Deck 16: Quality of Earnings Cases: A Comprehensive Review

Full screen (f)

Question

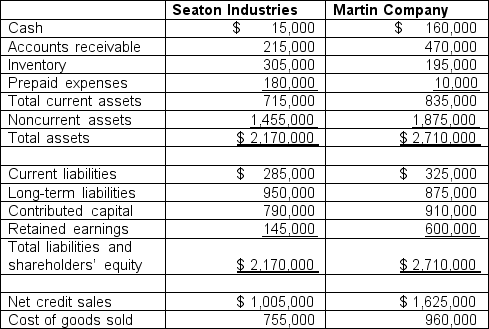

You have just been hired as a loan officer for Coastline Bank and Trust. Seaton Industries and Martin Company have both applied for $125,000 nine-month loans. It is the strict policy of the bank to have only $1,350,000 outstanding in unsecured loans at any point in time. Since the bank currently has $1,210,000 in unsecured loans outstanding it will be unable to grant loans to both companies. The bank president has given you the following selected information from the companies' loan applications.

Required: Assume that all account balances on the balance sheet are representative of the entire year. Based on this limited information, which company would you recommend to the bank president as the better risk for an unsecured loan? Support your answer with any relevant analysis, including examination of the current ratio, quick ratio, receivables turnover, and inventory turnover.

Required: Assume that all account balances on the balance sheet are representative of the entire year. Based on this limited information, which company would you recommend to the bank president as the better risk for an unsecured loan? Support your answer with any relevant analysis, including examination of the current ratio, quick ratio, receivables turnover, and inventory turnover. Question

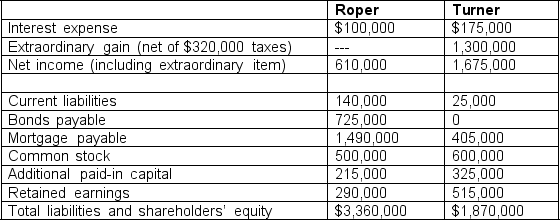

The following selected financial information was obtained from the 2010 financial reports of Roper Designs and Turner Industries:

Required:

Required: a. Assume that you are considering purchasing the common stock of one of these companies. (Since you have limited data, assume that the beginning balance sheet amounts equal ending balance sheet amounts for total assets and stockholders' equity.) Based on this information, which company has a higher return on equity? Would your conclusion be different if the impact of the extraordinary item had not been included in net income? Should the extraordinary item be considered? Why or why not?

b. Which company uses leverage more effectively? Does your answer change if you do not consider the impact of the extraordinary item on net income?

Question

When looking at the statement of comprehensive income in the 2009 annual reports of four similar companies in the same industry, you find the following:  Which company has an expense item that is likely to be persistent in terms of earnings?

Which company has an expense item that is likely to be persistent in terms of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

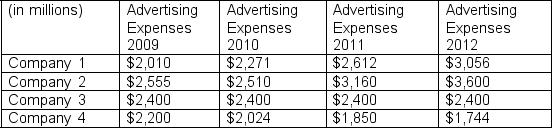

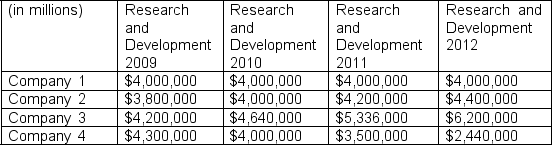

Solution C, because items that are expected to be persistent in terms of earning are those transactions like research and development costs, that are expected to be repeated in future years during the normal operation of the business. The other items, like a charge for disposal of a business segment, a provision for restructuring, and litigation charges, are all items that are not expected to occur again in future years.

Which company has an expense item that is likely to be persistent in terms of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution C, because items that are expected to be persistent in terms of earning are those transactions like research and development costs, that are expected to be repeated in future years during the normal operation of the business. The other items, like a charge for disposal of a business segment, a provision for restructuring, and litigation charges, are all items that are not expected to occur again in future years.

Question

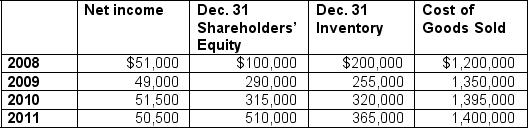

Parton Company began operation on January 1, 2008. The initial investment by the owners was $100,000. The following information was extracted from the company's records.

Required:

Required: a. Compute the return on equity for each year. (Assume a $0 inventory for January 1, 2008). Has the company been effective at managing the capital provided by the equity owners?

b. Does the information about inventory and the cost of goods sold indicate any reason for the trend in return on equity? Support your answer with any relevant ratios.

Question

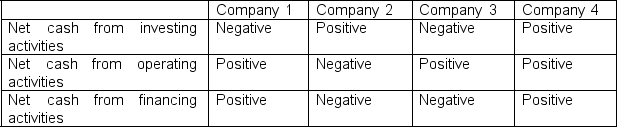

The following chart presents the cash flow profiles of four companies. All four companies are in the same industry and are comparable in size. Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Question

Question

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, and are competitors in the same market.  Based on this limited information, which company likely has the weakest quality of earnings?

Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution B, inventory changes are not in line with changes in sales.

Based on this limited information, which company likely has the weakest quality of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution B, inventory changes are not in line with changes in sales.

Question

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, are similar in size, and are competitors in the same market. The data cover Years 2009 to 2012.

Based on this limited information, which company likely has the weakest quality of earnings at Year 4 or 2012?

Based on this limited information, which company likely has the weakest quality of earnings at Year 4 or 2012?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Based on this limited information, which company likely has the weakest quality of earnings at Year 4 or 2012?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Question

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, and are comparable in size.  Based on this limited information, which company likely has the weakest quality of earnings?

Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

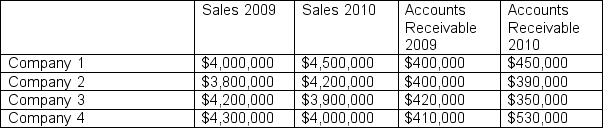

Solution D, accounts receivable changes are not in line with changes in sales, which are declining from 2009 to 2010.

Based on this limited information, which company likely has the weakest quality of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution D, accounts receivable changes are not in line with changes in sales, which are declining from 2009 to 2010.

Question

Question

The following information was taken from the 2009 annual reports of four different companies in the same industry.

Based on this limited data, which company appears to be more conservative and have stronger earning power?

Based on this limited data, which company appears to be more conservative and have stronger earning power?

a. Company 1

b. Company 2

c. Company 3

d. Company 4

Based on this limited data, which company appears to be more conservative and have stronger earning power? a. Company 1

b. Company 2

c. Company 3

d. Company 4

Question

Question

The following information is available on four different companies. All companies operate in the same industry, are of similar size, and use similar processes and equipment.  Based on this limited information, which company likely has the highest quality of earnings at the end of the three year period?

Based on this limited information, which company likely has the highest quality of earnings at the end of the three year period?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Based on this limited information, which company likely has the highest quality of earnings at the end of the three year period?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Question

The net income amounts for Box and Wood, Inc. over a four-year period is as follows:

After further examination of the financial report, you note that Box and Wood, Inc. made accounting method changes in 2008 and 2010, which affected net income in those periods. In 2008, the company changed depreciation methods. This change increased the book value of its fixed assets in each subsequent year by $10,000. In 2010, the company adopted a new inventory method that increased the book value of the inventory by $18,000.

After further examination of the financial report, you note that Box and Wood, Inc. made accounting method changes in 2008 and 2010, which affected net income in those periods. In 2008, the company changed depreciation methods. This change increased the book value of its fixed assets in each subsequent year by $10,000. In 2010, the company adopted a new inventory method that increased the book value of the inventory by $18,000.

Requirements:

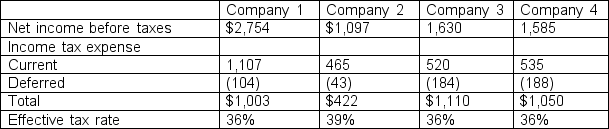

a. Calculate the effect of each of these changes on net income in the year of the change.

b. Prepare a chart that compares net income across the four-year period, assuming that Box and Wood, Inc. made no accounting changes. How would your assessment of the company's performance change after you learned of the accounting method changes?

c. What principle of financial accounting makes it difficult to make such changes? Describe the conditions under which Box and Wood, Inc. would be allowed to make changes in their accounting methods.

After further examination of the financial report, you note that Box and Wood, Inc. made accounting method changes in 2008 and 2010, which affected net income in those periods. In 2008, the company changed depreciation methods. This change increased the book value of its fixed assets in each subsequent year by $10,000. In 2010, the company adopted a new inventory method that increased the book value of the inventory by $18,000.Requirements:

a. Calculate the effect of each of these changes on net income in the year of the change.

b. Prepare a chart that compares net income across the four-year period, assuming that Box and Wood, Inc. made no accounting changes. How would your assessment of the company's performance change after you learned of the accounting method changes?

c. What principle of financial accounting makes it difficult to make such changes? Describe the conditions under which Box and Wood, Inc. would be allowed to make changes in their accounting methods.

Question

The following information is available on four different companies. Assume that there is no salvage value on the equipment. All companies operate in the same industry and use similar processes and equipment.  Based on this limited information, which company likely has the weakest quality of earnings?

Based on this limited information, which company likely has the weakest quality of earnings?

A) Morton

B) Starburst

C) Ames

D) Summers

Based on this limited information, which company likely has the weakest quality of earnings?A) Morton

B) Starburst

C) Ames

D) Summers

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/15

Play

Full screen (f)

Deck 16: Quality of Earnings Cases: A Comprehensive Review

1

You have just been hired as a loan officer for Coastline Bank and Trust. Seaton Industries and Martin Company have both applied for $125,000 nine-month loans. It is the strict policy of the bank to have only $1,350,000 outstanding in unsecured loans at any point in time. Since the bank currently has $1,210,000 in unsecured loans outstanding it will be unable to grant loans to both companies. The bank president has given you the following selected information from the companies' loan applications.

Required: Assume that all account balances on the balance sheet are representative of the entire year. Based on this limited information, which company would you recommend to the bank president as the better risk for an unsecured loan? Support your answer with any relevant analysis, including examination of the current ratio, quick ratio, receivables turnover, and inventory turnover.As a loan officer, there should be concern about the potential borrower's ability to meet its debts as they come due. Since both companies are requesting only nine-month loans, you should be interested in the potential borrowers' short-term solvency. Therefore, you would examine their current ratios and quick ratios. Further, you would consider the effect of the potential loan on these ratios. The current ratio is calculated as current assets divided by current liabilities.  It appears that both companies have more than sufficient current assets to meet their current obligations, including the new loan. However, some current assets, such as prepaid expenses and inventory, are not near-cash assets. Thus, a better measure of a potential borrower's ability to meet its current obligations is the quick ratio. This ratio is calculated as the sum of cash, marketable securities, and accounts receivable divided by current liabilities. Again, the effect of the new loan should be considered.

It appears that both companies have more than sufficient current assets to meet their current obligations, including the new loan. However, some current assets, such as prepaid expenses and inventory, are not near-cash assets. Thus, a better measure of a potential borrower's ability to meet its current obligations is the quick ratio. This ratio is calculated as the sum of cash, marketable securities, and accounts receivable divided by current liabilities. Again, the effect of the new loan should be considered.  Based on the quick ratio, Martin appears to be a much better risk than Seaton. Martin has approximately 2.5 times more near-cash assets available than Seaton to meet its current obligations. Therefore, Martin does not have to rely as heavily on converting other assets to cash as Seaton does to meet its obligations. The company that can most readily convert its inventory and receivables to cash might be the better risk. Two possible measures of a company's ability to generate cash from its receivables and inventory are the turnover and number-of-days ratios. Receivables turnover is calculated as net credit sales divided by average accounts receivable, and the number of days for receivables is calculated as 365 divided by the receivables turnover.

Based on the quick ratio, Martin appears to be a much better risk than Seaton. Martin has approximately 2.5 times more near-cash assets available than Seaton to meet its current obligations. Therefore, Martin does not have to rely as heavily on converting other assets to cash as Seaton does to meet its obligations. The company that can most readily convert its inventory and receivables to cash might be the better risk. Two possible measures of a company's ability to generate cash from its receivables and inventory are the turnover and number-of-days ratios. Receivables turnover is calculated as net credit sales divided by average accounts receivable, and the number of days for receivables is calculated as 365 divided by the receivables turnover.

Receivables turnover: Number of days:

Number of days:  These ratios indicate that Seaton, on average, collects its receivables 27 days quicker than Martin. Therefore, Seaton can more easily convert its receivables to cash than Martin can.

These ratios indicate that Seaton, on average, collects its receivables 27 days quicker than Martin. Therefore, Seaton can more easily convert its receivables to cash than Martin can.

Inventory turnover is calculated as cost of goods sold divided by average inventory, and the number of days is calculated as 365 divided by inventory turnover.

Inventory turnover: Number of days:

Number of days:  These ratios bode well for Martin. Martin sells its inventory, on average, 73 days sooner than Seaton sells its inventory. This difference implies that Martin generates more sales which, in turn, implies that it generates more accounts receivable. Although Martin does not turn over its receivables as often as Seaton, it has a larger amount of receivables to turn over. Thus, Martin potentially has more assets that can easily be converted into cash than Seaton.

These ratios bode well for Martin. Martin sells its inventory, on average, 73 days sooner than Seaton sells its inventory. This difference implies that Martin generates more sales which, in turn, implies that it generates more accounts receivable. Although Martin does not turn over its receivables as often as Seaton, it has a larger amount of receivables to turn over. Thus, Martin potentially has more assets that can easily be converted into cash than Seaton.

Based upon Martin's superior quick ratio and potential ability to generate cash from its larger receivables base, the recommendation should be that the bank grants the loan to Martin.

BT: AN

It appears that both companies have more than sufficient current assets to meet their current obligations, including the new loan. However, some current assets, such as prepaid expenses and inventory, are not near-cash assets. Thus, a better measure of a potential borrower's ability to meet its current obligations is the quick ratio. This ratio is calculated as the sum of cash, marketable securities, and accounts receivable divided by current liabilities. Again, the effect of the new loan should be considered. Based on the quick ratio, Martin appears to be a much better risk than Seaton. Martin has approximately 2.5 times more near-cash assets available than Seaton to meet its current obligations. Therefore, Martin does not have to rely as heavily on converting other assets to cash as Seaton does to meet its obligations. The company that can most readily convert its inventory and receivables to cash might be the better risk. Two possible measures of a company's ability to generate cash from its receivables and inventory are the turnover and number-of-days ratios. Receivables turnover is calculated as net credit sales divided by average accounts receivable, and the number of days for receivables is calculated as 365 divided by the receivables turnover.Receivables turnover:

Number of days: These ratios indicate that Seaton, on average, collects its receivables 27 days quicker than Martin. Therefore, Seaton can more easily convert its receivables to cash than Martin can.Inventory turnover is calculated as cost of goods sold divided by average inventory, and the number of days is calculated as 365 divided by inventory turnover.

Inventory turnover:

Number of days: These ratios bode well for Martin. Martin sells its inventory, on average, 73 days sooner than Seaton sells its inventory. This difference implies that Martin generates more sales which, in turn, implies that it generates more accounts receivable. Although Martin does not turn over its receivables as often as Seaton, it has a larger amount of receivables to turn over. Thus, Martin potentially has more assets that can easily be converted into cash than Seaton.Based upon Martin's superior quick ratio and potential ability to generate cash from its larger receivables base, the recommendation should be that the bank grants the loan to Martin.

BT: AN

2

The following selected financial information was obtained from the 2010 financial reports of Roper Designs and Turner Industries:

Required: a. Assume that you are considering purchasing the common stock of one of these companies. (Since you have limited data, assume that the beginning balance sheet amounts equal ending balance sheet amounts for total assets and stockholders' equity.) Based on this information, which company has a higher return on equity? Would your conclusion be different if the impact of the extraordinary item had not been included in net income? Should the extraordinary item be considered? Why or why not?

b. Which company uses leverage more effectively? Does your answer change if you do not consider the impact of the extraordinary item on net income?

a. Return on Equity = Net Income ÷ Average Stockholders' Equity ![a. Return on Equity = Net Income ÷ Average Stockholders' Equity Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity. b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage. Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1% Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9% From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be: Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294 Therefore, the financial leverage of the two companies would be: If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings. BT: AN](https://storage.examlex.com/TB5406/11eb49ea_7404_f939_ae87_95860832b37d_TB5406_00.jpg) Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be:

Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: ![a. Return on Equity = Net Income ÷ Average Stockholders' Equity Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity. b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage. Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1% Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9% From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be: Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294 Therefore, the financial leverage of the two companies would be: If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings. BT: AN](https://storage.examlex.com/TB5406/11eb49ea_7405_204a_ae87_fd7235deb323_TB5406_00.jpg) Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity.

Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity.

b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage.

Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets

Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1%

Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9%![a. Return on Equity = Net Income ÷ Average Stockholders' Equity Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity. b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage. Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1% Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9% From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be: Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294 Therefore, the financial leverage of the two companies would be: If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings. BT: AN](https://storage.examlex.com/TB5406/11eb49ea_7405_204b_ae87_db083c6a2024_TB5406_00.jpg) From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be:

From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be:

Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211

Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294

Therefore, the financial leverage of the two companies would be:![a. Return on Equity = Net Income ÷ Average Stockholders' Equity Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity. b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage. Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1% Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9% From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be: Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294 Therefore, the financial leverage of the two companies would be: If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings. BT: AN](https://storage.examlex.com/TB5406/11eb49ea_7405_204c_ae87_f9202fef13b6_TB5406_00.jpg) If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings.

If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings.

BT: AN

Based on return on equity, Turner is almost twice as efficient as Roper at managing the shareholders' capital. If unusual items were not considered, return on equity for each company would be: Turner now appears to be considerably worse than Roper at managing the stockholders' capital. Including unusual items in calculating return on equity does provide a more complete measure of how efficiently a company managed its stockholders' equity in the current year. However, since unusual items are, by definition, items that occur infrequently, these items do not indicate a company's continued ability to efficiently manage the stockholders' capital. Thus, unusual items probably should not be used to calculate return on equity.b. Financial leverage indicates how effectively a company uses debt for the benefit of stockholders. Financial leverage equals return on equity less return on assets. Thus, return on assets must be calculated before calculating financial leverage.

Return on Assets = (Net Income + Interest Expense (net of tax)) ÷ Average Total Assets

Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211 or 21.1%

Turner: ($1,675,000 + $175,000) ÷ [($1,870,000 + $1,870,000) ÷ 2] = 0.989 or 98.9%

From this analysis, Roper is approximately twice as effective as Turner at using debt to generate returns for its stockholders. If unusual items are not considered, the return on assets for each company would be:Roper: ($610,000 + $100,000) ÷ [($3,360,000 + $3,360,000) ÷ 2] = 0.211

Turner: [($1,675,000 - $1,300,000) + $175,000] ÷ [($1,870,000 + $1,870,000)÷2]= 0.294

Therefore, the financial leverage of the two companies would be:

If extraordinary items are not considered, Turner has negative financial leverage. That means that Turner is not generating a large enough return on its debt to even cover the interest expense. Thus, Turner is using debt to the detriment of its stockholders. It appears, therefore, that extraordinary items can affect the conclusions one draws when analyzing a company and its quality of earnings.BT: AN

3

When looking at the statement of comprehensive income in the 2009 annual reports of four similar companies in the same industry, you find the following: Which company has an expense item that is likely to be persistent in terms of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution C, because items that are expected to be persistent in terms of earning are those transactions like research and development costs, that are expected to be repeated in future years during the normal operation of the business. The other items, like a charge for disposal of a business segment, a provision for restructuring, and litigation charges, are all items that are not expected to occur again in future years.

Which company has an expense item that is likely to be persistent in terms of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution C, because items that are expected to be persistent in terms of earning are those transactions like research and development costs, that are expected to be repeated in future years during the normal operation of the business. The other items, like a charge for disposal of a business segment, a provision for restructuring, and litigation charges, are all items that are not expected to occur again in future years.

C

4

Parton Company began operation on January 1, 2008. The initial investment by the owners was $100,000. The following information was extracted from the company's records.

Required: a. Compute the return on equity for each year. (Assume a $0 inventory for January 1, 2008). Has the company been effective at managing the capital provided by the equity owners?

b. Does the information about inventory and the cost of goods sold indicate any reason for the trend in return on equity? Support your answer with any relevant ratios.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

5

The following chart presents the cash flow profiles of four companies. All four companies are in the same industry and are comparable in size. Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

6

Xenon, a major defense contractor, was faced with huge liabilities and feared violation of debt covenants. Therefore, Xenon declared Chapter 11 bankruptcy protection. Under Chapter 11, a company continues to operate but is protected from creditors while it tries to work out a reorganization plan. At that time the company's management chose to take several significant charges under bankruptcy proceedings, including a $1 million liability not required by GAAP, but that better reflected its commitments to employees.

Required:

Why would Xenon's management have chosen to take these charges at this time?

Required:

Why would Xenon's management have chosen to take these charges at this time?

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

7

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, and are competitors in the same market. Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution B, inventory changes are not in line with changes in sales.

Based on this limited information, which company likely has the weakest quality of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution B, inventory changes are not in line with changes in sales.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

8

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, are similar in size, and are competitors in the same market. The data cover Years 2009 to 2012. Based on this limited information, which company likely has the weakest quality of earnings at Year 4 or 2012?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Based on this limited information, which company likely has the weakest quality of earnings at Year 4 or 2012?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

9

The following information is presented from the financial statement of four companies that operate in the same industry, use similar processes, and are comparable in size. Based on this limited information, which company likely has the weakest quality of earnings?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution D, accounts receivable changes are not in line with changes in sales, which are declining from 2009 to 2010.

Based on this limited information, which company likely has the weakest quality of earnings?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Solution D, accounts receivable changes are not in line with changes in sales, which are declining from 2009 to 2010.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

10

You are reviewing the annual report for Mega City Electronics. You noticed that Mega City cut its dividend last year and the stock price when up.

Required: Explain how a dividend cut could lead to an increased stock price.

Required: Explain how a dividend cut could lead to an increased stock price.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

11

The following information was taken from the 2009 annual reports of four different companies in the same industry.

Based on this limited data, which company appears to be more conservative and have stronger earning power?

a. Company 1

b. Company 2

c. Company 3

d. Company 4

Based on this limited data, which company appears to be more conservative and have stronger earning power? a. Company 1

b. Company 2

c. Company 3

d. Company 4

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

12

Carlton Electronics posted net income of $500,000 in 2009, compared with a loss of $100,000 in 2008. Over $200,000 of the 2009 profit was due to a problem with faulty approximation in its Toledo operations. The problem occurred when a tax liability had been accrued in prior years assuming a higher tax rate that was actually in effect when the taxes were paid.

Required:

How do you interpret this in terms of quality of earnings? How can a change in expected tax rates lead to a positive effect on reported earnings? Does the $200,000 represent an increase in overall wealth of the company?

Required:

How do you interpret this in terms of quality of earnings? How can a change in expected tax rates lead to a positive effect on reported earnings? Does the $200,000 represent an increase in overall wealth of the company?

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

13

The following information is available on four different companies. All companies operate in the same industry, are of similar size, and use similar processes and equipment. Based on this limited information, which company likely has the highest quality of earnings at the end of the three year period?

A) Company 1

B) Company 2

C) Company 3

D) Company 4

Based on this limited information, which company likely has the highest quality of earnings at the end of the three year period?A) Company 1

B) Company 2

C) Company 3

D) Company 4

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

14

The net income amounts for Box and Wood, Inc. over a four-year period is as follows:

After further examination of the financial report, you note that Box and Wood, Inc. made accounting method changes in 2008 and 2010, which affected net income in those periods. In 2008, the company changed depreciation methods. This change increased the book value of its fixed assets in each subsequent year by $10,000. In 2010, the company adopted a new inventory method that increased the book value of the inventory by $18,000.

Requirements:

a. Calculate the effect of each of these changes on net income in the year of the change.

b. Prepare a chart that compares net income across the four-year period, assuming that Box and Wood, Inc. made no accounting changes. How would your assessment of the company's performance change after you learned of the accounting method changes?

c. What principle of financial accounting makes it difficult to make such changes? Describe the conditions under which Box and Wood, Inc. would be allowed to make changes in their accounting methods.

After further examination of the financial report, you note that Box and Wood, Inc. made accounting method changes in 2008 and 2010, which affected net income in those periods. In 2008, the company changed depreciation methods. This change increased the book value of its fixed assets in each subsequent year by $10,000. In 2010, the company adopted a new inventory method that increased the book value of the inventory by $18,000.Requirements:

a. Calculate the effect of each of these changes on net income in the year of the change.

b. Prepare a chart that compares net income across the four-year period, assuming that Box and Wood, Inc. made no accounting changes. How would your assessment of the company's performance change after you learned of the accounting method changes?

c. What principle of financial accounting makes it difficult to make such changes? Describe the conditions under which Box and Wood, Inc. would be allowed to make changes in their accounting methods.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

15

The following information is available on four different companies. Assume that there is no salvage value on the equipment. All companies operate in the same industry and use similar processes and equipment. Based on this limited information, which company likely has the weakest quality of earnings?

A) Morton

B) Starburst

C) Ames

D) Summers

Based on this limited information, which company likely has the weakest quality of earnings?A) Morton

B) Starburst

C) Ames

D) Summers

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 15 flashcards in this deck.