B) interest expense related to financing with bonds.

C) depreciation expense on machinery.

D) delivery cost of goods .

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

14

Financing transactions include

A) exchanges with shareholders.

B) revenues.

C) expenses.

D) most transactions that impact the income statement.

A) exchanges with shareholders.

B) revenues.

C) expenses.

D) most transactions that impact the income statement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

15

On the income statement, the loss from selling an independent business component of the company is reported as a(n)

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

16

On the income statement, interest revenue is found in

A) operating revenues and expenses.

B) other revenues or expenses.

C) the disposal of a business segment section.

D) the extraordinary gains or losses section.

E) the cumulative effects section.

A) operating revenues and expenses.

B) other revenues or expenses.

C) the disposal of a business segment section.

D) the extraordinary gains or losses section.

E) the cumulative effects section.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

17

Which one of the following events is not an operating transaction related to a company's primary activity?

A) Disposal of a business segment

B) Purchase of equipment

C) Payment for equipment maintenance

D) Purchase of inventory

A) Disposal of a business segment

B) Purchase of equipment

C) Payment for equipment maintenance

D) Purchase of inventory

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

18

On the income statement, interest expense is reported as a(n)

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

E) cumulative effect of a change in accounting principle.

A) operating revenue or expense.

B) other revenue or expense.

C) disposal of a business segment.

D) extraordinary gain or loss.

E) cumulative effect of a change in accounting principle.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

19

Which one of the following events is an operating transaction?

A) Payment of office supplies

B) Change in depreciation accounting principle

C) Purchase of another company for stock

D) Disposal of a business segment

A) Payment of office supplies

B) Change in depreciation accounting principle

C) Purchase of another company for stock

D) Disposal of a business segment

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

20

Non-operating items are found in the

A) asset section of the balance sheet.

B) liability section of the balance sheet.

C) cash flows from operations section of the cash flow statement.

D) income statement.

A) asset section of the balance sheet.

B) liability section of the balance sheet.

C) cash flows from operations section of the cash flow statement.

D) income statement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

21

On the income statement, unusual OR infrequent income events are found in

A) operating revenues and expenses.

B) other revenues or expenses.

C) disposal of a business segment.

D) extraordinary gains or losses.

E) cumulative effects.

A) operating revenues and expenses.

B) other revenues or expenses.

C) disposal of a business segment.

D) extraordinary gains or losses.

E) cumulative effects.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

22

Why is income so important to both investors and stock analysts?

A) It is strongly correlated to the market price of stock and bond prices.

B) It is equal to the amount that shareholders will receive as dividends.

C) Income is tied directly to revenue, i.e., a company that reports a large amount of revenue will always report a large amount of income.

D) It identifies if the company will be able to pay its current debts when they become due.

A) It is strongly correlated to the market price of stock and bond prices.

B) It is equal to the amount that shareholders will receive as dividends.

C) Income is tied directly to revenue, i.e., a company that reports a large amount of revenue will always report a large amount of income.

D) It identifies if the company will be able to pay its current debts when they become due.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

23

Carman, Inc. properly reported a change in accounting principle during 2009. This company must

A) have violated GAAP by not applying accounting principles consistently.

B) have convinced its auditors that the environment in which it operates has changed and another method is more appropriate.

C) be trying to cover up accounting errors.

D) have initially used the wrong method.

A) have violated GAAP by not applying accounting principles consistently.

B) have convinced its auditors that the environment in which it operates has changed and another method is more appropriate.

C) be trying to cover up accounting errors.

D) have initially used the wrong method.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

24

Which one of the following items is considered part of comprehensive income but not reported as part of net income?

A) Accounting principle changes

B) Foreign currency translation adjustments

C) Gain on sale of land

D) Dividend revenue

A) Accounting principle changes

B) Foreign currency translation adjustments

C) Gain on sale of land

D) Dividend revenue

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

25

Comprehensive income

A) may be reported on a separate statement or on the face of the income statement.

B) can be used as an alternative format of the traditional income statement.

C) includes some revenue and expense items that are part of continuing operations.

D) can be prepared instead of the shareholders' equity section of the balance sheet.

A) may be reported on a separate statement or on the face of the income statement.

B) can be used as an alternative format of the traditional income statement.

C) includes some revenue and expense items that are part of continuing operations.

D) can be prepared instead of the shareholders' equity section of the balance sheet.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

26

Paulson, Inc. reported net income of $60,000 during 2010. Throughout 2010, 20,000 shares of common stock and 5,000 shares of preferred stock were outstanding. The preferred stock has no dividend preference. Evans reported earnings only for continuing operations items. How much is earnings per share for 2010?

A) $3.00

B) $12.00

C) $2.00

D) Not enough information is provided.

A) $3.00

B) $12.00

C) $2.00

D) Not enough information is provided.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

27

Intraperiod tax allocation

A) is applied to each income statement item to provide creditors and investors a better indication of the company's true revenues and expenses.

B) is a method of allocating income taxes over multiple accounting periods.

C) is applied only to revenues since expenses are not taxed.

D) is applied to net income from continuing operations.

A) is applied to each income statement item to provide creditors and investors a better indication of the company's true revenues and expenses.

B) is a method of allocating income taxes over multiple accounting periods.

C) is applied only to revenues since expenses are not taxed.

D) is applied to net income from continuing operations.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

28

One objective of financial reporting is to provide information that is

A) helpful in assessing the amounts, timing, and uncertainty of future cash flows.

B) useful for competitors who need to assess economic activities.

C) a forecast of future operations.

D) unavailable to management.

A) helpful in assessing the amounts, timing, and uncertainty of future cash flows.

B) useful for competitors who need to assess economic activities.

C) a forecast of future operations.

D) unavailable to management.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

29

An income statement prepared with separate components

A) enables users to distinguish transactions that are due to operations from those that are not useful as predictors of future performance.

B) is prepared for income items that are frequent and usual.

C) is used primarily by companies involved with complex financing transactions.

D) may replace a statement of cash flows. .

A) enables users to distinguish transactions that are due to operations from those that are not useful as predictors of future performance.

B) is prepared for income items that are frequent and usual.

C) is used primarily by companies involved with complex financing transactions.

D) may replace a statement of cash flows. .

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

30

Mountain Corp. experienced the following events and transactions during 2010: Using the numbers of the events and transactions, identify which of the following sequences is the correct order for presenting the items on the income statement.

A) 5, 1, 3, 2

B) 4, 3, 5, 2

C) 4, 5, 2, 3

D) 1, 4, 3, 5, 2

Using the numbers of the events and transactions, identify which of the following sequences is the correct order for presenting the items on the income statement.A) 5, 1, 3, 2

B) 4, 3, 5, 2

C) 4, 5, 2, 3

D) 1, 4, 3, 5, 2

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

31

Publicly held companies must disclose earnings per share for all of the following except for

A) income from continuing operations.

B) losses from discontinued segments of a business.

C) other revenue and expense items.

D) cumulative effects resulting from changes in accounting principles.

A) income from continuing operations.

B) losses from discontinued segments of a business.

C) other revenue and expense items.

D) cumulative effects resulting from changes in accounting principles.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

32

Which one of the following is true about earnings per share?

A) Must be calculated as earnings per 'preferred' share

B) Must be calculated as earnings per 'common' share

C) May be increased or decreased because of outstanding stock options or convertible debt

D) Appears with the gross profit percentage on the income statement

A) Must be calculated as earnings per 'preferred' share

B) Must be calculated as earnings per 'common' share

C) May be increased or decreased because of outstanding stock options or convertible debt

D) Appears with the gross profit percentage on the income statement

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

33

If a loss is unusual in nature but not infrequent in occurrence, the loss should be disclosed

A) as an extraordinary item, net of taxes.

B) in the footnotes.

C) as a separate component of income from continuing operations.

D) as a separate item after the extraordinary items, net of taxes.

A) as an extraordinary item, net of taxes.

B) in the footnotes.

C) as a separate component of income from continuing operations.

D) as a separate item after the extraordinary items, net of taxes.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

34

Which one of the following transactions or events is never treated as an extraordinary item?

A) Losses from the early extinguishment of long-term bonds

B) Losses from flooding in locations where flooding is uncommon and has never occurred before

C) Operating losses from the discontinued segment of a business

D) Losses from volcanic eruptions in Kansas

A) Losses from the early extinguishment of long-term bonds

B) Losses from flooding in locations where flooding is uncommon and has never occurred before

C) Operating losses from the discontinued segment of a business

D) Losses from volcanic eruptions in Kansas

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

35

Which one of the following is true concerning discontinued operations?

A) It relates primarily to product changes in a company.

B) The gain or loss associated with the disposal is shown separately as a component of continuing operations on the income statement.

C) It is reported with 'other revenues and losses' on the company's income statement.

D) One of two separate disclosures required is income or loss from the segment's operations from the beginning of the current accounting period to the date of disposal.

A) It relates primarily to product changes in a company.

B) The gain or loss associated with the disposal is shown separately as a component of continuing operations on the income statement.

C) It is reported with 'other revenues and losses' on the company's income statement.

D) One of two separate disclosures required is income or loss from the segment's operations from the beginning of the current accounting period to the date of disposal.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

36

Changes in accounting methods must be disclosed in three prominent places. These are

A) the auditor's report, financial statement notes, and the balance sheet.

B) financial statement notes, the income statement, and the auditor's report.

C) the balance sheet, the income statement, and the statement of cash flows.

D) notes to financial statements, the management letter, and the income statement.

A) the auditor's report, financial statement notes, and the balance sheet.

B) financial statement notes, the income statement, and the auditor's report.

C) the balance sheet, the income statement, and the statement of cash flows.

D) notes to financial statements, the management letter, and the income statement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

37

Diluted earnings per share

A) is required for companies that have the potential for liquidation.

B) is a financing and investing activity.

C) shows the effects of possible increases in the number of outstanding common shares.

D) is reported for the 'other revenues and expenses' category on the income statement.

A) is required for companies that have the potential for liquidation.

B) is a financing and investing activity.

C) shows the effects of possible increases in the number of outstanding common shares.

D) is reported for the 'other revenues and expenses' category on the income statement.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

38

Which one of the following should be NOT reported net of income taxes?

A) Loss from early extinguishment of long-term debt

B) Cumulative adjustments resulting from a change in depreciation methods

C) Bad debt expense associated with a bankrupt customer

D) Gains or loss from discontinuing the operations of a major segment of a business

A) Loss from early extinguishment of long-term debt

B) Cumulative adjustments resulting from a change in depreciation methods

C) Bad debt expense associated with a bankrupt customer

D) Gains or loss from discontinuing the operations of a major segment of a business

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

39

Management of Walker Corporation chose to classify its major losses as extraordinary items. Managers might be biased toward this approach because

A) investors do not use extraordinary items when predicting future performance.

B) this treatment reduces income taxes.

C) extraordinary losses are considered a good predictor of the company's future solvency.

D) extraordinary losses bypass net income and are reported directly as part of comprehensive income.

A) investors do not use extraordinary items when predicting future performance.

B) this treatment reduces income taxes.

C) extraordinary losses are considered a good predictor of the company's future solvency.

D) extraordinary losses bypass net income and are reported directly as part of comprehensive income.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

40

A company should report a cumulative effect of an accounting principle change when

A) consistency has been violated.

B) errors are made and subsequently corrected.

C) FASB mandates a change from one method to another.

D) international reporting standards differ from GAAP methods.

A) consistency has been violated.

B) errors are made and subsequently corrected.

C) FASB mandates a change from one method to another.

D) international reporting standards differ from GAAP methods.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

41

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before change in accounting principle?

a. $55,000

b. $60,000

c. $65,700

d. $42,160

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before change in accounting principle? a. $55,000

b. $60,000

c. $65,700

d. $42,160

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

42

The following are the revenue and expense accounts for the year ending August 31, 2009, for Hammer Corporation:

A. Calculate the amount of gross profit for Hammer Corporation for the year ending August 31, 2009.

B. How much should be reported as 'Other Revenues'?

A. Calculate the amount of gross profit for Hammer Corporation for the year ending August 31, 2009.B. How much should be reported as 'Other Revenues'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

43

Hamilton Corp. had the following infrequent income statement items during 2009:

$45,000 of dividends received from a stock investment

$20,000 gain on the sale of a plant asset which became outdated because of new technology

$19,000 loss due to the sale of treasury stock at a price less than its original cost

$34,000 fair value adjustment increase to market for available-for-sale investments

$50,000 interest expense for the year of which only $42,000 was actually paid

How much should Hamilton report as a component of 'income from continuing operations'?

$45,000 of dividends received from a stock investment

$20,000 gain on the sale of a plant asset which became outdated because of new technology

$19,000 loss due to the sale of treasury stock at a price less than its original cost

$34,000 fair value adjustment increase to market for available-for-sale investments

$50,000 interest expense for the year of which only $42,000 was actually paid

How much should Hamilton report as a component of 'income from continuing operations'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

44

The management of Hammer Enterprises shares in a bonus that is determined and paid at the end of each year. The amount of the bonus is based on 12% of net income from continuing operations after tax. The bonus is not used in the calculation of income from continuing operations. During 2010, Hammer was sued and was ordered to pay $480,000 over and above the amount covered by insurance. The loss is tax deductible and the company's tax rate is 35%. The company was last involved in a lawsuit five years ago. Net income from continuing operations before tax for 2010, excluding the lawsuit loss was $750,000.

What would management's 2010 bonus be if the lawsuit is considered unusual by not infrequent?

a. $175,500

b. $32,400

c. $21,060

d. $20,160

What would management's 2010 bonus be if the lawsuit is considered unusual by not infrequent?

a. $175,500

b. $32,400

c. $21,060

d. $20,160

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

45

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of net operating income?

a. $44,000

b. $60,000

c. $47,200

d. $52,700

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of net operating income? a. $44,000

b. $60,000

c. $47,200

d. $52,700

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

46

The following income statement was reported by Snappy Seacraft Company for the year ending December 31, 2010:

Assume Snappy has an average of 25,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

a. $0.12

b. $0.20

c. $0.08

d. $0.60

Assume Snappy has an average of 25,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment? a. $0.12

b. $0.20

c. $0.08

d. $0.60

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

47

The management of Hammer Enterprises shares in a bonus that is determined and paid at the end of each year. The amount of the bonus is based on 12% of net income from continuing operations. The bonus is not used in the calculation of income from continuing operations. During 2010, Hammer was sued and was ordered to pay $480,000 over and above the amount covered by insurance. The loss is tax deductible and the company's tax rate is 35%. The company was last involved in a lawsuit five years ago. Net income from continuing operations (before tax for 2010, excluding the lawsuit loss was $750,000.

What would management's 2010 bonus be if the lawsuit is considered extraordinary?

a. $90,000

b. $57,600

c. $32,400

d. $58,500

What would management's 2010 bonus be if the lawsuit is considered extraordinary?

a. $90,000

b. $57,600

c. $32,400

d. $58,500

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

48

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before extraordinary items and change in accounting principle?

a. $37,760

b. $60,000

c. $65,700

d. $52,700

What is the maximum amount of dividends Sunrise can pay if the covenant is expressed as 20 percent of income before extraordinary items and change in accounting principle? a. $37,760

b. $60,000

c. $65,700

d. $52,700

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

49

Gleeson Industries consists of four separate divisions: compressed wood products, chemicals, stone products, and plastics. On March 15, 2010, Gleeson sold the chemicals division for $625,000 cash. Financial information related to the chemicals division follows:

The journal entry to record the sale of the chemicals division will include:

a. a debit to Loss on Disposal of Business Segment for $175,000.

b. a debit to Assets for $1,850,000.

c . a debit to Extraordinary Gain for $175,000.

d. a credit to Gain on Disposal of Business Segment for $175,000.

The journal entry to record the sale of the chemicals division will include: a. a debit to Loss on Disposal of Business Segment for $175,000.

b. a debit to Assets for $1,850,000.

c . a debit to Extraordinary Gain for $175,000.

d. a credit to Gain on Disposal of Business Segment for $175,000.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

50

Gleeson Industries consists of four separate divisions: compressed wood products, chemicals, stone products, and plastics. On March 15, 2010, Gleeson sold the chemicals division for $625,000 cash. Financial information related to the chemicals division follows:

If the income tax rate for the company is 35%, what amount of income tax liability on the disposal of the business segment will be recognized?

a. $218,750

b. $61,250

c. $5,250

d. $157,500

If the income tax rate for the company is 35%, what amount of income tax liability on the disposal of the business segment will be recognized? a. $218,750

b. $61,250

c. $5,250

d. $157,500

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

51

Nigel Corporation reported income from continuing operations before taxes and before adjustment of the transactions below in the amount of $1,000,000. A review of the 2009 income statement revealed several items that appeared to be incorrectly categorized. The following items were flagged:

a. Recorded a loss of $29,000 due to a vandalism attack by a gang on one of the company warehouses; vandalism attacks have occurred at least once per year since the company began operations

b. Incurred an unusual and infrequent hurricane loss of $41,000 to a company warehouse

c. Closed all five of the company's supermarkets in Manhattan after bag boys went on strike for an extended period of time; shutdown expenses totaled $38,000

d. Floods from overflowing toilets on the upper floors of a downtown office building in Denver caused more than $8 million in repairs. Flooding toilets are rare in this area and have never occurred in office buildings in Denver before. Insurance coverage paid $8.6 million to replace the damaged portions of the building.

Nigel has a 30% tax rate. Calculate income from continuing operations. For any item that is NOT a component of continuing operations, state how it would be reported.

a. Recorded a loss of $29,000 due to a vandalism attack by a gang on one of the company warehouses; vandalism attacks have occurred at least once per year since the company began operations

b. Incurred an unusual and infrequent hurricane loss of $41,000 to a company warehouse

c. Closed all five of the company's supermarkets in Manhattan after bag boys went on strike for an extended period of time; shutdown expenses totaled $38,000

d. Floods from overflowing toilets on the upper floors of a downtown office building in Denver caused more than $8 million in repairs. Flooding toilets are rare in this area and have never occurred in office buildings in Denver before. Insurance coverage paid $8.6 million to replace the damaged portions of the building.

Nigel has a 30% tax rate. Calculate income from continuing operations. For any item that is NOT a component of continuing operations, state how it would be reported.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

52

On January 1, total assets and liabilities were $30,000 and $12,000, respectively. On December 31, total assets and liabilities were $28,000 and $20,000, respectively. During the year, $7,000 of dividends were declared and paid and no stock was purchased or issued. Calculate the amount of net income or loss for the year.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

53

The following income statement was reported by Snappy Seacraft Company for the year ending December 31, 2010:

Assume Snappy has an average of 15,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment?

a. $0.33

b. $0.20

c. $1.00

d. $0.73

Assume Snappy has an average of 15,000 shares of common stock outstanding during 2010. Based on this information, what amount of earnings per share would be reported on the income statement as the disposal of the business segment? a. $0.33

b. $0.20

c. $1.00

d. $0.73

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

54

Cabell Inc. reported 'income from operations before taxes' in the amount of $402,000 before including the following items for the year ending December 31, 2009:

On December 31, 2009, borrowed long-term debt of $50,000 that limits dividends to 10 percent of net income from continuing operations

$21,000 unrealized gain from fair value adjustment related to available-for-sale investments

$30,000 loss recognized on the sale of a trading security

$58,000 loss recognized on a lawsuit relating to patent violations

$11,000 government fine for environmental violation

$63,000 write-down of obsolete inventory

$25,000 loss on the early retirement of debt.

The company's income tax rate is 30 percent. No taxes have been considered in any information provided. Prepare a calculation of income from operations starting with income from operations before taxes, as tentatively reported. Omit the heading. Be sure to label correctly.

On December 31, 2009, borrowed long-term debt of $50,000 that limits dividends to 10 percent of net income from continuing operations

$21,000 unrealized gain from fair value adjustment related to available-for-sale investments

$30,000 loss recognized on the sale of a trading security

$58,000 loss recognized on a lawsuit relating to patent violations

$11,000 government fine for environmental violation

$63,000 write-down of obsolete inventory

$25,000 loss on the early retirement of debt.

The company's income tax rate is 30 percent. No taxes have been considered in any information provided. Prepare a calculation of income from operations starting with income from operations before taxes, as tentatively reported. Omit the heading. Be sure to label correctly.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

55

On January 1 and December 31, 2010, retained earnings were $23,000 and $42,000, respectively. During the year, the only dividends were an ordinary stock dividend recorded at $11,000. Calculate net income for 2010.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

56

The following information was taken from the 2010 financial records of Hopewell Company.

The company's income tax rate is 35 percent, and the items above are treated identically for the financial reporting and tax purposes.

REQUIRED:

Prepare an income statement using this information.

The company's income tax rate is 35 percent, and the items above are treated identically for the financial reporting and tax purposes.REQUIRED:

Prepare an income statement using this information.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

57

Wellman Inc., a computer manufacturer located in Texas, lost an uninsured building due to the infrequent and unusual occurrence of a hurricane. The building has a balance sheet value of $20,000 and will cost $165,000 to rebuild. Wellman's income tax rate is 40%. Calculate the amount of any extraordinary loss that should be reported on Wellman's income statement. Prepare a partial income statement that shows how the item will be presented.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

58

On January 1, total assets and liabilities were $21,000 and $8,000, respectively. On December 31, total assets and liabilities were $30,000 and $7,000, respectively. During the year, $9,000 of dividends were declared and paid and $3,000 of stock was issued. Calculate net income for the year.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

59

Makar Corporation reported net income before extraordinary items and taxes of $200,000 for the year 2010. During 2010, the average number of common shares outstanding was 35,000. Basic net earnings per share for 2010 are reported to be only $2.00. Makar's income tax rate is 30%. How much was Makar's extraordinary gain or loss (before tax) from a major earthquake? The earthquake was the only item that was reported net of tax in the income statement for 2010.

A) $70,000.

B) $100,000.

C) $130,000.

D) none of the above

A) $70,000.

B) $100,000.

C) $130,000.

D) none of the above

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

60

Sunrise Designs maintains a credit line with Ohio River Bank that allows the company to borrow up to $1 million. A covenant associated with the loan contract limits the company's dividends in any one year. The 2010 income statement data for the company is as follows:

What is the maximum amount of dividends Sunrise can pay if the covenant associated with the credit line is expressed as 20 percent of net income?

a. $55,000

b. $60,000

c. $52,560

d. $53,700

What is the maximum amount of dividends Sunrise can pay if the covenant associated with the credit line is expressed as 20 percent of net income? a. $55,000

b. $60,000

c. $52,560

d. $53,700

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

61

Identify the GAAP requirements of comprehensive income.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

62

Is consistency violated when a company changes accounting principles?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

63

Jarvis Company provided the following information for the year ending December 31, 2009:

Prepare an income statement in good form. You may omit the heading. Include all earnings per share amounts required for the year ending December 31, 2009.

Prepare an income statement in good form. You may omit the heading. Include all earnings per share amounts required for the year ending December 31, 2009. Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

64

Calculate how much should be reported on Nichol's income statement as 'Income from Continuing Operations' for the period ended December 31, 2009.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

65

Hubbell Service showed the following information for 2010: Net sales revenue, $410,000; interest revenue, $11,000; cost of goods sold, $220,000; operating expense, $15,000, extraordinary gain on retirement of debt, $30,000; and dividends declared, $14,000. Calculate operating income for 2010.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

66

Hilton Corporation's income statement for the year ending December 31, 2009, appears below. Compute the maximum amount of dividends Hilton can pay if it has a debt covenant expressed as 20 percent of net income, and as 20 percent of net operating income. Which amount would a creditor more likely use as the restriction on dividends? Explain.

Compute the maximum amount of dividends Hilton can pay if it has a debt covenant expressed as 20 percent of net income, and as 20 percent of net operating income. Which amount would a creditor more likely use as the restriction on dividends? Explain. Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

67

Identify types of transactions that are considered exchanges of liabilities and shareholders' equity. Why are these transactions considered 'financing'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

68

How are operating transactions that are not based primarily on the normal operations of a company reported on the financial statements?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

69

On January 1 and December 31, retained earnings were $40,000 and $53,000, respectively. During the year, $21,000 of dividends were declared. Calculate net income during the year.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

70

How do items at the top of the income statement differ from items at the bottom of the income statement?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

71

How much should be reported on the income statement for the year ended December 31, 2009 as 'Extraordinary Gains or Losses'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

72

What is the definition of a business segment and what special reporting is required for discontinued segments?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

73

Why are losses resulting from employee layoffs and write-downs such as inventory and receivables reported as 'other expenses and losses'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

74

The following are the revenue and expense accounts of the current year for ABCO Corporation:

All items are before income taxes. The income tax rate is 20%. Calculate any extraordinary gain or loss that should be disclosed on the income statement.

All items are before income taxes. The income tax rate is 20%. Calculate any extraordinary gain or loss that should be disclosed on the income statement. Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

75

How much should be reported on the income statement for the year ended December 31, 2009, as 'Cumulative Effect of a Change in Accounting Principle'?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

76

One of the three objectives of financial reporting directly relates to the income statement and measure of income. Indicate the context of this objective, and explain how it relates to the earnings process.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

77

The following are some accounts for Marvell Corp. for 2009:

All amounts are before income taxes. Marvell has a 30% tax rate. Determine the amount of Marvell' 'other revenue' and 'other expenses' for 2009. List all non-income statement items and indicate on which financial statement they are reported.

All amounts are before income taxes. Marvell has a 30% tax rate. Determine the amount of Marvell' 'other revenue' and 'other expenses' for 2009. List all non-income statement items and indicate on which financial statement they are reported. Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

78

Name the specific items for which Nichol Corp. must apply intraperiod tax allocation in its financial statements.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

79

Balance sheet information of Digital Solutions, Inc. at December 31, 2008, is provided below.

During 2009, the company entered into the following transactions:

A. Which transactions are operating?

B. Compute net income for the year ending December 31, 2009.

C. Compute comprehensive income for the year ending December 31, 2009.

During 2009, the company entered into the following transactions: A. Which transactions are operating?B. Compute net income for the year ending December 31, 2009.

C. Compute comprehensive income for the year ending December 31, 2009.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

80

The following information was taken from the accounting records of ABCO Corporation for the year ending December 31, 2009.

A. In good form, prepare the section of the income statement that begins immediately under 'income from continuing operations'. Do not be concerned with calculating the amount reported as 'income from continuing operations.'

B. List all the items that would appear in the 'Other Revenue/Other Expenses' section of the income statement.

C. How is the number of shares of common stock outstanding used on the income statement?

A. In good form, prepare the section of the income statement that begins immediately under 'income from continuing operations'. Do not be concerned with calculating the amount reported as 'income from continuing operations.'B. List all the items that would appear in the 'Other Revenue/Other Expenses' section of the income statement.

C. How is the number of shares of common stock outstanding used on the income statement?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 85 flashcards in this deck.